🦘Deliveroo's IPO - Breaking Down the Potential Futures of the Company (Part II)

Overlooked #64

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the second part of a deep-dive on Deliveroo, one of the most iconic European consumer startups which made its public debut two weeks ago.

Last week, I shared the first part of my Deliveroo’s deep-dive digging at the company’s history. This week, I’m breaking down Deliveroo’s potential future growth levers. I will look at both explicit plans described in the IPO prospectus and implicit or more extravagant ideas to bring the company to the next level.

I will break down this paper into the following sections:

Deliveroo's Explicit Future: (i) doubling down on dark kitchens with Deliveroo Editions, (ii) a white label offering with Deliveroo Signature, (iii) going after the online grocery market, (iv) a pay to pay less subscription with Deliveroo Plus.

Deliveroo's Implicit and/or Extravagant Futures: (i) bringing non food brands & influencers in the food space with a business in box offering, (ii) going horizontal beyond food delivery, (iii) moving towards a super app, (iv) building a verticalized SaaS for restaurants.

Part II - Deliveroo's Future - Explicit Expansion Plans

Deliveroo Editions - Doubling Down on Cloud Kitchens

Dark/cloud kitchens are kitchens that only deliver and that don't have a dine-in experience. UberEats defined dark kitchens as "data-driven, delivery-only concepts operating out of existing brick-and-mortar restaurant kitchens".

One of the first articles published when I launched this newsletter 16 months ago was about dark kitchens. I started the article with the below introduction inspired by a conversation we had in 2019 with Anton Soullier from Taster and my colleague Nicolas Debock.

"Several hundred years ago, posting houses were places where horses were kept and could be rented or changed out. Travellers would arrive to these houses to exchange horses and move to the next leg of their journey. Logically, the posting houses also became auberges where travelers could rest for the night and eat something. Posting houses permitted the rise of auberges specifically suited for this infrastructure of posting houses to feed and offer rest to travelers. The same is happening with dark kitchens and the food delivery infrastructure."

As a result, it's not surprising that food delivery platforms which built the infrastructure are at the forefront of the rise of dark kitchens. UberEats, DoorDash, Glovo, JustEat and Deliveroo are all operating dark kitchens.

Deliveroo has been operating dark kitchens since 2016. It now has 250 Editions kitchens in 8 different markets. These kitchens are turn-key solutions for restaurateurs. Restaurateurs cook the food and Deliveroo manages all the rest (real estate location and utilities, kitchen equipment, software and delivery).

Food delivery platforms operate dark kitchen sites to build unfair competitive advantages: (i) you bring a proprietary supply of food concepts in underserved neighbourhoods, (ii) you improve the customer experience as kitchens are optimized for food delivery, (iii) you can take a higher take rate on orders as you provide more value to restaurateurs, and (iv) you strengthen your relationships with your best restaurants which make them more sticky to your platform vs. others.

What are the benefits for restaurateurs associated with operating a dark kitchen?

You can be in a tier-2 or a tier-3 location to operate your kitchen which cuts the rent costs significantly vs. a tier-1 location when you have a restaurant.

You have less labour costs as you have only cooks in the kitchen and no waiters.

You have reduced paid acquisition costs. You are ranked by the food delivery platform's algorithm which works like a SEO (based on your ratings, your operation excellence and your business volume) and you don't have to spend money on Facebook and Google to get new customers like most consumer brands.

Your kitchen is optimised for delivery which makes you more productive. For instance, Deliveroo's Editions orders are delivered 4 min faster than non Editions orders.

When a restaurant owner wants to try a new food concept or a new location, it reduces the investment's risk to launch it through a dark kitchen instead of building right away a new brick and mortar restaurant. Your cost structure will be much more flexible and you will be able to shift gears quickly if it does not work.

Covid was also a tipping point for the rise of dark kitchens. As restaurants were closed because of lockdown restrictions, they had to try new operating models to survive. Delivering food was the most common option for restaurants but some of them have gone one step further and have tried to recycle their underused kitchen to launch virtual food brands. If the dark kitchen model works for some restaurants, there is no way that they will come back to a traditional dine-in and single only restaurant model.

Will Shu believes that dark kitchens are the future of food delivery and are currently evolving from "a nice-to-have expansion play for restaurants to really a fundamental part of restaurants’ strategy.” As a result, in 2021, Deliveroo plans to double the number of Editions sites it operates worldwide.

Deliveroo Signature - A White Label Offering

Signature is a white label service launched in 2019 for restaurants willing to digitise their operations while keeping their direct relationship with customers.

With Signature, restaurants can access Deliveroo's delivery service using their own websites and applications. But the Signature offering goes beyond delivery. Restaurants can also use Signature for their on-site experience with click-and-collect and table services features as well as for their online presence with support from Deliveroo to create a website and or to design an app.

Deliveroo is moving towards a full-stack and omni-channel offering for restaurants. I won't be surprised to see other product bricks released to manage other sections of a restaurant operations (payments, reservations, staff planning, etc.). As we saw in the history section, Deliveroo is already working on certain additional bricks like food procurement.

It's not a revolution for food delivery platforms to add a white label offering. DoorDash launched a similar service called DoorDash Drive.

"In addition to our Marketplace, we have also developed a white-label logistics service, DoorDash Drive, which allows merchants that generate demand through their own websites, apps, and other channels to fulfil orders using our platform." (DoorDash's S1)

Today, Deliveroo is working with 50+ restaurants partners including chains like Nando's wagamama, Wingstop or PizzaExpress.

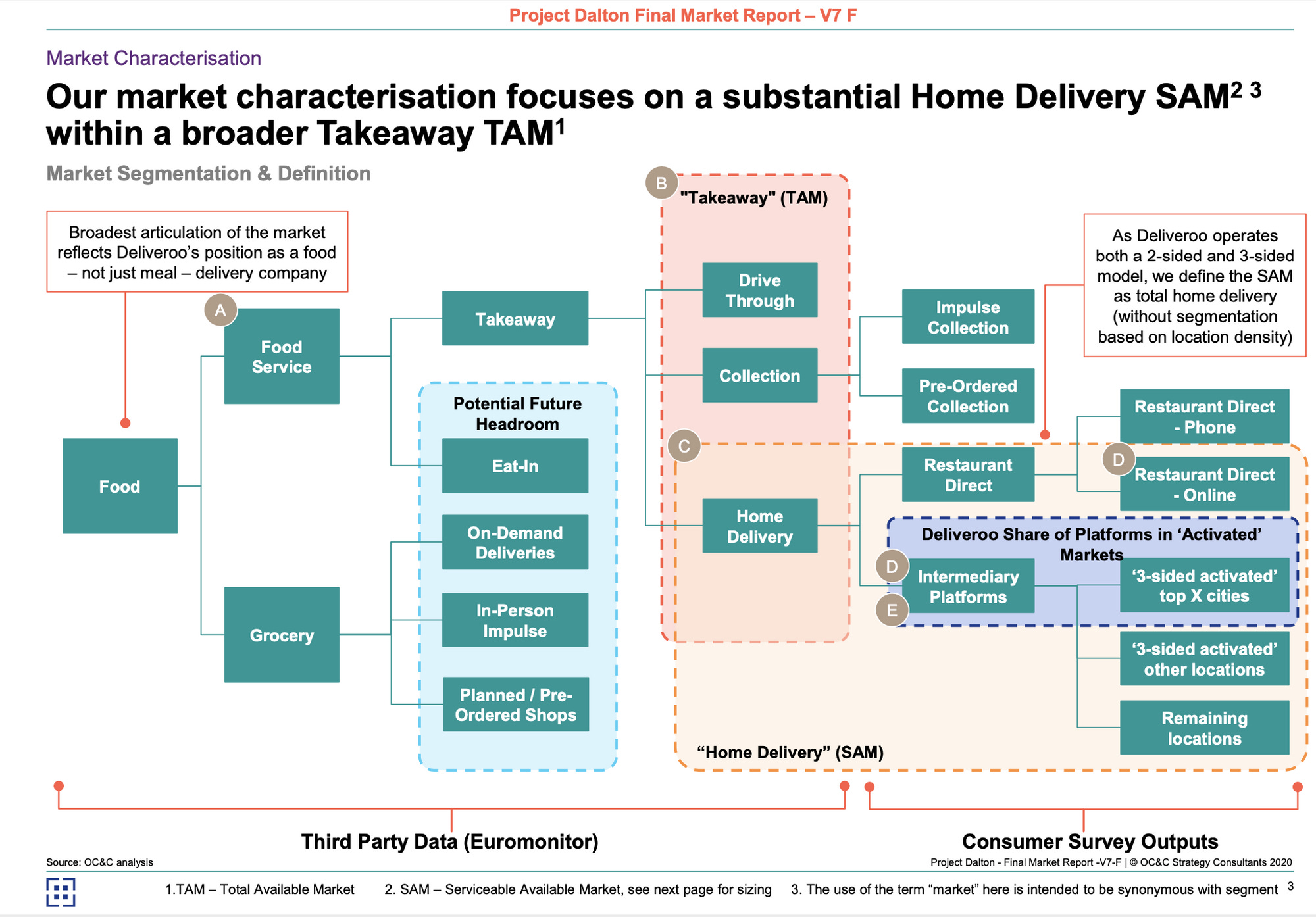

Going after the Online Grocery Market

The online grocery market is the next eldorado that Deliveroo is going after. To prepare its IPO, Deliveroo worked with a strategy consulting firm called OC&C to provide market sizing. In OC&C's final report, I discovered the two below slides which breakdown and size the Deliveroo's market in its current geographies. Historically, Deliveroo went after a piece of the food service market estimated at $26bn. In the past 12-18 months, Deliveroo has taken many initiatives to go after another market which is the online grocery market also estimated at $26bn.

Covid has accelerated Deliveroo's expansion in the grocery market. With covid, many shopping behaviours have shifted online including grocery which was one of the lowest ecommerce penetrated verticals in many European countries. Moreover, numerous national policies to fight against the epidemic (curfews, lockdown restrictions etc.) favoured delivery models. Deliveroo seized the opportunity to sign partnership with many leading European retailers including 7-Eleven, Carrefour, Casino, Waitrose, Conad etc. In 2020, Deliveroo signed 36 new partnerships with grocery chains.

Grocery is a great complement to restaurant food delivery. You tap into complementary use cases for delivery which will increase the utilization rate of the driver fleet and will also make the Deliveroo's subscription even more strategic.

Competition in the online convenience grocery market in city centres is going to be tough in the next 5 years. Grocery is not an homogeneous market. It can be divided into 3 main use cases: convenience / emergency shopping, weekly shopping and monthly stock-up. I think that Deliveroo will go mainly after the first use case. Deliveroo will go face to face with the new wave of goPuff copycats that are entering the market with a different operational model. Instead of a store picking model, these players have a distributed network of small dark stores in city centres. The latter model is supposed to be much more efficient logistically speaking compared to taking orders from retailers that don't have operations optimized for delivery.

I won't be surprised to see Deliveroo doubling down on groceries with this full stack approach of dark stores. Both Glovo and DoorDash have already launched a dark-store backed grocery offering. In fact, all leading food delivery players have the fleet of riders and the brand awareness to kickstart an in-house grocery offering. I believe that Deliveroo will be even more sensible to this model when the company realises that a dark grocery store is bringing the same benefits in terms of operation efficiencies as a dark kitchen for restaurants. If we push this idea one step further, we can imagine the rise of Deliveroo small city hubs which are both a grocery dark store and a Deliveroo Editions kitchen. Restaurant preparation and grocery preparation will be both on the same site and optimized for delivery. This could be the future of the retail market in city centers.

Former Deliveroo's executives also started a London-based goPuff-copycat called Dija. Before launching its own app, Dija made several tests on the Deliveroo's marketplace. I'm sure that Deliveroo will follow Dija closely and other contenders in this market. If it takes off, Deliveroo will either launch it in-house or swallow one of the emerging players.

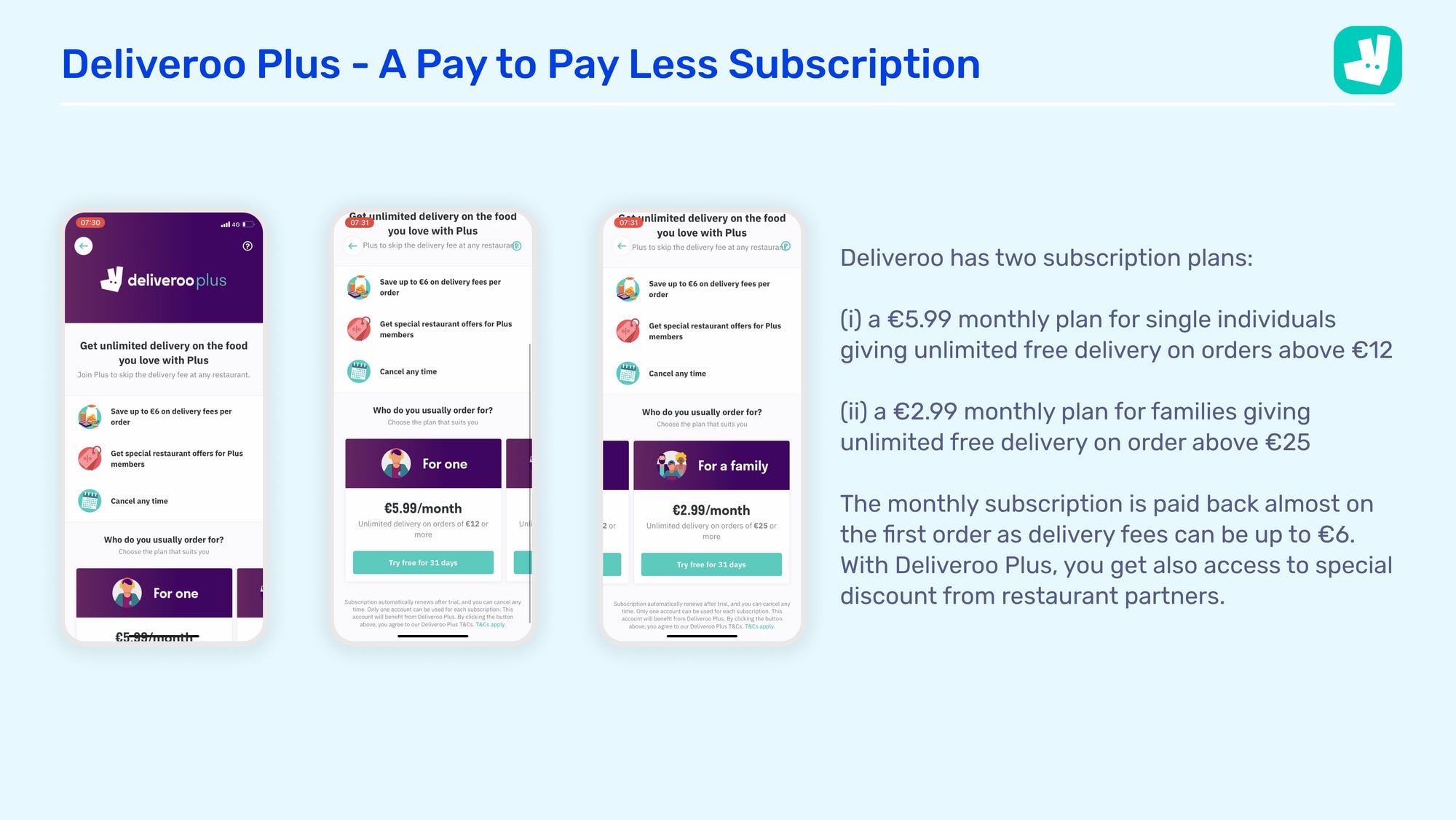

Deliveroo Plus - A Pay to Pay Less Subscription

In 2017, Deliveroo launched a consumer subscription offering called Deliveroo Plus to lock consumers on the platform and increase their purchasing frequency. As Will said in many interviews, Deliveroo is going after the 21 meals occasions that we have per week. Today, the Deliveroo's average user only orders from the service once a week. There is strong room for additional consumer adoption. When you add the fact that Deliveroo is now also going after the online convenience grocery market, it makes a lot of sense to launch a consumer subscription. Today, Deliveroo Plus is available in 8 of their 12 markets.

Deliveroo has two subscription plans: (i) a €5.99 monthly plan for single individuals offering unlimited free delivery on orders above €12, (ii) a €2.99 monthly plan for families launched in early 2021 offering unlimited free delivery on order above €25. The monthly subscription is almost completely paid back on the first order as delivery fees can go up to €6. With Deliveroo Plus, you also get access to special discounts from restaurant partners.

Deliveroo Plus is a "pay to pay less" subscription. You will pay a monthly or annual subscription to get access to special discounts. The more you use the service, the more you money you save. It's a model that we find both in the offline (Costco, Metro) and online (Amazon) worlds. It has become a standard in the food delivery market. For instance, DoorDash (6m subscribers) and Uber have launched similar subscriptions in the past 2-3 years.

Part III - Deliveroo's Future - Implicit / Extravagant Expansion Plans

Bringing Non Food Brands & Influencers in the Food Space with a Business in a Box Offering

General idea: With the combination of (i) a network of dark kitchens, (ii) the white label offering for restaurant partners, (iii) the Deliveroo's delivery network, Deliveroo has all the building blocks to help non food brands/influencers to launch temporary or permanent food concepts (cf. MrBeast with Virtual Dining Concepts).

In Dec. 2020, top U.S. Youtuber MrBeast (48.7m subs) launched a virtual burger chain called MrBeast Burger. He partnered with Virtual Dining Concepts (VDC) which helps restaurants generate more revenues out of their existing kitchens. VDC provides restaurants with delivery only food concept that they will operate in parallel of their regular activity to maximize the usage of their kitchens. MrBeast launched in partnership with 300 local restaurants across the countries. Fans were able to order from MrBeast Burger on all delivery apps (DoorDash, Ubereats, Postmates etc.) as well as on the proprietary MrBeast Burger app. As you can expect, it was an instant hit with only one video and several post on social medias. The app was downloaded more than 1m times. The restaurants were overwhelmed by orders. They faced two main operational challenges: quality control issues with some restaurants and not enough drivers to deliver all the burgers ordered.

In the future, I'm convinced that we will see more non-food brands and celebrities entering the food category with similar value propositions. Virtual Dining Concepts used a network of existing restaurants to launch MrBeast delivery only food concept. It comes with quality challenge as 300 independent restaurants can not be homogeneous in their preparation processes and food procurement.

When Deliveroo will have a sufficiently developed network of dark kitchens with Deliveroo Editions, it will have the power to test and scale temporary or permanent concepts like MrBeast Burger while maintaining a high level of quality and service.

Going Horizontal Beyond Delivering Food

General idea: In 2020, Deliveroo expanded its market from food delivery from restaurants to grocery delivery from grocery retailers. In the end, Deliveroo's prime asset is its ability to manage a last mile logistic network which can be used for a variety of use cases. A good inspiration could be Glovo that has been horizontal from almost day 1 and which has a super large offering in its most mature markets.

This idea is inspired by other players in the food delivery category (esp. Rappi and Glovo) and it's a way to double down on two strategic moves done by Deliveroo (adding a subscription and expanding into groceries).

When you take a step back, Deliveroo's main asset is to have built a last mile delivery network. It has been used historically to deliver food from restaurants but there is no reason not to recycle this network for other use cases.

In 2020, we saw that Deliveroo massively expanded its market by going after the grocery category. The startup signed agreements with major European retailers to deliver a portion of their catalogue from their stores in less than 30 min. It was the first time that Deliveroo added a new use case to its platform and I'm convinced that it will not be the last one.

Moreover, Deliveroo introduced few years ago the "pay to pay less" Plus subscription whose value increases when your purchase frequency increases. Adding other use cases beyond groceries and food delivery from restaurants is a way to maximize the value of the subscription.

In Europe, Glovo started with this horizontal positioning from day 1. The first version of the app was even an app with two buttons: "bring me something" or "deliver something to someone". When Glovo started to grow, the company kept this multi-category approach. Today, when you open the Glovo's app in its most mature market you can order from restaurants, grocery stores, a selected number of local shops, pharmacies and beauty shops. You can also order anything from Glovo as long as a courrier can bring it to you. Only 20% of deliveries are not food related but these deliveries bring 80% of the Golvo's WOW experience.

"It's a question of brand perception. I mean when we bring customers an aspirin at 2:00 AM, those are the “Wow!” moments that they want to talk about." - Sacha Michaud

Moving Towards a Super App

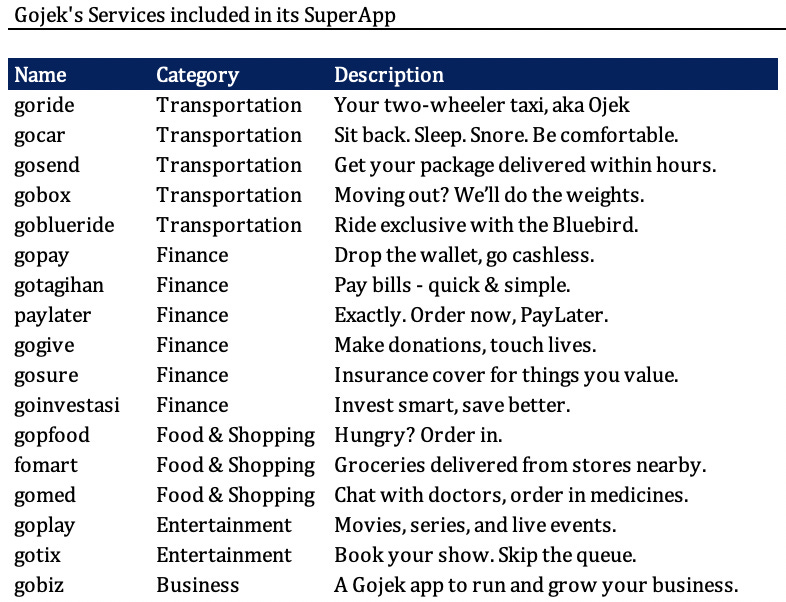

General idea: No western player has been able to build a Super App. Deliveroo can have this objective over the long run and can take inspiration from emerging country players like Rappi, GoJek or Meituan.

In emerging countries, many tech players have managed to combine in a single app a wide variety of services including food and grocery delivery, to transportation, banking, hotel and airplane booking, ticketing, gaming, education etc. They have become what we call "Super Apps". Instead of downloading an app for each service that you need as a consumer, you will access all these services through a single app. I will give you two examples:

Gojek in Indonesia. The company was founded in 2010 and launched its application in 2015 with services around delivery. Since then, it has expanded massively to other categories as you can see in the below graph from the Financial Times.

Rappi in Latin America. The company was started in Colombia in 2015 and is now present in 9 countries and 200 cities in Latin America. It started as a delivery service for restaurants, groceries and retail shops. It is now expanding into new categories including gaming, ticketing and live events.

Many Western companies are trying to go after this SuperApp model to diversify their revenue streams and expand in new business categories.

Uber is offering food delivery, micro-mobility services and financial services on top of its original ride-hailing value proposition.

Amazon has been bundling different services including gaming, video streaming and music streaming under its Prime subscription to go beyond ecommerce.

Snap is working on Minis which are small programs to get access to third party services with almost no friction without leaving Snap (e.g. going on a meditation session with Headspace, buying a cinema ticket etc.).

I believe that food delivery companies like Deliveroo are well placed to build a SuperApp because they can use their last mile delivery network across many use cases as we saw with Glovo. It's a great starting point to expand later on in other verticals.

Building a Verticalised SaaS for Restaurants

General idea: Deliveroo is already offering a wide range of services for restaurants that go beyond delivery. The company can double down in this direction and offer a one-stop-shop verticalised SaaS for restaurants to manage everything on site and for delivery.

I'm a big believer in the rise of vertical SaaS. In this model, the vision is to build a software that will be able to tackle all the pain points specific by the stakeholder in an industry. Most verticalized SaaS are digitizing large old-fashioned industries and come with a super strong value proposition: they are often perceived as the last software to unplug before going out of business. I will give you three examples of successful vertical SaaS:

Veeva in healthcare: it's a Customer Relationship Management software dedicated to the healthcare industry which has become completely dominant in large healthcare companies.

Shopify in the ecommerce industry: it has become synonymous with selling online. Shopify started as the go to platform to build your online store. It has expanded into adjacent areas to give more tools to its merchants in marketing, payments, financing, etc.

Amenitiz in the travel industry: it builds the one stop shop software for small hotels and B&B. It has a property management system, a booking engine, a channel manager and a website integrated in a single platform.

Being a verticalized software constraints your addressable market but it also brings many unfair advantages when it comes to distribution and the market penetration that you can reach. In the U.S., there is a successful vertical SaaS targeting restaurants which is called Toast. Toast has convinced 40k American restaurants and brands that it is the one software to "run your entire restaurant". It offers point of sales, online ordering, delivery services, payroll and team management, email marketing, order and pay solution, etc. In Europe, several players are positioned to serve the restaurant industry (Flipdish, Tiller, Choco, Rekki etc.) but none of them have become as pervasive.

It's an interesting path to pursue for Deliveroo as the platform has already made the effort to build a relationship with restaurants to have them on the marketplace. Moreover, overtime, Deliveroo has added many services dedicated to restaurants to help them thrive in the business beyond food delivery (e.g. a procurement solution, dine-in features, marketing support etc.). It seems to be a logical step to tackle other restaurants pain points and claim to become their all-in-one software solution.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋