🎨 Figma's IPO - S-1 Breakdown

Overlooked #202

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m digging into Figma’s S-1 ahead of its upcoming IPO.

On July 1st, Figma publicly filed its S-1 to list on the New York Stock Exchange in the coming weeks, aiming to raise up to $1.5bn.

In September 2022, Adobe agreed to acquire Figma for $20bn valuing the company at c.50x EV/ARR. However, the deal was terminated in December 2023 following anti-trust pushback in Europe and Adobe paid Figma a $1bn termination fee. Since then, Figma has more than doubled its business and aggressively expanded its product suite to become a true multi-product platform.

It will be fascinating to see where Figma starts trading. It’s arguably the strongest software company to go public since Klaviyo in September 2023, and I would not be surprise if it debuts at a valuation higher than Adobe’s acquisition offer. While the average SaaS company is trading at 8.6x EV/ARR (implying a $7.8bn EV for Figma) its rapid growth (46% YoY, no SaaS in the public market is growing faster than Figma) should command a significant premium. I expect Figma to trade closer to 20-30x EV/ARR in line with high-growth peers like Cloudfare, Axon and Crowdstrike suggesting a potential enterprise valuation between $18bn and 27bn.

In this post, I share my key insights from reading Figma’s S‑1, along with a high-level overview of its operating and financial metrics.

Key Learnings From Figma’s S-1

Figma is a best-in-class venture backed business.

Qualitatively, it’s a founder-led, clear category leader in product design (with an almost monopolistic position) aggressively expanding into adjacent markets such as whiteboarding, slide creation, website building, app building, and content marketing.

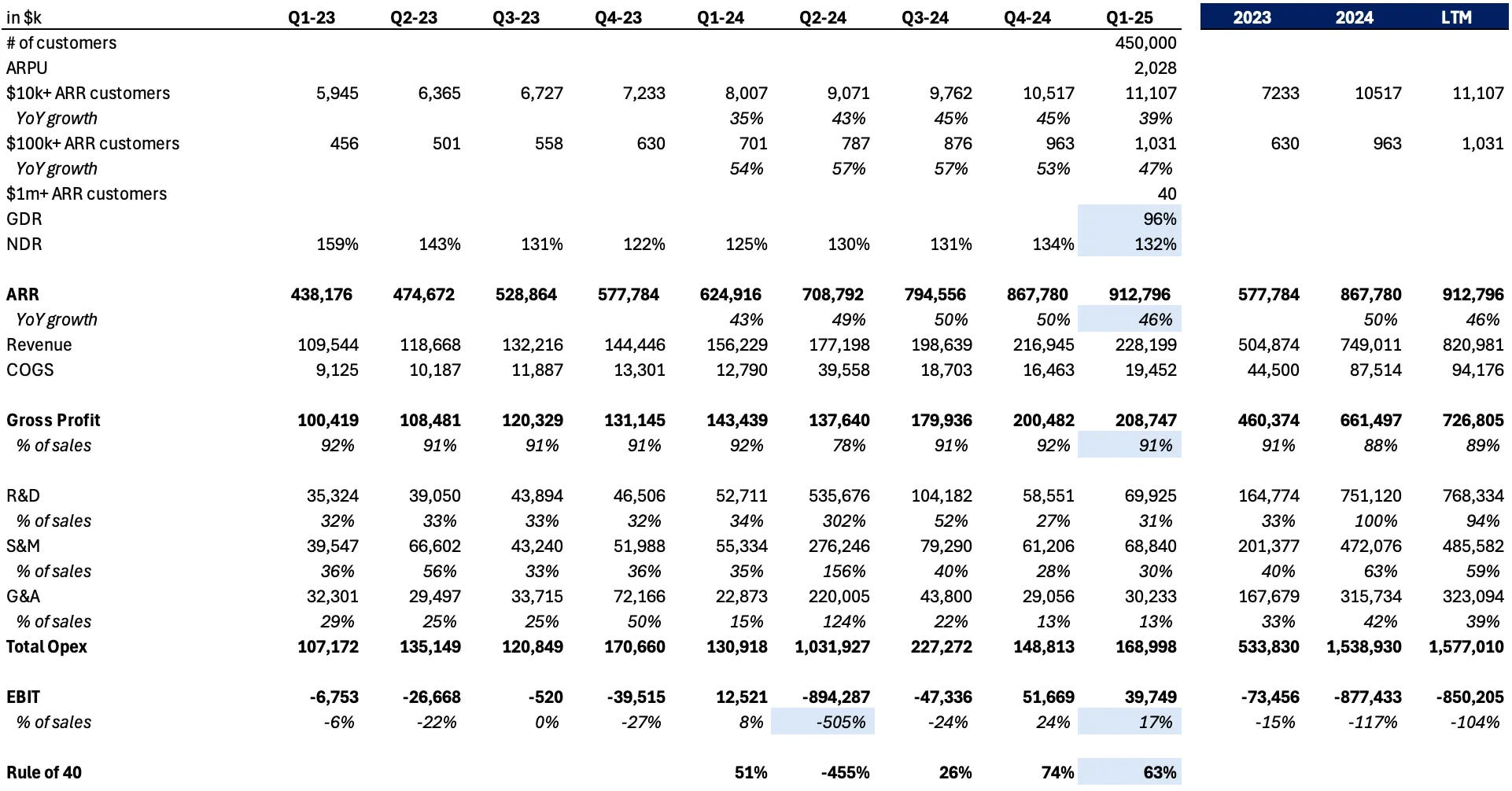

Quantitatively, it boasts outstanding metrics, with $913m in ARR (growing 46% YoY), 96% Gross Dollar Retention (GDR), 132% Net Dollar Retention (NDR), 91% gross margin, 17% EBIT margin, and a rule of 40 score of 63%.

Contrary to other best in class venture backed businesses (e.g. Stripe, SpaceX, Databricks) which are doing everything stay private forever, Figma decided to go public and had to justify its decision.

“In this prospectus, I’m excited to share more about Figma with you as we begin our transition into public markets. Given the trend of many amazing companies staying private indefinitely, you might be wondering why I have decided to take Figma public in the first place. Some of the obvious benefits such as good corporate hygiene, brand awareness, liquidity, stronger currency and access to capital markets apply. More importantly, I like the idea of our community sharing in the ownership of Figma — and the best way to accomplish this is through public markets.” - Dylan Field (Figma’s cofounder & CEO)

It’s a noteworthy statement in a world where one could argue that only tier-two companies are going public, while tier-one companies remain private indefinitely thanks to abundant capital.

I like Dylan’s point about community ownership. Like Robinhood (25.8m funded customers), Figma is well-positioned to perform in the public markets thanks to its large and highly happy user base (13m MAUs).

Figma is a founder-led business that will make everything to successfully ride the AI revolution.

“Our goal is to achieve long-term growth by supporting the rapidly evolving needs of designers. Some companies run out of ideas as they scale. At Figma, we have more ideas than ever. Expect us to take big swings when we see a chance to invest in our platform or pursue M&A at scale. That means at times we will make decisions that may not seem immediately rational.” - Dylan Field (Figma’s cofounder & CEO)

Figma is at a fascinating point in its journey, where it needs to prove that it can evolve from a single product into a multi-product platform and establish itself as an AI winner. In hindsight, I believe Adobe’s abandoned acquisition has been a blessing for Figma, significantly improving its chances of successfully navigating these two critical transitions.

From a product perspective, Figma successfully reinvented the product design category (vs. InVision & Sketch) by democratising it with 5 key levers:

Web-first leveraging WebGL’s technological enabler vs. desktop-first,

Multi-player with native collaboration between designers and the rest of the functions interacting with them starting with developers and product managers vs. single player,

Easy to use vs. usable only by professional designers,

Generous freemium to drive adoption across designers and within organisation vs. paying,

Continuously updated system of records where companies centralise their design system (collection of reusable components and standards to ensure brand consistency within the organisation across product interfaces) vs. file based system.

Figma is close to achieving a near-monopolistic position in product design, with over 80% market share. This gives Figma a captive cash-cow (13m MAUs and a significant cash flow) that can be leveraged to expand into multiple adjacent markets. Moreover, once your designers have implemented your design system in Figma, it becomes your system of records, massively increasing switching costs.

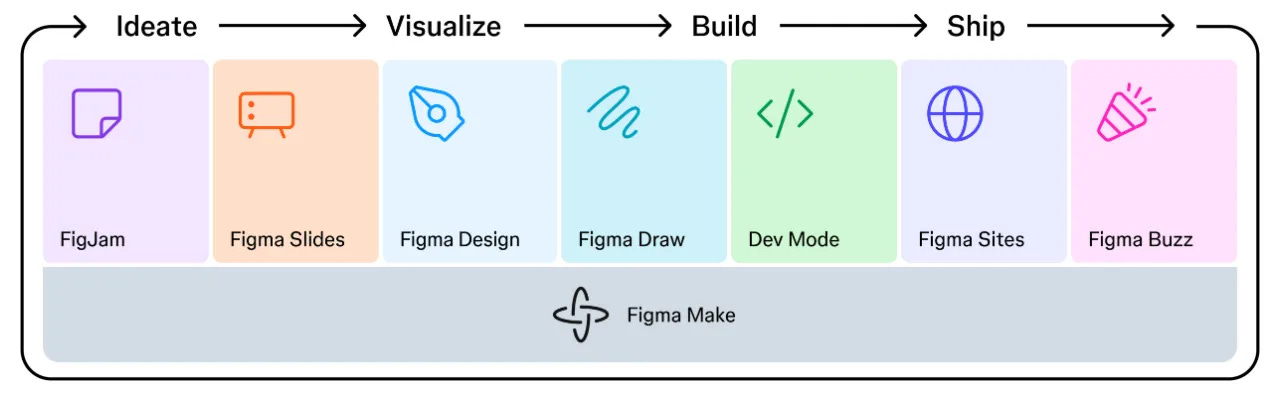

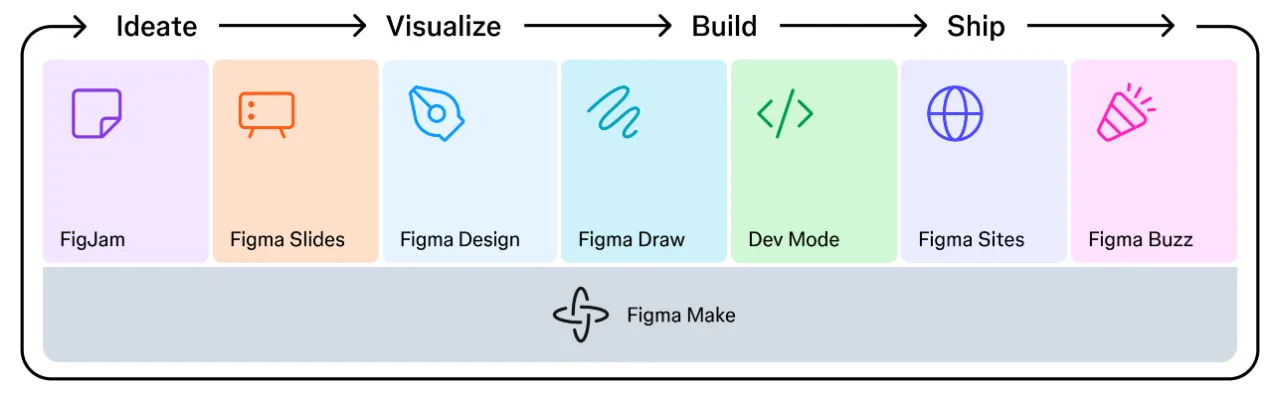

Figma is aggressively expanding its addressable market, having grown from one product to eight products over the past five years. Figma is trying to grab market share on existing categories (e.g. from Microsoft on slides, from Webflow on website building, from Miro on white-boarding or from Canva on marketing content) and to compete in emerging categories (e.g. prompt to app against Lovable).

“Long-term ARR growth ≃ NDR”. Figma has everything to sustain high growth at scale with its high NDR currently sitting at 132%. It has multiple levers to sustain it: (i) seat expansion, (ii) plan expansion, (iii) product expansion and (iv) price increases. If successful, Figma’s aggressive product expansion could provide a strong growth runway, much like ServiceNow’s expansion beyond ITSM or Monday.com’s move beyond horizontal project management.

Figma is one of the strongest examples of a product led growth business. It boasts a large base of enthusiastic free and prosumer users (over 13m MAUs) which serves as an excellent lead-generation engine for its sales motion. Figma began monetising only in 2017 and hired its first sales rep in 2018 with the launch of its Organisation Plan. Today, 70% of customers on Organization and Enterprise Plans started with at least one user on a Professional Plan. This product-led approach has proven highly effective: Figma now works with 95% of the Fortune 500 and 78% of the Forbes 2000. It also counts 40 customers generating over $1m ARR each.

Financial & Operating Metrics

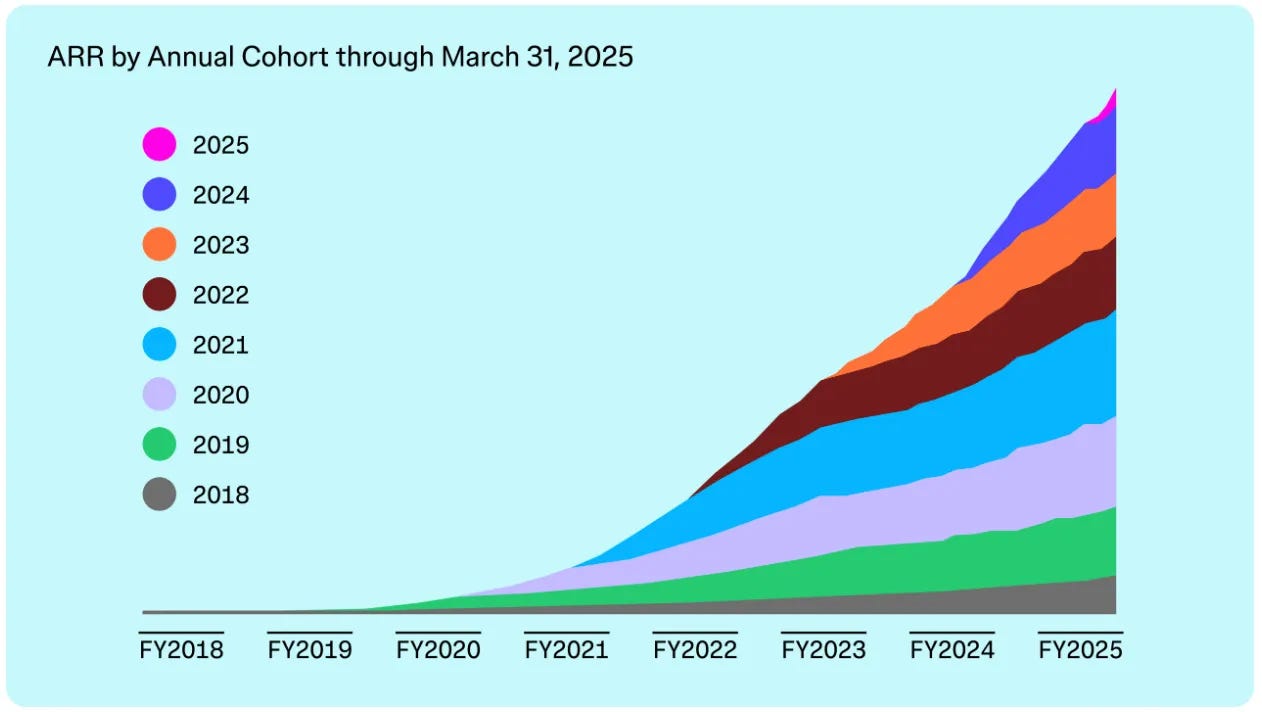

In Q1-2025, Figma reached $913m in ARR growing 46% YoY.

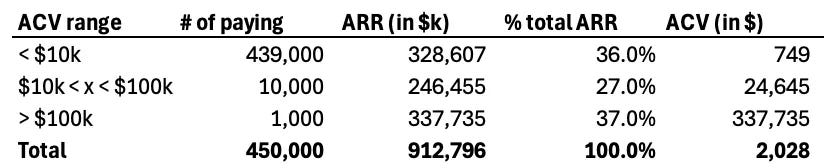

Figma has 13m MAUs (mix of paying & non paying users) with 1/3 of designers and 1/3 of developers. It has 450k paying customers implying a $2k ACV. Out of them:

11k are paying $10k+ ARR (64% of total ARR, $53k ACV),

1k paying $100k+ ARR (37% of total ARR, $328k ACV),

40 customers paying $1m+ ACV.

Figma has stellar retention rates with 96% GDR and 132% NDR for $10k+ ARR paying customers. 76% of customers are already using 2+ products.

I believe that Figma will maintain a NDR above 120%+ for several years, fuelled by increasing adoption within organisations (e.g. 78% of Forbes 2000 companies use Figma but only 24% pay $100k+ ARR) and successful cross-selling of the many new products it has launched over the past five years with with Figjam (2021), DevMode (2023), Slides (2024), Sites (2025), Make (2025), Buzz (2025) and Draw (2025).

Figma has also amazing unit economics being largely profitable with 91% gross margin, 31% of sales in R&D, 30% of sales in S&M and 17% EBIT margin. Everything results in a 63% rule of 40 when you add its ARR growth rate to its EBIT margin.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋