Trends - 200+ Tech Predictions Aggregated for 2020

Overlooked #3

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing with you all the tech predictions I have been reading in the past couple of weeks. I’m also talking about 10 trends I am interesting.

I compiled 200+ predictions for 2020 from the most prestigious people (Marc Zuckerberg, Azeem Azhar, Alex Danco, Charlie Tango, Albert Wenger etc.) and institutions (a16z, USV, GP Bullhound, CB Insights, Forbes, Deloitte, The Information).

It’s a great source of inspiration to think about the key topics that will shape this new year. I grouped them into categories and you can also access to the original sources. Click on the Airtable button to access the database. Enjoy and let me know which prediction is your favorite!

Here are 10 trends I am interested in. I don’t pretend to be able to forecast the future. In fact, most of them are inspired by the predictions I have aggregated. If you are building a business around of these trends, contact me and let’s have a chat.

Populations are getting fragmented into conflicting segments.

Wealthy people ⚔️ Poor people

Millennials ⚔️ Baby-boomers

Urban ⚔️ Suburban and campaigns

Communities

Fragmentation is a business opportunity. Being able to understand a segment better than anyone else and building products that suit their exact needs will make the difference.

The below graph from the Financial Times tends to prove that developing countries are reaching peak meat consumption.

Netflix documentary called “The Game Changers” is even trying to demonstrate that vegetarian diet is superior to traditional diet showcasing world class athletes who became vegetarian and managed to enhance their performances thanks to the shift.

In my opinion, the two main changes compared to past decades are that (i) people are becoming vegetarian no longer only to prevent animal suffering but to preserve the environment which is a way broader issue (ii) new companies developing plant based or cell-based meat alternative are no longer targeting the vegetarian niche but want to address everyone and especially the meat lovers by releasing alternative that taste and smell like real meat.

Facebook, Instagram, Twitter and Linkedin are anything but social. People are not building meaningful relationships on these platforms which are stressing performance over interactions and content over people. I expect new social networks to emerge in the coming years.

Every generation has its own preferred social network as showed in this graph from The Economist. I am sure that future teenagers will find their own social network and I will not be surprised if it ties closely to gaming. Fortnite has almost become a social media but the game-as-a-social-network design can be push further.

But we will also see the rise of social networks dedicated to baby boomers and older generations. I am always fascinated by these aged people travelling together in coaches or ferries to visit cities. They seem to have a lot of fun and to build meaningful relationships. For instance, in the US, Revel is building a great community of women over 50 y.o. who share real-life experiences like outdoor activities or casual conversations in living rooms. The business model is also worth mentioning as it is not based on advertising but on a $15 monthly subscription.

China launched a 10 year $300bn investment plan in 2015 named “Made in China 2025” to catch up with foreign tech capabilities in numerous industries like semi-conductors, artificial-intelligence, electric-vehicles, nuclear etc.

Since then, it has outrageously proved to the world that a State based tech program could have tremendous impacts on an economy. China is now at the forefront of numerous technologies like image recognition, bitcoin mining, alternative energy sources. Of course, China un-liberal political system has been a key catalyzer to achieve these goals and most political tech applications in China must be condemned. This success has revitalized protectionism in the US with a long lasting trade war between the US and China.

Some western nations have also launched strong programs to support the tech industry. The European Union has increased by 50% its 5-year program dedicated to the space industry up to €14.4bn and launched a €2bn fund dedicated to AI and blockchain. France has launched a €5bn initiative to fund late state national startups.

Another form of tech sovereignty is the opposition between public governments and private entities.

GAFAM are under the spotlight of national regulators because of their monopolistic positioning but also for tax-evasion accusations.

States do not want to lose their regal power. The political back-clash following the announcement of Facebook’s Libra initiative has been severe. Numerous initiatives are launched worldwide to build nation-controlled digital currency.

2019 was supposed to be a great year for tech IPOs. In fact, numerous flagships IPOs happened in 2019 but not all of them performed as expected.

4 companies (Uber, Lyft, Jumia and Pinterest) are now worth less than their last private valuation.

The most hyped IPOs under-performed compared to their initial offering price (Lyft, Uber, Pinterest).

Public investors favored SaaS business model which is now the standard in the IT industry. Fiverr is an exception. But it is a marketplace for freelancers with an existing other public peer with Upwork.

Regarding Beyond Meat, I agree with Damodaran to say that the company is overvalued. Investors go long on Beyond Meat doing a macro bet on the trend of the rise of vegetarian consumption habits. The market correction has started in the past few months and will continue next year as new entrants like Impossible Foods become listed and incumbents announce new meat alternative products.

Adding to that the WeWork missed IPO, the fact that Softbank is struggling to raise its Vision Fund II and the general feeling that we are on the top of an economic cycle, numerous elements tend to go towards capital rationalization in Venture Capital.

On the one hand, investors will push their portfolio companies to move faster towards profitability at least on certain parts of their business (e.g. a customer segment, a product, a geography). On the other hand, profitability will be perceived as the new unicorn to hunt for while investing.

At early stage, VCs will look for companies which are already break even and want to raise fund to accelerate their growth while maintaining their ability to go back to a profitable set up in case of a downturn. At later stage, it will become harder to raise fund without being profitable or showing a clear path towards profitability.

Climate crisis is threatening the humanity. It is mainly due to greenhouses gases emissions - 76% of them being carbon dioxide. Prominent tech companies like Stripe and Microsoft are taking radical decisions to offset their carbon emissions. In 2020, investors will follow suit and fund startups tackling this challenge.

US-tier one VC fund USV has already reshaped its investment thesis to invest in companies helping us to reach 100% renewable energy or to become carbon neutral by reducing / removing C02 emissions. The below slide details all the areas in which the fund will be interested to invest.

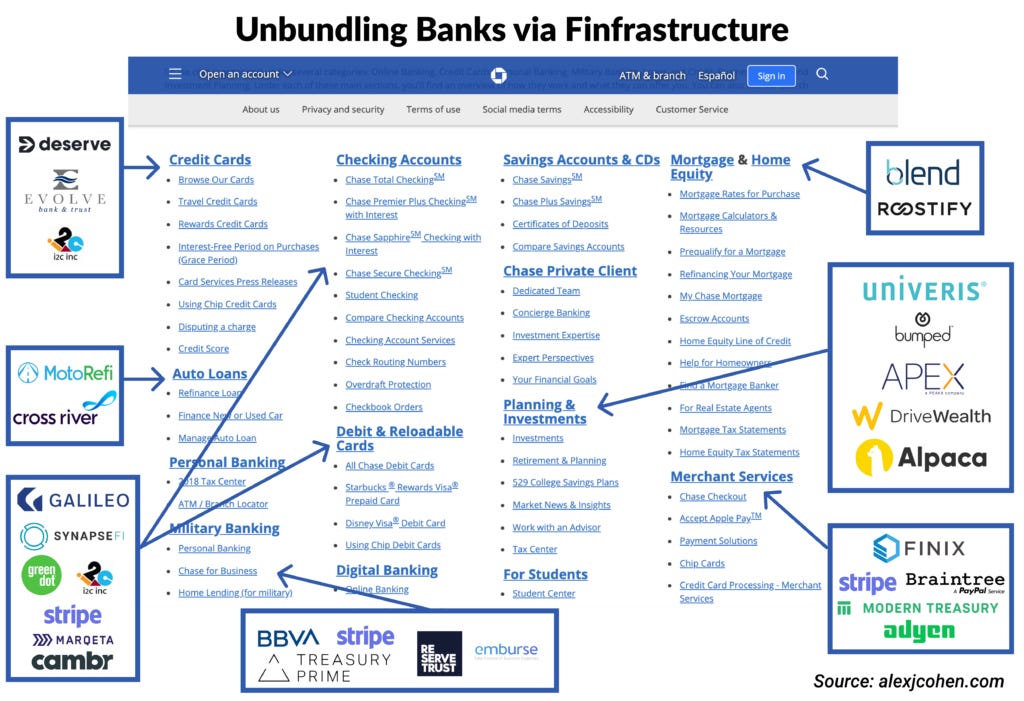

A first wave of fintech startups started to address easily solvable consumer needs. Europe is the land of neo-banks with N26, Revolut and Monzo leading the pack. Last year, we noticed the rise of startups helping you to make savings and offering you investment opportunities built thanks to PSD2 regulation which forced traditional banks to build APIs for third parties. Both neo-banks and saving apps were nice-to-haves for consumers but not must-haves.

This is changing.

Two contrarian movements will happen at the same time in 2020:

Existing fintech players to diversify their product offering to become essential for their customers. For them, re-bundling of financial products is happening.

New players will rise to tackle more complex financial products continuing the bank unbundling.

About, unbundling of complex financial products, I am particularly excited by two sectors:

Education. US student debt is out of control reaching $1.5tr and representing 80% of the student worldwide debt. Income Share Agreements (ISAs) appear to be a solid candidate to solve the US student debt crisis. Numerous startups are starting to build exciting businesses around ISAs (Lambda School, Holberton School, Edly, StudentFinance). ISAs replace a fixed interest loans independent from outcomes by a percentage of the future income taken on the salary for a certain period when (i) students start working and (i) are paid above a certain threshold. Doing so, ISAs ensures that interests between the school and the students are more aligned and the students have to pay back only when they get a decent job.

Real-estate. It’s a weird asset class: illiquid, binary (either you own your house or not) and overweighted by people (50%+ of the population have 80%+ of their worth invested in real estate). The real estate industry is also under-digitized and customer experience is awful. Full-stack companies based on complex financial structure are emerging to transform the industry. Some like Divvy are helping people to build progressive housing ownership. Some like Point are letting you sell only part of your house. Others like Kodit and Casavo are buying your house on the spot and resell it at a premium after refurbishment works.

Finance-as-a-feature is also a growing trend. It says that all companies will incorporate financial products in their offering. Starting with GAFAs, it will expand to other consumer brands and tech companies which want to add a moat to their business and collect more precious data on their users.

The level of education about crypto has risen in the past few years. Crypto is starting to be democratized. Entrepreneurs with non crypto-background now understand the value it added compared to traditional businesses.

Crypto capital markets have to be built from scratch (cf. its three main categories in the below framework from Etienne Brunet). Experienced financial professionals left or are leaving their bank to build a business in crypto. They usually aim to start building a product for the crypto market with the ambition to bring back their innovation to traditional financial markets where they come from. The lack of regulation in the crypto market foster product innovations that could be replicated in other asset classes.

Chris Dixon stated back in Feb. 2018 that decentralized platforms need to go through two phases of product-market-fit:

“ Product-market fit between the platform and the developers/entrepreneurs who will finish the platform and build out the ecosystem,”

'“Product-market fit between the platform/ecosystem and end users.”

In 2020, certain crypto projects will achieve this second phase of product market fit. A crypto consumer product will reach massive adoption. Of course, Facebook Libra is well positioned to get this spot. Gaming and social apps based on tokens could also become viral this year and utility consumer apps will follow.

People and businesses are more concerned than ever about their data privacy. This concern was translated into regulations either in Europe (GDPR) and in the US (CCPA in California).

Gartner is forecasting that by 2022, 50%+ of the global population will have will have its personal information covered under local privacy regulations in line with GDPR vs. 10% as of today.

Numerous startups are seizing this opportunity to build privacy-related products. In that regards, Clément Vouillon‘s tech landscape on B2B privacy startups is noteworthy.

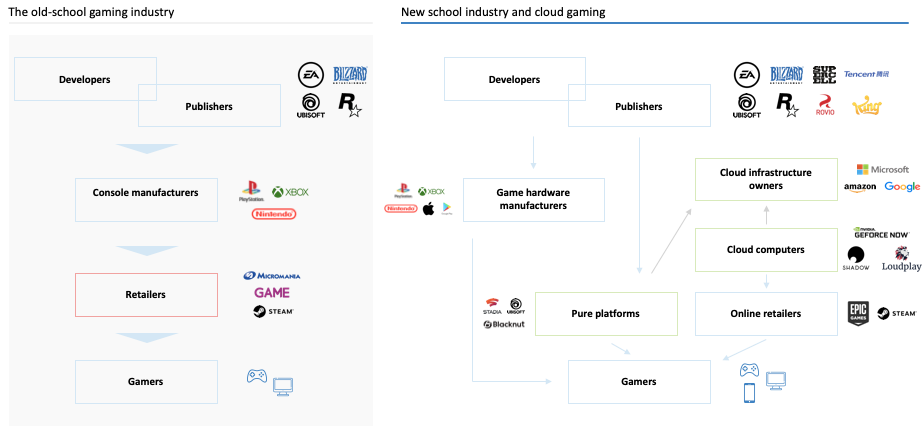

Streaming has already changed the way we listen to music (Spotify, Apple Music, Youtube Premium) and we watch to movies and series (Netflix, Disney, Hulu, HBO).

In gaming, streaming means replacing an expensive console or PC with a subscription service connected to the cloud managing the heavy computational requirements from some games. It’s technically harder than music and video because games are unpredictable and latency must be highly limited to guarantee the best experience.

Streaming and cloud gaming will completely reshape the value chain of the industry and the bargaining power between stakeholders. Google Stadia has been live since November 2019. Traditional hardware manufacturers Microsoft and Sony will announce their streaming projects in 2020. Tier-2 players in the industry including Ubisoft, Electronic Arts, Nvidia, Apple and Amazon have also live streaming projects or projects to be announced in the 12-18 coming months.

In 2020, players will be testing the different plans because they offer great value for money compared to paying upfront fees for games and hardware. Yet, it is still unclear to see how the industry will be structured when the market gets more mature.

Thanks to Julia for the feedbacks! Thanks to Maxime for the graph about the gaming industry evolution! 🙏

See you next week for another issue! 👋 Do not hesitate to share the newsletter to your friends and to subscribe if it is not already the case!