🇮🇹 The Italian Tech Ecosystem - Rome Wasn't Built in a Day

Overlooked #144

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol). vSols are industry-specific solutions that aim at becoming the leading industry OS. They combine dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol.

Today, I wrote a collaboration piece with Timothy Motte on the Italian tech ecosystem. Timothy has a great newsletter called The Realistic Optimist in which he covered many emerging tech ecosystems across the world including Singapore, Bosnia, Iraq or Algeria.

In recent months, I’ve spent a lot of time digging into the Italian tech ecosystem to see if we should spend more time in the country as a pan-European fund. After meeting with over 100 entrepreneurs and investors in the past 12 months, I’m convinced that the Italian tech ecosystem has reached a tipping point and that it’s going to be one of the most interesting tech ecosystems in Europe in the next 5 years.

I wanted to find an excuse to write about the Italian ecosystem and it was great to combine my learnings from the ground with Timothy’s perspective on overlooked tech ecosystems across the world. Of course, if you’re building an exciting startup in Italy or if you want to talk about the Italian tech ecosystem, feel free to send me an email at adewez@eurazeo.com.

Zoom in, zoom out

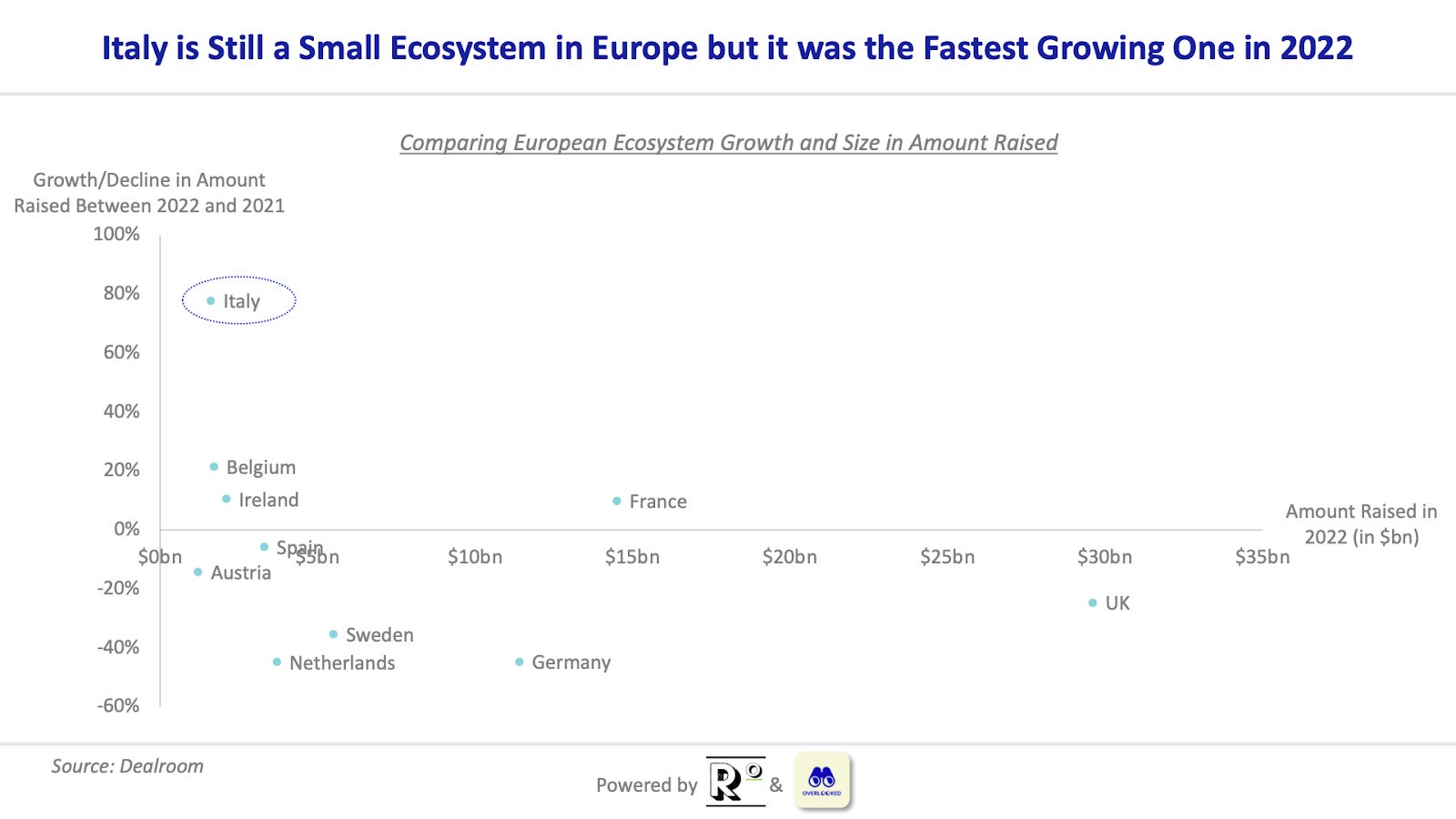

A first, unadulterated view of the Italian startup ecosystem looks promising. Startups in the country have raised more and more funding, year after year. Italian founders even raised more money in 2022 than in 2021 (73% more to be exact), a global anomaly given the virulence of the current funding winter. The exceptional 2022 year was topped off by the minting of the country’s first two unicorns after the dotcom bubble, Scalapay and Satispay. While the former operates in the turbulent BNPL sector, both mintings represent tangible milestones translating the ecosystem’s growing maturity.

Zooming out to take a pan-European view displays a less rosy view, or an exciting opportunity for growth depending on your mood. When compared to its European neighbors, especially the ones with relatively similar socio-demographic makeups (Spain, France, Germany) the Italian ecosystem is a definite laggard.

“On the European stage, the Italian startup ecosystem is neck and neck with Latvia's. Both recently welcomed their first unicorn, both have similar VC funding per capita, and both are showing great promise in fintech. Credit where credit is due – Latvia is doing a fantastic job. But the economic powerhouse with 30 times the population that is Italy should be operating on another level.” - TechEU

Italy especially pales in comparison to its European counterparts on one specific metric: VC funding per capita. The latter is a key indicator of an ecosystem’s liquidity and ability to prop up new successful startups. In H1-2022, the figure stood at $18 for Italy, way behind Spain’s $40 France’s $145, and Estonia’s $750.

Ecosystem makeup

Before diving into the analysis of why the ecosystem is where it is, let’s first take a quick panorama of what the ecosystem looks like.

While it is always hard to pinpoint the beginning of something as impalpable as a “startup ecosystem”, its formalization can be traced to the passing of the country’s 2012 “Startup Act”. Quickly becoming a must-have for ecosystems around the globe from Argentina to the Philippines, Italy’s version of the startup act granted eligible companies with tax incentives for equity investments, a simplified procedure for bank loans, and tailor-made labor rules.

Milan, Italy’s financial center, takes the lion’s share of the country’s startup funding, followed by Rome, Turin, and Bologna. The historical gap between the industrially rich north and the country’s south is replicated within its startup ecosystem. As I related in my Tunisia article, a startup ecosystem’s development inevitably happens in clusters, and Milan’s role as the ecosystem’s neuralgic center isn’t bound to change anytime soon.

As demonstrated by its two maiden unicorns, fintech is the Italian ecosystem’s specialty as of now. Given that all subsequent digital startups will need efficient digital financial services, fintech’s dominance makes sense in the context of a relatively young ecosystem. The energy sector comes in second, heavily skewed by the performance of Newcleo, a nuclear energy startup that might soon become Europe’s most funded one. Health & Life Sciences, facilitated by the country’s strong research field, comes in 3rd. Finally, Proptech, propelled by heavy-raiser Casavo comes in 4th according to EY’s 2022 Venture Capital barometer.

Aside from Scalapay and Satispay’s success, the Italian ecosystem has already witnessed its first exits and mega-rounds. On the exit side, Depop (e-commerce) was acquired by Etsy for $1.6bn, Face.it (gaming) sold to Savvy Games (Saudi gaming arm) for $500m, early stage Italian funds into Musixmatch (music) partially exited during a growth transaction with TPG, and Facile.it (online comparison website) acquired by Silverlake for $1.1bn. On the mega round side, Casavo (proptech) raised $400m and Bending Spoons raised $340m. And Italian companies aren’t just getting acquired, with stories such as Bending Spoons which acquired US company Evernote and Casavo which acquired French company Proprioo to expand in France.

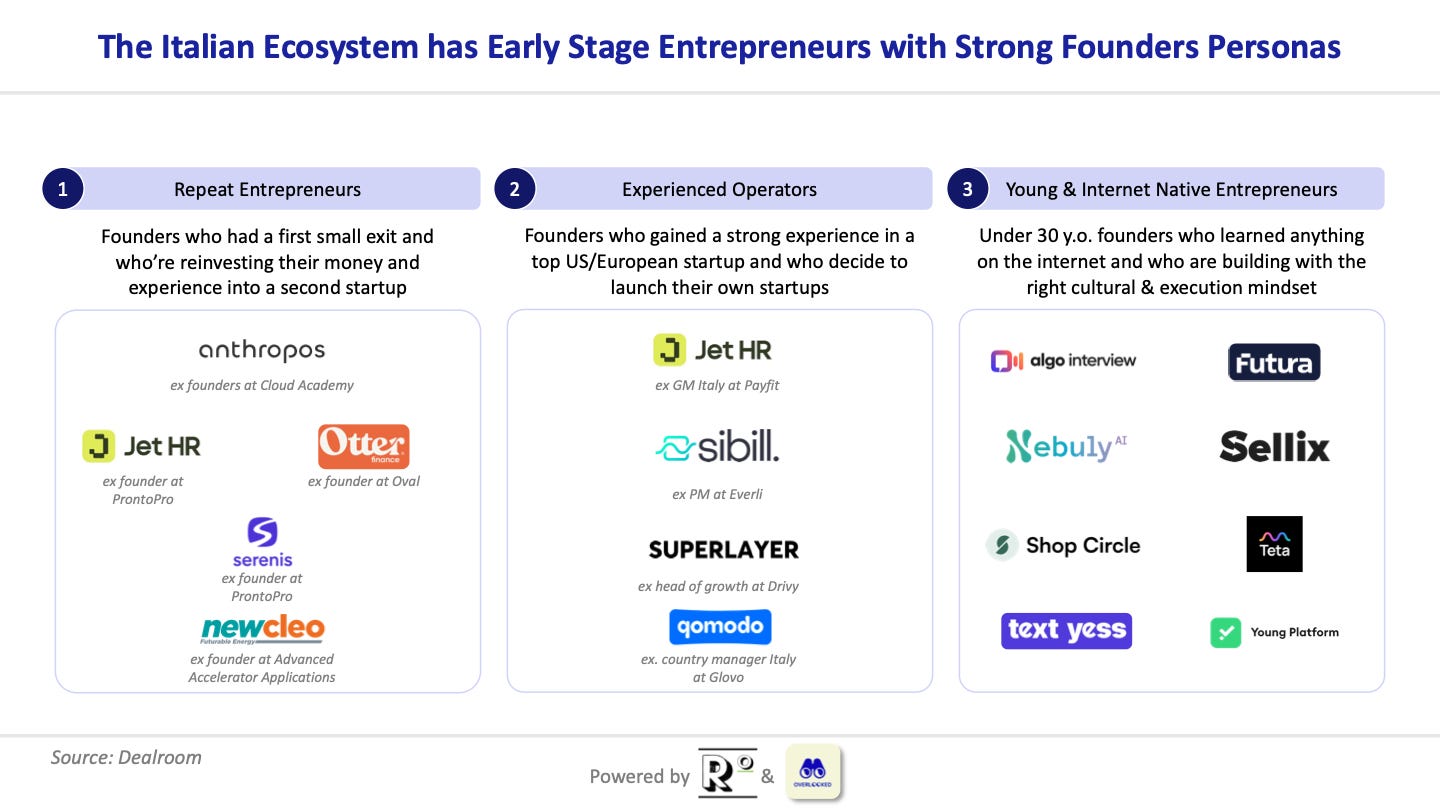

This tangible financial traction is further complemented by founders of exited companies or of top Italian startups investing back into the ecosystem (e.g. Giorgo Tinacci from Casavo, Raffaele Terrone from Scalapay, Max Ciociola from Musixmatch). The founders of some of the companies cited above now act as angels within the Italian ecosystem.

This enthusiasm is joined by the creation of new venture funds (e.g. Lumen Ventures founded by founders at Freetrade), the entrance of some of Italy’s top family offices, the launch of corporate venture funds (e.g. Intensa San Paolo launching a €250m CVC fund called Neva SRG or Angelini launching a €300m CVC fund dedicated to life sciences and healthcare) as well as renowned foreign investors (Benchmark backing Commerce Layer or Insight backing Unobravo - a deal sourced and led by an Italian at Insight) into the Italian startup world.

Despite such feats, the Italian ecosystem is still undeniably in the early innings of its development, the graph below demonstrating that statement.

Assets and liabilities

An outsider’s frustration at the Italian startup ecosystem’s lagging development can stem from the realization of Italy’s numerous advantages. The country has an excellent talent pool, molded by the Italian university scene that hosts some of the best institutions in Europe.

“We will find that in the first ~200 positions globally, both France and Italy place 5 universities each, the two highest ranked being Italian: Politecnico di Milano (20th) and Politecnico di Torino (39th) . The Ecole Polytechnique (X) and CentraleSupelec, the first two French schools in the list, rank respectively as the 52th and 72th.” said Matteo (VC at Plug & Play) and Ubaldo (VC at Wellness Holding)

Compared to France where the fast-growing startup ecosystem has been irrigated by graduates from the best engineering and business schools in the country, Italy still loses a significant amount of its best talent to brain drain. The country’s mediocre R&D spending worsens the case for its best researchers to stay at home.

In another Italian paradox, the country hosts an incredibly creative culture, supported by centuries of pioneering the arts, exporting world-known brands, and establishing itself as a renowned tastemaker. That creative side is complemented by an entrepreneurial one, the MSME sector employing 76% of the workforce. The country’s manufacturing savoir-faire could also be an advantage for hardware startups. Yet, despite those factors, Italian founders still complain of a lack of risk-taking, forward-looking, moonshot-seeking mindset, which some say is easier to find in the US.

The ecosystem’s youth inevitably renders it structurally weak in certain aspects. For example, some note that the country’s incubator scene hasn't yet developed to world-class standards. Local institutional investors, including corporates and pension funds, are criticized for being too conservative and not pouring much-needed money into the country’s VCs. The recently elected far-right government, headed by prime minister Giorgia Meloni, isn’t the most tech-forward thinking leader the ecosystem could dream of.

The scarcity of knowledgeable and trigger-happy angels, a consequence of the little number of exits, also represents an obstacle to the ecosystem’s funding liquidity.

The French connection

While the traumatic episode of Zidane’s headbutt on Materazzi during the 2006 World Cup Final might never be consumed, the Italian ecosystem seems to be getting inspiration from its neighbor up north on matters of startup development.

Nowhere is this more evident than in the activities of CDP, the Cassa Depositi e Prestiti, which is equivalent to France’s BPI, the Banque Public d’Investissement. In France, BPI is widely considered one of the ecosystem’s most important actors, especially in the extraordinary growth and development the ecosystem has seen over the last decade. As I outline in my article about France:

“As a public investment bank, BPI can offer a variety of different financial tools while also positioning itself on riskier or more “domestic-focused” innovations that aren’t necessarily appealing to traditional VCs”. - Realistic Optimist

This propensity to invest in the local startup ecosystem with substantial funds, all while being able to adopt an extremely long-term approach has made CDP one of Italian startups’ main financiers to date.

“CDP Venture Capital has started to direct public and private money towards Italian VC, with €1.8bn AUM and a portfolio of 10 funds covering the entire startup lifecycle, from Tech Transfer all the way to late stage and pre-IPO. CDP VC’s investment activity, very rapid and highly selective, has been focused on creating the infrastructure to develop the market as well as on investing directly on strategic areas where the market was failing (e.g. early-stage deep-tech startups, etc.)” - Alessandro Scortecci, head of Strategy and Business Development at CDP Venture Capital SGR

Similar to BPI, the enthusiasm infused by CDP is partly aimed at encouraging other important Italian economic actors to get in on the action. While direct causality might be hard to prove, the fact that Italy’s national electricity grid operator is launching its own CVC is telling.

The parallels between the Italian and French startup ecosystem can be dug even deeper, with the establishment of the Italian Tech Alliance strongly reminiscent of the role played and agenda held by France Digitale. The creation of Exor Seeds to invest €150k tickets in Italian pre-seed and seed stage startups at scale, which resembles the structure of Kima Ventures (one of France’s most active early stage VCs) can also be pointed to.

Both countries should learn from their common weaknesses. Italy and France share the tricky similarity of having large enough domestic markets to reach significant scale without expanding internationally. This could create an artificial glass ceiling on the ecosystem. Italy could learn from the way France managed to dynamize a legacy, quasi-aristocratic, and closed business environment, a trait shared by the Stivale.

Conclusion

One’s enthusiasm regarding the Italian startup ecosystem revolves around seeing the cup half full or half empty. Some may argue that the consistent year over year growth is a sign of great potential, while others argue that its meager performance compared to its European neighbors makes it an underperforming ecosystem.

The title of this publication might guide the reader into which option I subscribe to. What I've noticed while writing my 70+ articles is that momentum is extremely important for an ecosystem to experience the initial exits that will make the ecosystem self-sufficient. Italy's results over the last couple of years place the momentum on its side.

That momentum is fragile, however. Italy’s good 2022 performance can also be attributed to the fact that the country is catching up to its potential, and that the performance thus isn’t that extraordinary in and of itself. The failure of one of the ecosystem’s headliners, a non-negligible probability given Scalapay and Casavo’s shaky business models, would hurt the ecosystem. For the moment, the ecosystem’s 2023 performance is more on par with 2020 than last year’s.

The Italian government made waves recently by banning OpenAI’s chatGPT. While the issues raised by the Italian regulators are more than valid, such a staunch decision displays a refractory view of innovation. At the end of the day, not only is the ban easily circumvented through a VPN, but banning a tool other countries have access to severely disadvantages the Italian worker.

The brightest point here in my opinion is the comparison to the French startup ecosystem. Both countries are similar, and the problems Italy is trying to solve at the moment (i.e. retaining their best talent by creating an exciting local startup scene) have been in large part accomplished by France.

At collective.work, the startup I work at, all three founders would’ve been more susceptible to exile 10 years ago. One of them came back from London to build a startup at home. The two others, top business school graduates, decided to found and incorporate their startup in France, carried by a tech patriotism that is easier to follow when the ecosystem is on your side. Italy is already trying to leverage its potent diaspora through a drastic tax incentive program for Italians wishing to return home.

For Italy, taking inspiration from the French tech ecosystem playbook has been a great way to bring its local scene to the next level. There are other French recipes that can be replicated in Italy (e.g. a safety net to launch a startup equivalent to the “rupture conventionelle” in France which enables employees to leave their job to start a company while receiving unemployment allowances or nurturing its startup mafias to accelerate the velocity of its tech ecosystem flywheel) before the Italian tech ecosystem finds its own singularity.

Thanks to Michele, Matteo, Lorenzo, Andrea and Julia for their valuable feedback!

| A guest post by

|

Super cool analysis, thanks guys!

I would add also the following when talking about foreign funds investing in the ecosystem:

Xfarm, one of the most important agritech Italy ventures, backed which a €17M Series B led by Swisscom Ventures last year.

When talking about Depop, it's worth mentioning though that despite the founder was Italian, they moved to the UK after their €2M seed so I wouldn't consider their exit a sort of an "Italian" exit.

Finally, when talking about crowdfunding, Mamacrowd by Azimut is probably the biggest one, but it's worth adding Doorway (https://www.doorwayplatform.com), a fairly new player acquiring traction in the ecosystem supporting startup investment education for the country's financial players boosting Italian startup growth in terms of equity fundraising.