🇫🇷 The State of the French Tech Ecosystem 2024 - "A Tale of Two Cities"

Overlooked #190

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the 2024 edition of my report on the French tech ecosystem.

I'm delighted to share my 2024 report on the French tech ecosystem with c.100 slides covering everything: general metrics, tech trends, AI, unicorns, funds investing in France, exits and an outlook for 2025!

I’ve prepared several posts based on the report, highlighting the key themes covered. The first post has to be focused on AI, which has been the primary growth driver in the ecosystem, while the rest continues to recover from the tech downturn.

The report reflects my views and do not necessarily reflect the views of my employer. If you have any feedback or if you spot any mistake in the report, please do send me an email at alex@20vc.com.

We’re also organising a 20VC event at Station F tomorrow evening (Jan. 15th) to present the report and interview top founders, including Alex from Deel, Arthur from Pennylane & Eléonore from Pigment. We have a few spots left for founders. Feel free to email me if you would like to join.

In 2024, the French tech ecosystem was “a tale of two cities”. French startups raised €7.1bn raised (+3% YoY) across 518 funding rounds (-18% YoY). Excluding AI, the amount raised by French startups declined by 11% YoY.

AI

The three key learnings are: (i) AI funding has been the major growth driver of the ecosystem in 2024, (ii) Paris has become the main AI hub in Europe, (iii) France has a rich ecosystem of 760+ AI startups across the entire value chain from foundation models to infrastructure & applications.

AI funding has been the major growth driver (27% of € raised vs. 15% of € raised in 2023, +82% YoY) of the ecosystem in 2024.

Paris has become the main AI hub in Europe driven by multiple factors (i) top engineering schools, (ii) great research ecosystem both on the public & private side with AI labs from top tech companies (DeepMind/Meta), (iii) strong government involvement, (iv) 5 unicorns at the centre of the global AI revolution (Dataiku, HuggingFace, Mistral, Owkin & Poolside).

760+ French AI startups which raised a round after 2020. We mapped the most prominent ones and got the following key learnings:

(i) France loves foundation models (Mistral focused on multi-modal models, Poolside focused on code, Aqemia & Owkin focused on drug discovery in healthcare, Entalpic & Altrove focused on materials).

(ii) In 2024, emergence of a wave of infrastructure tools to deploy LLMs in production (especially for large companies) with extremely talented teams: ZML, Vertesia, Adaptive, BlueMorpho.

(iii) Multiple applications (both industry specific & function specific) built in super crowded areas (e.g. customer success, AI ambient listeners in healthcare, AI-powered SDRs) - competing with 10+ other players in Europe and 10+ more in the US.

(iv) Specific trends emerged in 2024 in the applications layer: answering to RFPs (Explain, Tengo), designing marketing assets (Lasqo, Pimento), advertising automation (Arcards.ai, Poolday.ai) or deploying general agents to improve the productivity of white collar workers (Dust, Phacet).

TL;DR: If you build in AI, you have wind in your sails. It’s easier to attract talents, get commercial traction and funding momentum.

Outside AI

Outside AI, (i) the venture market adjustment that began in 2023 has persisted into 2024. (ii) however, the outlook is not entirely negative.

We had a pandemic-era deals surge in 2021-2022. The venture market adjustment that began in 2023 has persisted into 2024 with:

More than 9 bankruptcies of companies which raised €30m+ (Ynsect, Cubyn, Master's, Luko, Intercloud, Prophesee, Cityscoot and Jungle),

Multiple down-rounds and layoffs happening (e.g. bottom quartile of French unicorns reduced their headcount by 3% YoY in 2024),

Multiple cofounders/CEOs stepped down to steer companies into a new direction (e.g. Olivier Pailhes at Aircall, Mathilde Collin at Front, Nicolas Cohen at Ankorstore),

In the 2020-2022 cohort of unicorns, 80% (24/30) have not raised another round to date and 40% (12/30) are no longer worth $1bn+/need to confirm their $1bn+ valuation

It takes longer to raise capital, valuations & round sizes are depressed, you need to over-deliver to ensure fundraising success.

However, the outlook is not entirely negative:

Two out of three new unicorns were in more traditional sectors with Pennylane (all-in-one financial and accounting platform for SMBs) and Pigment (modern FP&A platform for mid-market & enterprise companies),

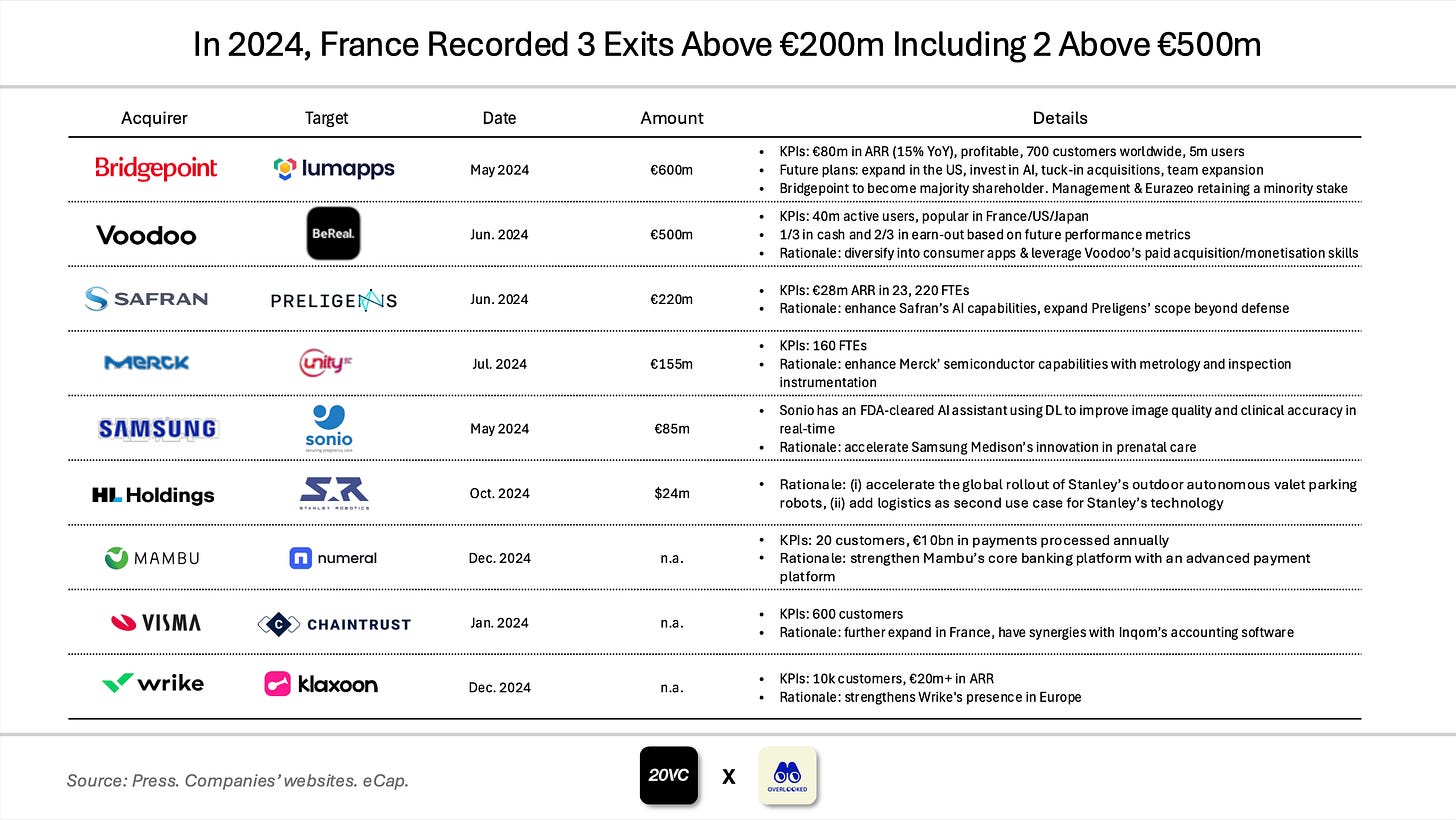

The two largest exits were outside AI with Lumapps sold to Bridgepoint (€600m) and BeReal sold to Voodoo (€500m),

There is a strong growth funding appetite for categories like vertical software (Akur8, OneStock), climate (Electra, Elyse) and fintechs (Payflows, Pennylane),

Multiple themes remain well funded at early stage: crypto (Deblock, Flowdesk), B2B finance (Freqens, Payflows), deep-tech (Bacta), defense (Dark, Comand, Deepmine).

I’d like to thank everyone who contributed to the report. More specifically and as always thanks to Julia (🦒).

Bravo :)