🌱 Decentralized Finance - Providing Financial Services to the 1.7bn Unbanked People

Overlooked #16

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m digging into a cryptonetworks trend: the rise of Decentralized Finance (DeFi). It’s a set of Ethereum-based financial applications which have the potential to provide financial services to the 1.7bn unbanked people around the world in the next few years.

Let's introduce Decentralized Finance (DeFi) with two recent developments within its community.

First, with the covid-19 market crash, Ethereum (ETH) price decreased by 62% from $284 on February 14th to $108 on March 17th. As a consequence, the most prominent DeFi project called MakerDAO got into serious trouble. MakerDAO is both the largest lending DeFi platform and the issuer of the DAI stablecoin. On March 12th, the lending platform broke down because it became under collaterized allowing a trader to steal $4m worth of ETH.

As a reminder, a stablecoin is a new generation of cryptocurrency designed to avoid the volatility generally associated with cryptocurrencies like ETH and Bitcoin (BTC) by pegging its value to a stable asset (like a fiat currency) or a basket of stable assets.

Second, last week, Libra's founder, David Marcus announced the new version of its project reducing drastically the initial ambitions of the newly formed Facebook crypto arm. Instead of launching its own digital stablecoin indexed on a basket of existing currencies, Libra will launch multiple digital stablecoins backed by individual fiat currencies.

Instead of sending dollars to your friends through Venmo, you will send them "Libra digital dollar" through Messenger. Libra's initial value proposition was disappointing. This revised value proposition is even less compelling. This change is the consequence of the strong public backlash from governments refusing to give away their sovereignty power to mint currency.

These two pieces of news illustrate numerous components surrounding the hype and disenchantments around DeFi:

The strong appetite of the main crypto and tech players for this ecosystem,

The lack of a clear regulation around crypto-based financial services,

The fact that we are still in the early days of DeFi and that the robustness of most projects is still limited,

The value proposition of DeFi is still unclear and often blurred by poor projects - like Libra.

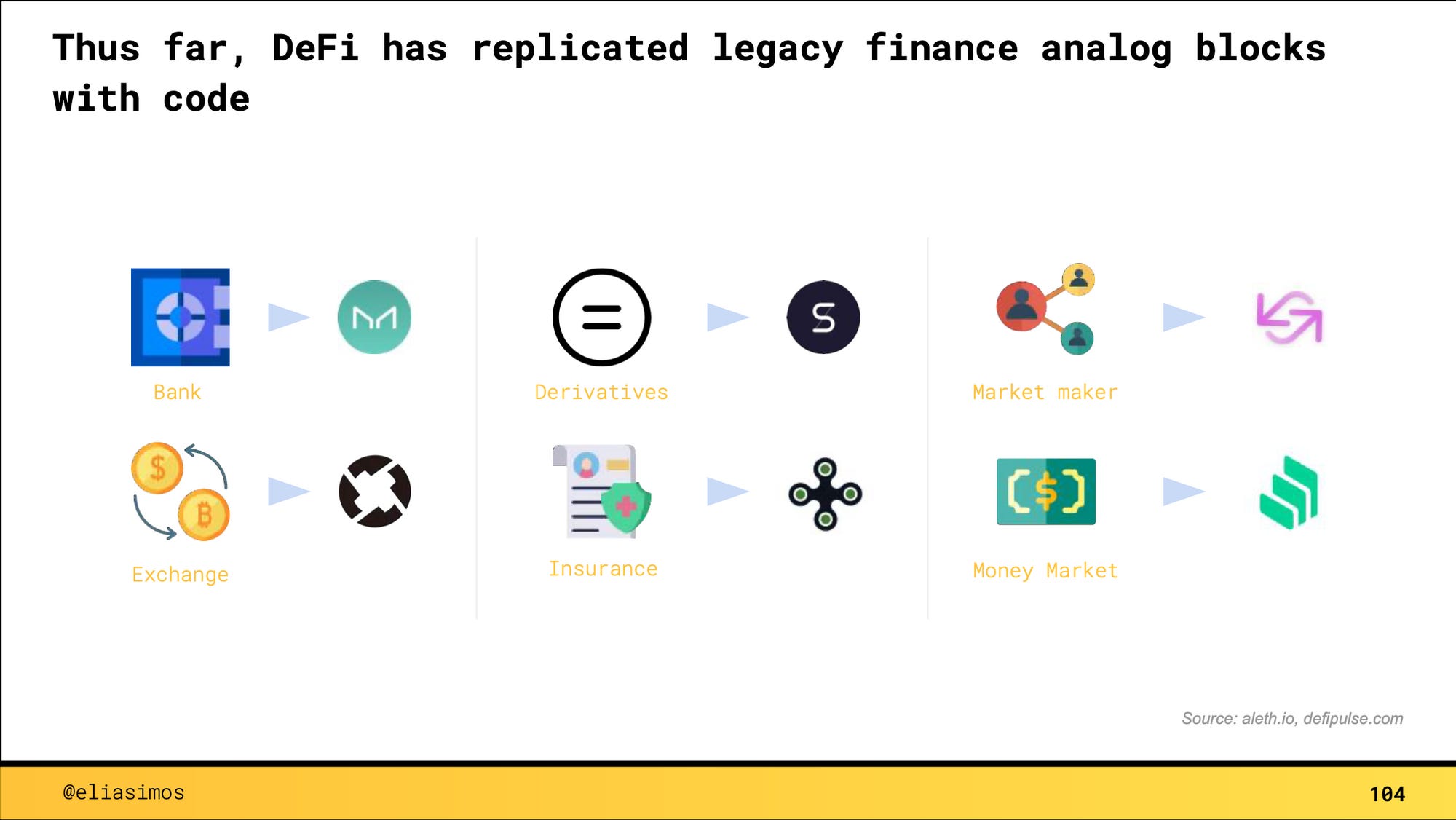

DeFi is an open-source and decentralized financial ecosystem built on top of the Ethereum blockchain. The vision is to build an alternative set of financial services using the key blockchain properties that can imitate what you could obtain from the traditional centralized financial system but also by going one step further and creating other innovative financial services.

Benefit #1 - DeFi applications are based on the ETH blockchain.

They use smart contracts which are programs running automatically on the blockchain when certain conditions are met. Compared to BTC, smart contracts powered by ETH allow developers to build much more complex applications than just savings / receiving cryptocurrencies. As the operation is automated, you do not need to have a central institution as a middle man to make the operation happen.

Benefit #2 - DeFi applications are decentralized.

The traditional finance world is centralized in the hands of central banks, governments and institutional banks. These institutions set the rules of the game and can change them arbitrarily. It means that users can be excluded from the traditional financial institutions and when they are not, they can be worse-off because of measures that destroy their wealth (cf. recurring high inflation in Latin American countries). Moreover, skipping those intermediaries could reduce the frictions and costs associated with financial services.

Benefit #3 - DeFi applications are non custodial.

Users are the only ones to own their funds. The apps used to store their assets and make transactions don't own their funds and they will ask for users permission each time they want to access them.

Benefit #4 - DeFi applications are composable.

It means that as all projects are open-source, when you build a new DeFi application, it is possible to use existing bricks to build your own service. Hence the expression "money legos" used to talk about DeFi. This composability is a strong accelerator of innovation because it allows entrepreneur to start building their project by combining existing bricks before adding their layer of innovation.

Joel Monegro at Placeholder is giving great examples of this composability. "Consider Zerion (a Placeholder investment), Instadapp and Multis. They are building similar crypto-finance apps using many of the same protocols, like Ethereum, Compound, Maker, and Uniswap. This allows them to deliver a complete suite of financial services (transactions, borrowing, lending, trading, investing, etc.) without building all that functionality, infrastructure and liquidity in-house. The protocols provide specific services across many interfaces and the apps on top share resources and data with no centralized platform risk. Sharing the infrastructure lowers the costs across the board."

Consumer applications (like Argent or Multis that we will look at later on) are built on top of several composable protocols. You pick several crypto-services in the infrastructure layer and add your services and your interface to serve customers.

Benefit #5 - DeFi applications can invent new financial services

Today, DeFi applications are replicating traditional financial services (savings, loans, trading, insurance etc.). Tomorrow, innovative services will be invented that cannot be powered by traditional finance.

Benefit #6 - DeFi applications will be accessible to the 99%

DeFi allows users to bypass traditional banking intermediaries to access financial services with only a smartphone and an access to the internet. 1.7bn adults remain unbanked.

The world connectivity is increasing everyday. Almost anyone in the world is now able to access mobile coverage. Tomorrow, I’m confident that accessing to connectivity will be a commodity and that every population could access banking products through DeFi.

DeFi stakeholders are looking at 3 different ways to follow the growth of the ecosystem:

The total valued locked in DeFi applications and protocols,

The number of DeFi users and the number of different protocols they use over time,

The evolution of the number of DeFi projects.

In mid-February, the total value locked in DeFi applications and protocols crossed the $1bn threshold with a 100% growth in the first 6 weeks of 2020. With the market crash the value locked in DeFi has now decreased by 22% to $780m.

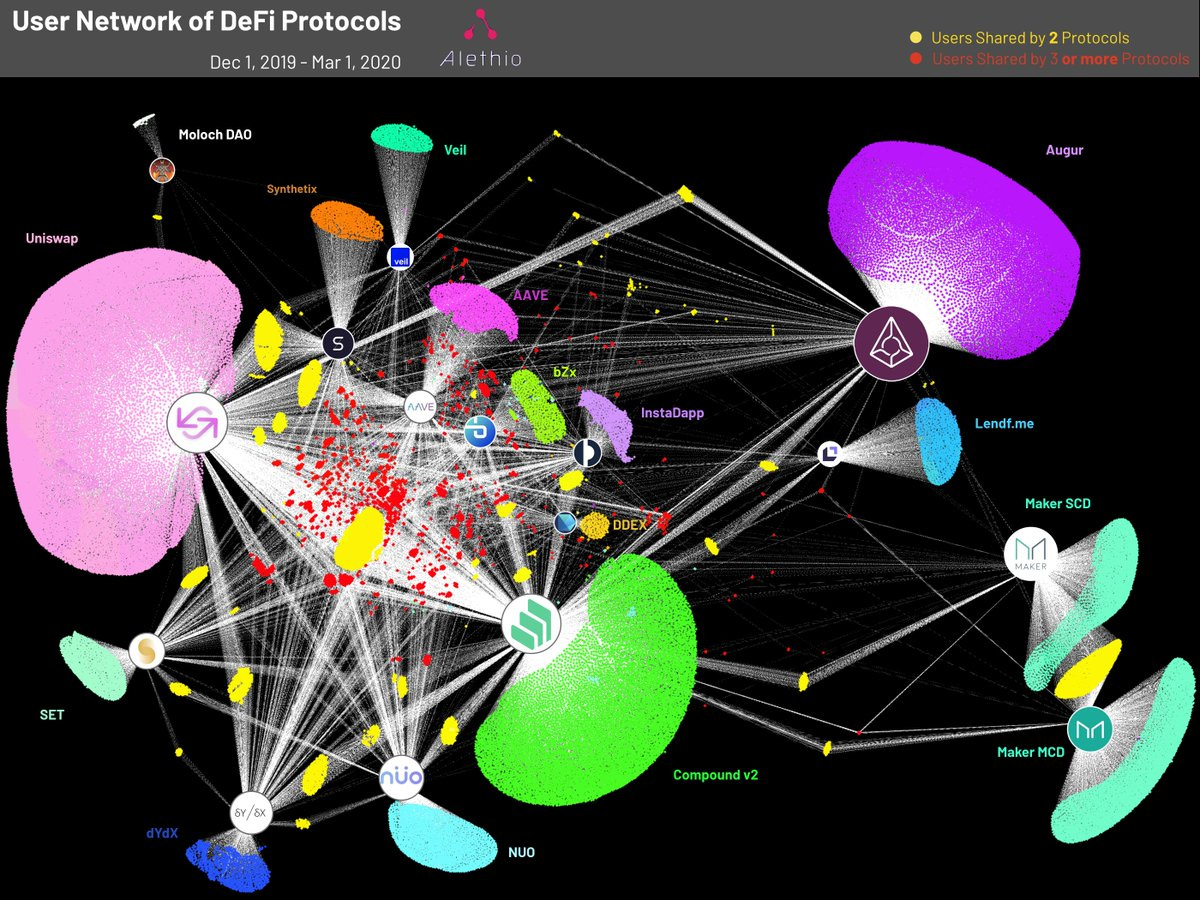

Another way to look at the DeFi ecosystem's growth is to look at the evolution of the number of users of the different applications and protocols. In the below graphs, each colored node around a protocol represents a user that has interacted with the protocol and the points in red, orange or yellow represent users which have interacted with 2 or more protocols. The evolution is striking between May 2019 and March 2020. Firstly, the number of meaningful projects has exploded. Secondly, the number of users using several DeFi protocols has increased dramatically.

You can also dig into the DeFi ecosystem by looking at the below mapping from Defiprime. Here is the signification of the main categories:

Asset management tools: non-custodian wallets, apps and dashboard to manage your cryptocurrencies,

Decentralized lending and borrowing: platforms providing loans to businesses or individuals as well as interests to lenders using DeFi lending protocols,

Tokenisation of assets: platform to invest into tokenized cryptocurrencies and real world assets that are not accessible otherwise (too expensive, geographical restriction, unavailability),

Decentralized exchange: crypto exchanges operating in a decentralized way,

Infrastructure: legos that consumer and business facing applications will use to offer their services,

Stablecoins: cryptocurrencies that are indexed to a fiat/crypto currency or to a basket of fiat/crypto currencies.

This will be an introduction to the following projects. All of them are much more complex than what I wrote in the following lines. The goal is more to incentivize you to check these projects, rather than being exhaustive.

Maker (2014, US-based, Polychcain, a16z & Paradigm backed)

Maker was founded in 2014 as an open source project on the ETH blockchain. It's also a Decentralized Autonomous Organization ruled by governance tokens called MKR that are distributed in a decentralized way. Of course, the contributors to the Maker project hold MKR tokens.

Maker is both a decentralized bank and a decentralized stablecoin.

Maker is a decentralized bank. It has the same "core infrastructure and accounting layer" than a bank but does not pretend to build an end to end financial experience. It builds the core financial infrastructure and then it lets an ecosystem of end users applications emerge on top of it.

Maker is also a stablecoin (DAI), which is used to power these third party applications. The stability brought by a stablecoin is crucial in order to realize the full potential of blockchain technology because regular people and businesses will never use cryptocurrencies in their daily activities if those cryptocurrencies remain volatile.

People and businesses can borrow or lend DAI without the need of a third party and with more attractive financial terms (higher interest rates when you lend and lower cost when you borrow). Every loan is over-collateralized with a smart contract: you have to put ETH as a collateral representing at least 150% of the initial loan. The goal is to have a resilient mechanism to prevent major ETH value shifts.

The main challenge of building a crypto-backed stablecoin is security. You have to prevent any unexpected behavior that could happen automatically in the code run by the decentralized application behind the stablecoin.

As I told you during the intro, when ETH price dropped by 30% in one hour on March 12th, the liquidation system linked to Maker failed and somebody was able to steal $4m in ETH. Over collateralization was not sufficient to prevent this failure. More precisely, Maker protocol is connected to third parties that are supposed to liquidate risk positions in the system and one of these third parties failed to liquidate a position because of the drop and the congestion in the ETH network. Therefore, the protocol in itself did not break.

Maker compensated the loss by automatically diluting the stablecoin with a recapitalization done the week after the event mainly backed by VC fund Paradigm. It was one of the greatest stress test for the DeFi ecosystem. Maker survived thanks to this recapitalization but the event demonstrates several facts about the current state of DeFi:

Most projects are still in beta stages and users can lose their funds by using DeFi services,

Private investors (especially VC funds) are crucial to support the projects especially when these are struggling. Paradigm could hold around 3% of MKR and a16z around 6%.

VCs funds as well as the Maker foundation (12% stake) are whales in the project which is antithetical with the willingness to make it decentralized. Even if these stakeholders are crucial to fund and support the project development, a decentralization mechanism will have to be set up to reduce this token concentration.

Libra (2019, US-based, foundation created by Facebook)

Facebook announced Libra in June 2019. As opposed to most stablecoins it was supposed to be indexed not only to one currency but to a diversified basket of low volatility assets labeled in different currencies.

If Facebook had been able to make this original Libra used as the main currency on the internet, it could have possibly replaced national currencies and users could have ended converting their Libra into their national currency only occasionally for the last physical stores where Libra would have not been accepted yet.

Libra is managed by a non profit organization called the Libra Association aiming at reaching 100 founding members. Each founding member paid a minimum of $10m to join and optionally become a validator node operator, gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra. The Libra Association founded as a centralized entity was supposed to become decentralized over the medium term.

Libra’s Association Members at Launch in Jun. 2019

Libra’s Association Members at Launch in Apr. 2020

The public backlash mentioned in the introduction had the two following consequences:

Numerous strong stakeholders like Visa, Mastercard, Stripe or Paypal left the Libra’s association

Libra will no longer be a unique stablecoin but multiple digital version of the local currencies in the markets in which Facebook operates.

I discussed the weak value proposition offered by Libra in the introduction. Another issue is Libra’s Facebook paternity because GAFAM are at the forefront of the centralized world that cryptonetworks are trying to dismantle. Combined with the complete lack of trust from users and governments into the platform, Libra seems to be doomed like Sisyphus rolling his boulder to the top of the mountain.

Uniswap (2017, US-based, Coinbase and Paradigm-backed)

Uniswap is a decentralized exchange. It allows anyone with an internet connection, a Metamask wallet and some ETH-based tokens to contribute to the liquidity of the exchange and to earn commissions for doing this job. You no longer have a central structure like Binance or Coinbase managing the liquidity and the trades on the exchange.

Centralized exchanges maintain an order book and facilitate matches between buyers and sellers. Uniswap has smart contracts holding liquidity reserves of different tokens and trades are executed against these reserve. Prices are set automatically. Reserves are pooled by a network of liquidity providers. Each liquidity provider will earn a proportional share of the transaction fees compared to the amount he put in the network.

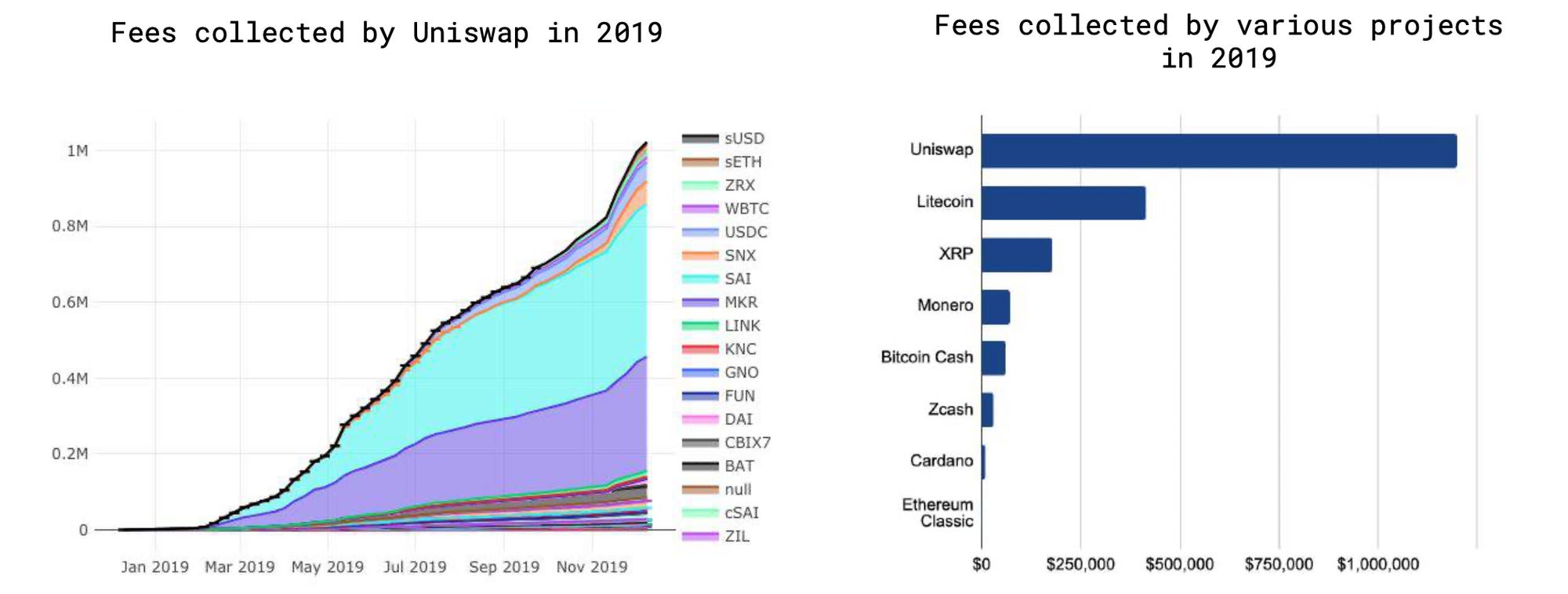

The company was started as a side project in 2017 by an engineer who wanted to launch something while learning Ethereum programming. The founder started to recruit other team members only after its seed round in April 2019. Uniswap experienced a strong growth during its first full year of operations in 2019 collecting more fees than numerous other flagship projects in the crypto ecosystem like Litecoin and Ripple.

Argent (2017, UK-based, Paradigm, Firstminute, Creandum and Index-backed)

Argent is a non custodial crypto wallet. It means that only the user can access his assets whereas a traditional bank has access to your assets and even has its business model based on earning interests from your assets. Thanks to this model, even if Argent goes bankrupt, you will still have access to your assets.

The company was founded in 2017 and raised a $12m series A round in March 2020 led by Sequoia crypto fund Paradigm. It’s the 1st investment of Sequoia's crypto fund in Europe. Existing investors Index, Creandum and Firstminute are also participating.

Argent has an amazing product compared to most DeFi consumer products. It simplifies the process of acquiring cryptos (reducing fees and steps) and investing in DeFi protocols like Compound or Maker. In fact, Argent has developed native integrations of DeFi protocols like Maker, Kyber and Compound that orchestrate automatically the operations between the wallet and the different protocols. As a result, with 1 click Argent, multiple calls are done to realize the desired actions. This is possible thanks to the composability of DeFi applications. It takes 30 seconds to make operations that took me 30 minutes to realize without Argent. It has the potential to become an app as popular as Cryptokitties and Coinbase allowing non crypto users to enter the crypto ecosystem.

Multis (2018, France-based, YC and eFounders backed)

Multis is building a crypto bank for companies. Multis is offering several financial services through a neobank-like user experience. The company was founded in 2018 in Paris within company builder eFounders and went to the US-based accelerator Y-Combinator (Summer 2019).

It's based on a multisignature wallets powered by two "money legos" which are Gnosis and Portis. A multisig is a smart contract that locks funds and requires the approval of a defined number owners with their own keys to process transactions. Multis offers the following financial services: fiat/crypto conversion, token swap, international wire transfers, lending to earn interests, borrowing, multisig permission management etc.

Cross-border payments is an interesting use case for DeFi applications highlighted in Multis offering. Those payments are extremely expensive and take days to be processed with legacy payment providers like Paypal or Western Union. On the contrary, using stablecoins allows you to send the funds instantly at almost no costs.

Thibaut Sahaghian (CEO) takes the following example. "Consider a $1,000 online purchase: Paypal will take a 4.4% transaction fee or $44 plus a fixed fee based on the currency received. Payment will be processed and settled within 4-9 days, depending on geographics. Now consider ETH or stablecoins. Same purchase, same geographics: the network takes a fixed fee of 20-50 cents—sending $1,000 or $100,000 does not change a thing. Payment will be processed and settled in minutes."

Multis is a another great proof of how powerful composability is in DeFi. In the below graph, Multis is showcasing all the partners it has used to build its neobank. Compared to what is happening in the traditional finance world where you have to applied to many different licenses and to build a robust infrastructure, in DeFi, you only have to combine several existing lego blocks layers and add your innovative banking layer to build a neobank.

We are still in the early days of Decentralized Finance. Ethereum (and hence DeFi) has the most active development community in the crypto ecosystem with c. 1.2k monthly active developers (out of 6.8k monthly active developers in crypto) but it remains a drop in the ocean compared to the 6m developers working on Android for instance.

The same reasoning applies to the number of users. Only 226k users interacted in 2019 with at least one DeFi protocols - less than the number of inhabitants in a medium-sized French city like Bordeaux (257k).

Nonetheless, I’m super excited by this DeFi ecosystem. I love the vision of bringing financial services to the 1.7bn people that don't have access to a bank account and to offer an alternative to our centralized banking system. DeFi has an edge compared to other many sectors: brilliant minds that are working to build great applications, tier one investors ready to back them and early adopters who understand the value provided by these new applications (cf. the below power user) but also who are willing to overcome all the UX pains and financial risks.

Thanks to Julia for the feedback! 🙏

See you next week for another issue! 👋