💳 Amex - The Largest Financial Closed Loop Ecosystem

Overlooked #130

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m starting a series of company deep-dives in the financial services sector with a deep-dive on American Express.

Introduction

I’m starting a series of company deep-dives in the financial services sector. I’ll cover both incumbents and fintechs. I’m planning to publish one company profile every month. In the coming months, I’ll talk about Marqeta, Ramp, Modern Treasury, Block and nCino. If you want to co-author a deep-dive on Overlooked on another financial services company, let me know.

I’m thrilled to start with a deep-dive on American Express. I’m breaking down this deep-dive into 3 sections:

Part I - History

Part II - Product

Part III - Noteworthy Insights

History

In 1850, Amex was founded in New-York as an express mail business as a result of the merger of three companies owned by Henry Wells, William G. Fargo and John Warren Butterfield. An express mail business is a mail delivery service for which customers will pay a premium for faster delivery. Amex grew by expanding its geographical footprint in the U.S. via partnerships with other express mail, steamship and railroads companies.

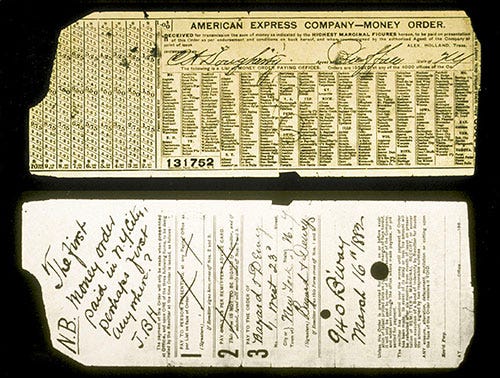

In 1882, Amex expanded into financial services by launching a money order business to compete with the US Post Office. A money order is a pre-paid cheque which is safer to send via mail compared to cash. It was used by workers to send money back to their families or by people who wanted to pay their bills and did not have access to a checking account.

In 1891, Amex launched a second financial services product with traveler’s cheques for travellers to get cash in local currency when they’re traveling abroad. Traveler cheques worked with a counter signature system and a watermark to identify them.

In 1917, the US government killed Amex’s express mail business by nationalising and consolidating all express companies in a single company whose mission was to serve the US national interests during WWI. Amex stayed solely a financial services business.

In 1958, Amex entered the card business with a card targeting business travellers.

At the time, cards were emerging with a first successful card program launched by the Diners Club in 1950. It was a charge card to pay in selected New York restaurants. Card members had to settle their bills at the end of each month. Diners Club had 20k members at the end of 1950 and 42k at the end of 1951. Restaurants were charged 7% per transaction and card members had to pay $5 per year.

To launch its card, Amex partnered with the American Hotel Association. It got immediate traction. It had sold 250k cards ($6 annual fee) and had 17.5k merchants at launch. 3 months later, Amex had attracted 500k members. It was not a credit card but a charge card for which members had to pay off their balance at the end of each month.

In 1959, Amex was the 1st issuer to introduce a plastic card which is more resistant than a paper card and whose data (name, address, card number) could be read by imprinters.

In 1963, Amex was impacted by the salad oil scandal. Amex had a subsidiary providing loans to warehouses in exchange of collateral in physical inventory. A company called Allied led by Anthony De Angelis tricked the system and put sea water instead of oil into barrels to raise debt from Amex. When Amex discovered the scam, the stock lost 50% of its value as instead of having $150m in collateral, Amex’s inventories were only worth $6m. In the middle of this corporate crisis, Warren Buffet became a significant shareholder in Amex, knowing that the company would survive the scandal.

In 1966, Amex launched its Gold Card.

In 1984, Amex introduced its Platinium Card. It was launched as an exclusive product. It cost $250 per year and it was offered by invitation only by Amex to its top card members (high spendings, long tenure, great payment history, etc.). In 2019, Amex’s Platinium Card became more broadly accessible via applications.

In 1987, Amex launched its Optima Card which was its first credit card without the need to have to fully pay back your balance at the end of each month.

In the 1980s, Amex made several acquisitions to become a financial services conglomerate. It acquired companies in investment banking, trading, brokerage and international private depository.

In 1991, Amex launched a Membership Miles program. It’s a program in which card members earn 1 point for every dollar spent on their Amex’s card and in which they can redeem points to purchase plane tickets from top airlines.

In 1993, Harvey Golub became Amex’s CEO and Chairman. He was recruited to turn around the business. He implemented a strategy to refocus Amex around the card business and away from the grand vision to become a financial supermarket. As a result, Amex divested is all the activities not related to its card core business n the following year.

In 1995, Amex launched a co-brand credit card with Hilton.

In 1996 Amex opened its network to other banks to let them issue cards on Amex’s network. As a result, banks started to partner with Amex which also acts as card issuer instead of just being competitors. In 2019, 44m out of 114m Amex’s cards were issued by third party banks.

In 1999, Amex launched its Centurion card. It was the same rationale as the Platinium Card: opening a new segment for Amex’s most affluent and loyal members. The card was accessible only by invitation and cost $1k per year at introduction (vs. $5k today) with a $10k initiation fee.

In 2002, Amex launched a card called Clear which was advertised as the first credit card without any fee.

In 2004, Amex launched a co-brand credit card with Costco which was also usable as a Costco’s membership card. Amex and Costco ended their partnership in the US in 2016. Costco replaced Amex by a co-brand program with Citi and Visa. It was a big loss for Amex as Costco was generating 9% of Amex’s volumes and 20% of its interest bearing credit-portfolio.

In 2008, Amex acquired GE’s Corporate Payment Services business for $1bn to expand in the B2B segment.

In 2019, Amex acquired LoungeBuddy which gives a pay per use access to airport lounges around the world.

Product

General Description

American Express offers solutions for 3 main personas: consumers, businesses and merchants.

For consumers, it provides personal cards, savings accounts, personal loans, checking accounts and gift cards.

For businesses, it provides business cards, corporate programs, payment solutions, business checking accounts, business line of credits.

For merchants accepting the American Express payment network, it provides marketing tools, financing & payment solutions and savings on third party providers (e.g. Fedex, Quickbooks, Indeed, Snap Ads, Faire, etc.)

For Consumers

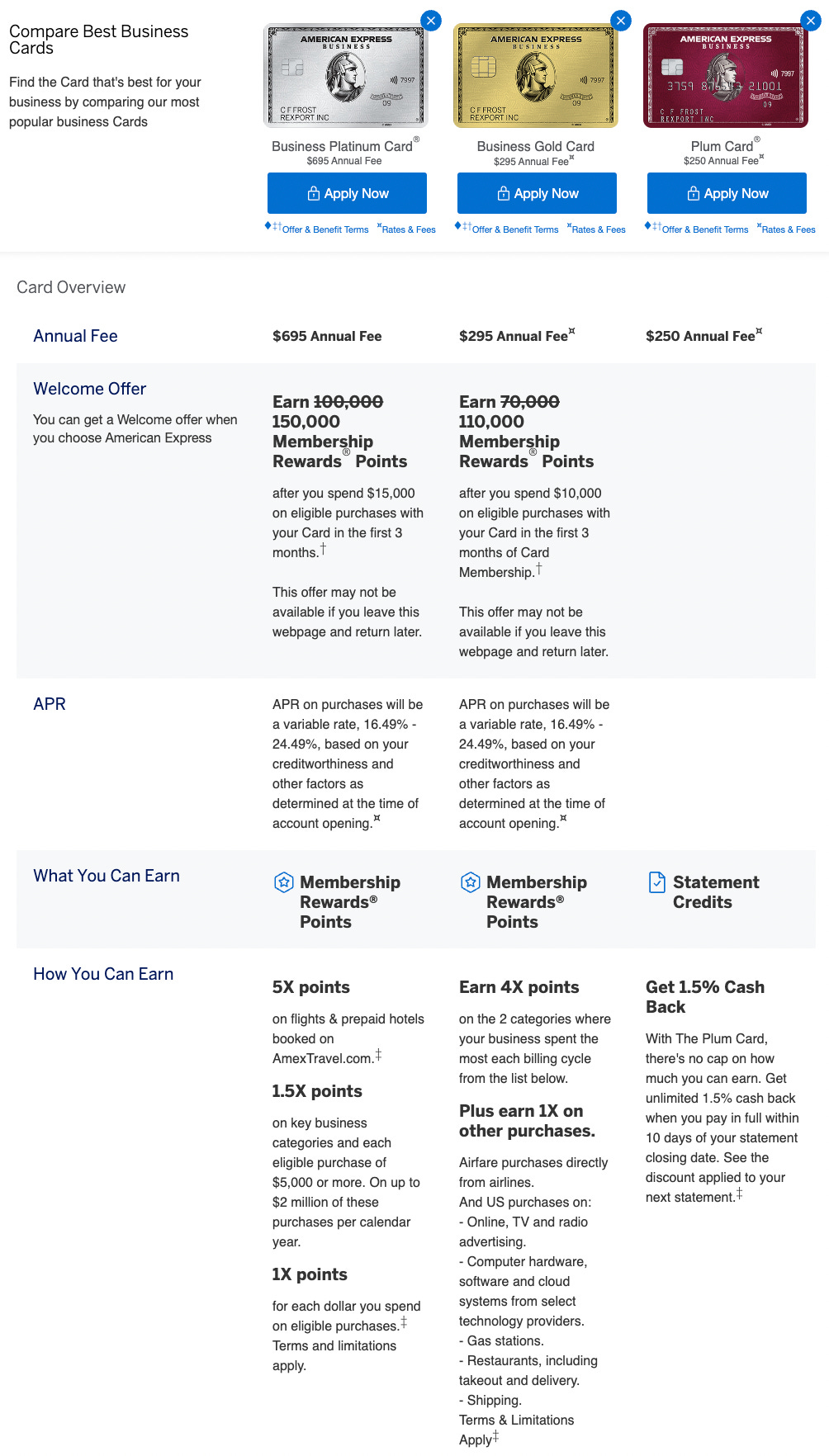

Amex’s flagship product for consumers is the credit card. Amex offers 15+ different credit cards depending on consumer preferences.

Some credit cards are free. Other credit cards require consumers to pay an annual subscription (e.g. $695 per year for the Platinum Card).

Amex also has major co-branded credit cards programs with partners like Delta, Hilton or Marriott which give specific benefits when you’re spending money with them (e.g. for Marriott, credits to spend at the hotel, free nights, free room upgrades, premium interne access, etc.).

Amex offers an attractive cash-back program. Every time you spend with your Amex’s credit card, you earn points that can be redeemed at specific merchants locations (e.g. Walmart, Uber, Audible, etc.). By default, you earn 1 point for every dollar spent. On certain purchases, you can multiply the number of points per dollar spent (e.g. 5x on prepaid hotels on AmexTravel.com).

Besides credit cards, Amex offers other products for consumers whose goal is mainly to bring consumers into its ecosystem and to convert them in the mid-term to buying an Amex’s credit cards. For instance, it offers a debit card offering a 0.6% annual return on your balance and points on your spendings. It also offers a high yield savings account with above the market returns and less constraints (e.g. no minimums).

For Businesses

For businesses, Amex also offers credit cards with a cash back-back system offering more rewards than personal credit cards because interchange fees are higher on business cards, offering business-specific benefits (e.g. discounts on specific software solutions like Adobe or Indeed) and including business-specific features (e.g. pay over time option, expense management, connection with accounting tools, etc.).

Around the credit card, Amex has a suite of financial tooling to make businesses much more efficient. It includes expense management (Amex @Work), AP automation (Automated Payment Solutions), single used cards (vPayments) and business lending (Kabbage).

For Merchants

When Amex tries to be accepted by a merchant, it explains that Amex (i) has 112m card members in the US, (ii) has become a mainstream payment method in the US (99% of places in the US accepting credit cards accept Amex), (iii) attracts higher spending consumers and (iv) unlocks specific benefits like free marketing to consumers (free signage) and specific discounts with third party service providers.

Revenue Streams

Amex has 3 main revenue streams: (i) discount revenues which is the percentage Amex takes on transactions processed by its merchants partners, (ii) card fees which is are annual membership fees paid by Amex’s B2C and B2B cardholders, (iii) interest income on credit cards and on other loans provided to B2C and B2B businesses.

Noteworthy Insights

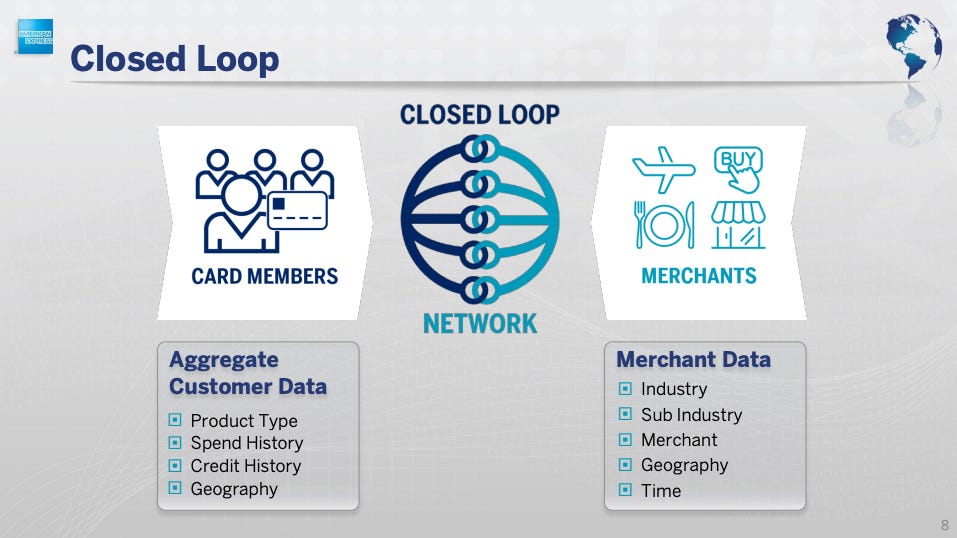

Amex is a closed-loop ecosystem that directly owns the relationship with both its merchants and card members. On the contrary, Visa and Mastercard are open-loop ecosystems. Both are open card networks that will work with third parties (merchant acquirers, merchant processors, issuer processors, payment issuers) which will own the relationship with merchants and card members. With a closed-loop ecosystem, Amex accesses unique data on both its card members and its merchants that can be leveraged to create an unique value proposition for each of them (e.g. having a higher spending limit on its credit cards for B2B businesses, having the best cash-back program for B2C card members or giving marketing tools to merchants to target Amex’s card members).

Amex is a vertically integrated model combining card issuing, merchant acquiring and a card network. It improves unit economics and it gives you access to richer data that you can leverage to offer unique products to both merchants and consumers. This model is Amex’s main moat creating both differentiation and a more attractive financial profile compared to most other players in the payments value chain.

Amex is selling status much more than a simple card. Amex’s consumers are called Card Members. Amex wants them to belong to an exclusive club which gives them a top-notch customer service and special rewards. Amex has been great at segmenting its users into tiers (Green → Gold → Platinium → Centurion) with each tier getting access to new and unique benefits and with the last-tier being reserved to Amex’s top card members.

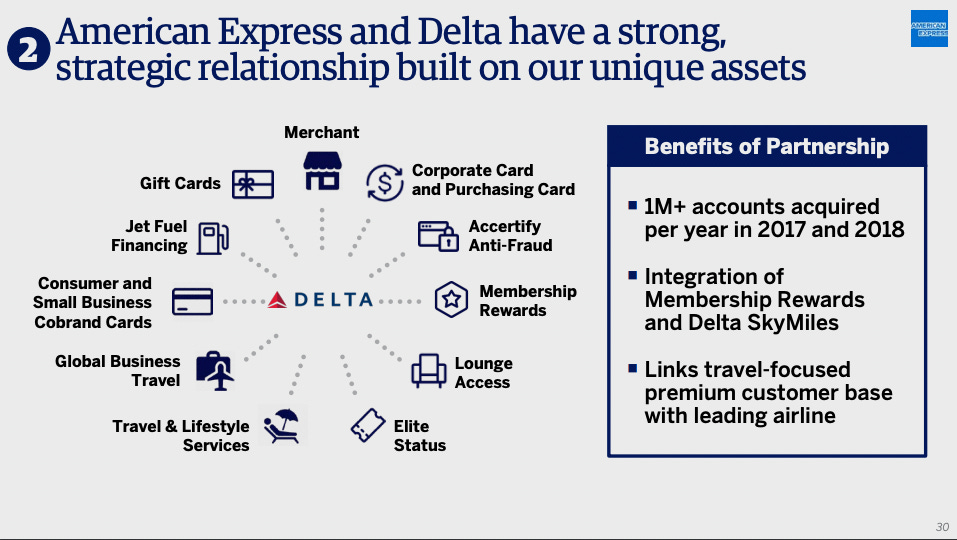

Amex pioneered co-branded card programs with leading B2C and B2B brands. Today, it is quite mainstream to add financial services as a revenue stream when you have established a strong brand. Launching a card for your customers to capture interchange fees on their spendings and strengthen your relationship with them has become easier with card issuing platforms like Marqeta or Stripe. But Amex has been offering this model to brands for several decades. It started in the travel space (e.g. with airlines, hotels and car rental companies) in which it has a strong footprint but has since expanded in other categories (e.g. partnering with Amazon or BMW). Moreover, with its vertically integrated positioning, Amex is able to build multi-dimension partnerships going beyond sharing interchange fees with a strong brand. For instance, Amex’s partnership with Delta enable all Amex’s business and consumer cardholders to access specific benefits when they’re traveling on Delta (additional miles, lounge access, elite status etc.).

“On a long enough timeline, everyone sells financial services.” Amex started as a delivery company in 1850 and introduced financial services to support its delivery operations. Moreover, Amex leveraged its vertically integrated model to enable many strong non-financial brands like Amazon, Costco, Delta or Hilton to launch their own card program.

In B2C, Amex is focused on premium consumers with higher spendings (3x average annual spend for Amex card members vs. competitor cards) and better credit profiles. As a result, Amex has less card members than other card networks (in 2019, 114m members compared to 2bn for Mastercard and 3.3bn for Visa) but is able to extract much more revenues per card member ($350+ per card holder vs. less than $10 per card holder for Visa and Mastercard).

In the SMB segment, Amex’s credit card is a wedge to build a broader suite of financial tools. In the US, Amex has a strong footprint in the SMB segment with its business cards capturing 45% of total spendings, having a 97% annual renewal rate in 2021 and being 3x larger than its closest competitor. But Amex’s strategy is to go beyond cards to become an all-in-one financial platform for SMBs. There is a strong potential as 70% of Amex’s B2B customers use only 1 product in its product suite.

Amex has a dual strategy to ramp-up merchants’ coverage: direct for large merchants, indirect for the long-tail. Directly, it has a sales team signing and managing large merchants (e.g. Amazon, Delta, Walmart) which represent 13% of accepting locations but 73% of the spend volume. Indirectly, it partners with card issuing platforms (Fiserv, FIS) and merchants acquirers (Stripe, Square, Adyen). Merchants acquired indirectly are key for the coverage, as they represent 87% of accepting locations but only generate 27% of spend volume. With this strategy, Amex has reached a 99% coverage in the US, being as accessible as competing card networks Visa and Mastercard.

Revolut re-used Amex’s initial wedge to target business travellers. Revolut started with a cardthat offered free currency exchange and money transfers (up to £500), aimed at business travellers and expats. It was the initial bet that allowed them to become the financial super-app that we know today. Similarly, Amex’s initial financial products were money orders targeting workers that worked in a different State than their families (launched in 1857) and travellers checks for business travellers who needed cash when they arrived in a new country (launched in 1891).

Thanks to Julia for the feedback! (🦒) Thanks for reading! See you next week for another issue! 👋

Wow great piece !!!

Brilliant piece!! Thank you !!! I just got my AMEX in EU and still wondering why thier fintech and SME/B2B services are so simple. You don't even have english language in the Belgium app and Apple Pay.

How could they lost all of the fintech hype!