Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a mapping of European vertical SaaS. I collaborated with Louis at Point Nine to build a database of 452 European vertical SaaS companies. We showcased those that raised more than $5 million on a map and derived key statistics and insights.

Methodology

We focus exclusively on vertical SaaS as “software digitizing workflows in a given industry.” We don’t take the broader definition, which we call “Vertical Software 2.0,” which includes B2B Marketplaces (more details in this post).

We first built a database of 452 European vertical SaaS companies and examined funding amounts to understand the ecosystem’s maturity level. There are so many companies now that the database is only partly complete; we hope this post is just a starting point to build a more comprehensive overview. If you’re running a Vertical SaaS company and we missed you, please write to us here. We’ll publish an updated version soon.

Second, we reduced our sample to the 257 European vertical SaaS companies that have raised more than $5m as a (somewhat arbitrary) measure of success. We have showcased these companies on the map and computed a few stats to derive conclusions about these businesses.

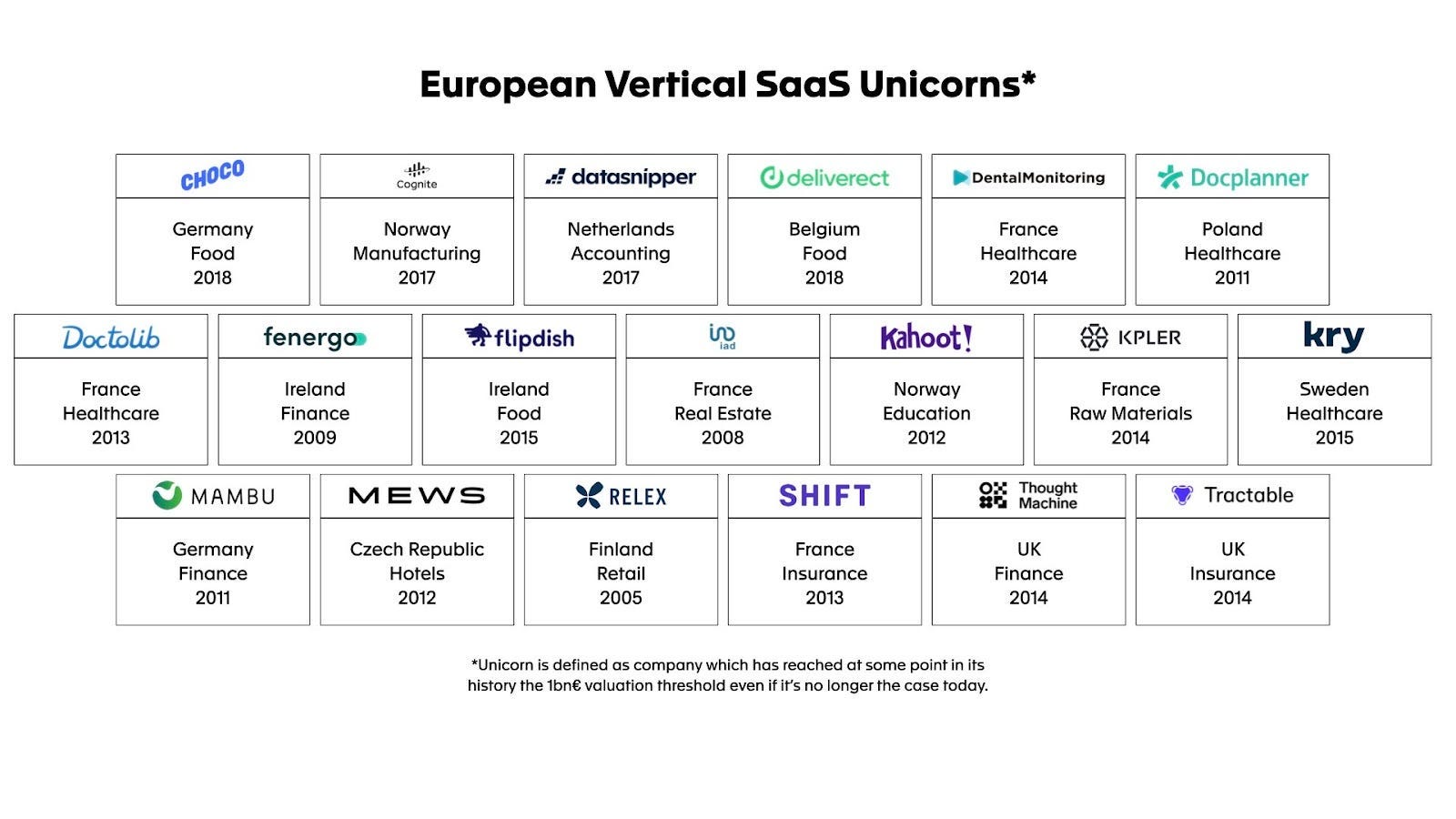

Third, we looked closer at the 19 European vertical SaaS unicorns in our database to understand their expansion journeys and funding paths to unicorns.

Maturity of the ecosystem

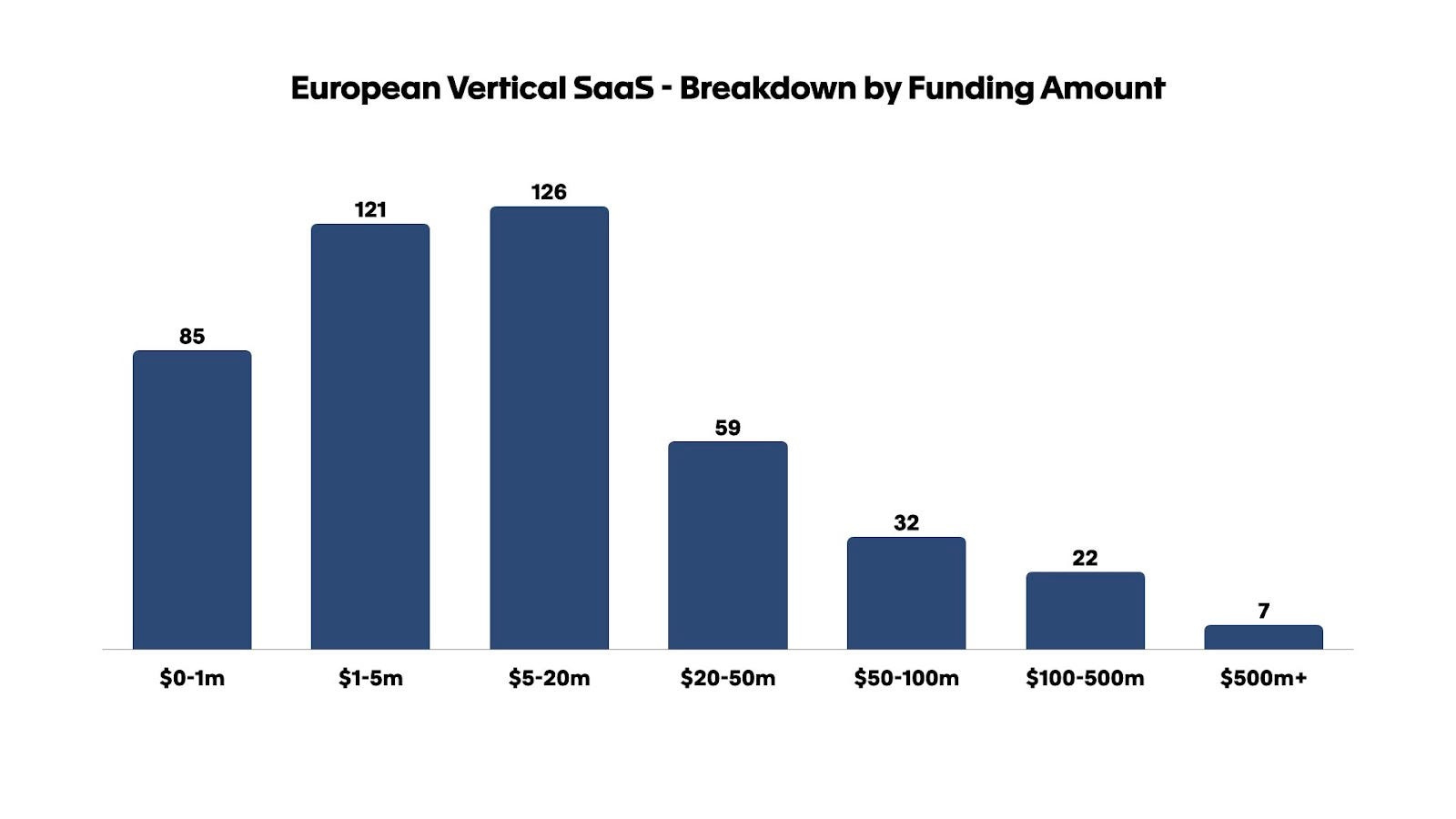

Of the 452 European vertical SaaS businesses in our database, 374 have raised more than $1m, 257 more than $5m, and 124 more than $20m.

Only 30 companies have raised over $100m, and 7 have raised over $500m. These are Doctolib (healthcare), Relex (retail), Fenergo (finance), Kry (healthcare), Thought Machine (finance), Shift (insurance) and Kahoot (education).

Based on our database, in the past 15 years, the number of European vertical SaaS created yearly has increased from 10–20 companies between 2011 and 2015 to 40–70 companies between 2016 and 2021. There’s obviously a survival bias in these stats. However, our day-to-day observations confirm the data: the number of Vertical SaaS companies created yearly is increasing. For companies started between 2022 and 2024, we’re waiting to have them appear on our radar.

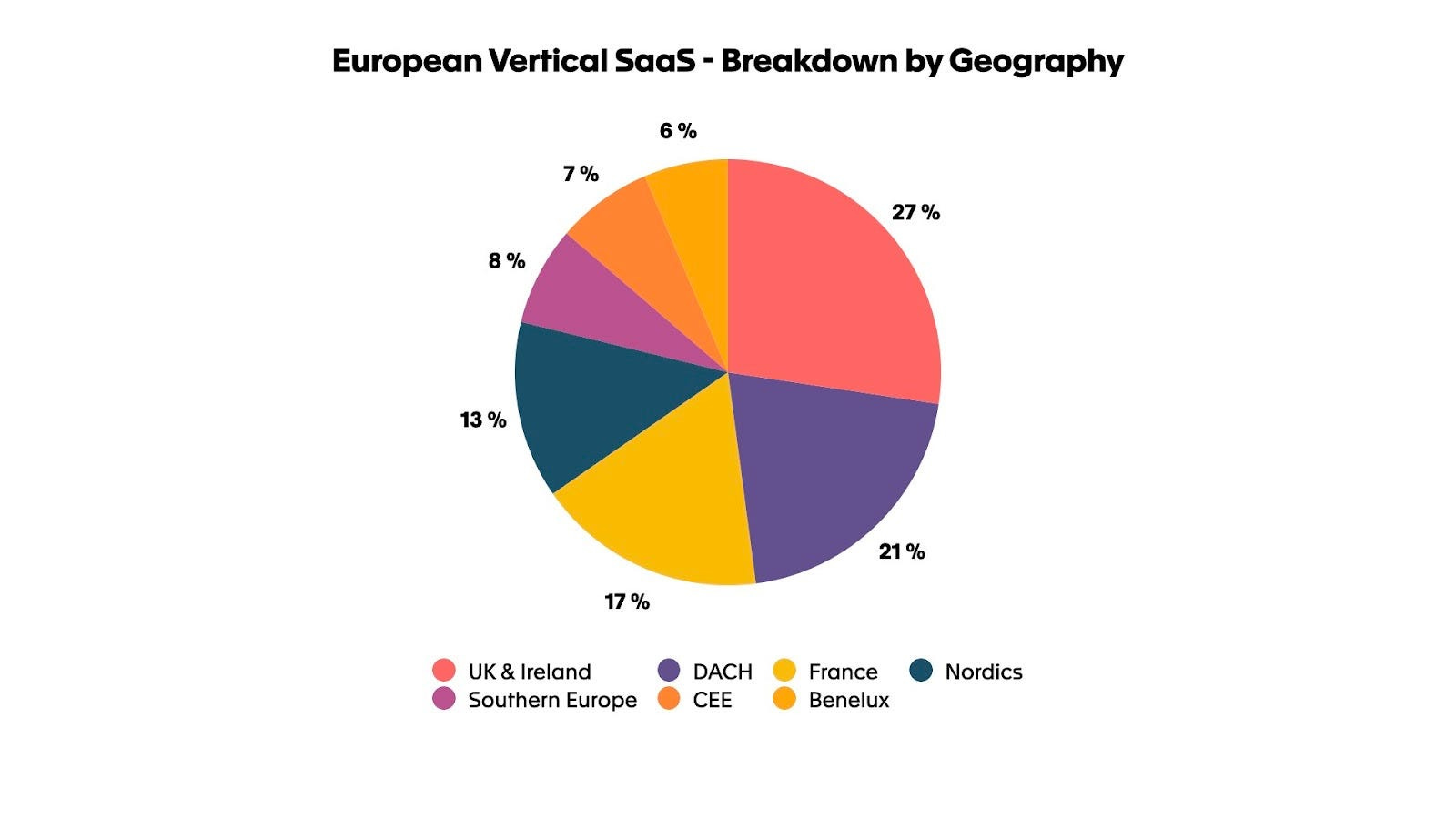

The geographical split of these vertical SaaS businesses reflects the European tech landscape more broadly, with the UK (113 companies), Germany (73 companies), and France (79 companies) being the most represented countries in our database (the 3 countries combined represent 58.5% of the total).

The map

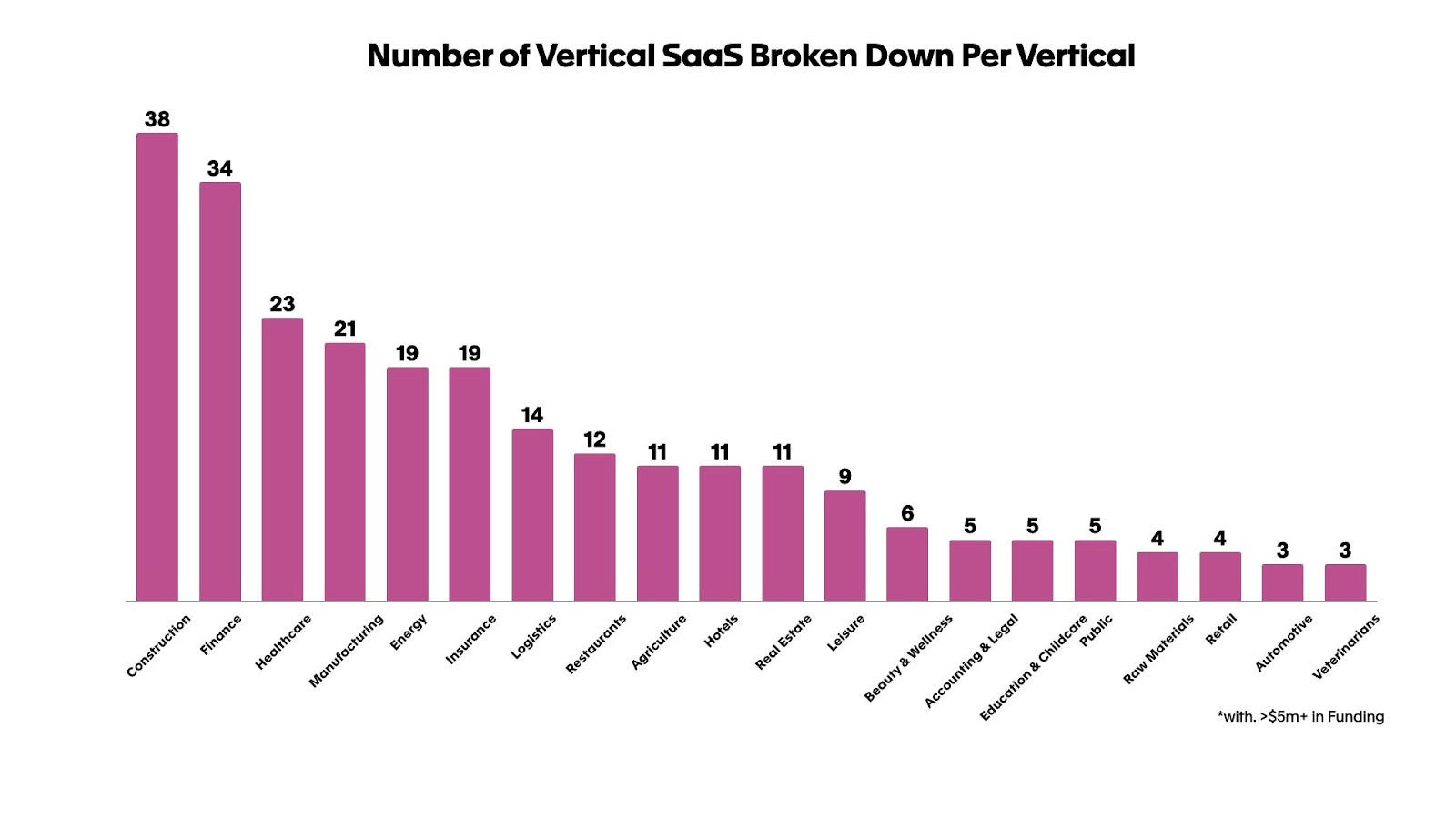

We have divided the map into 19 different sectors: energy, public, healthcare, raw materials, agriculture, real estate, finance, insurance, education, leisure, beauty, accounting and legal, logistics, manufacturing, hotels, restaurants, automotive, retail, wholesale, e-commerce, and, construction.

Construction (38 companies), finance (34 companies), and healthcare (23 companies) are the most represented verticals, accounting for 37% of the companies showcased in our mapping.

When it comes to the total amount raised by industry, healthcare ($2.7bn raised), finance ($2.7bn raised), and insurance ($1.3bn) are amongst the better-funded industries. On the flip side, agriculture ($0.2bn raised by 11 companies in our database) and construction ($0.9bn raised by 38 companies) are less well-funded verticals compared to the number of startups they attract.

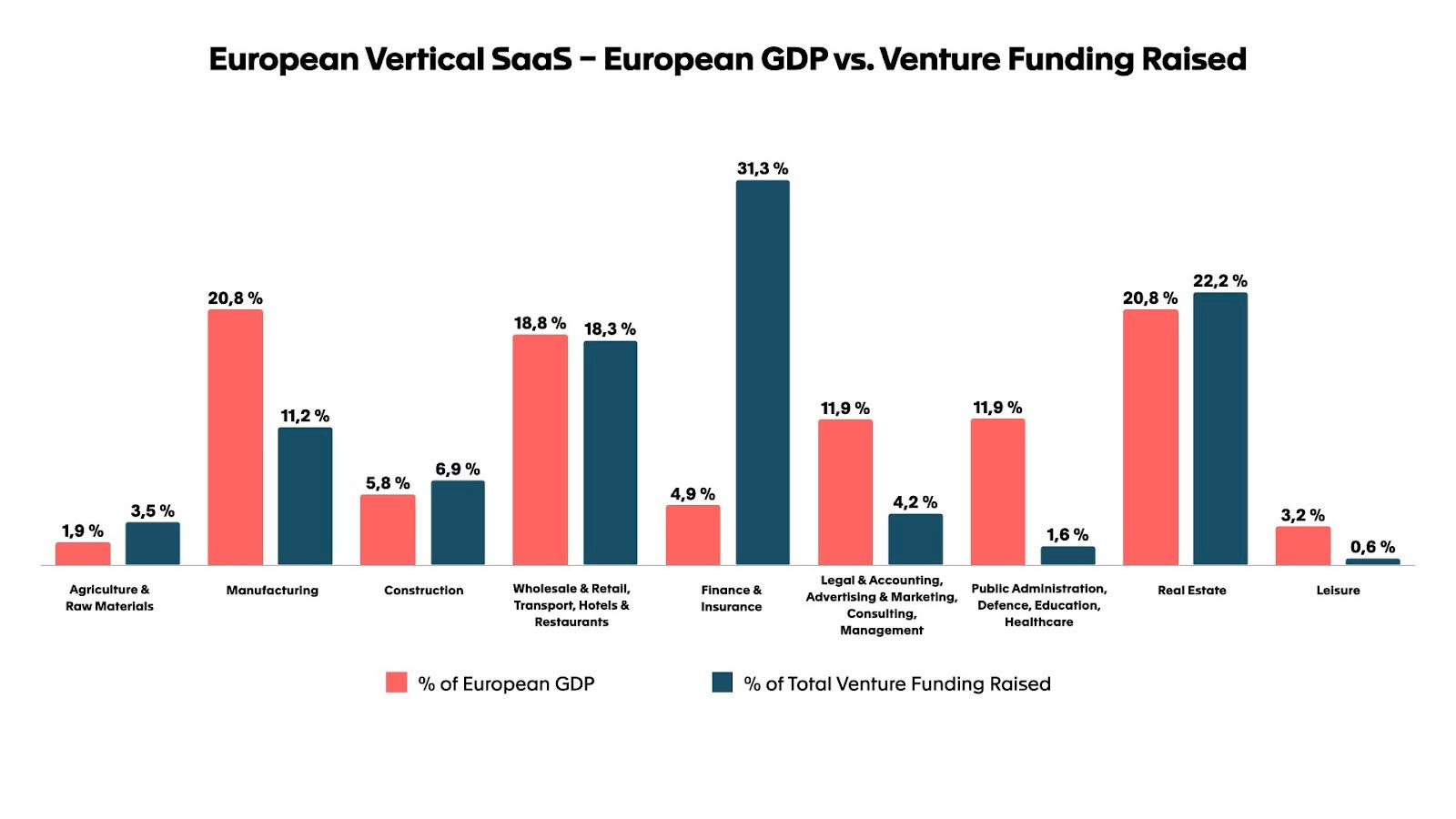

We also wanted to compare the total amount of venture funding per industry to the importance of each industry in Europe’s GDP. To that end, we have compared our industry split to a breakdown of the European GDP by industry, which you can find here.

As the graph above shows, we observe that finance and insurance (31.3% of the total amount raised vs. 4.9% of total GDP), public administration, defense, education, and healthcare (mostly driven by healthcare, 22.2% of the total amount raised vs. 20.8% of total GDP) are well-funded verticals compared to their importance in Europe’s GDP.

Manufacturing, real estate, and white-collar services seem to be less of a priority for VCs compared to their GDP contribution. However, the broader adoption of AI and / or robotics should spur a new wave of investment into these sectors and bridge the current gap.

Zooming on European Vertical SaaS Unicorns

There are 19 vertical SaaS unicorns in Europe. Healthcare (4 companies), food (3 companies), finance (2 companies), and insurance (2 companies) are the most represented verticals.

Some sectors, such as food delivery (Flipdish, Deliverect), greatly accelerated during the pandemic. SaaS multiples have compressed since then and with weakening market tailwinds, it might take time before these sectors live up again to their “COVID valuations.”

In Europe, a vertical SaaS company’s median “time to unicorn” is about 8 years (3.8 years for the fastest one, Deliverect, and up to 12.9 years for Fenergo and IAD).

Looking at the amount raised, €232m is the median amount in funding needed to reach a unicorn valuation (€93m for the most capital-efficient one, Datasnipper, and €754m for the most capital-intensive one, Relex).

There seem to be two main funding paths for vertical SaaS businesses in Europe. One path is to fundraise like a typical venture-backed startup, raising back-to-back funding rounds every 12–36 months (e.g. Docplanner, Tractable, Deliverect). Another path is to leverage vertical SaaS’ inherent capital efficiency due to lower competition intensity and more targeted sales & marketing efforts to bootstrap your way to a significant revenue milestone (€1–10m ARR) before raising your first round of capital (e.g. Fenergo, Kpler, Mews, Datasnipper).

Conclusion

The vertical SaaS ecosystem in Europe started a long time ago with companies such as Relex (2005) and Fenergo (2009). Two decades later, we believe we are still at the inception of value capture. On the one hand, some verticals lag behind when it comes to digital penetration relative to their GDP contribution. New technologies like sensors, AI, or robotics should accelerate that digitization. On the other hand, vertical SaaS are becoming increasingly multi-faceted. By integrating financial services, building a marketplace, and/or adding AI, we believe that some of them will be able to capture even more value moving forward. This is the logic of our Vertical Software 2.0 post.

That’s it for this first edition of the map. We look forward to making it even more comprehensive and continuing our learning journey in this ecosystem. Next week, I’ll publish another post with more recent learnings on vertical software.

We would like to thank everyone who helped build the database, including Clément Vouillon, Robin Dechant, David Guérin, Andreas Helbing, Javier Valverde, Michele Foradori, Hadrien Comte, Pierrick Cudonnec, Michael Lavner, Tobias Reimann-Dubbers, Federico Maroli, Michael Droesch, Patric Hellermann and Cecilia Manduca.