📖 Venture Chronicles - April 2023

Overlooked #145

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of April.

For 2023, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for April!

Saturday, Apr. 1st: Tidemark wrote about the need for SaaS companies to offer multi-products. - Tidemark

“SaaS, as we know it, is dead. The single-point solution companies, hooked to a never-ending sales and marketing dollars treadmill, are doomed.”

“We believe there’s an opportunity for multi-product SaaS companies to create what we call Platforms of Compounding Greatness, or PCG. The key difference is offering multiple products that work better in partnership.”

To become a successful multi-products company, you need to start with a “control point” (i.e. a product owning crucial data or a crucial workflow for your customer). You will expand from there into 4 directions: (i) following business workflows, (ii) following the money, (iii) becoming the single source of truth of your customers, (iv) enriching your customer data with additional data.

“Cross-compounding allows companies to even escape the bounds of a single customer set. PCG offers a bigger TAM and improved incremental economics, and they are also worth a lot more money.”

Sunday, Apr. 2nd: Justin Gage at Technically wrote about databases. - Technically

“Many databases are designed with specific types or shapes of data in mind”. […] The real reason why the data type matters is not the actual storage of the data – remember, you can store anything anywhere – it’s the insertion and retrieval of the data.”

Justin differentiates (i) user facing databases (used for the core data in your app, data constantly used, high integrity and speed required), (ii) analytical databases (used for analytics and data science, large and complex queries, data used less frequently) and (iii) operational databases (monitoring internal operations).

Monday, Apr. 3rd: Logan Bartlett at Redpoint shared the market update he presented to Redpoint’s LPs during their Annual General Meeting. - Logan Bartlett

Tuesday, Apr. 4th: Stripe published its annual letter. - Stripe

Stripe processed $817bn in transactions in 2022 (26% annual growth). The number of customers on Stripe grew by 19% YoY (1k new companies per day, 55% outside the US). In 2022, 1/10 people in the world transacted with a business powered by Stripe.

“An important but little-reported fact is that the population-wide propensity to start a business appears to have increased significantly and persistently since the onset of the COVID pandemic. […] According to the US Census , the rate of business formation has increased by 44% since 2019. Delaware, similarly, saw 24% more incorporations in 2022 than in 2019.”

Stripe is releasing more no-code products (e.g. Payment Links, Stripe Billing’s customer portal, revenue recovery). It’s an evolution in Stripe’s model which was mostly focused on API-first products.

Wednesday, Apr. 5th: Scopely was acquired by Saudi Arabia for $4.9bn. More precisely by Savvy Games which is part of Saudi Arabia’s Public Investment Fund. Scopely is a leading mobile game developer/publisher and raised its previous round in 2020 at a $3.3bn valuation. Previously, Savvy Games had acquired other gaming assets including Faceit and ESL. It had also invested in public companies like Nintendo, Tencent and Activision Blizzard. Saudi Arabia plans to invest $38bn into the gaming sector to become the top gaming hub for Middle-East and Africa. - Bloomberg, Techcrunch, Savvy Games

Thursday, Apr. 6th: Lux Capital is another fund refocusing its investment strategy and reducing the amount it was planning to raise. In fact, Lux is back on the market to raise a new $1bn fund and it decided not to raised a dedicated vehicle for growth stage opportunities. The new fund will be primarily focused on early stage with the possibility to keep investing at growth stage. - Techcrunch

Friday, Apr. 7th: a16z wrote a blog post on building a vertical operating system. - a16z

a16z defines an operating system as a “unique and valuable system of record” which is most of the time recording the “foundational customer unit of the business” (e.g. Salesforce).

“A system of record runs a portion of a business, while a vertical operating system runs the entire business.” When you build a vSaaS, you should be the system of record for the entire business and not only the system of record for one piece of the business (e.g. Toast vs. Quickbooks).

“One of our favorite aspects of vertical operating systems is that they can add products and services to shrink the total addressable market of their horizontal competitors, while also increasing their own addressable market.”

“Almost all vertical operating systems start with a best-in-class wedge product that creates a system of record around the foundational customer unit. And then, from that initial foothold, the company launches other products and services that capture more and more of the employee workflow.”

Saturday, Apr. 8th: Social Capital published its annual letter for 2022. - Chamath Palihapitiya

“We believe there has been a common theme that has defined our work over the past 12 years: partnering with ambitious, independent thinkers who as founders are building companies from first principles.”

“As we enter a sustained period of non-zero interest rates, discipline of mission must now also intersect with discipline of management and operation. Efficiency, risk management, business model fundamentals, and most importantly, sustained profitability, are must-haves – not nice-to-haves.”

“While the previous market regime rewarded growth at any cost, the message to companies has now taken a u-turn. Our advice to founders: profits and cash flows matter again, and growth must be balanced with attractive margins to create sustainable business models that will endure the test of time.”

“VC portfolios are now impaired – the extent of which is debatable but meaningful. The best VCs will take the medicine of markdowns early. It will allow them to preserve credibility with their limited partners while also showing leadership to their portfolio companies to show alignment and long-term thinking. If they don’t do this hard work now, they will create a long-term reputational risk by allowing founders to meander in this critical moment while they try to maintain fake performance metrics.”

Sunday, Apr. 9th: I listened to a How I Got Here’s podcast episode with Richard Valtr who is Mews’ founder. Mews is a modern property management system for independent hotels and small hotel chains. - How I Got Here

“I started Mews back in 2012 while I was building a hotel in the centre of Prague which is where I'm from. I thought that creating this entire operating system for hotels would be as easy as building an hotel without a reception desk like I was building at the time. I thought the PMS part of it would take about a year to do and nine years later, I’m still struggling to do it.”

Richard Valtr’s mother developed properties and hotels in Czechoslovakia after the second World War. Richard used to spend his summer holidays as a night receptionist. Richard studied and worked in London in the film industry. His mom asked him to work in the family business for a couple of years. He seized the opportunity and built an hotel from scratch.

“The first idea for Mews was a guest-facing app that would link visitors to the hotel to the actual staff. It was a way for everyone to feel that even though you're in a big hotel you have that kind of intimacy to a host. It was a platform where the guests could personalize their stay (e.g. all the things they wanted to do in the city in which they were, all the ways they wanted to be served). On the other side, it would be a task management software communicating with the PMS to be able to have this personalisation at scale.”

“At the time, PMS providers told me that it was impossible to link my app to their system because there was no open API or that I would have to sign a six-figures check to do a special integration project with them. It pushed me to build my own PMS.”

Incumbent solutions’ architectures are unsuited. PMS like Oracle are room centric when Mews wants to build a guest centric PMS. CRS like Sabre don’t care about what happens on the property once a reservation is made. Also, several big players in the industry failed to build and distribute their own PMS - like Sabre who spent $100m on a PMS project.

Mews struggled with building a sufficiently mature product because the PMS is a complex piece of software. It’s an hotel record system and it has to take into account for local market specificities (e.g. accounting, travel taxes) while selling across the world.

Mews found a first niche in the hospitality market with hostels which like low-cost airlines needed to have a system with enough flexibility to unbundle and re-bundle the hospitality offering (e.g. pay extra to have a private room and/or bathroom) when most hotels have standardised and bundled offering (with services always included liked a bed, table, bathroom and wardrobe).

Mews was the first player in the hospitality tech sector to have an open API and an API-first product. The hospitality tech industry was super closed before which was massively slowing down the innovation in the sector. Incumbents did not want to open their systems because it would have jeopardised their cash flows.

“I've probably knocked on the doors of every single VC in Europe at least three to four times. It was mainly because of the fact that what we were doing is quite large and investors don’t love travel.”

“We ended up just basically bootstrapping [instead of raising with poor deal terms or with investors we did not want]. We invented this thing where we would share our product roadmap with our initial customers and tell them that we could prioritize certain features if they paid us $10k per feature.”

Mews is a Payment Facilitator (PayFac). “A lot of the problems that you have within hotels are kind of fintech problems.” For instance, at checkin, you need to authenticate the person coming through the door which is something you do with his credit card. In 2014, Mews integrated Braintree and built a payment infrastructure close to what a Shopify is building on top of Stripe for its merchants. Mews can be described as a Shopify for hotels.

Monday, Apr. 10th: Lux raised $1.15bn for Lux Ventures VIII to invest from incubation to pre-IPOs with tickets from $100k to $100m. - Lux

“We’re emphasizing lots of early-stage activity and many themes including inner space (breakthrough biology + technology), outer space (manufacturing + aerospace + defense), and latent space (the magic of AI models + computational infrastructure).”

“While we consistently partner with early-stage founders, we also futureform by creating entirely new advanced technology ventures from scratch that should exist and don’t yet. Through our internal Lux Labs program, we have incepted dozens of new companies across a wide array of emerging technology areas and brought them to market.”

“Like the founders we back, we too have a forever chip on our shoulder, a constant reminder to maintain our scrappy roots with fiery competitiveness and heightened intensity to futureform and create the world we want to live in.”

Tuesday, Apr. 11th: Graneet raised a $8.7m series A co-led by existing investors P9 and Foundamental. Graneet is a vSol for the construction industry, building a mini ERP for small construction companies. It started in financial management before expanding into expense management. It focuses on helping small construction companies improve their margins in a low-margin industry and in an industry drastically impacted by recent macro shift (increase in raw materials, supply chain disruption). Graneet tripled its revenues in the past 6 months and works with several hundreds of customers. It will use the funding to expand its product suite with new finance related modules, to accelerate distribution and to expand internationally. - Techcrunch, Louis Coppey, Batiweb

Wednesday, Apr. 12th: AutoLeap raised a $30m series B led by Advance Venture Partners. It’s a vSol for auto repair shops competing directly with Shopmonkey that I previously covered in this newsletter. Using AutoLeap, car repair shops manage to increase their sales by 30% and reduce the time they spend on admin tasks by 50%. 90% of auto repair shops are using archaic technology (spreadsheets and clunky invoicing tools). It will use the funding to grow its team as well as to invest in product development and customer support. - Techcrunch, AutoLeap

Thursday, Apr. 13th: Thynk raised a $13m series A led by Singular with the participation of a solo GP fund managed by Itai Tsiddon and CNP. Thynk is a vSol for hotels building a CRM for hotel chains to manage the B2B side of their business (e.g. when a company books a seminar). It works with hotel brands all over the world including Postillion (Netherlands), Rotana (UAE), Groupe Lucien Barrière (France), Design Hotels (Germany) or Mint House (US). Like Veeva and nCino, Thynk is built on top of Salesforce and targets enterprise customers in its industry. Moreover, Thynk acts as a middleware connecting the IT stack of the different properties (PMS and POS) into a single system of records that can be activated at the hotel chain HQ. - Thynk, Techcrunch

Friday, Apr. 14th: Alex Niehenke from Scale wrote about the 3 most common objections people have when looking at vertical SaaS (small TAM, low buyers’ willingness to digitise, hard to penetrate). - Scale

“Oracle's Cerner alone does over $5bn sales annually selling hospital software in what some estimate to be a +$30bn software market.” “Chase spends $14bn (11% of revenue) annually on technology.”

“Some verticals are difficult to penetrate because of regulations or other industry-specific factors that raise the barrier to entry. One of the simplest barriers is a shortage of people who have deep knowledge of the problems facing the industry, and therefore the ability to solve them - i.e. founder-market fit.”

“The tight networks of buyers within these segments create informal referral networks that drives new business. In short, if a startup creates a positive experience for their first customer, there’s a good chance their next wave of customers is a direct intro away.”

“Founders in vertical SaaS generally come from within the industries they’re building for and bring deep domain expertise with them. The sense I’ve gotten from these founders over the years is frustration with an investment market that is willing to throw 100X multiples at horizontal SaaS while insisting that startups in vertical segments aren’t venture scalable.”

Saturday, Apr. 15th: I listened to a Tim Ferriss’ podcast episode with Luis von Ahn who is Duolingo’s founder and CEO. - Tim Ferriss

“The easiest way to make money when you’re teaching somebody is just to charge them to learn. That’s how education monetizes. It was very important for us that we didn’t do that, because the mission of our company was really related to giving access to education to everybody for free.”

“In the end, we ended up finding a monetization model that worked out really well, which is this freemium model that is similar to what the dating apps do, or what Spotify does, which is you don’t have to pay, but you may have to see some ads at the end of a lesson. We make money from the ads. If you don’t like the ads, you can pay us to subscribe to a premium version of Duolingo, and then we turn off the ads, and we give you a few extra perks.”

“Something like 97% of our active users use Duolingo for free. Still, we make more money than all other education apps. We’re very proud of that.”

“It’s like the whole company was basically against monetizing. It took us about six months to finally convince everybody that monetization was not a bad thing, and that, in reality, what it would allow if we could make a lot of money, we could use that to invest it and to teach better.”

“Our employee churn is very low. Employees stay for a very long time at Duolingo. So the majority of people that started at Duolingo 10 years ago, they’re still around.” “I think a lot of it has to do with the fact that we have a really good company culture, but also that we’re in Pittsburgh.”

Duolingo has two main categories of users.

“One big bucket, which is about, call it 50-60% of our users, is people learning English. These are people who are usually not in the US. They’re usually in a non-English speaking country, and they’re learning English. The reason they’re learning English is they actually need to learn English to get ahead in life. So either they want to get into a better educational institution or they just want to get a better job. The thing about English that is so magical is that anywhere you live, if you speak English, just by speaking English, you can make more money.”

“The other big bucket of people are people who are English speakers already who are learning another language. So think of this as a person in the US who’s learning Spanish or French, et cetera. They’re pretty different. It’s more of a hobby. […] The funny thing about these people is when you ask them, “What would you do if Duolingo went away?” The most common answer is, “I would spend more time on Instagram.” They’re not that committed.”

“In the US, 80% of our users were not learning a language before Duolingo.”

“I actually think that for the first 0 to 30 people, the best thing you can do as a CEO is to be a micromanager.” You have one unique goal which is to get to product market fit and “you should micromanage people to get to product market fit” because at this stage “you’re not in the business of coaching people”.

Duolingo has metric-based teams (e.g. time spent learning, retention) and not feature-based team (e.g. leaderboard). These teams must improve a single metric. They can impact all the aspect of the product and the GTM to improve this metric. At some point Duolingo had 40-50 metrics based teams and decided to gather them into areas (monetisation area including ad revenues per day or subscription revenue per day, time spent learning area, retention area).

1.5m DAUs have a streak on Duolingo that is longer than a year.

Duolingo is pushing for daily app usage for two main reasons. First, to learn a language, you need to build an habit and the most effective habits are daily. Second, daily usage enables Duolingo to be faster at iterating on product & distribution (faster results on AB tests if the timeline to get feedback is a day and not a week or a month).

Sunday, Apr. 16th: Ben Thompson interviewed Scott Belsky, Adobe’s Chief Strategy Officer. - Stratechery

Shifting the Adobe’s product suite to the cloud and to a subscription model enabled the company to upgrade the product every week (vs. every 18 months) and to democratise its products (e.g. $10 per month to access Photoshop vs. an expensive upfront fee).

“My view is that there are going to be more tools, not less, in the future, and that our market is expanding. We’re not just focused on core creative pros that went through design school and hold their skills of using Photoshop as stripes. It’s now a far broader audience of folks who want to be a part of this, non-pros and pros alike, which means that there need to be collaborative capabilities for all of these products, and so the view has been that if we can ensure that Adobe’s providing indispensable value to all of these folks, they don’t need to be on our first-party tool, they can be using third-party tools, as well.”

“A prompt is the new [design] template.”

“When I go and sit down with the CIOs of some of these big marketing conglomerates and they say they don’t want to use generative AI because they don’t want to attest to their customers that they use something that they weren’t allowed to train off of, and so we want to have commercially viable models, that’s one important thing for us. Number two is we want to make sure that we bring these into the tools that people are already using. For the vector thing, for example, it’s made to work with Illustrator. Also, what we’re doing in terms of bringing this technology into Photoshop, we’re allowing people to further edit the prompts and have the outputs be nondestructive so people can actually further edit with it, as opposed to just be stuck with whatever the prompt gives you.”

“There are creatives and there are creative directors, and [with generative AI] everyone’s becoming a creative director, not a creative.”

“Firefly is our family of generative AI models. We certainly have the classic text-to-image but we also have text styles, so you can actually, with any prompt, affect the style of fonts, which is something new that we brewed in the lab. And then we’ve also done a lot of work now around vector creation, text-to-vector creation, and also taking a sketch and then creating multiple vector options that you can then take and then have infinite points on Illustrator to further edit this vector.”

Today, marketing personalisation is based on segmentation. Tomorrow, marketing personalisation will be “based on creating a custom asset for every single person in my database based on what I know about them”.

“If we were only focused on bringing these generative AI capabilities into our tools, then we would get stuck, because you can only do so much of retrofitting and putting things into things. That’s why we’re try^ing to do both the AI-first creative approach, which is built out of Firefly as it is in the open today, as well as bring these capabilities into our tools, we have to play both.”

Monday, Apr. 17th: Every wrote about vertical labor marketplaces. - Every

A vertical labor marketplace is an online platform matching workers and employees with unique features built for a given industry going way beyond matching (e.g. helping recruiters track candidates in a recruitment funnel, issuing credit cards to employees, processing payroll, etc.).

There is a momentum for vertical labor marketplaces for 3 main reasons: (i) workers are leaving their job at an historically high rate, (ii) with the rise of remote work, employers are now willing to hire outside their city/country, (iii) there are massive labour shortage in certain industries (nursing, agriculture, skilled trades).

“Embedded finance makes it a lot easier for vertical labor marketplaces (and vertical software companies in general) to solve problems: initial wedge products are easier to build, and add-on products enable a single company to serve multiple needs. Instead of just a pure “matching” platform between workers and employers, you can imagine applicant tracking systems, benefits administration, compliance, payroll, payments, and other services that startups can now easily build.”

Tuesday, Apr. 18th: Woodoo raised a $31m seed round led by Lowercarbon to produce augmented wood. It replaces the lignin in the wood by other chemical elements to give it unique characteristics transforming the wood into a substitue for materials like steel and leather. Woodoo is working with customers like LVMH, Volkswagen or Garnica. It will use the funding to scale its commercial pipeline and its production capacities. - Techcrunch, Sifted

Wednesday, Apr. 19th: I listened to a podcast on the impact of generative AI on the gaming industry with Danny Lange who is SVP of AI at Unity Technologies. - Cross Validated

“[Generative AI] is a game changer. That's a fact. I would also admit, having been in this area for over two decades I keep getting amazed and surprised at the same time. Things are progressing much faster than than I thought that anyone thought.”

“There's no doubt that if we look at the graphical side first, it is tools like Midjourney and Stable Diffusion. The fact that you can create graphics that are awesome quality can be used directly in a game. That's already had a huge impact.”

About Unity’s AI marketplace.

“It's really a two-sided marketplace. It's also really important to take… the way that there are AI companies, there are startups out there who create this fantastic new technology. And it's a race and it's a competition to get it to the market. At the other end of the other side of the market, there's all, they're all the game developers. They're looking for productivity improvements. They're looking for new technology to dazzle their players. So what we are doing with this marketplace slash ecosystem is to make it easier for the startups, for the technology providers to meet their future customers, the game developers”

“It's a very important moment to be completely upfront here. At Unity, we have basically concluded that the developments are going so fast right now, we can't be the builders of all this. We need to bring the builders to our customers, the game developers, and that's what we are doing with this marketplace.”

Main challenge around implementing AI within Unity. “So the real challenge here is to bring [AI] to these developers without making them AI technology experts, but they have to be power users of it. So ease of use is really what matters here and bring value.“

“We are trying to go in and create something that virtually nobody has done before. […] You can write once and run on many different platforms and we are bringing that to the AI space.”

The importance of having a feedback loop. “A lot of people have noticed that Midjourney, the imagery they create gets better and it just improves. And I know a lot of people who spent all day using Midjourney to generate graphics content for game development. And at the same time, look at Stable Diffusion, the model distributed open source by Stability AI. It's sort of the same as it was two or three months ago. So the difference is that there's no feedback loop. You build a model in open source. You share it with the world. The world is happy, but then the world uses it and they don't actually make it better. So one of the most important elements here is what I would characterize as the network effect. […] That feedback loop, Midjourney gets it. The open source projects, they don't really get it.”

Thursday, Apr. 20th: Marie at Fly wrote a guide for founders who want to raise a $10m series funding round in 2023. - Marie Brayer

“Series A VC funds are growing in size reaching more than $500m, sometimes more than $1bn. To make the returns they need to deliver, they must find companies that have the possibility of reaching valuations of $5bn or more. If your startup’s potential valuation is capped too low, no one will touch it.”

There is a scissor effect in early stage venture: “VCs need to back €5B+ companies but it’s 4x harder to hit such lofty valuations”.

“With their pockets empty, a growing percentage of VC firms are simply not in a position to invest, and may not be for some time to come.”

“95% of the time it’s not productive to speak to an analyst/“investor”/associate/junior person at a big firm. Look at their LinkedIn profile to understand what they actually do besides their title. It is also not a positive signal if people with these profiles ping you between rounds. It’s their job to maintain the CRM. They are just checking a box. What matters is an intro to a general partner ideally or a partner (or someone who can make a deal).”

“The best possible outcome of a first meeting is: “Let’s book another meeting.” A 50/50 outcome is: “Oh, send us your data.’” Anything else, particularly compliments, is a pass.”

“A good funnel looks like this (modulo the waves we talked about): Overall, 40 relevant VCs in your list → you meet 30+ of them → 10 or more (ideally more) enter DD following a great first meeting → 5 survive the DD, →1–4 offer a term sheet → you pick one or two co-leads and complete with followers if needed. It usually takes at least five meetings to get a term sheet.”

Tips to make a great impression during the 1st meeting with a VC: (i) present a data-backed VC business case, (ii) be opinionated & present unique insights, (iii) talk about “your massive ambition”.

Friday, Apr. 21st: Tech companies continue to layoff their employees: (i) Clubhouse laid off 50% of its employees, (ii) Lyft 30% and (iii) Dropbox 16%. - Dropbox 1, Dropbox 2, Clubhouse, Lyft

Clubhouse

“As the world has opened up post-Covid, it’s become harder for many people to find their friends on Clubhouse and to fit long conversations into their daily lives.”

“It’s hard for teams to coordinate, people feel blocked by us, and brilliant, creative people are left underutilized. In order to fix this we need to reset the company, eliminate roles and take it down to a smaller, product-focused team.”

“We have a clear vision for what Clubhouse 2.0 looks like and we believe that with a smaller, leaner team we will be able to iterate faster on the details, build the right product and honor our teammates who helped us get here.”

Lyft

Lyft could reduce its costs by 50%. It’s Lyft second wave of layoffs (1.2k employees impacted vs. 700 for the 1st wave).

“We need to bring our costs down to deliver affordable rides, compelling earnings for drivers, and profitable growth.”

Dropbox

“While our business is profitable, our growth has been slowing. Part of this is due to the natural maturation of our existing businesses, but more recently, headwinds from the economic downturn have put pressure on our customers and, in turn, on our business.”

“The AI era of computing has finally arrived. We’ve believed for many years that AI will give us new superpowers and completely transform knowledge work. […] In an ideal world, we’d simply shift people from one team to another. And we’ve done that wherever possible. However, our next stage of growth requires a different mix of skill sets, particularly in AI and early-stage product development.”

“I’m determined to ensure that Dropbox is at the forefront of the AI era, just as we were at the forefront of the shift to mobile and the cloud.”

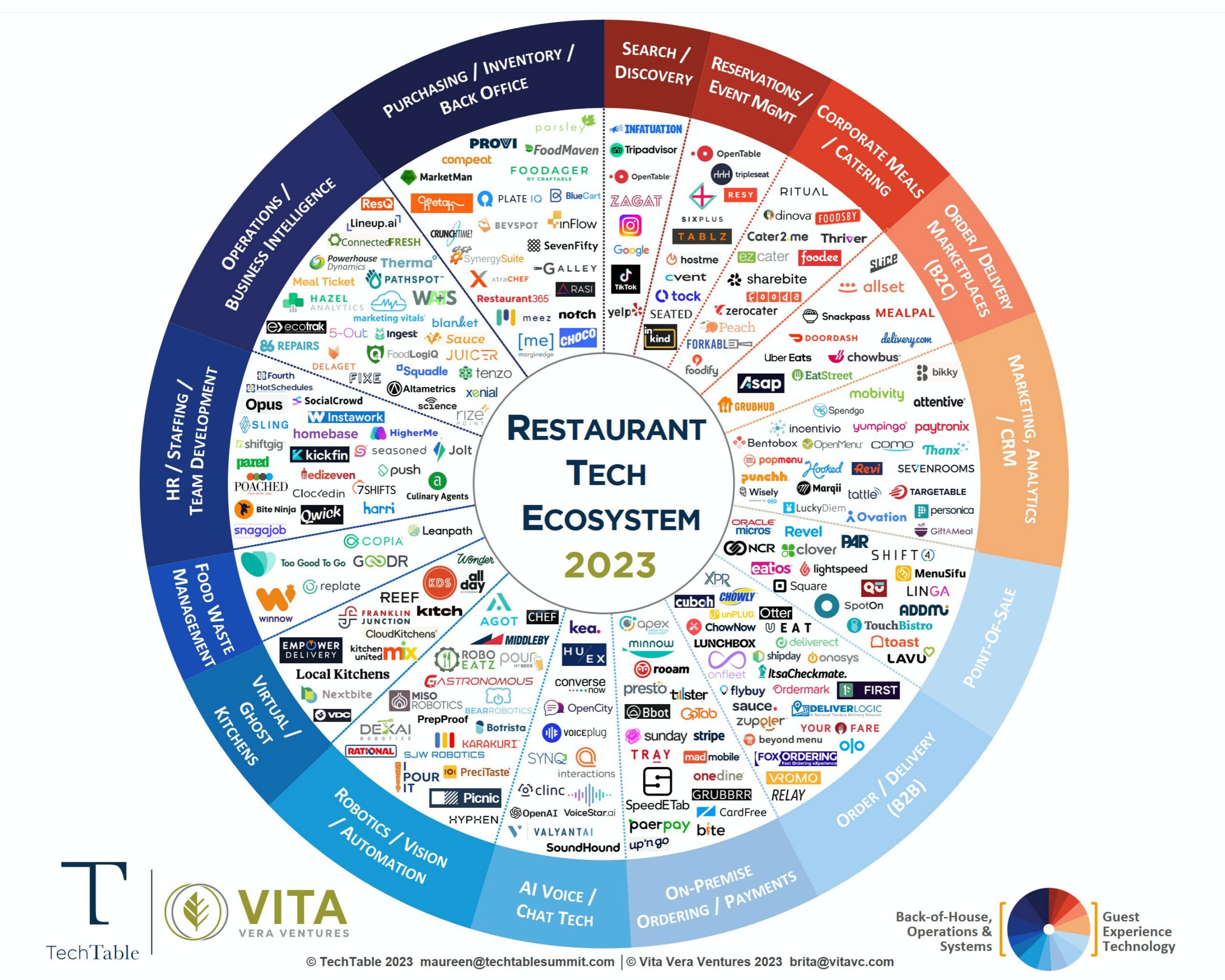

Saturday, Apr. 22nd: The Spoon published its map of tech solutions addressing the restaurant industry. - The Spoon

“More restaurant tech companies may be forced to shut down rather than finding a soft landing through acquisition.”

“While single-point solutions for things like online ordering, loyalty programs, and delivery were popular during the pandemic, we have reached a moment now with perhaps too many point solutions in the market.”

“According to the National Restaurant Association, almost 2/3 of US restaurant operators say they do not have enough employees to support existing demand.”

“We have now reached a unique moment where new technologies like ChatGPT will be able to create meaningful and personalized interactions with guests.”

Main trends: (i) chat/AI across marketing and operations, (ii) AI for scheduling to free up managers, (iii) dynamic pricing, (iv) reusable containers & tech-driven circular economy for foodservice.

Sunday, Apr. 23rd: Deconstructor of Fun published a paper on Supercell’s recent strategy. - DoF

Supercell is struggling to grow both its revenues (€1.8bn in 2022, 6% decline YoY) and EBITDA (€623m in 22, 14% decline YoY). This struggle is mainly driven by Clash Royale and Brawls Stars whose revenues have massively declined in 2022.

Since 2018, Supercall has not released a game which went beyond soft launch. “The lack of successful new game launches by Supercell stems mainly from the fact that all their games after Brawl Stars only offered incremental innovation over products that already existed in mobile, instead of a more disruptive proposal on the platform.”

“Innovation, something that Supercell has traditionally excelled at, is important because genre-defining games get a first-mover advantage.” This first mover advantage is translated in two ways: (i) you’re the 1st to capture the social dynamics around a game, (ii) you have a stronger retention because of progression sunk costs.

“We are skeptical that a company like Supercell can form and maintain its culture in new teams in a fully remote setup. Their creative method is founded on small teams that work closely together forming tight bonds between individuals, which fosters spontaneous generation and communication of ideas and allows fast pivoting.”

“Since the beginning, Supercell had its proprietary engine that has evolved from a 2D engine into a full-fledged 3D engine with strong multiplayer capabilities, as can be seen with Brawl Stars. […] Supercell is adding more resources to once again make their own engine a competitive advantage on all the platforms.”

Monday, Apr. 24th: Dealroom and KFund published a report on the Spanish ecosystem. - Dealroom

Spain minted 4 new unicorns in 2022: Fever (events), Factorial (HR), Domestika (education) and Travelperk (travel). Spanish startups raised €4bn in 2022 (15% decline YoY).

Tuesday, Apr. 25th: Amazon published its 2022’s Letter to Shareholders. - Amazon

“In 2008, AWS was still a fairly small, fledgling business. We knew we were on to something, but it still required substantial capital investment. There were voices inside and outside of the company questioning why Amazon (known mostly as an online retailer then) would be investing so much in cloud computing. But, we knew we were inventing something special that could create a lot of value for customers and Amazon in the future. We had a head start on potential competitors; and if anything, we wanted to accelerate our pace of innovation. We made the long-term decision to continue investing in AWS. Fifteen years later, AWS is now an $85B annual revenue run rate business, with strong profitability, that has transformed how customers from start-ups to multinational companies to public sector organizations manage their technology infrastructure. Amazon would be a different company if we’d slowed investment in AWS during that 2008-2009 period.”

“Over the last several months, we took a deep look across the company, business by business, invention by invention, and asked ourselves whether we had conviction about each initiative’s long-term potential to drive enough revenue, operating income, free cash flow, and return on invested capital.”

“When we look at new investment opportunities, we ask ourselves a few questions: (i) If we were successful, could it be big and have a reasonable return on invested capital? (ii) Is the opportunity being well-served today? (iii) Do we have a differentiated approach? (iv) And, do we have competence in that area? And if not, can we acquire it quickly?”

“Amazon Business allows businesses, municipalities, and organizations to procure products like office supplies and other bulk items easily and at great savings.” “Amazon Business launched in 2015 and today drives roughly $35B in annualized gross sales. More than 6m active customers, including 96 of the global Fortune 100 companies, are enjoying Amazon Business’ one-stop shopping, real-time analytics, and broad selection on hundreds of millions of business supplies.”

“Amazon has been using machine learning extensively for 25 years, employing it in everything from personalized ecommerce recommendations, to fulfillment center pick paths, to drones for Prime Air, to Alexa, to the many machine learning services AWS offers.” “We have been working on our own LLMs for a while now, believe it will transform and improve virtually every customer experience, and will continue to invest substantially in these models across all of our consumer, seller, brand, and creator experiences. Additionally, as we’ve done for years in AWS, we’re democratizing this technology so companies of all sizes can leverage Generative AI.”

Wednesday, Apr. 26th: Blue Orca Capital published a short selling report on Shift 4 Payments which is offering financial services in industries like hospitality, sports, food, retail, casino or non profit. - Blue Orca

“We see Shift4 as, in reality, a roll-up of low-tech POS systems and payment processors which is substantially less profitable, generates far less cash, and is materially more levered than investors are led to believe.”

“Ultimately, we believe that Shift4’s aggressive financial maneuvers mask a company that is far less profitable and less cash generative, and far more levered, than investors are led to believe.”

“In Q3 2022, Shift 4 Payments bought out 50% of its independent sales force of third-party distributors, thereby capitalizing the residual commissions owed to distributors and shifting one of its largest COGS line items into the cash flow statement, inflating GP and EBITDA.”

“Many of these resellers look like nonsensical takeout candidates, including small mom-and-pop businesses with limited IP. Their websites were antediluvian, and one was in arrears on its business filings. We see no reason for such M&A other than financial engineering.”

“These distributors are responsible not only for marketing Shift4’s products and services, but for managing the relationship between Shift4 and merchants over the life of each deal, for which they receive a residual commission.”

“Note that distributors do not appear to be attractive businesses: these are people-intensive organizations which, as the servicer of Shift4’s merchants throughout the life of their customer relationship, are effectively cost centers for the Company. They almost universally have little meaningful IP. They are simply an outsourced sales force whose incentive structure happens to hit Shift4’s income statement at the COGS level. We don’t see why Shift4 would have any interest in acquiring these “businesses” aside from taking the opportunity to inflate EBITDA.”

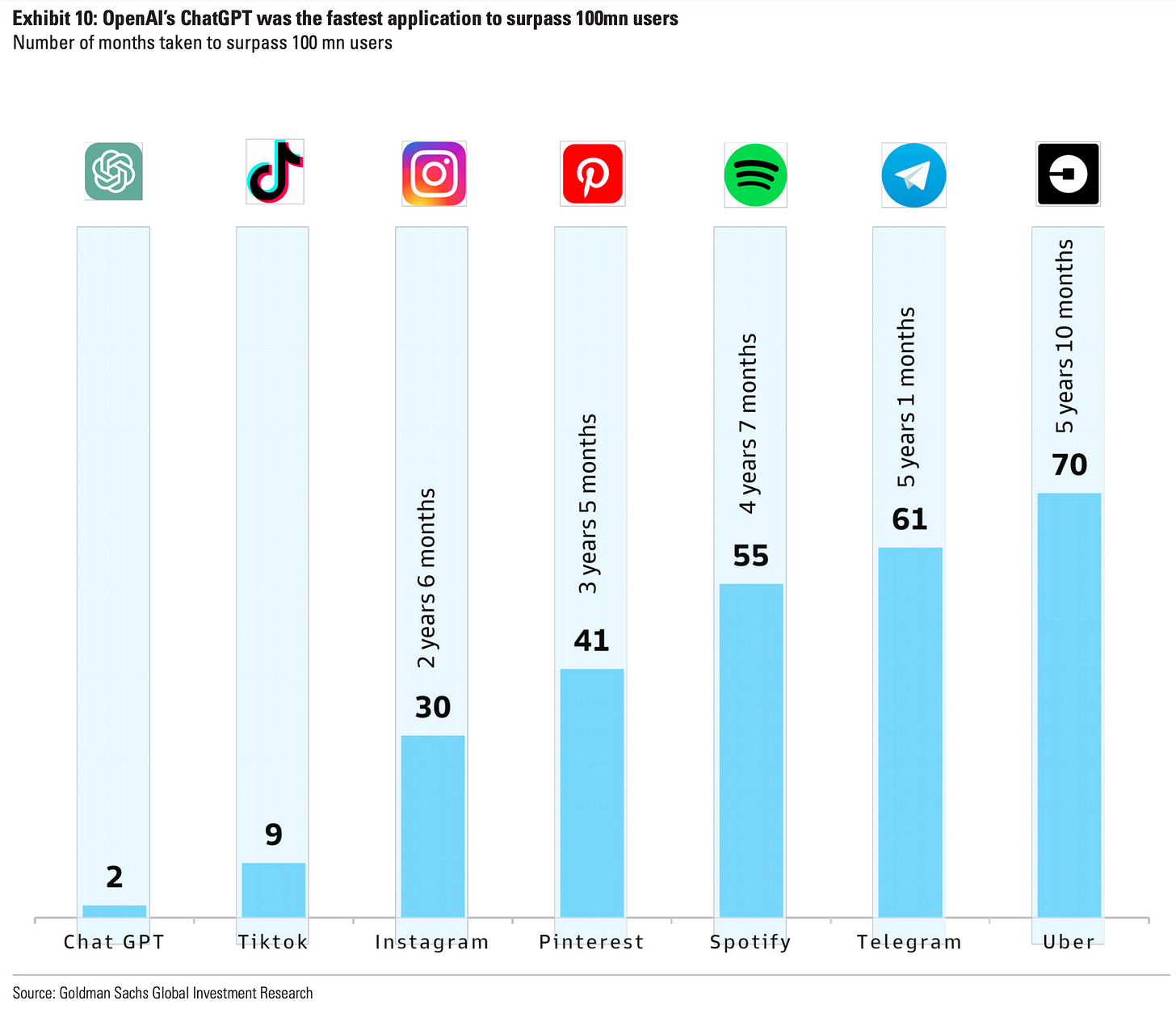

Thursday, Apr. 27th: Goldman Sachs published several reports on generative AI. - GS

“Cloud computing created new investment opportunities by enabling the delivery of software as a utility. Generative AI further unlocks value as it extends this utility and provides new tools for enhancing end-user productivity.”

“We estimate a Generative AI Software TAM of ~$150bn, vs. the global software industry TAM of $685bn. The GS Macro team estimates AI could drive ~$7tn in global economic growth over 10 years, underpinned by productivity growing 1.5pp faster annually.”

“We believe Generative AI could drive the next wave of innovation/monetization in enterprise software after cloud computing.”

“By adopting Generative AI, SaaS companies are opening opportunities for upselling/cross-selling products, increasing customer retention and expansion rates. This can present multiple levers for growth from: 1) new product/ application releases, 2) premiums for AI integrated SKUs, and 3) price increases over time as the value proposition and stickiness of existing products grows with the integration of AI.”

“Transformer models learn relationships between variables based on sequential data or context. The transformer technology looks at associated words in a sentence and builds patterns over time, invariably forming the idea behind a sentence. This technology allows AI models to compute the relationship between input and output data without having to sequence it, considerably reducing the time to train models and reliance on structured data sets, overall enhancing the self-learning capabilities of AI.”

“LLMs are based on transformer architecture and use deep neural networks to generate outputs. Transformer neural networks use the self-attention mechanism to capture relationships between different elements in a data sequence, irrespective of the order of the elements in the sequence.”

“ChatGPT is based on GPT-3, a large language model also developed by OpenAI and with ~175bn parameters, much bigger than the ~20bn parameters ChatGPT has been trained on.”

“GPT-4 is trained on ~100+ trillion parameters compared to GPT-3 which was trained on ~175bn parameters. This is expected to make GPT-4 more creative, accurate and close to human performance. GPT-4 can be customized to generate outputs that are in a particular tone, type of writing style and is also multilingual.”

“The benefit of Generative AI is that the computer can just take your text or voice and translate that into code that can quickly run various tasks, such as risk analytics, statistical modeling, routine memo drafting, forecasting, collateral generation, financial reporting, etc.”

“Extrapolating our estimates globally suggests that generative AI could expose the equivalent of 300mn full-time jobs to automation.”

“The boost to global labor productivity could also be economically significant, and we estimate that AI could eventually increase annual global GDP by 7%.”

“Generative AI’s ability to 1) generate new content that is indistinguishable from human-created output and 2) break down communication barriers between humans and machines reflects a major advancement with potentially large macroeconomic effects.”

Friday, Apr. 28th: Coumpound published its annual letter for 2022. - Compound

“We have yet to see material startup mortality. We expect this will come in the second half of 2023 as companies run out of runway from their 2020/2021 financings.”

“The broader market continues to soften, with mid-stage and growth-stage financings continuing to be nearly frozen except for the top-tier, most-consensus investments.”

“While seed has been less impacted by the slowdown, we are happily starting to see diligence processes take more normal lengths of time (1–2 weeks versus 1–2 days). This allows us to build stronger conviction, and as importantly, more meaningful relationships with founders.”

On generative AI:

“We’ve seen existing teams with great distribution be well-poised to take advantage of the payoffs of these APIs or fine-tune models to improve their products, increase monetization, and box out competitors with less distribution.”

“2024/’25 as the commoditization curve of AI continues to destroy thin layers of applications with high churn and low defensibility.”

“Time and time again we describe our strategy as getting to emerging categories early, going deep in them, and exploiting our advantages over multiple fund cycles. This allows us to make non-consensus investments with a hopefully better view on time-to-readiness for complex technologies. As time goes on we continue to gain conviction in this approach, and also notice where we can improve in the long-term.”

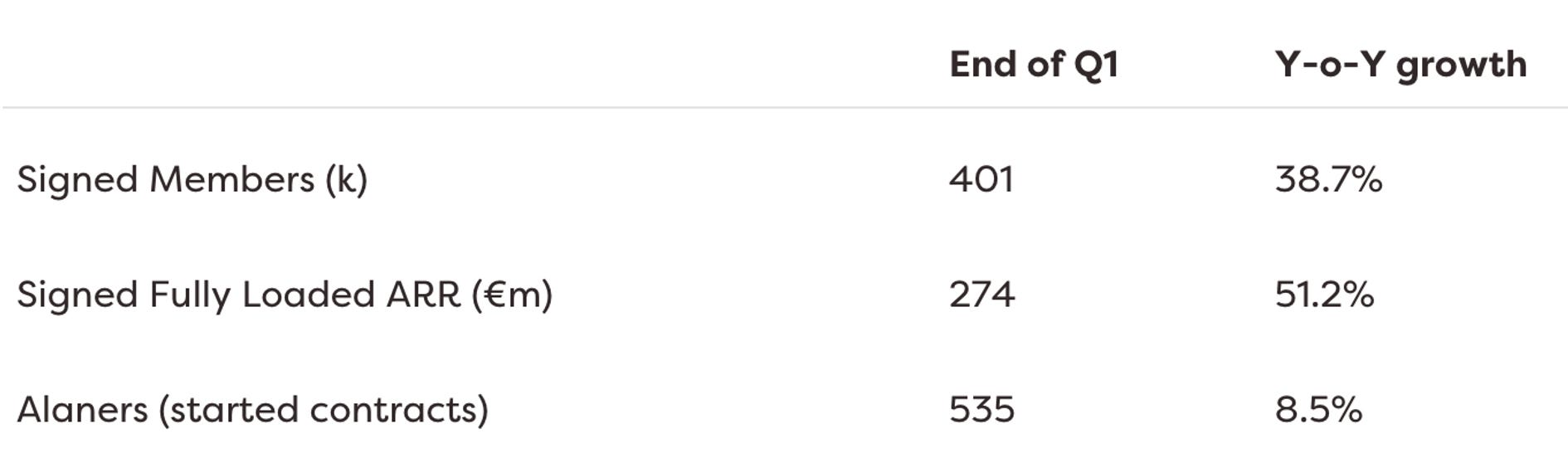

Saturday, Apr. 29th: Alan published its Q1-2023’s letter to shareholders. - Alan

“Following the decision to bundle our Mind and insurance offers to position Alan as the one-stop health partner, we took the decision to integrate the Mind app into the main app. The goal is to become part of the daily routine of our members.”

“Cost to serve has been a key priority over the past quarter, and we have reduced it thanks to strong initiatives ongoing across the company such as customer support’s tools, increased automation rate, successful progress on cost optimization of key vendors.”

“Our AI strategy aims to position Alan as the showcase example of an AI-enabled company by the end of 2023, revolutionizing our daily operations, products, and services.”

“We are working on a range of initiatives, including empowering our customer service team with automated answers, transcribing documents for faster reimbursement, personalizing emails for more effective communication, and making it super simple for members to find their coverage details.”

Sunday, Apr. 30th: I listened to a Pod of Jake’s podcast episode with Keith Rabois on his new business called Openstore which is a Shopify e-commerce merchants aggregator. - Pod of Jake

“E-commerce is a particularly broken and stagnant industry at roughly 12 to 14%. of retail. We think we have a formula to unlock the next 50% of the e-commerce penetration in the US.“

You should match your fundraising to various milestones. Every round of capital should de-risk key aspects of the business. “Defining milestones against time is not a productive exercise” (e.g. raising to have 12-24 months of runway). You want to achieve specific milestones de-risking the business with the capital you raise instead of just raising to fund the business for a specific period of time.

“Openstore’s mission is to reinvent e-commerce to allow for serendipitous discovery of products in a way that bypasses or obviates the need to shop in the real world.” Openstore wants to replace the trip to the shopping mall by an app.

“We want to create is an Instagram to Shopify experience that allows people to be delighted with new ideas, new products that they wouldn't have been searching for on Google or Amazon.”

Openstore provides liquidity to the long tail of Shopify stores ($500k to $10m in annual sales) by offering them a price using data to buy their business or by guaranteeing them the cash flow from their business while operating their business from them (Drive offering recently launched).

With Openstore Drive, instead of acquiring businesses, Openstore charges 10% in management fees to operate the store instead of owners while guaranteeing them the income you can generate from the store. Owners don’t sell their store. At the end of each year, they can decide to sell, to stay in the Drive program or to opt out from the Drive program. It’s a way for Openstore to accelerate the construction of its brands portfolio without having to wait for owners to be ready to sell their business. Openstore acquired c. 40 stores and have many merchants which signed up to Drive

“I genuinely believe that horizontal businesses are better than vertical businesses. This is sort of moderately controversial. I think, basically, there's a fixed cost and pain to building a startup. And so you might as well amortize the same pain across the biggest possible vision.”

“You want to create an automated system that allows you to price merchants in an hour, and allows you to close merchants in a matter of days.”

“We do provide 80% of the cash on an acquisition upfront with 20% earned over a few weeks.”

Openstore has an ideal tech stack that it implements in acquired companies. It has also a product called Gumdrop enabling micro-influencers to promote Openstore’s product and be remunerated.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋