🖱 ServiceNow - Scaling to $10bn in ARR

Overlooked #173

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a deep-dive on ServiceNow.

Today, I’m excited to share a deep-dive on ServiceNow. I co-authored this post with my friend Chirag Modi, who curates the weekly newsletter "European Tech Weekly," summarizing funding rounds in Europe.

ServiceNow is a publicly listed enterprise SaaS company boasting a market capitalization of over $148bn and generating over $10bn in ARR. It is a massive enterprise platform, comparable in scale to Salesforce, Workday, Oracle, Adobe, or SAP. Despite its size, it remains a lesser-known story compared to its counterparts.

In this post, we aim to shine the spotlight on this fascinating business. We've divided the post into five sections: (i) key insights, (ii) company history, (iii) platform overview, (iv) operating and financial metrics, and (v) opportunities for founders interested in pursuing ServiceNow.

If you want to talk about ServiceNow or if you’re building something to go after ServiceNow, feel free to reach-out!

Part I - 12 Key Insights From Studying ServiceNow

TAM expansion

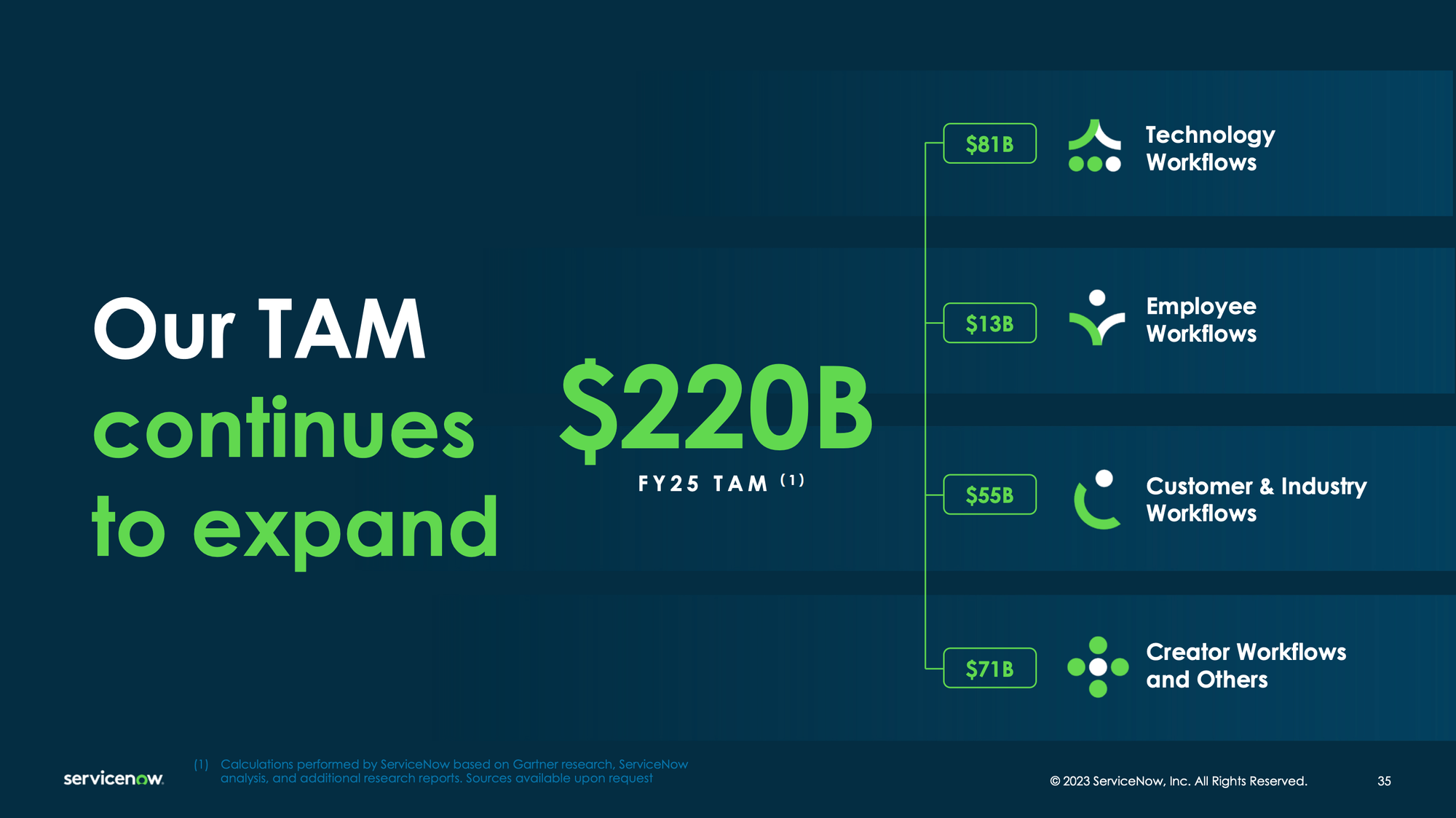

The best companies continuously expand their Total Addressable Market (TAM). ServiceNow initially entered the IT Service Management (ITSM) market, which was valued at only $1.5bn when the company went public in 2012. Since then, it has expanded into adjacent markets within the IT department, such as IT Operations Management (ITOM) and beyond the IT department to include departments like HR, CS, Security and Finance. It has also introduced industry-specific versions of its platform targeting sectors like healthcare, financial services or telecom. Today, ServiceNow has 4 main products (ITSM, ITOM, CS and HR) with sales exceeding $1bn each and the company is going after a $220bn TAM.

Infrastructure vs. Applications

Selling infrastructure without applications that deliver clear ROI to customers is challenging. From day one, ServiceNow's founding team envisioned building an agnostic platform for creating workflows within enterprises. They developed the platform and entered the market, but initially struggled to gain traction due to a vague value proposition. To gain commercial traction, they built their first application around IT Service Management (ITSM), leveraging their deep understanding of that market. Later, as their customers began using ServiceNow's products for purposes beyond their original scope, the company reintroduced its initial vision, enabling businesses to create customized workflows tailored to their needs.

Cloud vs. On-Premise

ServiceNow's initial wedge into the market was marked by offering a cloud-based and innovative ITSM product at a time when incumbents primarily provided on-premise solutions. Upon entering the ITSM market, ServiceNow found itself in competition with legacy players such as BMC, IBM, CA, and Peregrine, all of whom offered on-premise products and prioritized profitability over growth, often due to private equity backing. Similar to several SaaS giants like Salesforce and Workday, ServiceNow capitalized on the structural transition to the cloud to gain market share in the ITSM sector.

Partners’ Ecosystem

ServiceNow's sustainable growth at scale relies on a large network of 2.9k partners who resell and implement its platform. It wants its ecosystem to generate 3-4 dollars for every dollar in ServiceNow’s revenue. It maintains a broad network of consulting firms and system integrators, including KPMG, Accenture, Deloitte, IBM, and EY. These partners undergo training provided by ServiceNow and have commercial agreements with the company, enabling them to earn revenue through platform resales and implementations. ServiceNow operates a comprehensive education program called RiseUp, with the goal of upskilling 1 million individuals on its platform by 2024. These individuals are trained for various roles, including system administrators, support specialists, change adoption specialists, app developers, implementers, business process analysts, and technical project managers.

Bundling vs. Unbundling

Platforms tend to outperform point solutions, particularly in markets where budgets are tightening and customers seek to streamline their tech infrastructure. “93% of executives are consolidating tech vendor spend, favouring platforms.” ServiceNow is a compounding platform helping enterprise companies consolidate their IT stack. Offering 37 different solutions across 5 key functions (IT, security, HR, finance and CS), ServiceNow’s growth strategy primarily hinges on expanding into its customer base of Global 2000 companies. Despite challenging macroeconomic conditions over the past two years, the company has sustained robust revenue growth. This resilience is attributed to its value proposition centered around consolidating IT infrastructure by migrating various business workflows to ServiceNow, thus reducing reliance on multiple solutions.

Glue

ServiceNow's success stems from its role as the linchpin connecting various mega-platforms utilized by enterprise companies. Enterprises typically employ 4-5 key platforms (such as CRM, ERP, HRIS, and cloud providers), each confined to specific functions (e.g., sales for CRM). ServiceNow acts as the glue on top of these platforms to construct cross-functional workflows. ServiceNow often describes itself as the "system of actions" atop existing "systems of records." This unique positioning grants ServiceNow a formidable defensibility, as employees engage with its workflows on a daily basis.

Serial Acquirer with a different approach

ServiceNow has earned a reputation as a serial acquirer, completing over 30 acquisitions to acquire talent (e.g. in design or AI) or to expand into new product areas (e.g. observability, skills management, and business continuity). Unlike many SaaS platforms like Salesforce, Autodesk, or Adobe, ServiceNow adopts a unique approach when acquiring complementary products. Rather than integrating them as they are, ServiceNow opts to rebuild them from scratch, ensuring seamless integration into its platform and safeguarding against technical debt.

“When companies in our peer group try to pivot to other domains, they typically buy. We did not do that. We built internally, leveraging our single, unified platform to capture new domains (e.g. HR, customer service) within the enterprise. In the process, we evolved our approach to product management, which was critical to sustaining our organic growth story.” - Chirantan Desai (COO at ServiceNow)

Experienced Revenge Founder

ServiceNow was founded by Fred Luddy just two weeks before his 50th birthday. Before this venture, Luddy served as the CTO of Peregrine Systems, where he reportedly lost his entire net worth due to an accounting scandal (he was not involved). The founding story of ServiceNow serves as a compelling example that age is merely a number and that the second act of resilient founders can often be more impactful than their first.

Hunting Elephants

ServiceNow stands as a prime example of a company that has achieved remarkable success in hunting elephants. It strategically targets large enterprises as customers, boasting over 1.9k customers generating $1m in ACV. While many SaaS companies typically begin in the SMB or mid-market segments before scaling upmarket, ServiceNow defied convention by acquiring enterprise customers like Deutsche Bank and UBS right from the start.

Integrating Gen AI

ServiceNow perceives Gen AI as a catalyst for furthering adoption across all of the company’s digital workflow offerings and driving net dollar retention. Leveraging Gen AI, ServiceNow has achieved a remarkable 40% penetration of Pro+ offerings, which integrate this technology, resulting in a 25% average selling price uplift compared to the standard SKU. Moreover, the company has developed a two-pronged Gen AI strategy. First, a general-purpose approach that entails a connector/integration hub with OpenAI, already available today, with potential future collaboration with Google Cloud. Second, the domain-specific models approach, which involves leveraging open-source models trained on ServiceNow's use cases/workflows, supplemented by customer-specific data.

Capital Efficient Growth

ServiceNow has only raised $66m in VC funding and roughly $210m at IPO. It is a prime example of a business that scaled profitably even in private markets. It defies conventional wisdom that you need significant capital to grow, especially if you are targeting large enterprises due to longer sales cycles and R&D costs etc. While the software space has gotten more competitive over time, focusing on procuring large profitable contracts is also a potential option to fund R&D.

One Architecture Facilitating Product Velocity

“ServiceNow is a true platform company as the “entire product is built on one architecture, one code base, one data model so that the engineers can build great products on top of it” - CJ Desai, ServiceNow’s President & COO during 2023 Analyst Day

The fundamental unified architecture requires fewer engineering resources for new applications and drives ease of use when customers look to extend the Now platform to new workflows.

Hence, the platform inherently benefits from (i) higher innovation velocity, (ii) better R&D economics and (iii) faster time to value for customers. As an example, ServiceNow created and launched a new product called Hardware Asset Management in just 16 months by leveraging the platform's core capabilities. The company only needed 11 developers to create the first version of the solution and scaled it very effectively due to cross-selling with existing products.

Part II - History

Act 0 (2003-2005): The Path to PMF From the Vision to Be an Infrastructure Platform for Business Workflows to Reaching PMF with a First Application Focused on ITSM

Fred Luddy cofounded ServiceNow in 2003, initially under the name GlideSoft. Fred was previously CTO at Peregrine System from 1990 to 2003 operating in the IT Service Management Space (ITSM). During its tenure, Peregrine achieved a $4bn in valuation translating into $35m worth of shares for Fred. However, Peregrine went bankrupt in 2003 due to financial fraud.

“It was November 5th, 2003. I knew that we had to start a company before I became 50, because a 50-year-old can't start a company. So, at 49—November 24th is my birthday—we started.” - Fred Luddy (ServiceNow’s founder)

Until mid-2005, Fred Luddy was the only employee at ServiceNow focused on building the platform he had envisioned. At this point, he raised a $2.5m round from JMI, started to grow its team and commercialise its platform.

I had 12 customers during production, which was in the beginning of 2005. It took us 18 months and I had no employees. I had one $800 computer, worked out of a Teleco closet, and had a borrowed IP address. - Fred Luddy (ServiceNow’s founder)

Since its inception, Fred harboured the vision of constructing a workflow platform to assist enterprises in crafting custom workflows across various functions within their organizations. Fred developed the initial version of the platform and attempted to enter the market. However, he struggled to find product-market fit due to the forward-looking nature of his vision. He was frankly ahead of his time. To provide tangible ROI to enterprise customers, he pivoted to building the first application leveraging his platform. He began with ITSM leveraging his unfair advantage in the market, which was predominantly occupied by on-premise, slow-moving incumbents during the transition from on-premise to the cloud.

"We had this really great, simple platform for creating workflows, and we would go to people and say, Hey, you can do all these things with this, and they just weren't interested. So we went back and said, Okay, we say this is this great tool for doing things like IT-support management, so why don't we back that up and make an IT-support product?” - Fred Luddy (ServiceNow’s founder)

Act 1 (2005-2011): Scaling Exponentially the PMF on ITSM

In 2006, Glidesoft was renamed ServiceNow. Later this year, in Dec. 2006, it raised a $5m series B from JMI Equity.

In 2007, it opened an office in San Jose in Silicon Valley.

In Apr. 2009, it raised a $6m series C. In Nov. 2009, Sequoia led a $41.4m series D into the company.

Between 2005 and 2009, ServiceNow experienced exponential growth going from $0.85m to $5m (5.9x YoY) to $13m (2.6x YoY) to $28m (2.2x YoY) and to $45m+. It achieved this traction with only $7.5 million in venture funding and remained profitable from 2007 onwards.

Act 2 (2011-2014): Going Public and Scaling Beyond ITSM into the IT Department

“We asked Fred what valuation he wanted and we hit the bid. Zero negotiations. We had never seen references where a piece of software spread through organizations like this. At our first board meeting they beat plan by 70%. Second board meeting, everybody’s clapping — another huge quarter. But all of a sudden Pat Grady and I got very concerned, because it was clear the internal workings of the company weren't keeping up with these tailwinds in the market.” - Doug Leone (Sequoia)

In 2011, Frank Slootman joined as CEO and Fred Luddy transitioned to the role of CPO. Sequoia and Luddy collaborated closely to identify someone who could propel the company to the next stage of its journey. Frank Slootman restructured the go-to-market strategy and bolstered the product to focus more on enterprise customers, where the product-market fit was strongest. This strategic shift was crucial to ensuring the company's sustainable growth.

“ServiceNow was already at a $75 million revenue run rate; the infamous start‐up “chasm,” as popularized by management author Geoffrey Moore, had scarcely been a speed bump. Amazingly, the company had been bootstrapped with only $6–7 million in capital, and it had managed to put $50 million in cash on the balance sheet from operations. The company was still being run by its founder and CEO but was unduly controlled by its finance function: it was literally starving for resources. When I met the R&D department, it turned out that was just the founder and a handful of his cronies. On the P&L, R&D did not even break 2% of revenues. You would normally expect that percentage to be 15–20 times larger in a company at this stage of evolution” - Frank Slootman in Amp it Up

Between 2011 and 2014, ServiceNow expanded its total addressable market beyond ITSM selling complementary products to the IT department starting with IT Operations Management (ITOM). ITOM made sense because it had a larger TAM, the same buyer as ITSM, the workflow functionality at its core and it allowed ServiceNow to go deeper into the IT stack of its customers becoming the system of records for IT assets, services, infrastructure and applications (i.e. the configuration management database).

“I was focused on how ServiceNow could expand beyond its initial TAM. […] As I went through the CEO interview process with the board of directors, I kept hearing about customers who used the product in completely different domains than IT. […] It looked like this was a generic service management workflow platform that could be adapted for any service domain. Once we got beyond our urgent, short‐term operational challenges, we expanded the company from licensing just the help desk management staff to everybody in the IT function, a much larger universe of employees. The idea was that everybody in the IT department was involved in the workflow to resolve incidents. Not just the help desk but also system and database administrators, network engineers, and application developers. ServiceNow became a system of record as well as a system of engagement for the entire IT department. It was becoming the chief information officer's system. The expanded positioning enabled us to move higher in the customer's organization, do bigger deals, and truly become a strategic IT management platform for large enterprises. - Frank Slootman (Amp it Up)

Expanding beyond ITSM marked a pivotal turning point in the company’s history. While ITSM served as a solid niche to begin with, it represented a relatively small $3bn market in which ServiceNow was rapidly gaining market share. In 2021, ServiceNow had a 40% market share in this software category.

“Quite honestly when I joined ServiceNow, it was not too much on the ITSM opportunity. No offense, it was very interesting. But what really, really attracted me to ServiceNow is the opportunity to take the IT service model and make it an enterprise service model. And when I first started talking to Fred, he was flipping out one example after another in this company and that company where people have taken the IT service model and deployed it and repurposed it in all these different places. And that to me was really super interesting.” - Frank Slootman (2014 Analyst Day)

In late 2011, VMware tried to acquire ServiceNow for $2.5bn. Sequoia refused to sell the company and offered to buy the shares of any shareholders selling at this price.

In Mar. 2012, ServiceNow raised $28.9m in series E. In Jun. 2012, ServiceNow went public via IPO raising $210m at a $2.96bn market capitalisation. It also relocated its HQ to Santa Clara.

Act 3 (2014-2017): Finding PMF beyond the IT Department and Fully Realising the Workflows Platform Vision

Once [the expanded positioning as strategic IT management platform] was underway, we expanded even more by launching a half dozen business units in service domains outside of enterprise IT. They used the underlying ServiceNow software platform but adapted it for new uses at the application level. We now had unique products for each service area. I expected only a few of these service lines to make it, but they all caught fire, some more than other” - Frank Slootman (Amp it Up)

In 2014, ServiceNow started to expand aggressively beyond the IT department launching an Emerging Products division with in-house products in HR, customer service and security.

At this point, ServiceNow had to massively upgrade the UX/UI of its platform because functions beyond the IT department were much more demanding on that parameter. This became a top priority, prompting ServiceNow to acquire a design agency called Digital Telepathy in Oct. 2017 to bring more design talents to the team.

“What we arrived at was a singular focus on fashioning our rather industrial user experience to a consumer-grade service experience […] It was important to the company's future yet also hard because it required changing our DNA. Our customers were IT people who had a high tolerance for these rather industrial, not very user‐friendly experiences. The company had to forcibly move itself away from where it had come from.” - Frank Slootman (Amp it Up)

Act 4 (2017-today): Scaling Beyond the IT Department

In Feb. 2017, ServiceNow announced that John Donahoe would replace Franck Slootman as CEO. John Donahoe was CEO at eBay and CEO at Bain before joining the company. John arrived at a point where the diversification beyond IT started to take-off and needed to be consolidated.

In 2018, ServiceNow launched NowX as an internal incubator for developing new products with the ambition to release 2-3 new commercial products every year.

In May 2023, ServiceNow announced a strong partnership with Nvidia to deploy AI applications within ServiceNow’s customer base.

Act 5 (future): What Does it take to Build a $100bn Revenues Software Company?

Today, ServiceNow is generating $9.46bn in ARR in Q4-2023 growing 27% YoY. It managed to create a new software category in the IT stack for large enterprises being the glue between major IT platforms like SAP for ERP, Workday for HRIS and Salesforce for CRM. Additionally, it built two proprietary platforms for the IT department (ITSM, ITOM) and for the CS department.

As ServiceNow moves forward, the lingering question that some market research analysts had regarding the company’s ability to expand its TAM when it went public and was focused only in ITSM resurfaces. While ServiceNow has the potential to double or triple its ARR with its current product scope, reaching the $100 billion ARR mark will require exploring new avenues. Several paths seem available: (i) expanding more aggressively into applications by building an ERP or a CRM, (ii) going downmarket with a lighter version of the product and go-to-market, (iii) embedding AI into the platform to drastically increase its ACV by tapping into HR budgets and no longer software budgets.

Part III - Platform Overview

In the history section, we covered ServiceNow’s product expansion that can be summarised into 4 different steps:

Step 1: It started as an IT Service Management product which is a set of workflows and tools to deliver IT service management tasks like incidents, service requests, problems and changes more efficiently.

Step 2: It expanded into a broader IT platform called Digital Operations. Today, it also includes includes IT Ops Management (individual processes and services that are managed by an IT department), IT Asset Management (manage hardware, software, and cloud IT assets from a single platform), Application Portfolio Management (manage the application estate of the business) and Enterprise Asset Management (automate the full lifecycle of physical business assets).

Step 3: In 2014, ServiceNow went after most C-Levels beyond the IT department leveraging its platform to productise business workflows. It started in Customer Service, HR and security. Since then, it has also added finance, ESG and risk management.

Step 4: Today, ServiceNow is expanding its platform into 3 different directions: (i) selling its no-code/low-code platform to build internal apps, (ii) verticalising its products to certain industries (e.g. healthcare or telco) and (iii) embedding AI into its products.

Today, ServiceNow can be described as the “platform of platforms”. It helps companies to drive adoption of their historical platforms (e.g. HRIS, ERP, CRM) by digitising business workflows on top of these platforms. It also help companies to implement cross-platforms workflows (e.g. employee onboarding which requires actions in the HRIS and in the IT systems) acting as the glue between platforms which are used to operate in silos. On top of this positioning, ServiceNow has built two end-to-end platforms in IT and in CS where competition was weaker. It has also its no-code/low-code platform that can be used by employees and partners to create internal apps customised to the needs of each customers.

ServiceNow is a true platform company. Its “entire product is built on one architecture, one code base, one data model so that the engineers can build great products on top of it” said CJ Desai (President & COO) during 2023 Analyst Day. More specifically, at the core of its platform is a configuration management database (CMDB), which provides customers with a singular data model and contains information about all of an organization’s software and hardware assets and corresponding dependencies. Further, since inception, the platform was built using declarative (what to do) vs. imperative (how to do it) design principles. This enables fewer engineering resources for new applications and drives ease of use when customers look to extend the Now platform to new workflows. Hence, the platform inherently benefits from:

Higher innovation velocity. For instance, the company created and launched a new product called Hardware Asset Management in just 16 months by leveraging the platform's core capabilities.

Better R&D economics. To develop the Hardware Asset Management solution mentioned above, the company only needed 11 developers to create the first version of the solution. Another example is the risk product suite, which only needed 12 R&D personnel to launch and generates 250m in revenue 3 years post-launch.

Faster time to value for customers. ITSM product serves as a strong wedge for ServiceNow to cross-sell other products while ensuring that implementation is achieved much faster as the customers have develop competency of the ServiceNow platform.

Part IV - Operating & Financials Metrics

ServiceNow is the poster-child of the perfect venture backed SaaS growing exponentially towards $100m in revenues and IPO before finding a flywheel to sustain 20-30% annual growth at massive scale. Commercialisation started in 2005. It took the company only 6 years to reach $100m in SaaS revenues. It went public in 2012 and reached $1bn in sales in 2015 - just 10 years since product commercialisation. After this, it showcased durable growth despite being at a massive scale.

ServiceNow has been impressive at maintaining a strong annual growth rate at a massive scale. In 2023, ServiceNow reached $8.97bn in sales growing at 24% YoY including $8.68bn in SaaS revenues growing at 26% YoY. Since passing the $1bn revenue mark in 2015, it has managed to sustain a 30% CAGR. The durable growth is driven by best-in-class metrics with regards to (i) land (new net ARR), retain (renewal) and (ii) expand (upsell/cross-sell).

Part 1: Land. ServiceNow has 1.9k customers doing more than $1m in ACV and is adding 50-100 customers in this bucket every year. ServiceNow is also landing larger deals with new customers given the current breadth of its product suite. New customer ACV ($1m+ ACV) has increased 70% over the past four years with the number of products purchased in the first year increasing 30%.

Part 2: Retain. Service has a best-in-class 98-99% logo retention because it targets enterprise customers (Global 2000 companies) and is a very stick product as it is positioned as a critical system of actions.

Part 3: Expand with cross-sell & upsell. ServiceNow has c.125% net dollar retention rates driven by high attach rates.

Cross-selling new products and upselling to premium SKUs are driving growth as ServiceNow expands relationships with existing customers, where it sees the potential to grow total ACV 7x with its existing product set. 86% of new ACV coming from existing customers is a testament to the significant opportunity in expanding these relationships across multiple dimensions: quantity of seats/units, new applications, new buying centres and geographies.

ServiceNow’s best-in-class NDRs show that even with larger lands there is a significant opportunity to expand accounts. According to management, 85% of new business comes from existing customers. The expansion is also applicable to older cohorts as shown on the chart below. As an example, a customer that spent $100k with ServiceNow in 2010 is spending over $2.6 million with them today. That's 26x where they started, representing an annual growth of 191%.

ServiceNow has successfully diversified its revenue streams, expanding beyond the confines of the IT department and beyond North America. By 2023, IT accounted for only 55% of total revenues, a significant decrease from 89% in 2014. Similarly, North America's share of total revenues decreased to 64% by 2023.

ServiceNow is disciplined at keeping professional services to the minimum to maximise its valuation. Only 3.2% of sales are done by professional services compared with 17.6% in 2013. ServiceNow has built a strong ecosystem of 2.5k+ partners across the world in charge of implementing its platform. It uses professional services only for 3 reasons: (i) deploying key customers which absolutely want to be deployed by ServiceNow, (ii) building best in class deployment playbooks that can be taught to partners and (iii) iterating quickly with customers on newly launched products until you reach product market fit.

ServiceNow has been operating margin positive since 2019. In 2023, it had an 8.5% EBIT margin. If we look at the rule of 40 defined as ARR growth + NTM FCF margin, Service now has a 56% rule of 40 compared to 32% for the median of public SaaS companies tracked by Meritech and only beaten by Crowdstrike, Monday, Zscaler and Snowflake. ServiceNow can achieve a good balance of growth and profitability at scale due to durable growth and its inherent leverage in S&M and R&D.

ServiceNow has scaled aggressively its revenues without investing massively in R&D. In 2011, when Frank Slootman joined the company, ServiceNow was at a $75m revenue run-rate but was spending spending less than 10% of its revenues in sales and marketing which is extremely low for a venture backed company in exponential scaling mode. It shows the strong product market fit that ServiceNow had in the ITSM category. Nevertheless, it was a Damocles sword over the company that could have prevented it from expanding its TAM if Frank Slootman had not reinvested massively into the product to go into other IT products first and other functions second.

Disrupting the Disruptor: What are the Opportunities for Founders to Go After ServiceNow?

There are multiple routes to disrupt ServiceNow including:

Unbundling ServiceNow (e.g. Zip). ServiceNow is offering multiple products in 6 key areas: IT, security, finance, HR, customer service, risk and ESG. There is an opportunity to disrupt ServiceNow by building a more agile product (full stack or an orchestration platform) in one of these areas. For instance, Zip’s initial wedge was an intake-to-procure product to streamline the procurement process. It’s built on top of ERPs including Netsuite, Oracle and SAP Ariba. This product is similar to what ServiceNow is offering in its finance area. Oftentimes, challengers tend to also focus on a customer segment (SME, middle market or large enterprises) to provide the necessary escape velocity for a certain use case. As an example, Zip started in the SME/middle market segment and is now moving upmarket with their solution.

Building an open-source alternative. While ServiceNow offers extensive customization capabilities, it's not an open-source platform. Open-source alternatives could disrupt by offering similar functionalities with the added advantage of community-driven development, customization, and potentially lower costs.

Building verticalised versions of ServiceNow. In recent years, ServiceNow started to build industry specific versions of its platforms in industries such as the public sector, financial services, healthcare, telecommunications, media, tech and manufacturing. There is an opportunity to build vertical SaaS companies for mid-market and enterprise customers in a given industry which will deeply integrate into the IT stack of the industry and which will productise workflows running on top of this IT stack. You can go directly after ServiceNow’s industry specific versions because it shows that there is a market pull or you can go after other industries (e.g. construction, education, etc.).

Building a next generation low-code/no-code platform (e.g. Retool). Simplifying the development and customization process could be a significant disruptor in the ServiceNow space. Low-code/no-code platforms empower business users to create and customize workflows without extensive coding knowledge, reducing dependency on IT teams and accelerating time to value.

Building a ServiceNow for SMBs and mid-market companies (e.g. Atlassian). As we discussed, ServiceNow is targeting mostly Global 2000 enterprises creating an opportunity for players with a similar value proposition going after SMBs and mid-market customers. It’s an opportunity that Atlassian is already sizing with a go-to-market motion which is not sales led but much more product led.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Very well researched piece, learned a lot even though I thought I knew NOW well.

Thanks Alexandre,

It is very detailed while keeping simplicity to read/understand.

Very useful, you did a great job !