👶 Neobanks for Teenagers

Overlooked #12

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m talking about neobanks for kids and teenagers.

This week, Revolut announced the launch of Revolut Junior which is an new app and service dedicated to kids between 7 and 17 years old. The Junior account is connected to the Revolut app of the parents in which they can control the spendings of their children and wire them money instantaneously.

I like this new offering because it solves two key issues of other neobanks for children with (i) a differentiated acquisition strategy in which existing 10m Revolut customers will use Junior accounts for their kids, (ii) no uncertainty on what happens at 18 y.o. because of the natural shift from a Junior account to a normal account.

I strongly believe that teenagers behave differently than the previous generations and entrepreneurs who are able to size this difference could build outstanding businesses. It’s one of the numerous reasons why we invested into Yubo - a social network to help teenagers find new friends in live streaming rooms.

This is also true for finance. A new wave of startups building neobanks for teens all over Europe has emerged. I’m still uncertain on whether it’s a good opportunity for Venture Capital, but here are some insights on this trend and I will be happy to have your thoughts on the topic. Don’t hesitate to drop me an email (ade@idinvest.com) or answer to this newsletter.

GoHenry compiled its users data (75k children based in the UK between 6 and 18 y.o.) to publish The Youth Economy Report in July 2019. The report is amazing and the numerous testimonies from children are incredible. You should read it. Here are some key insights on how differently teenagers manage their money:

1/ Digital banking native generation. It is the first generation to have natively access to money the same modern way adults could enjoy today (online, card-based, contactless). Before that, pocket money for children was mainly cash based and it was impossible to understand behaviors.

2/ Pocket money is the main revenue source. In average, a British child earns £9 per week and this amount increases with age. Over half (51%) of the children receive their pocket money on a weekly basis and 32% on a monthly basis. Most parents give this pocket money at the end of the week either on Friday or Saturday before weekend activities. Only 17% of payments are rewards from traditional households tasks (e.g. washing the dishes, homework, brushing teeth, walking the dog etc.) I love the below graph giving the split depending on the task done.

Top kids' chore - Reward depending on the task done

Weekly pocket money paid by parents to UK children depending on their age

3/ Spendings vary depending on age and gender. Up to the age of 10, boys and girls spend most of their money on groceries (sweets and magazines). Between 11 and 15 y.o. girls will spend most of their money on clothes and fashion and boys on video games. After 16 y.o. both girls and boys will start spending predominantly in bars and restaurants. Before 11, most of the spendings are done with parents. After that, they are done with friends. Interestingly, 33% of total spendings are done online while 53% in brick and mortar store (vs. respectively 18% and 82% for adults). Only 14% of spendings is used to withdraw cash money in ATM. Not bad compared to previous generations who were only receiving and spending pocket money in cash.

The top 10 spending centers for Gen-Z

4/ Gen-Z is better at monitoring its spendings. UK children save £62 per year on average or £5,15 per month. It means that 13% of their earnings remain unspent, three times higher than the 4.8% UK Households Saving Rate. Gen-Z is growing in the aftermath of the financial crisis and is more conscious of the value of money.

1/ Europe fintech ecosystem is better than its US counterpart especially for neobanks. Revolut, N26 and Monzo are great success stories with respectively 5.8m, 3.5m and 2.4m users as of Q3-19. Nikolay Storonsky (Revolut founder) said that "We are three/four years more advanced compared to US companies in terms of product, in terms of regulation, in terms of size." European neobanks are even expanding outside Europe entering the US and South American markets.

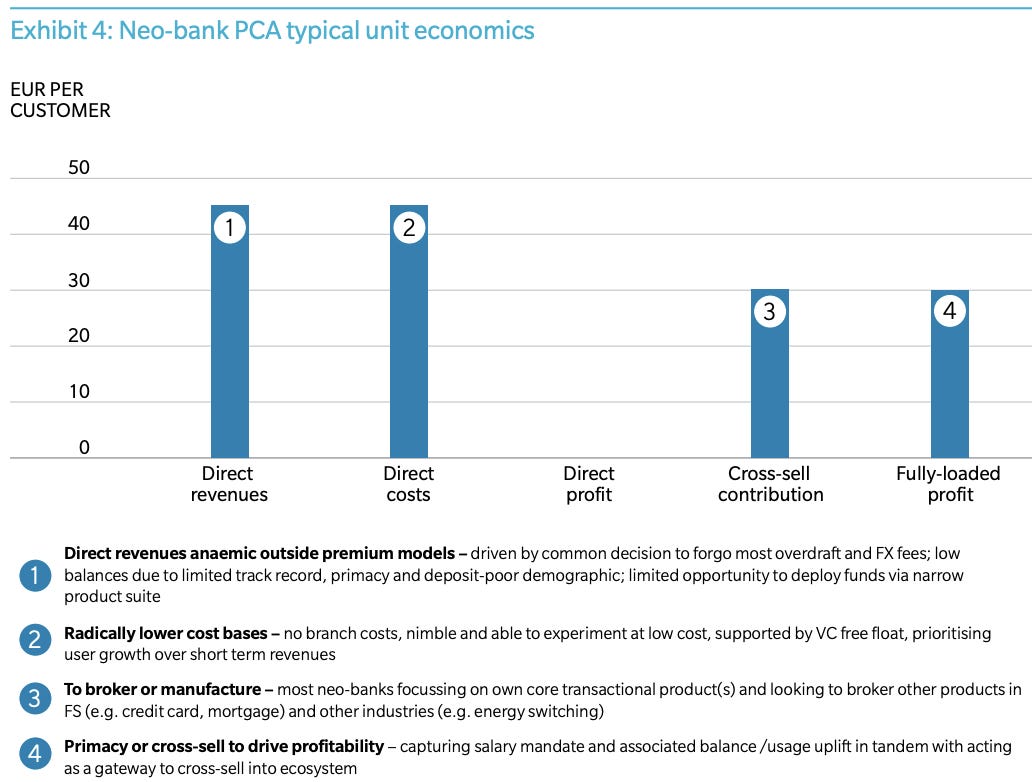

2/ Neobanks have different unit economics vs. traditional banks. A traditionnal bank current account is loss-making on a standalone basis. Reaching breakeven and generating profits are dependent on the ability to cross sell other financial products to customers. A neobank claims to operate at scale at a fraction of the cost compared to incumbent banks meaning that the current account is sufficient to breakeven expenses. Profitability remains dependent on cross-selling. Yet, these new unit economics are still not totally proven. Moreover, neobanks have other challenges: not all the customers are comfortable to have them as primary accounts, the deposit balances are rather low compared to incumbents.

3/ Europe has already experienced a wave of failed startups in this field. N26 initial pitch was to build a pocket money card for kids associated with a mobile app called Papaya. They pivoted towards more promising customer segments. Refering back to this idea, founders said that the market was too small and complicated compared to the huge opportunity to build a universal neobank. A neobank for teens called Osper was founded in 2012 in the UK. It received funding from tier 1 investors in 2014 like LocalGlobe, Index and Horizons Ventures. The company seems to be struggling with only 18 FTEs registered on Linkedin, a CEO who is not a founder, low and declining downloads and DAU numbers on Apptopia, and no funding round raised since then.

4/ Here could be some reasons:

Not enough money on their current accounts to break even the spendings and impossible to sell traditional financial products (e.g. mortgages).

Churn topic when children hit adulthood.

Timing: digital banking adoption was low 5y ago compared to today.

5/ Competition from neobanks will be fierce. (i) Revolut has launched its offer dedicated to kids (7-17 y.o.). Parents will control their children accounts from their current account and once kids turn 18 y.o., their accounts will be automatically converted to a traditional Revolut account. (ii) Monzo is already offering a full UK current account (contactless debit card, Monzo app, Apple Pay etc.) for teens aged 16-17 y.o. There are some spendings restrictions (e.g. gambling) but the limits are switched off when they turn 18 y.o.

6/ Key differentiators between competitors.

Cracking monetization. Two main positioning are possible: parents-focused or teens focused. In the former case (GoHenry, Pixpay), you can charge parents a monthly fee. In the latter case (Kard, Vybe, Gimi), you have to find other monetization sources (paid customization, insurance, teenagers spendings data, brand partnerships).

Ability to build a community of engaged users through Instagram, ambassador programs (Kard) or crowdfunding campaigns (Monzo, GoHenry).

Capacity to understand teenagers’ behaviors and build your features and growth strategy accordingly.

🗞 Neobanks Skeptic (Fred Destin, July 2017)

🗞 Europe is beating the US in fintech innovation (Sifted, July 2019)

🔎 The Current Account Conudrum (Oliver Wyman, 2018)

🔎 The UK Youth Economy Report (GoHenry, July 2019)

🎧 Alexandre Prot - De McKinsey à Qonto (GDIY, Nov. 2018, 🇫🇷)

🗞New apps are teaching children how to manage their money (The Economist, May 2019)

🗞Challenger banks eye the untapped teenage market (Sifted, Sep. 2019)

🗞The Pivot of N26 (Berlin Valley, Aug. 2016)

🗞Is Gaming the New Gambling (Anthemis, Nov. 2018)

Thanks to Julia and Maxime for your valuable insights!

See you next week for another issue! 👋

Looking to start your own digital bank / challenger bank / neobank with affordable investment and short timeframe? Then, I have good news for you. Here is the company you are looking for - https://optherium.com/digital-banking/

Optherium provides everything needed for the fast launch & effective management of your own digital bank in one place, including licenses, software, compliance, data protection, fraud prevention, dedicated technical and customer support teams, etc.

Turnkey Neobank by Optherium is a fully customizable and unhackable solution, backed with the EMI license in the EEA, banking license in the USA, and Brazil. Moreover, any 3rd party API’s and any new functionality may be easily integrated into the platform. It allows businesses to expand rapidly to any country in the world and also to create unique functionality for end-users.

This is the most advanced solution that exists on the market and the first neobank built by a cyber-security tech company. Thus, your business and users' data is fully protected from hacking and malicious insiders.

White-label Neobank allows businesses to save up to €5M on investments and 3 years of life on the development of the solution from scratch. With Optherium's turnkey neobank business can launch a digital bank in 1-3 months in the EEA and less than 3-6 months in any other country in the world.

White-label Neobank by Optherium is a revenue-generating tool, offering businesses customizable transactional and subscription fees are powerful sources of income for any enterprise.

Learn more - https://optherium.com/digital-banking/