💰 Coupa - A Procurement Platform Being Acquired by Thoma Bravo for $8bn

Overlooked #134

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing a deep-dive on Coupa. It’s a business spend management platform which is being acquired by PE fund Thoma Bravo for a $8bn enterprise valuation.

Next week, I’ll release the 2022 edition of my French tech ecosystem report. I’ve been working on it for 2 months to make it better than the previous edition. I’m looking forward to hearing your feedback!

On Dec. 12th, tech buyout fund Thoma Bravo announced its intention to acquire Coupa for a $8bn EV which implies a 8.4x EV/NTM revenue multiple based on projected revenues from broker consensus.

With the current tech market meltdown, the two main actors acquiring a company will be: (i) market consolidators (cf. Figma’s acquisition by Adobe that I covered in a previous post) and (ii) PE funds acquiring top assets at attractive valuations (cf. Coupa’s acquisition by Thoma Bravo).

When the acquisition occurred, I was looking at Coupa’s model because I was looking at verticalized procurement solutions. The acquisition became a perfect excuse to spend even more time digging into the company.

Coupa is a US-based company started in 2006 which raised $165m in the private market from investors like Blue Run, Battery, Mohr Davidow Ventures or T. Rowe Price before becoming a public company in 2016. It’s a business spend management platform which helps businesses keep their indirect spending (i.e. spendings not related to the production of products or services sold by the company) under control. It has 4 core modules which are (i) travel & expense management, (ii) procurement management, (iii) AP management and (iv) payments. In the last twelve months, Coupa generated $818m in revenues with 1,730 customers generating over $100k in ACV and registered -$272m in operating profit.

My favourite thing about Coupa is that it’s a platform combining dynamics from the 3 most common business models in venture: SaaS, marketplace and financial services. Coupa is sold as a SaaS to its customers but it has cross-side network effects between its customers and their suppliers. Moreover, Coupa has been putting a strong emphasis in recent years on embedding financial services into its platform with Coupa Pay (e.g. paying invoices, offering early payment discounts to suppliers etc.).

I divided this post into the following sections:

History

Product overview

Operating & financial performance

Why is Thoma Bravo buying Coupa?

Why is Coupa an interesting business?

Part I - History

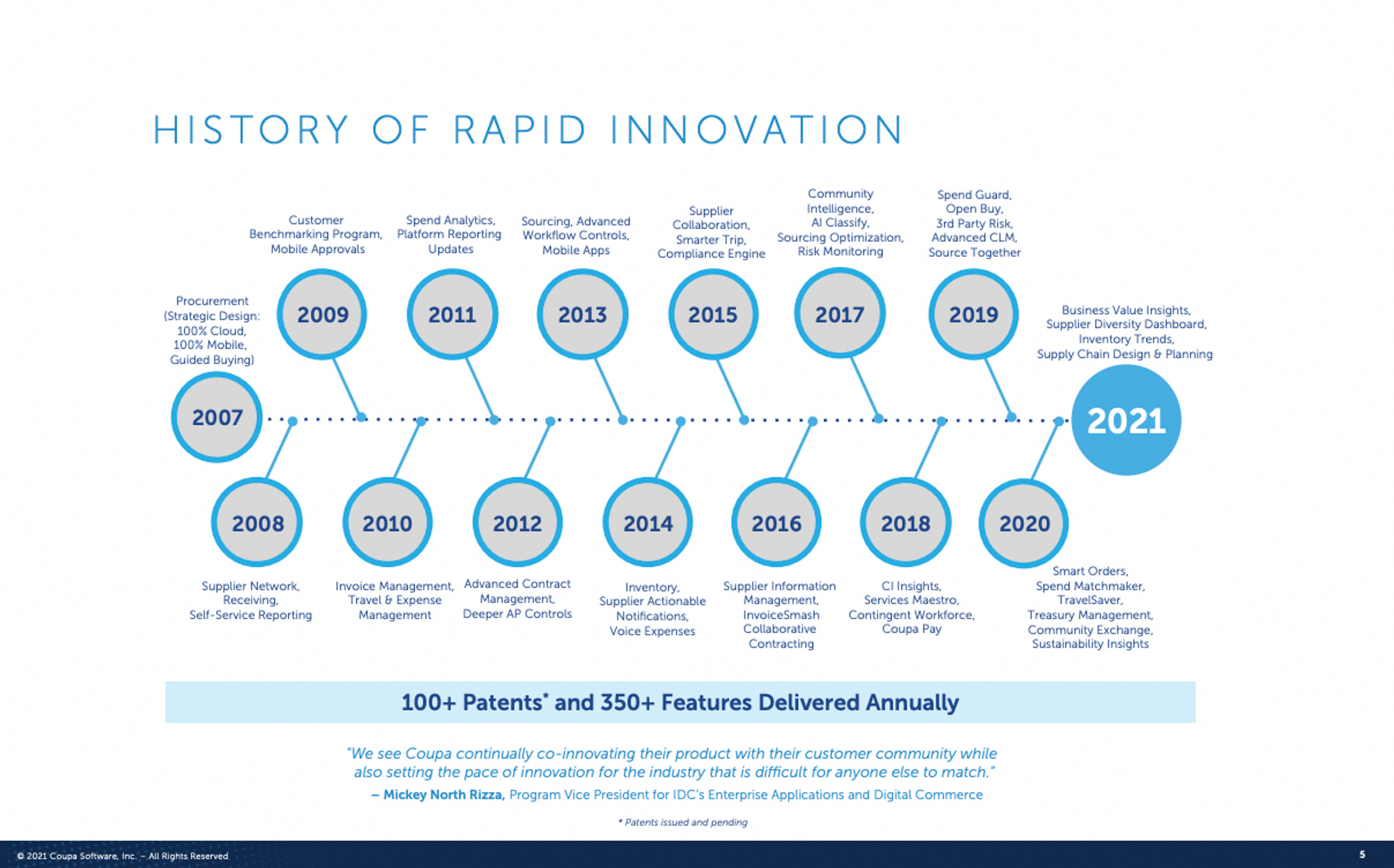

Coupa was founded in 2006 by Dave Stephens (CEO) and Noah Eisner (VP Product Development). It became a procurement platform in 2008 before raising a $6m series B led by Battery. In 2009, Coupa changed its CEO, with Rob Bernshteyn joining the company in February and Dave Stephens leaving it in September.

With the right positioning and top-management, Coupa started to grow at a strong pace (130% annual revenue growth between 2009 and 2012). It raised multiple rounds of funding every 12-24 months ($7.5m series C led by El Dorado in 2009, $12m series D led by Mohr Davidow Ventures in 2011, $22m series D led by Crosslink in 2012) and added several product modules (Supplier Network in 2009, Customer Benchmarking in 2010, Expense Management and Invoicing in 2011, Analytics in 2012, Advanced Contract and e-Invoicing in 2013).

Between 2014 and 2016, Coupa entered a new dimension while preparing for its IPO: (i) it managed to raise from flagship investors like Meritech, Iconiq and T. Rowe, (ii) it expanded in Europe, (iii) it started its external growth strategy (acquiring 4 companies).

In Oct. 2016, Coupa went public raising $133m at an initial $1.7bn valuation. Since then, Coupa has pursued its platform expansion combining internal product development and external growth with 3 main additions to its platform: supply chain management (following the $1.5bn acquisition of Llamasoft in 2020), payments (with the launch of Coupa Pay) and Community.ai (leveraging data from Coupa’s customer base to make AI-based and community based cost savings recommendations).

In Dec. 2022, a new chapter started for Coupa with Thoma Bravo’s $8bn acquisition, taking the company private.

Part II - Product Overview

Coupa is a business spend management platform. It has 4 core modules:

Procurement Management: streamline purchase requisitions and order processes (e.g. marketplace with pre-approved suppliers and in-inventory goods) to maximise spending under management, fraud detection and real-time budget management.

Accounts Payable Management: invoice management supporting electronic invoicing and providing automation to reduce manual tasks (automated approvals, automated reconciliation).

Travel & Expense Management: all-in-one travel and expense management solution (travel sourcing, booking, travel support, expense reporting, virtual payments, analytics, benchmarking).

Payments: payments orchestration (for payments to suppliers, employees and subsidiaries) and working capital management. Coupa Pay supports multiple payment methods including domestic and international bank transfers, one-time use virtual credit cards, digital checks and digital wallets.

Besides these 4 core modules, Coupa offers complementary applications including:

Supply Chain Design & Planning: model and optimise your supply chain.

Strategic Sourcing: find the best suppliers to operate your business with a platform to source suppliers and compare their bids.

Contract Management: contract lifecycle management (drafting, approval workflows, contract updates, alerts) giving autonomy to employees while improving efficiency for legal teams.

Contingent Workforce Management: platform to create requests to source and select contingent workers providers as well as to onboard them.

Treasury Management: optimise cash and liquidity thanks to a platform directly linked with business current and future spendings.

Supplier Risk Management: reduce third party-party risk with a platform to source, onboard and monitor suppliers.

Spend Analysis: AI-based and benchmark-based insights on your spendings.

To better understand Coupa’s platform, it’s worth looking at several customer success stories:

Sanofi (international pharma company with 100k employees and €35bn in revenues) decided to implement Coupa to streamline its procure to pay process. Before Coupa, Sanofi had 22 different systems and 40 different processes to manage procure to pay across geographies and entities. Today, Coup manages €10bn of spendings, is used by 60k different users and helps Sanofi being compliant worldwide.

Groupon (international marketplace providing deals for local experiences with 6.7k employees and $2.8bn in revenues) had no procurement tools before using Coupa. It decided to use Coupa to digitise procurement processes to have better visibility on spendings. 4k users are on Coupa, 80% of invoices are now backed with purchasing orders (vs. 40% before) and only 2 FTEs are working part-time as admins on Coupa.

Maersk (international shipping company) started to use Coupa to unlock procurement savings and digitise procurement processes by implementing systematic reverse auctions to select and manage suppliers.

Part III - Operating & Financial Performance

Coupa is targeting mostly enterprise customers or customers with the potential to becoming enterprise customers in the coming years resulting in an ACV that is above $250k.

Coupa sustained a strong annual growth in recent years (above 25% YoY) despite reaching large scale (above $300m in ARR).

Compared to most SaaS, Coupa is spending a high percentage of sales on sales and marketing costs. In the LTM, it was almost 50% of sales spent on S&M expenses.

Coupa is loosing money on professional services. It may be willing to lose money at onboarding because it knows that it’s an extremely sticky product once customers are properly onboarded and that it’s an important success factor to upsell customers other modules in the following years post onboarding. Moreover, Coupa has a relatively low gross margin on SaaS which has deteriorated over-time from 79.5% in 2015 to 67.7% in the LTM.

Coupa’s efficiency has massively deteriorated in the past 36 months. In FY20, Coupa was reaching 30.8% on the rule of 40. In the LTM, Coupa is now -15.6% on the rule of 40 because operating expenses were growing almost as fast as revenues.

Part IV - Why is Thoma Bravo Buying Coupa?

On Dec. 12th, tech-focused private equity firm Thoma Bravo announced its intention to acquire Coupa at a $8bn entreprise value which is a 8.4x EV/NTM revenue multiple based on brokers consensus and a 77% premium on unaffected share price. Coupa ran a competitive process with 14 buyers (3 strategic and 11 PE firms). Abu Dhabi Investment Authority is co-investing in Coupa as minority shareholders and Thoma Bravo has raised $2.6bn in debt to fund the transaction.

With the public tech market under meltdown, several private equity firms have kickstarted a buying spree. In 2022, Thoma Bravo (i) has raised $32bn in fresh funds and (ii) has acquired high profile tech companies such as UserZoom, Anaplan, Sail Point and UserTesting. Once Coupa’s transaction completed, Thoma Bravo would have invested 50% of its $24.3bn ****large-cap buyout fund.

This buying spree is driven by 2 main factors. First, public tech companies are now trading at attractive multiples. Second, the current macro context requires public tech companies to shift from a growth at all cost mentality to efficient growth and profitability. This shift requires changes that are too radical to be conducted in the public market.

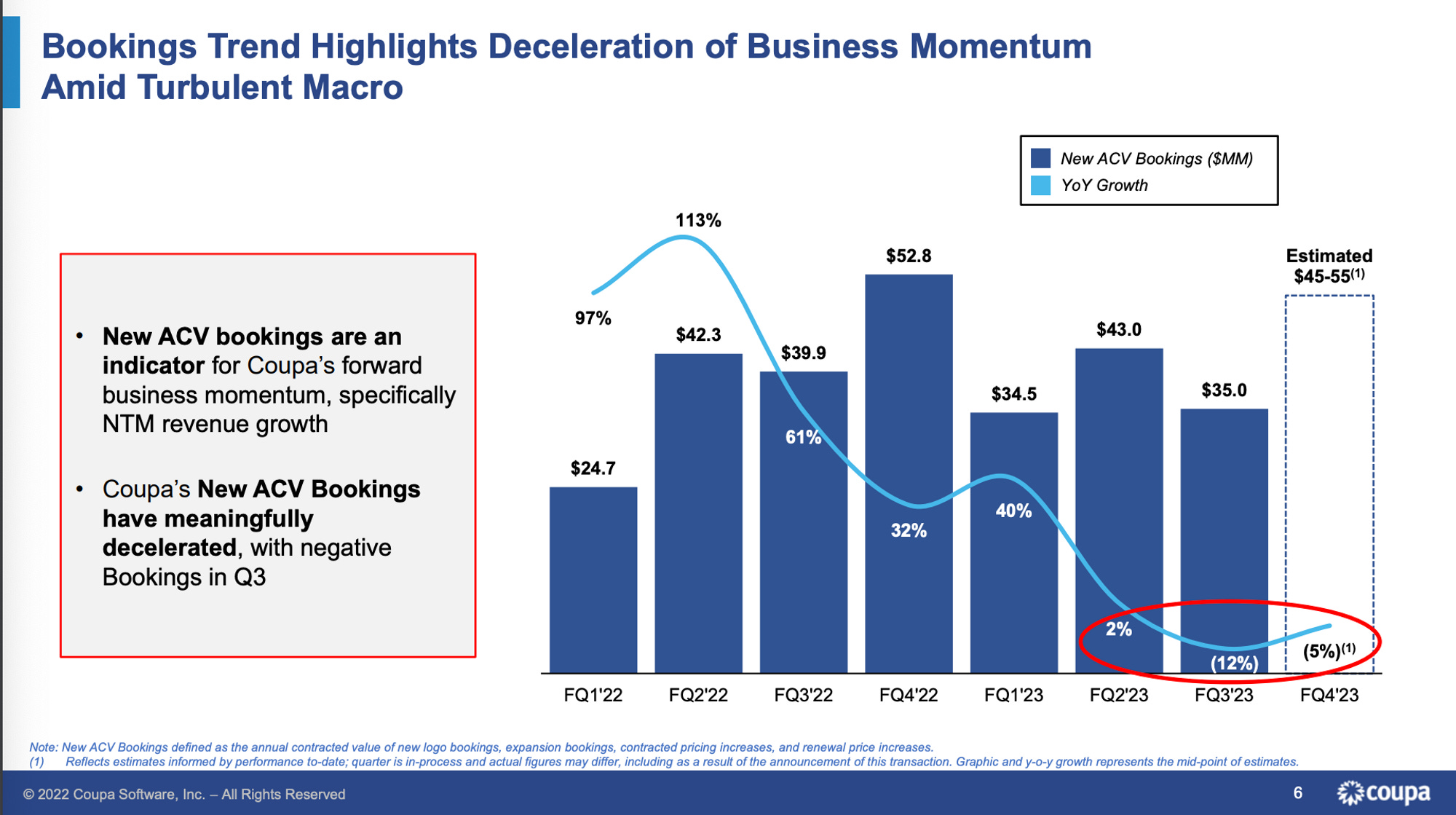

On Coupa, both factors are present. Coupa was trading at an historically low EV/Sales NTM multiple (with a bottom at a 5.1x EV/Sales NTM multiple in November). Moreover, as we saw in the previous section, Coupa has become a relatively inefficient business with operating expenses growing as fast as sales and with gross margin deteriorating. Lastly, Coupa is impacted by the current macro-environment pushing companies to make savings and to slow down their acquisition of new software with bookings declining YoY in Europe and flat YoY in the US.

Why is Coupa an Interesting Business?

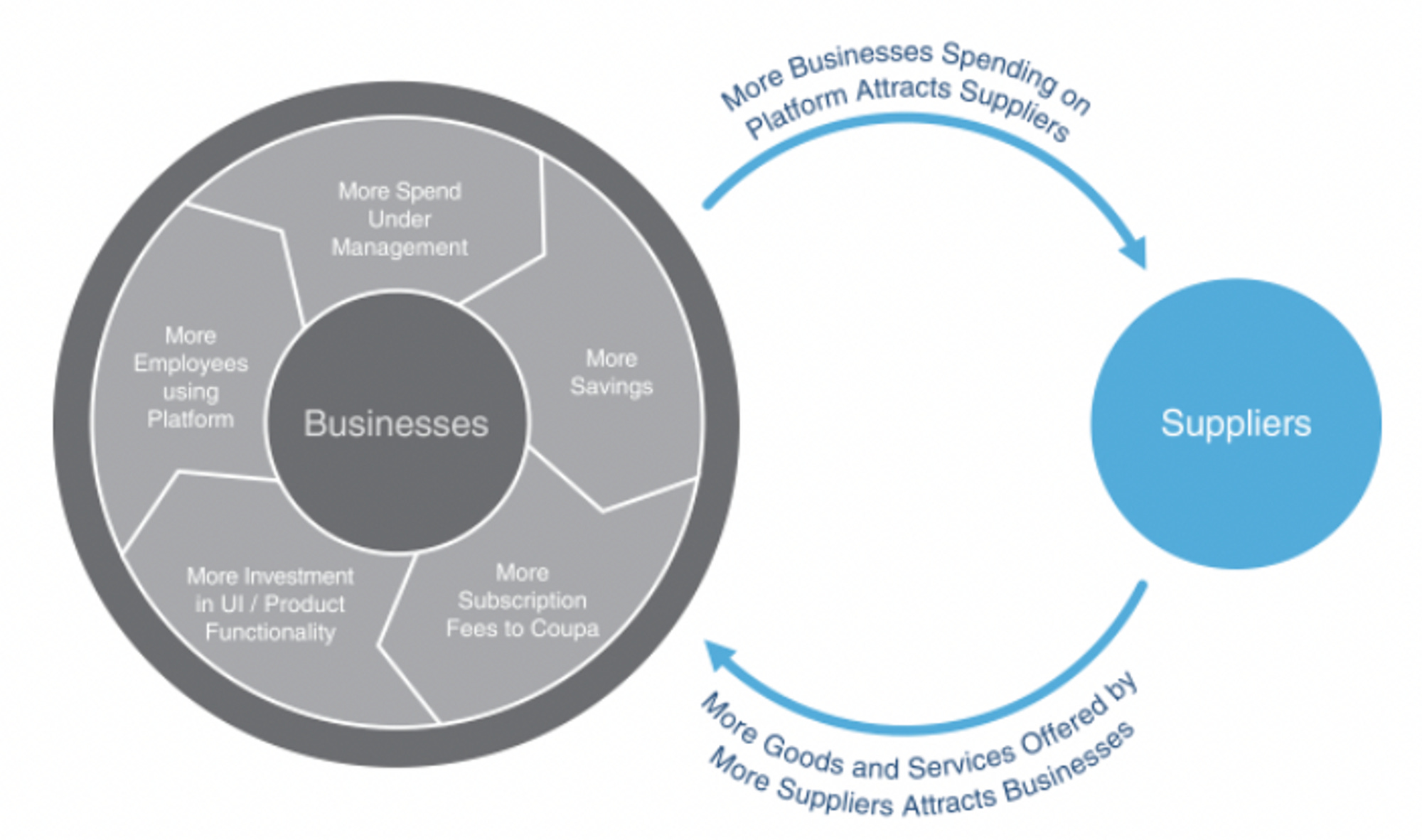

Open software. Compared to most tech solutions which are only used by its customers, Coupa is an open software used by its customers but also by the suppliers of its customers. It creates a network effect as suppliers can become customers and as after certain scale, suppliers can push companies to use Coupa as procurement platform.

Unbundling the ERP. Historically, an ERP was the system of records for companies to track all their fluxes. With its business spend management platform, Coupa is contributing to unbundle the ERP by becoming the system of records for suppliers and spendings. It’s a similar play also done by CRMs which are system of records for front office work and HCMs for employees data.

Fintech-enabled SaaS. Coupa is progressively embedding and scaling financial services in its procurement platform. It helps customers to streamline payments to suppliers and employees. It also offers methods to optimise working capital (e.g. early payments discounts).

Coupa is a “modern software”. It replaces on-premise, upfront fee, hard to use and closed products with a cloud-based, SaaS-based, easy to use and open-platform (for suppliers and third party apps built on top of Coupa). Its market momentum was the transition to the cloud. It’s a market momentum that was leveraged by many SaaS behemoths but that may no longer be sufficient for startups launching today.

Coupa has cross-side network effects. The more customers and the more spending under management is on Coupa, the more likely suppliers will start using Coupa’s interfaces. On the contrary, the more suppliers are using Coupa’s interfaces, the more savings can be unlocked for Coupa’s customers making its value proposition even more appealing for new customers.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Exceptional deep dive into Coupa’s business model. I loved it. Can’t wait to read the next article you push out. Cheers 🥂