💵 nCino - Cloud Banking Platform for Salespeople

Overlooked #138

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol.Today, I’m digging into another vertical SaaS called nCino which is a cloud banking platform to help salespeople working in financial institutions to originate loans and open bank accounts.

“A bunch of us went hunting in East Texas. […] Two guys went out and killed an alligator. About three weeks later, the hunting organisation told us that the alligator head was available. We decided to get it to put the alligator’s head into a conference room. We stopped thinking about it again until customers start asking “So what is this about?” Without thinking I said “Well, that means around here we eat the competition”. [It became a culture totem]. Last year, I gave each of my direct reports a little alligator head to have on their desk to remind them every day to bring their A-game in order to win.” - Pierre Naudé (CEO at nCino)

Beyond celebrating alligators, nCino is a singular venture success story:

It started as a spin-off of a traditional bank who remained the majority shareholder for several years. It was subsequently replaced by Insight who was nCino’s majority shareholder at IPO.

Like Veeva, nCino started as a verticalised CRM built on top of the Salesforce’s developer platform. It helps financial institutions’ salespersons originate loans and open bank accounts.

nCino went public in July 2020 at a $2.8bn valuation after raising from investors like Wellington, Insight, Salesforce Ventures and T. Rowe. Today, it’s trading at a $3.5bn market capitalisation and a $3.5bn EV implying a 7.7x EV/NTM Sales multiple.

nCino is another addition to my collection of vertical SaaS deep-dives. I previously covered companies like Toast, Procore, Olo, Veeva and Shopify.

I divided this post into the following sections:

Part I - History

Part II - Product

Part III - Metrics

Part IV - Main Learnings

Part I - History

nCino was started in Wilmington in North Carolina as an internal project in a US-based bank called Live Oak Bank which wanted to transition to the cloud.

In 2011, nCino was spun-off in order to sell the core banking system developed internally to other financial institutions. At the time, Live Oak was a majority shareholder.

In 2013, nCino raised $9m from angel investors.

In 2014, nCino started to sell its core banking system to customers in the US and raised a $10m series A from Wellington after tripling its annual revenues.

In Feb. 2015, nCino raised a $29m series B led by Insight.

In 2015, nCino expanded its product suite with a customer portal as well as with treasury management sales and onboarding tools.

In 2016, it launched a solution to streamline the account opening process.

In 2017, nCino made its banking OS available internationally and opened an office in London with a first customer called OakNorth Bank.

In Jan. 2018, nCino raised a $51.5m series C led by Salesforce Ventures

In May 2018, it launched a solution in retail lending.

In 2018, it opened an office in Australia.

In 2019, nCino expanded in Japan via a joint-venture and opened an office in Canada. It also launched nCino IQ which is a AI/ML layer on top of its bank OS.

In Oct. 2019, nCino raised a $80m round led by T. Rowe Price and Salesforce Ventures

In Jul. 2019, it acquired Visible Equity for $73.2m which is a financial analytics and compliance SaaS.

In Nov. 2019, it acquired FinSuite for $11.5m to improve its AI/ML product.

In Jul. 2020, nCino went public at a $2.8bn valuation raising $270m.

In Nov. 2021, nCino acquired SimpleNexus for $1.2bn. It’s a US-based cloud based and mobile-first home ownership SaaS. It’s used by all the stakeholders involved in a real-estate transaction (financial institutions, real estate agents and borrowers) in order to streamline the mortgage application process.

Part II - Product

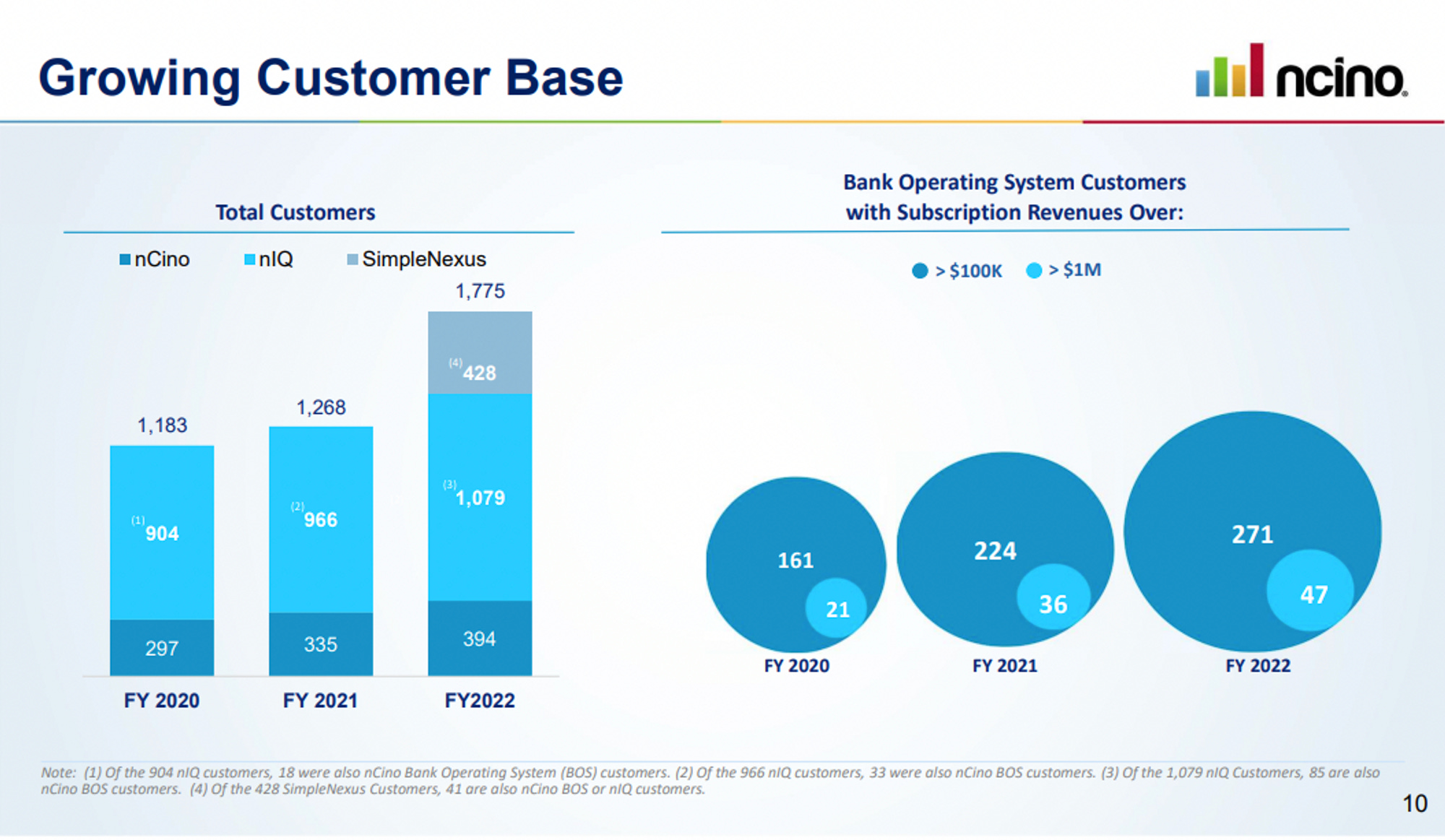

nCino is a bank operating system used by 1,750 financial institutions including Wells Fargo, BNP Paribas, OakNorth Bank, Barclays and Santander. It’s used by employees across business lines (mortgage, retail banking, SMB banking, large corporate banking, asset financing & leasing).

Its core product is a verticalised CRM built on top of Salesforce’s developer platform and adapted to financial services specific workflows. It helps salespeople originate loans, open accounts and manage customer portfolios. Around the CRM, nCino provides financial institutions with additional modules such as business intelligence, enterprise content management, compliance & risk management, nCino IQ (using AI/ML for automations, forecasting and data recognition).

nCino brings efficiency to its customers both increasing revenues while reducing operating costs. It also gives a unified view of the business which enables financial institutions to personalise the customer experience and to take data-driven decisions. nCino helps small and medium financial institutions to compete with the largest banks (e.g. Bank of America, JP Morgan, Citi, Wells Fargo) and digital first banks which are massively investing in technology by maximising every touch-points they have with all existing and potential customers. nCino also reduces the complexity of its customers’ tech stack as it replaces 7-15 custom built or point solutions.

In Nov. 21, nCino acquired a company called SimpleNexus for $1.2bn. SimpleNexus had $54m in ARR, 163% in net retention rates, 41k loan officers as users, 300 employees and 400 customers. It helps streamline the mortgage application process for all the stakeholders involved in a real-estate transaction (real estate agents, financial institutions and consumers).

Part III - Metrics

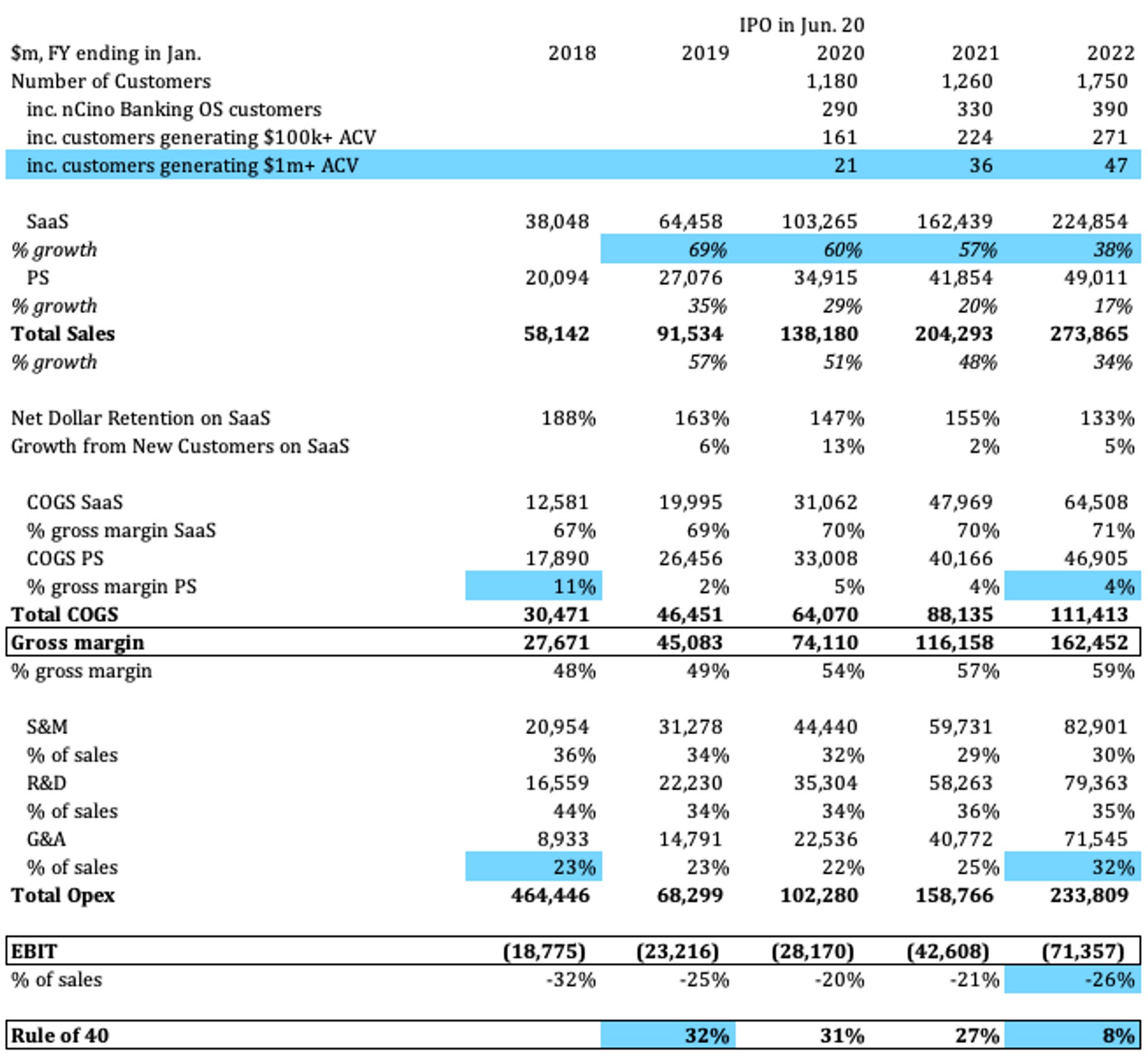

In 2022, nCino generated $225m in SaaS revenues growing at a 38% YoY mainly driven by existing customers with a 133% net dollar retention on SaaS revenues.

nCino serves mainly enterprise customers: it has 271 customers generating more than $100k in ARR and 47 of them are even generating more than $1m in ARR.

nCino is a SaaS with low gross margins (59% in 2022) compared to most SaaS business driven by two factors: (i) 18% of its revenues is coming from professional services on which nCino has a 4% gross margin and (ii) nCino is built on Salesforce which is capturing a significant part of the SaaS gross margin (70% gross margin on SaaS in 2022).

nCino has good gross and net retention rates. It has a land and expand go to market strategy. It starts by installing a point solution (e.g. loan origination, deposit account opening, nIQ AI modules) in a given area of the bank (e.g. commercial banking, SMB banking, mortgage) before expanding by adding other solutions and other areas in the bank. In 2020, it had a 97% gross retention rate and a 147% net retention rate. nCino is a sticky product with high switching costs as it’s a record system and it takes 6-18 months to implement the solution. Moreover, nCino has a strong natural expansion potential because it bills 30% of annual contract value at Y1, 80% at Y2 and 100% at Y3.

nCino is still unprofitable with a $71m operating loss.

nCino is not as cash efficient as direct peers Veeva and Olo which are also vertical SaaS serving enterprise customers. It overspends versus its peers in sales & marketing (30% of total sales vs. 17% for Olo and 16% for Veeva) and it has been consistently below the rule of 40 (8% in 2022).

Part IV - Main Learnings

nCino is selling to enterprise customers. It only has 1.2k customers. It has 271 customers generating more than $100k in ARR and 47 customers generating more than $1m in ARR. nCino has long sales cycles (6-18 months) and long delivery cycles (3-18 months). It works with integration partners (e.g. Deloitte, Accenture) to handle the delivery.

nCino is a platform “built by bankers for bankers”. It’s another proof-point that industry expertise matters in vertical SaaS. It’s easier to sell a product when you built it internally in a bank before selling it to other financial institutions.

nCino is operating in an industry with favourable dynamics. Like healthcare for Veeva, finance is a highly profitable and regulated industry. As a result, customers are more willing to spend on software and the need for an industry expert is higher to tackle regulation specificities.

nCino is built on top of Salesforce’s developer platform and has strong ties with Salesforce.

nCino uses Salesforce’s core CRM modules (lead generation, account management, opportunity management, dash-boarding). nCino customises Salesforce’s modules to adapt them to the financial industry. nCino goes also beyond Salesforce in the sense that it manages the steps beyond customer closing with tasks such as client onboarding, deposit account openings and loans origination.

nCino has a partnership with Salesforce that will last until 2027 and Salesforce is an important shareholder in the company with a 13.2% ownership at IPO.

nCino is an authorized Salesforce reseller. It can resell Salesforce to certain financial institutions, mostly small banks and community banks (less than $5bn in assets) that don’t have pre-existing relationships with Salesforce.

At the same time, I don’t think that it has always been a rosy relationship. For instance, Salesforce has built its verticalised solution to go after the financial industry.

nCino’s “why now” was mostly about building a modern vertical SaaS replacing a fragmented tech ecosystem with siloed, closed and on premise tools with a cloud based and open platform.

Insight leveraged its unique edges to turn nCino into a massive financial success. Contrary to most VC funds, Insight is an extremely flexible investor. At IPO, it owned more than 50% of the company. It did not hesitate (i) to clean the cap. table by buying shares from the bank that was behind nCino’s inception, (ii) to hold common shares in the business and (iii) to give full autonomy to the management with only 1 board seat even as a majority shareholder.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋