👩⚖️ How is the Ongoing AI Revolution Affecting the Legal Tech Industry?

Overlooked #164

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a guest post from my colleague, Carole, about the legal tech industry. I believe it’s a post worth sharing for two main reasons. First, it provides more insights into a vertical that I have not yet explored in this newsletter. Second, we’re convinced that it serves as a great case study for considering how the current AI revolution will impact vertical solutions. If you’re building something in this space or are seeking a sparring partner to exchange views on the legal tech industry, feel free to reach out to Carole at cdufretay@eurazeo.com.

In this paper, we will explore the impact of the current AI revolution on the legal industry. While legaltech has historically faced skepticism from VCs, the rise of AI has created new opportunities for future success stories in the industry.

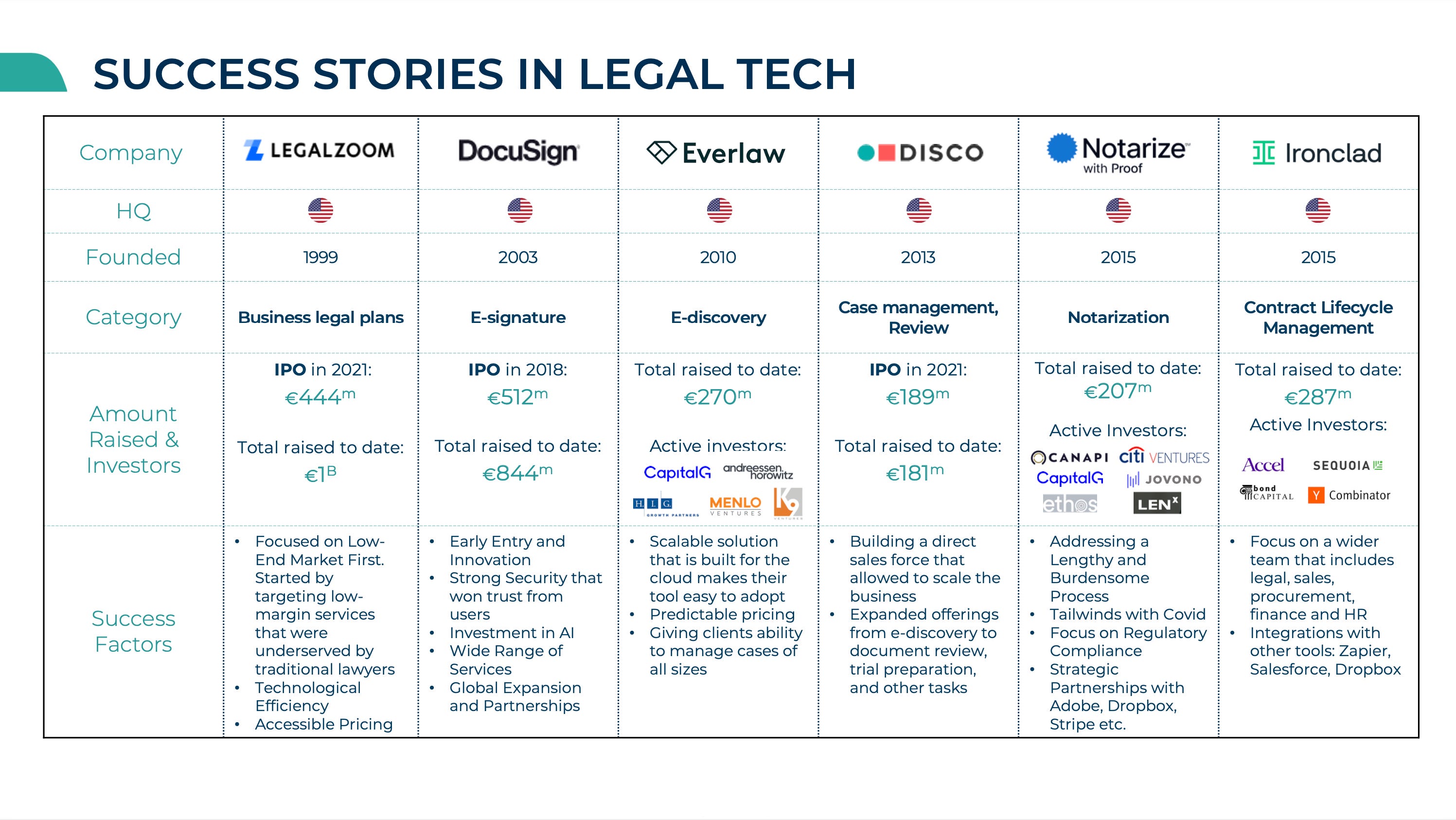

Legaltech startups faced several challenges over the years, including slow adoption from law professionals, difficulty to present a clear ROI, data security concerns, and integration with existing systems. However, these challenges have not prevented several startups from creating billion-dollar outcomes including LegalZoom, DocuSign, Clio, and Disco.

Today, there are key factors contributing to a renaissance in legaltech, including the rapid digitization post-covid, a generational shift amongst lawyers and a heavy focus on efficiency gains and a rising competition on low-value / high-volume contracts. The ongoing AI revolution elevates this renaissance to another level.

There are four main trends that we’re excited about in legaltech:

The use of generative AI for contract creation and management,

Research tools in general as well as their application in case prediction and dispute resolution,

Legal co-pilots and how they change the basics of the work on a day to day,

IP filing and management.

We divided this post into the following sections:

Part I - Why LegalTech has Historically Been a Challenging Area for Venture Investments?

Part II - LegalTech has Already Generated Several Successful Venture Outcomes

Part III - There is an Amazing Momentum to Build a Legaltech Startup

Part IV - Breaking Down the LegalTech Market

Part V - LegalTech Trends to Watch-Out (Contract Creation, Research & Litigation, Co-Pilots, IP Management)

Part VI - What are the Key Success Factors to Build a Successful LegalTech Startup?

Part I - Why LegalTech has Historically Been a Challenging Area for Venture Investments?

Legaltech has historically been slower to adopt technology compared to other functions such as human resources and finance for several reasons:

Slow adoption from law professionals. There is an inertia when it comes to adopting tech tools in the legal industry. This could be partly attributed to the ageing workforce in the industry, accustomed to traditional tools.

Unclear ROI. A clear demonstration of ROI is vital, and it is not always easy to assess. Due to the current macroeconomic environment, this is even more important. This is especially the case when selling to large international law firms, who operate on a billable hour model. Hence, if a solution cuts how much firms bill without presenting a way to make back that revenue, it can become harder to sell the solution.

Data security concerns. Legal departments handle sensitive information, and clients expect their data to be protected at all times. As companies adopt new tools, the risk of experiencing security breaches rises, which puts pressure on legal tech providers.

Integration with existing systems. Integrating legal tools within a firm’s existing software and systems is not easy, especially given the huge amount of legal data and security checks needed. Ensuring seamless compatibility and data transfer between different tools requires some implementation and migration time. The simpler the integration, the better. Historically, law firms have tended to use Office 365’s suite, and hence some of the most successful products have been those that have integrated with it.

Investors could also add other challenges such as low barriers to entry, long sale cycles, and crowded markets… but let’s not stop here and let’s dig deeper.

Part II - LegalTech has Already Generated Several Successful Venture Outcomes

Part III - There is an Amazing Momentum to Build a LegalTech Startup

Legaltech has now reached an inflexion point driven by several factors:

Rapid digitisation post-Covid-19. As a result of Covid-19 restrictions, progress that would have normally taken years was achieved in just weeks (introducing video court hearings, law firms adapting to remote working, remote access to legal documents, etc.)

Generational shift. As is often the case with vSaaS solutions, there is an ongoing generational worker shift in the legal industry with younger practitioners joining the workforce and accessing management positions. They are more eager to adopt digital products to improve their productivity

Be more efficient or die. Many legal tasks are low-value and high-volume like signing a NDA. These tasks can be automated and legal firms have to automate them if they want to stay competitive and leverage them to sign higher-value missions.

Gen. AI. AI legal tools used to lack accuracy and precision. Most legal documents are long, use complex language, and intentionally bury key clauses. Because legal work requires a high level of precision, it has always been more challenging for computers to understand those documents compared to day-to-day human language. However, recent AI breakthroughs, such as LLMs, now allow machines to understand and analyse text with human-like fluency. Gen. AI is a natural fit for an AI disruption because legal tasks are highly valuable, and a high percentage of tasks can be accomplished by AI.

Part IV - Breaking Down the Legal Tech Market

Market Sizing

In 2022, $23.5bn was spent on legal-tech. This market will grow at a 9.1% CAGR to reach $47.2bn in 2030.

In the US, there are 450k law firms and 1.3m lawyers compared to 50k law firms and 1.2m lawyers in European Union and the UK. In the US, companies spend 0.40% of their revenues on legal compared to 0.24% in the UK.

55% of lawyers work in law firms and 37% in companies’ in-house legal teams, but between 1997 and 2017 US in-house law departments have grown 7.5x faster than law firms.

Breaking Down LegalTech Categories

To have a better understanding of the legal tech sector, we have broken it down into its main categories:

Contract Lifecycle Management: it entails the creation, execution, and analysis of legal contracts. Typically, this process is fragmented as it involves using multiple tools. The primary users of CLM systems are legal teams, but they can also be used by other departments, including sales, HR, procurement, finance, and operations teams.

Legal Research: used by lawyers to prepare winning strategies and provide better advice to clients. Traditionally, legal research was conducted manually using a law library, books, periodicals, indexes, and digests. With the advancements in language processing and search engines, legal research is done almost exclusively online. The primary uses of legal research are fact-finding, fact-organising and fact-confirming, where they integrate citation checkers.

E-Discovery: digital investigation that attempts to find evidence in email, business communications, interviewing key stakeholders, reviewing case facts and other data that could be used in litigation or criminal proceedings. Another important aspect of e-discovery is data security. Due to the sensitivity of information cloud solutions, they must have strong security controls.

IP Management: software designed to help organisations manage and protect their IP assets. Intellectual property includes creations such as inventions, designs, symbols, names, and images used in commerce. This includes filing & approval, portfolio management, compliance monitoring, collaboration and communication, risk mitigation, search and analysis, reporting and analytics.

Practice Management: software to support the delivery of law firm services: onboarding, payments and e-billing tools, AML compliance, time recording, or managing activities, etc.

Legal Relationship Management (CRM): solution tracks all contact data, communication and case history details to enable legal professionals to keep track of a client's journey. Importantly, it enables firms to manage client intake processes to aid business development.

Consumer Marketplaces: helping people and businesses take care of their legal needs entirely online. Legal services marketplaces are able to match people and businesses with a lawyer based on their needs and budget. This provides flexibility and transparency.

Notarisation & e-Signature: official fraud-deterrent process that assures the parties involved in a transaction that a document is authentic and trustworthy. Due to the pandemic, electronic notary and signature software has become more widely used. This type of software has several benefits, such as saving time and resources that were previously allocated to the notarisation process, providing audit trails, and supporting the data integrity of sensitive documents.

Part V - LegalTech Trends to Watch-Out (Contract Creation, Research & Litigation, Co-Pilots, IP Management)

1. Gen.AI native CLM

What does the traditional CLM (Contract Lifecycle Management) market look like?

Most traditional CLMs like ContractPodAI, Ironclad and Evisort were founded between 2012 and 2020. CLMs were initially created to help with a process that was hyper-fragmented as it involved using multiple tools. This creates friction and inefficiency in the process. For example, contracts could be drafted using MS Word, shared via email, negotiated, signed using eSignature tools, stored in shared drives, and then tracked in Excel spreadsheets. CLMs would help with that, being a great workflow tool to assist and analyse existing documents and data but not particularly tackling the creation part efficiently, where the new generation is much more focused on.

Double-clicking on the structure CLM historical market

Limited market for CLMs: Our research showed that most companies globally do not actually have a CLM and have no plans to implement one. CLMs are not as popular as CRMs, which is one reason why there are so few unicorns in the legal technology space. Most companies do not feel the urgent need for a tool like this, where implementations take, on average, 6-12 months. Also, tools are generally expensive and require multiple stakeholders to adapt their traditional workflows. The global CLM market was valued at $1.3bn in 2022.

Highly fragmented but crowded CLM landscape: In addition to the lack of adoption of CLMs, the industry is also very competitive and highly fragmented, with no clear market leader. There are over 100 CLMs in Europe.

The Generative AI Revolution

Many new players focus on supporting the entire document lifecycle, from automatic contract creation to review, execution, and managing obligations, or choose to focus on a specific part of the workflow.

This category is adjacent to traditional CLMs but much more focused on the contract piece and leveraging Gen AI and, hence, what we believe is really powerful.

For instance, RobinAI is a pioneer in this category in Europe:

RobinAI is a UK-based startup founded in 2019 which aims to make contracts simpler and faster for law firms and internal legal teams through 3 main products: draft, review and query. Additionally, it enables teams to store contract data and query relevant information, either replacing CLMs or being a layer on top of a usual contract database.

One of the strengths of RobinAI relies on the access to contract language from thousands of contracts and the proprietary dataset that they established over the last few years (through various contract types), making their AI solid and accurate. Indeed, they create, in collaboration with their clients, negotiating playbooks that the AI will use to draft and negotiate contracts. Because RobinAI captures all corrections made within the system, they continuously improve their AI and partner with Anthropic for their LLM capacity.

They also recently launched an AI chatbot that enables users to obtain insights from the documents and also see the references from case laws.

But could existing CLMs (Contract Legal Management) add those Gen. AI features and win the race?

Can historical CLMs incorporate LLMs into their product offering and use their distribution advantage and a sticky client base to sell those across the legal market faster than the newer pure AI players?

Yes, they are well-positioned & have been on the market for longer…

Indeed, more traditional CLMs have been on the market since the 2010s and gained the trust of some law firms. Moreover, given that CLMs are the host of customer data, it can be challenging to churn and migrate that data to other providers. In addition, law firms are more and more focused on leveraging their current software stack better. Hence, existing players are expanding the capabilities of their products to stay competitive.

For instance, Ironclad released a Contract Management AI in early 2023 using Gen AI & GPT-4 to analyse contracts, flag areas that require review and provide suggestions… It is going to be interesting to follow their journey and new product features. We can expect a few CLMs adding Gen AI features but we believe that there is a blue opportunity for a pure AI player.

… Older CLMs are limited in adopting Gen AI in their core value proposition, and hence stay behind in terms of product depth, accuracy and quality especially in the contract creation piece

For those first-generation CLMs to integrate deep adoption of AI, it will require them to pivot slightly away from their core CLM product, where it is already challenging to cover the large surface area of client requirements, and would need:

Team of software engineers and optimise their architecture to integrate and exploit AI

Access to leading foundation model providers like OpenAI and Anthropic

Proprietary data to train advanced models

Indeed, LLMs, out of the box, are not capable of tackling many of the most rudimentary legal problems. It’s mainly when LLMs are paired with highly relevant proprietary datasets that they begin to meaningfully address the day-to-day issues legal teams face. Any documents are the legal property of the clients, and they always need to ask for their customers’ consent before using any data or feeding any kind of LLMs.

Also, even though CLMs are used by a proportion of lawyers, they are not so much adopted by internal legal teams, hence overall a low penetration rate until now which for us does not represent a big threat or barrier to entry for new Gen AI native comers.

In a nutshell, as previously stated, the CLM market isn’t a new space and remains highly fragmented while being very crowded. We personally believe that there are a lot of opportunities for new players and don’t see CLMs as competitors, being different enough in their core value proposition. It is possible that, in reality, those AI-first solutions or co-pilots will sit on top of CLMs (in the cases where customers have one) & on top of all the other tools that lawyers use, at least in the first instance. Law firms and internal legal teams have historically been quite frustrated with their tech stack and are keen to try and test some new solutions which is a good opportunity for new players with a AAA product.

2. Research, Litigation & Case Prediction

Empowering users to make better and faster decision making with full context (both leveraging their own internal data at a company level and external public legal data)

Knowledge search engines help search for legal documents, cases, and other relevant information. It’s an essential process yet a time-consuming aspect of work. Given a high-quality dataset, LLM-powered assistants can now efficiently summarise critical points and identify relevant case laws. Junior lawyers can then check the appropriate cases are true (not hallucinating), which is a considerable saving of time. This is partly possible thanks to how the data is embedded in vector databases.

It can be used either for:

Public legal data in general, with the likes of Doctrine or more recently Atla (YCS23) selling to internal legal teams in companies such as N26,

Or for internal use, to efficiently search inside very long legal documents using keywords where the tool can understand the overall context.

Here, you usually need both codes of laws (published books that are public) and court records (public, but most of the time you also need to partner with governments to get more granular data that you need to then anonymise.)

Atla is an example of an interesting company leveraging high volume of data to answer specific questions with context. Atla (YCS23) positions itself as a “helpful and honest legal AI assistant”. Their primary focus is on synthesising information and acting as an AI assistant for in-house legal teams, especially for startups or scaleups, to tackle any questions or legal advice they would need for the new launch of a product for example… Hence helping to cut external spending and accelerate decisions. Their algorithm breaks down complex questions and uses ML to extract key info, adding references to the relevant sources of information used to get more context on the topic or question at hand.

A common use case of research tools is also helping with case prediction & dispute resolution

Legal professionals are able to optimise legal research but also strategy, document review, and assess case strength. It helps in the form of case prediction as well as detecting trends in historical judgments and applying these to the case at hand, analysing the likely potential outcomes.

Players include Lex Machina, Solomonic CourtCorrect, EvenUp or SettleIndex which supports with predictions and helps corporates, law firms and insurers with their modelling tool to figure out when best to settle or take a case to court in order to maximise the best outcome.

Another one is Case Law Analytics, part of Eurazeo’s venture portfolio, which was recently acquired by LexisNexis (August 2023). It is a French legaltech company specialising in the modelling of legal risk and judge biases, founded in 2017. It creates mathematical models that rely on AI and in-depth legal expertise & data to simulate the legal reasoning deployed in a given situation and analyse the risks associated with a litigation case or a contract.

Here, a machine can analyse much more than a human can with a full view of the overall environment.

A more recent player is Wexler, which is based in the UK. Wexler helps litigators at law firms and in-house compliance, tax, and HR teams carry out their fact-finding and case preparation. They leverage LLMs to create timelines from any documents for any contentious matter, creating a source of facts for every case.

3. AI Legal Co-pilots / Assistants

In the future, one can picture a life with a series of AI agents to assist workers in their daily lives and work tasks. This can also apply to legal teams. A Co-pilot will serve as a layer of deep legal intelligence that can interact with other tools, applications, and customer data.

Instead of jumping between applications, the Co-pilot can interact with CLMs or contract databases to locate contracts. Rather than using Word, the Co-pilot can use relevant templates and playbooks and update them to reflect the latest legal developments. Instead of querying a legal research database, the Co-pilot can interact with the relevant system to find accurate cases that are meaningful to the problem at hand.

This is Harvey’s long-term plan in the US. The company raised from OpenAI and Sequoia and has a contract with Allen & Overy to deploy the solution in all their offices. They were founded last year and raised over $25m. In the same space, there is Casetext with their tool CoCounsel, which was acquired by Thomson Reuters in the US for $650m in June 2023. CoCounsel is an AI legal assistant, focusing now on document review, research memos, deposition preparation… Both players primarily focus on common law (based on judicial decisions compared to civil law, which is adopted in most European countries).

A few companies are emerging in Europe, positioning themselves as co-pilots/assistants, tackling one step or a few steps of the workflow, usually either starting with research or litigation as mentioned above (Wexler.ai, Atla or LegalAI) or with contract creation (Genie AI, Jimini or Legalfly). We expect most of them to develop more and more features to be as horizontal as possible while being deeply integrated into legal workflows.

GenieAI has an exciting approach, mainly targeting small to mid-size companies to empower not only in-house lawyers but also operations managers to draft some contracts, leveraging templates across many use cases: commercial, employment, IP & Data, etc.

Another company in the space is Jimini. Founded in 2023 in Paris, they aim to become an AI co-pilot enhancing lawyers’ capabilities on multiple tasks: legal research, review of long & tedious documents, and drafting. The founding team has experience in building legal businesses and is targeting law firms as well as in-house legal teams.

Last but not least, LegalFly is an AI co-pilot for litigation, contract review & drafting based out of Belgium. The co-founders do not come from a legal background but from a product one (being at Tinder & Match Group before) and hence have a product-first mindset, which shines through in how they build their company. Not only are they creating and deploying a suite of tools that fit users’ needs very accurately, but they are also building a community of tech-savvy lawyers ready to use AI, who have become their main cheerleaders.

It’s interesting to see those vertical plays of Gen AI, building various products for legal workflows where the user won’t have to navigate between multiple tools between their legal research and their drafting piece.

4. IP Management

What is IP Management and what is the current state of the market?

Every day and everywhere, incredible creators inspire us by shaping the future of innovation. They want to protect their ideas and innovations, but unfortunately, the infrastructure that intellectual property (IP) runs on currently does not do justice to the innovation that flows through it. The number of patents and trademarks has been increasing worldwide. WIPO has recorded the highest level of international patent applications in 2022, totalling 278k (WIPO Patents, 2023) and more than 30m IP applications (across patents, TMs and Designs) are filed globally. Despite challenging economic conditions during 2022, firms around the world continued to invest in innovation and intellectual property. The market size for intellectual property management software was $8.2bn in 2022 and is expected to grow to $25.0bn by 2031 (13.2% CAGR).

Existing workflows are manual and cumbersome

However, manual and cumbersome tasks consume a significant amount of valuable time and cost in the IP process. This includes exchanging data worldwide by emails or letters and updating records in point solution applications by endless manual data entries. This friction makes innovators and IP professionals waste their time, talent, and skills. Significant portions of the IP budgets are wasted on completely irrelevant activities and reliance on outdated platforms and manual labour.

When creating and filing for a trademark or patent, you must go through many steps. First submission of the disclosure or brand name, checking what exists and what does not in various databases, planning your filing strategy across various jurisdictions, drafting your initial patent/trademark application in compliance with various national/regional laws and rules, translation of the application into various languages to enable the filing in other jurisdictions, and paying a renewal fee in each country where you file the patent/trademark. In addition, you need to find the right people to work with in other countries (having a strong network is important), quoting, pricing, payments and billing, paying the FX, docketing (data entry), and managing the end-to-end IP lifecycle that needs to be carried out every single day with no room for errors or disruption. Hence, as an IP professional, you need to fulfil all these steps and keep track of all activities and deadlines by managing an end-to-end IP lifecycle with no room for errors or disruption.

Many workflows are examples of how workload-heavy dealing with IP is:

i) Patent renewals are typically paid annually in most countries (with some exceptions), so there is a constant need to monitor and renew, which makes it complicated when dealing with large portfolios

ii) IP Professionals currently only outsource certain aspects of the activities in the IP lifecycle (e.g. prior art search and renewals)

iii) IP rights need to be sought in every single country, which is why you need to develop relationships with partners across borders.

There is lot of room for many exciting opportunities in the IP management software and services space

Over the years, there have been a few acquisitions and consolidations in the sector, with big players such as Clarivate which acquired CPA Global in a $1.6bn (DCAT, 2020) and Corsearch, which acquired Incopro in 2021. Another established player is Questel, part of Eurazeo’s PE portfolio and one of the leaders in IP and Legal Operations.

Today, the possibility of using AI to automate many of the steps, starting with drafting the patent application, is fascinating. Advancements in LLMs present an opportunity to speed up patent applications and facilitate the workflow from beginning to end while also making it cheaper by notably heavily reducing the need for lawyers to spend expensive time on repetitive tasks and instead focus on the actual value-adding tasks. This will be of enormous benefit to founders and in-house counsels, especially in spaces like DeepTech, BioTech and Pharma.

Moreover, IP data is getting more accessible, and Patent and Trademark Offices are also becoming more digitised, which helps the new players revolutionise this quite outdated market.

Recent players in the IP space include Digip, IPRally, Greyscout or RightHub. A player like RightHub positions itself as the infrastructure for IP (like an Amadeus for travel). They facilitate the communication and workflow of corporates/inventors and lawyers (agents), which is still done archaically, inefficiently, and costly. The platform provides a workspace where industry stakeholders can transact and work with colleagues and firms across the globe in a modern, efficient and effective fashion. This eliminates a lot of manual work that is currently done by administrators – saving costs for firms. Their aim is to build an integrated platform that combines a community, IP portfolio management and a marketplace across the IP lifecycle.

“The Intellectual Property space is the lifeblood of innovation. I’ve been in the IP space for 20 years, building software solutions and tech-enabled services for law firms and corporates. The objective has always been to bring down the time, cost, and risk in the most common activities in the IP lifecycle, which in turn will enable innovation and broader protection thereof. However, the way the IP industry still operates is very fragmented, out-of-date platforms and does not really solve the real pain point of the customers. The current ecosystem is closed off which does not allow for any real change or true innovation to take place in the industry. All the efforts are being spent on adding more features into the already heavyweight point solutions that businesses and law firms use. With the increasing digitisation of the Patent and Trademark Offices, availability of data and APIs as well as cloud computing, a whole new world is open to truly create some real value and fundamentally change how extremely costly and risky administrative activities are being carried out today”. - Toni Njim, CEO & Founder of RightHub:

Part VI - What are the Key Success Factors to Build a Successful LegalTech Startup?

A well-thought GTM is essential to distinguish yourself from the crowdedness of the market as well as to avoid very long sales cycle. We believe that the approach of targeting the in-house legal team is very interesting.

The billable hours business model of law firms means they have fewer incentives to reduce time-based billing. However, given the rise of competition, more and more clients ask for a transition from hourly billing to upfront packaged legal solutions (despite lawyers arguing that they are not fully aware of how much time is needed and hence even more eager to get tools that will make them more efficient). Our research has led us to believe that most companies actually do not have any software, even CLM tools, and are actively looking to invest in some AI legal tools to support them.

Going after internal legal teams also means there is a flywheel effect. The internal legal team can be a great way to work your way backwards towards large law firms while having a generally shorter sales cycle. In-house lawyers can be the biggest cheerleaders if they see the value in the products.

However, one worry about the internal legal team is that their budget can be lower for such tools (except for the likes of FTSE100). When looking at the drafting & negotiating use case, some legal teams outsource to legal providers that do contract reviews, like Ontra for private markets, and competition on price for those low-value contracts can begin.

Gen AI and real tech expertise will be crucial differentiators in order to get the most accurate tool. The use of LLM & strong proprietary data that can train the model by accessing data from thousands of contracts or law cases is key. Moreover, the ability to capture all corrections made within the system to consistently improve accuracy & potentially style personalisation for each customer is a big plus.

However, a data breach is the worst threat for a legal firm & any legal tech needs to be careful with privacy policies when training their model. When selling to law firms, startups need to understand each firm’s data policy and reassure them about data breaches. A lot of start-up pitches don’t insist enough on data compliance, and hence, potential customers can be scared that it won’t fit within their IT system.

Some recent legal tech companies chose to use some open-source LLMs (i.e. Llama), which can be less powerful than using proprietary data and closed-source LLMs, but a strategic choice over the long-term race: they have one model per customer which keeps the data private, or through only using vector databased and anonymised data.

A solid legal network can also make a difference in this crowded market. Either by having a founder with previous experience in law and/or recruiting top profiles from the legal industry. Doing so can not only help secure leads more efficiently but also gain the trust of clients in a risk-averse industry. If that’s not the case, creating a community of power users with law professionals who are tech-savvy and want to introduce AI in their field of work will be key.

Something rising is also the ability to extract value from legal documents: give visibility on obligations, spending, and risks of the company and help with the overall firm strategy.

Conclusion: How Far will AI Tools Impact the Industry?

Overall, we believe that repetitive tasks & low value-added tasks will be replaced by AI to free up lawyers’ time. The question remains whether AI will also be used and trusted for more complex and high-value contracts.

However, there will always be a human in the loop at some point in the workflow.

Law firms and legal teams will never completely trust and rely on the machine, given the nature of their work. Therefore, AI legaltech will always stay a tool that empowers (but does not replace!) the users - no matter how strong the AI gets (compared to other sectors where AI applications can be much more automated, i.e. customer success or art generation).

According to lawyers, they expect their junior intake to reduce from 50% as juniors will be able to do tasks quicker, and firms will shift the hiring to more specialised and tech-savvy roles.

It also comes back to the logical question of who holds the liability, and it is true that this has not been helped by the hallucination stories that happened over the last few months. The use of an LLM-powered assistant raises an important issue and area of weakness of current iterations of AI (i.e., the recent scandal surrounding the use of Chat-GPT, which produced non-existent cases and quotes). Hence, there is a need for verticalised players and a focus on explainability, transparency and honesty.

Thanks a lot to my colleagues Aby, Alex, Briac and Tara for their help on this article, to Ved, passionate and expert in legaltech, and to all the amazing founders I have met along the way.

Hi! I'm Harshith. Really loved your post. It breaks down LegalTech very clearly. I write on VC and Startups in the LegalTech sector as well. My latest post breaks down the biggest M&A transaction in the LegalTech space so far. Check it out down below. Let's connect!

https://harshithviswanath.substack.com/p/breakdown-of-clios-acquisition-of

👏