European VC Funds Raised €11.6bn in 2019

Overlooked #1

Hi, it’s Alexandre from Idinvest. Today, I’m talking about the European Venture Capital firms which raised a new fund in 2019.

Raising money for a startup is a milestone. It brings cash to reach the next development step of your company. It raises brand awareness which in turns facilitate recruitment, sales, communication etc.

But Venture Capital funds are also raising money from investors. And it is also a crucial step in their existence. Reading new fund press release and digging into the data is a great way to have a pulse of where the European VC ecosystem is heading.

Ready to jump in? Let’s go!

1/ Why does a Venture Capital (VC) fund need to raise capital? VC firms are managing money from external investors through funds they will raise every 3-7 years. VC is an asset class belonging to the Private Equity (PE) market i.e. the funds perform investments in equity securities of unlisted companies. All PE firms are structured in a similar way with four main stakeholders:

Limited Partnership: juridical entity which will receive the money from investors and which will own the portfolio companies.

General Partners (GPs): the management team which will manage the limited partnership by investing and monitoring companies. GPs invest 1-3% of the total fund size. But these people need to raise money from external investors.

Limited Partners (LPs): investors which will invest in the limited partnership and will expect a return on investment at the end of the fund (usually 10 years). LPs will invest 97-99% of the total fund size. There are many different types of LPs including institutional investors, corporates and even individuals.

Investments: companies in which the GPs will invest in and monitor during the lifetime of the fund. At the end, GPs will sell their stake in the companies and expect to make a good return.

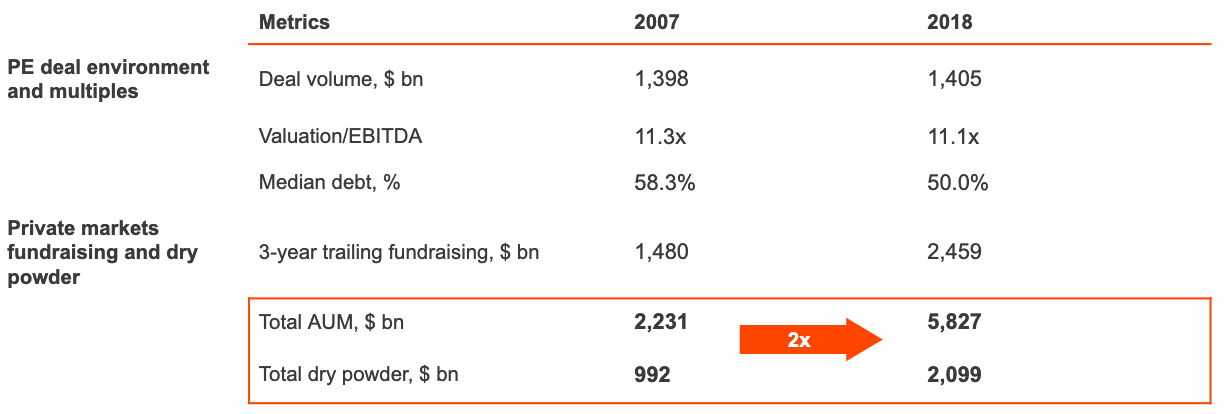

2/ The amount of capital available is at an all time high. $2.1tr need to be invested by PE funds worldwide which is twice the 2007 level, prior to the financial crisis.

3/ VC fundraising is the fastest growing asset class in private markets in terms of fundraising in the past 5 years with a 18% CAGR (vs. 6.2% for the whole PE industry).

4/ 126 European VC funds raised €11.6bn in 2019 (Dealroom data). It is a record year in terms of amount raised by European funds with a 15% increase compared to 2018. Nonetheless, the number of funds raised decreased by 18% compared to last year. This is due to the concentration of funding in tier one funds with the top 10 funds attracting €4.4bn in 2019 compared to €3.0bn in 2018.

This is an extract of some European VC which raised a new fund in 2019. You can find complementary information on these VC and others in this Airtable.

Learning #1 - Be rich or be different. “To succeed in venture capital, you must be one of the top five firms. And to get there, you must have an amazing deal flow.” - Marc Andreessen (a16z founder). To be successful in venture, you have to source and beat other funds to enter in the shareholding of the most promising companies. There are two ways to do so:

You are a historical tier 1 fund like Accel, Index, Balderton or Atomico in the UK. You will have a strong brand, a solid historical track record and tons of cash to deploy. Startups will be knocking at your door. And when it’s not the case, they will never refuse a meeting with you.

You are able to differentiate yourself from other VC funds and bring more value to a specific categories of startups. This differentiation could be (i) a sectorial specialization (e.g. Notion and Axeleo in B2B startups), (ii) a focus on a certain stage (e.g. seed specialists like Frst, LocalGlobe, Cherry), (iii) the ability to lead geographical expansion in certain geographies (e.g. EQT which funds US companies wanting to enter in Europe)

Learning #2 - VC funds are becoming data-driven. Numerous European unicorns have grown up outside the major tech hubs like London, Paris, Berlin and Stockholm. For instance, UiPath was born in Bucharest (Romania), Bolt in Tallinn (Estonia), Bitfury in Amsterdam (Netherlands) etc. Developing internal sourcing and scoring algorithms to source startups from everywhere in Europe could be a key differentiator.

EQT (€660m fund, 🇸🇪) has an in-house team developing a software called Motherbrain to source investment leads. It is tracking 8m companies and 40k VC funds and has been already used to source several deals like Peakon, AnyDesk, Handshake, Warducks or Standard Cognition.

InReach (€53m fund, 🇬🇧) claims to be an '“AI-powered” VC fund with more engineers in its team than investment professionals. GPs invested €3m in a software whose aim is to find and qualify deal opportunities. The end-game is to be able to scale VC sourcing and to have the same deal-flow than a VC that would hire VC associates to manage sourcing in every European tech hub.

Learning #3 - VC funds as operational platforms. Following their counterparts in the US (First Round, a16z etc.), European VC are structuring the value they add to their portfolio companies beyond money. Providing an in-house HR expert to help startups recruit key people has become the norm. Same for providing them with marketing and sales playbooks in adequation to their stage.

Project A ($200m fund, 🇩🇪) is the paroxysm of this trend in Europe. The fund defines itself as the “operational VC” with an in-house team of 100 experts dedicated to help portfolio companies in every business areas (engineering, marketing, product, design, communications, business intelligence, sales, customer success, organizational building, hiring). Projects duration range from 1 hour to 3 months and startups are free to decide whether they need help or not.

Learning #4 - US VC funds are starting to hunt on European lands. This point does not appear in the data. Yet, it should not be underestimated. Sequoia is seeking candidates to set up an office in Europe. Kleiner Perkins and Benchmark have started to invest in European companies in the past few years. In France, 61% of startups which raised a round above €40m in the past 3 years had a US VC on board. It is great news for the whole European ecosystem. It validates the fact that Europe is an attractive territory to build tech giants. Strong founders will get access to another source of funding and European VCs will have to step up their game to be able to compete with US peers.

🗞 Preparing for 2020: Our Predictions for European Venture Capital (Dec. 2019, Speedinvest)

🗞 Blossom Capital & High Conviction Investing (Feb. 2019, Ophelia Brown, Blossom Capital)

🗞 VC have to go big, go brand, or go home (June 2019, Sifted)

🗞 US VCs are coming (Jan. 2020, Sifted)

🗞 US venture capitalists: here are 10 tips if you want to make it in Europe (Dec. 2019, Nicolas Colin, Sifted)

🗞 Why Silicon Valley Investors are Bonkers for European Startups (Dec. 2019, Forbes)

🔎 From Value-Added VC to Equity Crowdfunding Syndicates: the new Platforms of the Venture Capital Industry (May 2016, Louis Coppey, Point Nine)

🔎 Private Markets Come of Age (2019, McKinsey)

Thanks to Julia for the feedbacks! 🙏

See you next week for another issue! 👋 Do not hesitate to share the newsletter to your friends and to subscribe if it is not already the case!