🚗 11 Key Learnings for B2B Marketplaces from Studying ACV Auctions

Overlooked #169

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a deep-dive on a B2B marketplace in the automotive space called ACV Auctions that I co-authored with my friend André.

By the way, in 2024, I’m planning to write deep-dives on ServiceNow, Zoho and Odoo. If you’re interested to co-author a post on these companies, feel free to reach out at adewez@eurazeo.com.

I discovered ACV while exploring vSol for the automotive industry and writing about Shopmonkey. I knew almost immediately that I wanted to cover the company for three main reasons. First, publicly listed B2B marketplaces are scarce, and ACV is probably the most successful one in the US. Second, it’s an execution masterpiece, both in terms of exponential growth and B2B marketplace monetization by layering in additional services, including transportation, logistics, and insurance. Third, I knew that I would have a great co-author with my friend and fellow investor André from Talis Capital, who's been spending a lot of time on marketplaces.

We divided this post into the following sections:

History

Product

Unit Economics

Key Learnings

History

In Nov. 2014, Jack Greco, Joe Neiman and Dan Magnuszewski cofounded ACV in Buffalo in Upstate New York. Dan was managing director at a local incubator called Z80 Labs in Buffalo, Joe had built out an independent dealership and Jack was a local entrepreneur, CFO and investor.

In Jun. 2015, ACV sold its first car and raised a $1m seed round from angels and received a $1m investment from 43 North.

In Jan. 2016, after finding PMF in their operations in Upstate New-York, ACV started to expand into new East Coast territories including Pennsylvania (first) and North East Ohio, Western Massachusetts, as well as Washington (last). In Sep. 2016, they raised a $5m series A led by Tribeca Venture Partners with the participation of Softbank, Armory Square and Rand Capital. With the funding round, George Chamoun joined the company as CEO. George previously cofounded Synacor which was a tech partner for video and communication companies. At the time, ACV was working with 800 dealerships.

In Mar. 2017, it raised a $15m series B led by Bessemer. In Jun. 2017 it expanded into 8 additional territories on the East Coast including Boston, Cincinnati and Nashville. In 2017, ACV also launched its first value added services with an insurance called Go Green.

In 2018, ACV raised two funding rounds: a $31m series C in March with Softbank and Bessemer and a $93m series D in December with Bain. It went from 5k cars to 10k cars sold monthly in this timeframe. ACV expanded into adjacent markets, first the Midwest and then the West Coast. It also launched ACV Transportation as a second value added service.

In 2019, ACV launched its third value added service with ACV Capital. It also made its first acquisition with TrueFrame which is provider of comprehensive vehicle inspections for dealers and their retail consumers. It brought to its marketplace two key product innovations to bring inspection to the next level with AMP (Audio Motor Profile) to record engine sounds of vehicles sold on its platform and with Virtual Lift which was a mobile vehicle undercarriage imaging tool to take pictures underneath the car without having to put it on a lift. It concluded the year with a $150m series E raised in November at a $1.5bn valuation with Wellington and Fidelity.

In Apr. 2020, it acquired ASI which is an automotive inspection service for commercial vehicles (off-lease, off rental, fleet). It helped ACV to expand its sourcing from retail oriented dealers to commercial wholesale.

In Mar. 2021, it went public raising $400m at a $3.9bn valuation. In Jul. 2021, it acquired MAX Digital which is an inventory management system for $60m.

In 2022, it launched several product innovations on its marketplace including programmatic buying and private marketplaces for major dealer groups which want to keep more supply in-house within the group in a macro environment in which inventory has become more difficult to acquire. It also acquired Monk which is an AI-inspection tool for $19m.

In Oct. 2023, it launched ClearCar which is a suite of products for dealers to source consumer vehicles using real time market data to price cars based on their condition. It’s ACV’s third way to source vehicles beyond dealer sourcing and wholesale sourcing.

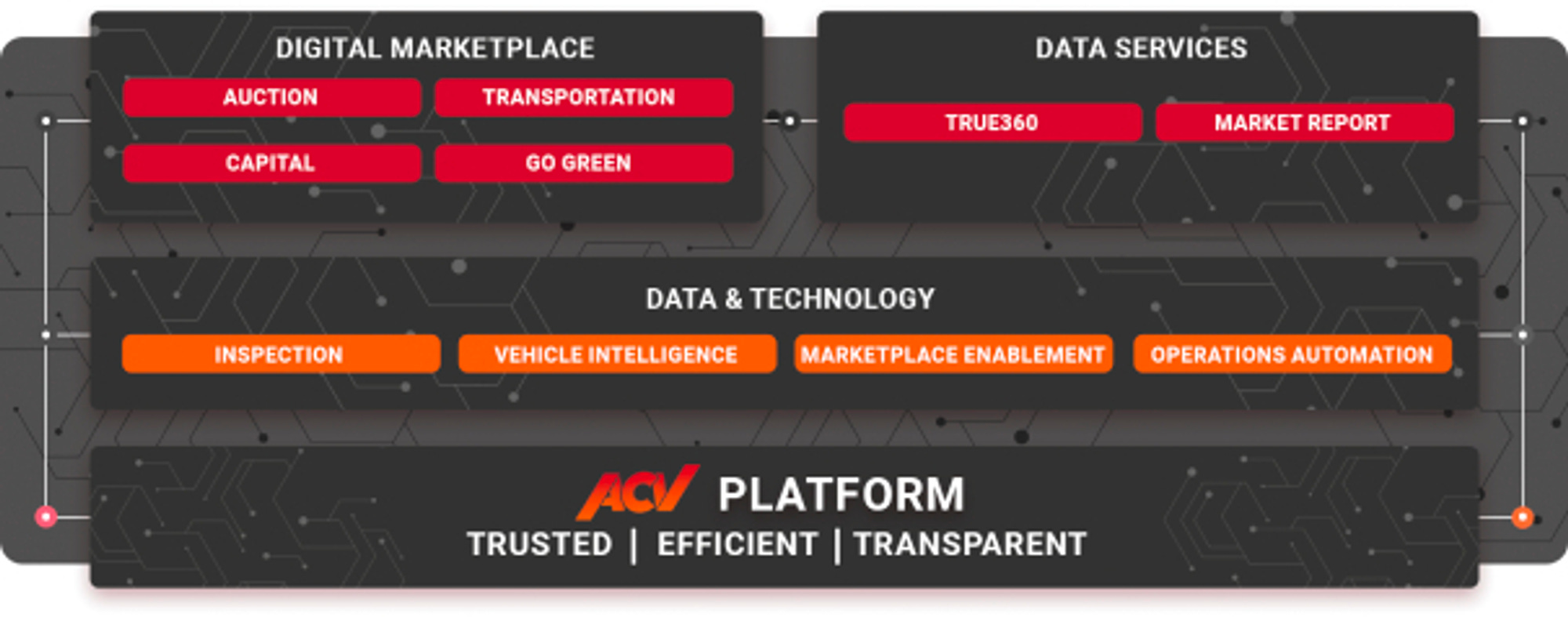

Product

ACV is a B2B marketplace connecting wholesale buyers and sellers of used vehicles across the US. At its core, the company replaces physical auctions with an online alternative for sellers to run 20-minute live auctions. Thanks to technology, ACV has created an alternative that is better (with the average dealership transacting c.50 cars per year), cheaper ($300 more profit per car sourced on ACV on average) and faster (20h saved per month) than physical auctions.

For each listing, ACV will generate a vehicle inspection report which is performed by an ACV trained inspector who will follow a detailed inspection process. He will take 30-40 photos of the car. He will answer 25+ questions on the car. He will use a ACV’s Virtual Lift to take 2k+ photos of the car’s underbody. He will record the sound of the engine with ACV’s Audio Motor Profile tool.

When buyers and sellers transact, ACV upsells them complementary value added services including insurance (GoGreen, 99% attach rate), transportation (50% attach rate) and financing (10% attach rate). On insurance, ACV sells an insurance product for sellers to protect them against claims from buyers on defects not identified on the vehicle inspection report. On transportation, ACV has a network of carriers to transport cars across the US optimising costs and transportation times. On financing, ACV offers working capital financing for buyers to purchase cars on ACV. In 2024, ACV will also launch ACV Capital for ClearCar to help dealers fund cars’ acquisition from consumers.

Moreover, ACV is selling SaaS products to car dealers including vehicle inspection reports (True360 Report) and market reports on used cars transactions.

Unit Economics

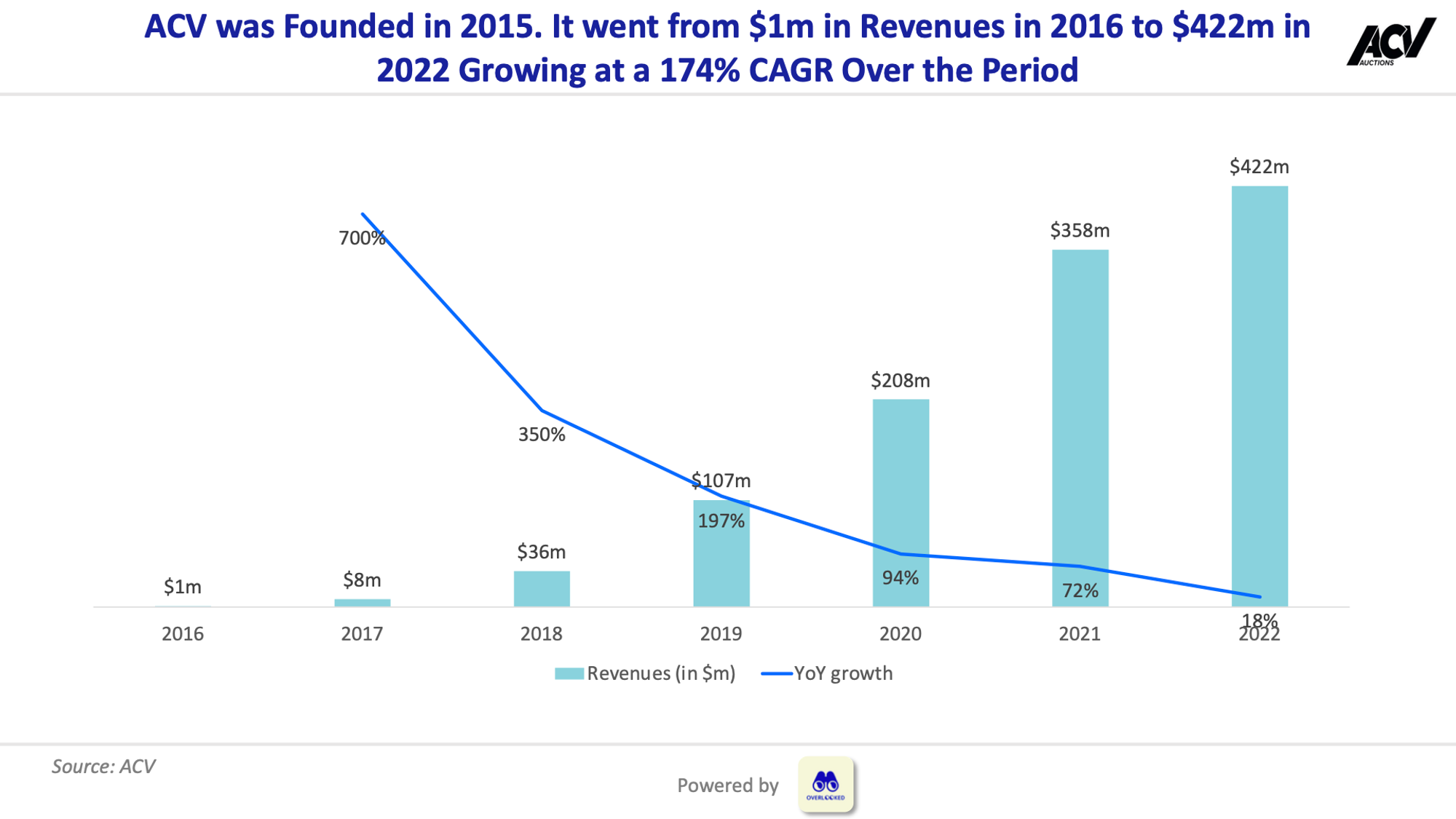

ACV has experienced exponential growth since its inception in 2015. It went from $1m in revenues in 2016 to $422m in 2022 growing at a 174% CAGR over the period.

In 5y, ACV increased its GMV by 14x from $635m in 2018 to $9bn in 2022. ACV experienced a massive growth spurt between 2018 and 2021, however due to the overheated used car market in the US, growth slowed down significantly in 2022. In 2022, ACV had only a 14% GMV annual growth (vs. 139% in 2021) mostly driven by AOV growth (from $14k to $16k) as the number of units sold declined by 3% YoY (compared to 30% for the entire dealer wholesale market).

With scale, ACV managed to improve its profitability reducing its EBIT margin from -74% in 2019 to -25% in 2022. Whilst overall gross take rate has reduced with scale, ACV significantly improved their net take rate. In 2022 ACV had a 4.7% gross take rate (vs. 5.94% in 2019) and a 2.1% net take rate (vs. 1.3% in 2019). This is as fixed costs as % of sales are declining on the incremental unit sold.

In terms of unit economics per vehicle sold, ACV charges both the seller and the buyer. The seller has to pay a $50 listing fee and a $75 insurance fee (Go Green). The buyer has to pay a buyer fee which is a percentage of the car value capped at $350. On top of this take rate, the buyer can pay for additional value services like transportation and financing. In 2022, ACV made on average $772 per vehicle sold (vs. $442 per vehicle sold in 2019). On the variable cost side, ACV has to pay for the vehicle inspector, the titles clearing, the payment, the financing and the insurance. It ends up making $339 per car post variable costs.

11 Key Learnings for B2B Marketplaces from Studying ACV

Human intensiveness. It’s hard to digitise a B2B transaction without a human intensive motion to onboard and animate suppliers as well as to streamline transactions. “It's a ground game. It really is. You have to be out there interacting daily with dealers.” said an ACV’s sales manager in an expert call. In the end, ACV is a human intensive business relying on a network of field sales and inspectors. This network is necessary to create the trust needed to enable digital transactions and it’s a long term moat -extremely hard to replicate for a new entrant. ACV operates nationally in the US, which is split into over 200 territories. In each territory, it has a territory manager overseeing a direct sales team and vehicle condition inspectors. Direct sales are in charge of acquiring new dealers and expanding ACV’s share of wallet within dealers that are already in its customer base. Inspectors are visiting dealers in the customer base on a daily to weekly basis in order to inspect the vehicles that will be sold on ACV’s marketplace.

10x experience. To digitise a B2B transaction, you need to create a digital experience that is 10x better than the physical experience. For both parties, ACV provides a 10x improvement compared to physical auctions because it’s:

Cheaper: 2/3 the price Manheim would charge in physical auctions because Manheim’s cost structure is higher with people inspecting, washing, reconditioning and driving cars around at the physical auction.

Better: more liquidity and more informed purchasing decisions thanks to ACV’s vehicle inspection report which is much more informative than looking a car for 5 minutes in a physical auction before submitting an offer.

Quicker: replacing the need to go physically to an auction by 20-min online auctions per vehicle.

Trusted thanks to GoGreen assurance. In fact, the trust layer is the most important part here as ACV was the first to stand behind their condition reports, which was key to move these transactions online.

Going deep before going broad. Before scaling as a marketplace, it's essential to narrow your focus to a specific geography or subcategory where you can ensure both buyers and sellers are more satisfied than they would be with any alternative. As Sarah Tavel said in her hierarchy of marketplaces, “the ultimate success of your marketplace will depend on your ability to create meaningfully more happiness in the average transaction than any substitute”. ACV followed this playbook by building a high density and frequency of transactions in Upstate New-York before growing more aggressively into other US states.

TAM Expansion. As you grow as a B2B marketplace, there are multiple levers that you can activate to expand your addressable market. ACV used a combination of the following levers:

Expanding its geographical scope starting from upstate New-York before expanding to the East, then the West and now operating nationally in the US over 200 territories.

Adding value added services to increase your take rate with services such as insurance, financing and transportation.

Expanding into other used vehicles supply pools starting with used vehicles from dealers before expanding into used vehicles from commercial wholesale (leasing & renting) and giving tools to dealers to helped them source used vehicles directly from consumers (C2B2B).

Monetisation through productisation: ACV expanded their monetisation significantly over time by layering in additional services. In the last reported full financial year (2022), principal auction transaction generates c. 2.0% take-rate. Layering on transportation and financing of the transaction adds c. 1.7%, assurance that ACV gives buyers adds c. 0.7% and the data business generates c. 0.4% take-rate. In combination this results in a take-rate that is more than double the original 2.0% at c. 4.7%. However, one must note that many of these businesses have vastly different levels of profitability, i.e. in combination the auction and assurance vertical is c. 75% gross margin, whereas transportation and capital is only c. 13% gross margin and the data services business is c. 33%. Especially transportation benefits from territories maturing and so does the inspection business, so these verticals offer significant upside and whilst they may not be as profitable as the initial transaction revenue, they offer significant LTV expansion potential.

Consumer-like customers in B2B setting: ACV has a very unique customer profile in that their B2B customers (dealerships) behave more akin to consumers in terms of transaction speed, yet have very high AOV (>$15k per unit). Car dealerships are principally a volume business where traded-in vehicles tie up liquidity and cost floor space. Hence, if a dealer chooses to sell a car at auction, he is interested in a fast efficient turnaround, minimising their cost associated with the process and speeding up their cash conversion cycle. This is the core product that ACV delivered with their 20-minute auctions, allowing franchise dealers to free up cash quickly and wholesalers and independent dealers to buy at any time, compared to the usual process of physical auctions, which happen more infrequently and were a far worse customer experience for dealerships (e.g. no need to visit an auction).

Built traction first: The principal product ACV offers is a transaction and given the consumer-like behaviour of their customers, the founding team proved out the product in Buffalo, NY, generating significant GMV off the back of a simple website and mobile app. Being the best in a small geography proved network effects early, which we see in the rapid maturing of new states that ACV expanded to only a few years ago today. Unless a B2B marketplace appeals to large enterprises with longer procurement processes, it is often possible to prove its potential without the need to build a very large initial software product. ACV is a prime example of building traction first and executing on a product strategy based on that initial finding of PMF.

Acquisitions: ACV acquired 5 companies, starting in Dec-19 with the acquisition of TrueFrame and ASI (Apr-20), both vehicle inspection providers, MAX Digital (Jul-21) a dealership SaaS, Drivably (Feb-22) a trade-in software for dealerships and Monk.ai (Feb-22) which provides automated vehicle damage detection services to automate car condition reporting. These acquisitions have been part of the objective of becoming an end-to-end partner to dealers and to selectively enhance parts of ACVs roadmap. For instance, Monk allowed ACV to further leverage its data moat using inspectors label damages data to enhance Monk’s AI capabilities of Monk, which in turn decrease inspection costs for ACV as a whole.

Going National: ACV allows for buyer matching nationally, because the product is digital first. The B2B car auctioning industry was mostly analogue when ACV started, and given people wanted to inspect cars ahead of buying, the buying radius was limited. ACV launching digitally and offering assurance as well as transport partners technically facilitates a far larger radius than was originally possible. However, the individual playbook ACV uses is still focused on franchise penetration within individual states as network effects start locally. This lent itself to an adjacent market hypothesis going geography by geography, increasing density exponentially.

Market and platform advantage: ACV had a significant headstart to the industry. Joe Neiman spent nearly 7 years in the industry, owning his own independent used car dealership turning over 500 units annually. Dan’s father owned a car dealership. Jack was in retail and his father was in auctions. Prior to launching, the team also worked in the industry for a year. 50% of their initial staff came from auctions or dealerships. This meant the team had significant internal knowledge of the industry and it also guided how they could think about product. Understanding workflows and customers, especially in under-digitised industries is a great competitive advantage and something ACV was able to utilise. Importantly, given its extensive experience, the founding team was also simply able to speak the language of the industry rather than being perceived as someone coming from the outside telling people how to operate.

Moats: Moats in this business centre around transaction velocity. New entrants will have a hard time competing with a platform like ACV as they leverage their significant scale. Today, ACV offers coverage of the entire US market and is starting to leverage significant cost advantages on a transaction level through having territorial saturation. In essence, the more transactions ACV does, the better the prices for their transport can become, to an extent where they are unmatched. The same goes for their financing offer and their data services. ACV exhibits increasing returns of scale. As long as the company continues to execute on their playbook of maturing newer territories, it will be hard to compete for new entrants. Existing auction houses can compete, but their relationships with dealerships is different to what ACV has built, which is in effect more sticky. ACV is not likely to capture the entire market but slowly chip away market share from auction houses like Manheim who took to long to digitise their operations.

Thanks to Julia and Jack Greco (cofounder at ACV) for the feedback! Thanks for reading! See you next week for another issue! 👋

| A guest post by

|