🗺 Y Combinator - Summer Batch 2020

Overlooked #33

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing insights on the last Y-Combinator batch.

Last week, Y-Combinator did the Demo Day of its summer 2020 batch. For the first time, it was a fully remote program. I love to spend time looking at the companies in the batch because it gives you a good pulse of where tech is heading.

In this article, I will share insights on trends and interesting startups that participated into the batch. I also did this exercise for the previous batch here.

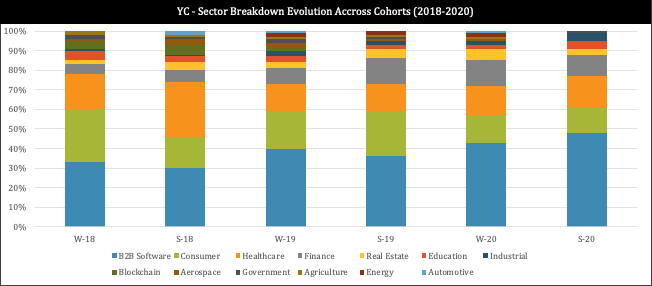

General Data

c. 28k investors intros have been done through the YC platform for 197 companies in the batch - implying an average of 140 intros per company. YC has never been as efficient in its fundraising machine role for its companies.

36% of YC companies were not based in the US before joining the program which is in line with previous batches

Looking at the sector breakdown evolution (I used YC breakdown) across cohorts: finance and B2B software are trending up while consumer and blockchain are going down.

I also manually tagged all the startups in the batch based on their activity, their pitch during the Demo Day and press articles. My tags are a mix of sectors, business model, trends. It's not exhaustive but it gives a good idea on certain trends. For instance, you see that the developer tools is a huge category and entrepreneurs are building products around key themes like APIs, artificial intelligence, data management, databases and open source.

A Covid-related Batch

Building on the above graph, you understand pretty quickly that most projects are in sectors boosted by the covid-crisis:

Healthcare: remote-health (telemedicine, process digitalization, wearables), covid-relation solutions, wellbeing.

Education: homeschooling, educational video content for kids, income-share-agreements, personalized teaching.

eCommerce (cf. infra)

Food: fast convenience delivery, local groceries delivery, alternative meat, pre-prepared meal kits, tooling for restaurants.

Logistics: building the infrastructure layer to power eCommerce (e.g. same day delivery to compete with Amazon Prime) and food innovations driven by micro warehouses, data and automation.

Video: Zoom unbundling with full stack approaches on a specific vertical (teaching, conferences, sports), replicating real social interactions through video as a channel, collaboration through video

Passion economy: many creators have lost a in-person revenue line in their business with covid and solutions are rising to help them create / boost a digital revenue line (cooks, fitness instructors, influencers, etc.)

eCommerce Revival - Building Around Shopify

With covid, eCommerce penetration rates have exploded around the world. Companies building pick and shovels for merchants have experienced a strong growth in the past few months. This growth has also attracted a new wave of entrepreneurs and projects.

Ben Evans on Ecommerce penetration rate evolution

It's anything but surprising to see that Shopify was the most quoted tech company by entrepreneurs during the Demo Day. If you take a step back, these companies can be classified into four categories:

Companies building products for merchants using Shopify and more broadly for e-commerce companies. These companies are following the "arm the rebels" Shopify narrative: give independent merchants superpowers to compete with Amazon.

Companies building Shopify equivalents in geographies in which Shopify is less relevant - like Bikayi building a version dedicated to the Indian market.

Companies replicating this core Shopify's idea of having a single platform enabling small independent businesses to monetize their online activities. Sometimes, it makes sense. Other times, the comparison is farfetched. For instance, Epihub presents itself as the "Shopify for anyone teaching online". It's a digital hub that enables teacher to schedule classes, to run them, offers a library of resources for students as well as a payment system to charge students.

Companies with a business model in which you add a fintech product on top of a SaaS dedicated to small businesses. This category is worth mentioning but I believe that YC companies are a bit too early to pitch this dual business model to investors. Bill.com has a business model like this. Carta will end up having a similar business model.

Most companies in the batch were in the first category. Here is my top five:

Jika (US): it's a tool to automatically set up, run and track A/B tests within a Shopify website.

Hypothenuse (Singapore): it's a product to generate text automatically for e-commerce websites such as product description, marketing messages, social media posts, blog posts etc.

Depict.ai (Sweden): it's a product recommendation engine which is not based on transactional data (because most merchants don't have enough data to do this) but on product images and descriptions.

Once (France): the company pivoted from a tool to build stories to a tool to build mobile-optimized storefronts for ecommerce merchants.

Photoroom (France): it's mobile app to remove background and customize product photos. The vision is to build the Photoshop for mobile but it's widely used by merchants in the e-commerce sector.

When looking at these companies, I believe that it's key to assess (i) platform dependance as well as (ii) whether the product is a nice to have or a must have.

Verticalized productivity SaaS - Giving superpowers to a key function within a company

Productivity tools are rising everywhere. Notion (horizontal and collaborative note taking app, $2.0bn valuation), Gong (AI-tool to increase the productivity of sales and customer support that is now becoming a CRM, $2.2bn valuation) and Figma (collaborative web based design tool, $2.0bn valuation) have already topped unicorn valuations. Other younger tools like Superhuman (email productivity tool) and Roam Research (horizontal note taking tool) are the darlings of both users building cults around the product and investors. Both are paving the way for a new generation of productivity tools.

In the YC batch, here are my favorite productivity tools:

Matter: an app to be much more productive while reading. You access to content from several sources and in several formats (web, newsletters, books). There is nothing on the market to aggregate all the content in a single space, read it efficiently and export it smoothly to a note-taking app. The most advanced people I know are using a combination of tools and connectors to make it happen. It's not simple and most of the time you have to pay for 3-4 different tools to make the magic happens. Matter is trying to tackle part of these issues starting by aggregating content in a single place (saving long tweets and newsletters).

Clover: a note-taking tool dedicated to creative people. It has a Roam-like approach to note taking using the idea that current tools are not perfect to mimic our brains. Clover offers two views (a writing mode and thinking mode) and is going after the designers niche instead of a horizontal target.

Omni: AI tool to power sales and customer support teams by giving them suggestions from the company knowledge base and best practices during their real time interactions with customers.

Opvia: "Airtable for scientists" to address their specific pain points (spreadsheets everywhere, old dated data management tools, no collaboration, no-quick analytics etc.)

When you take a step back, building a productivity tool super focused on a key function (scientists, sales, customer support, designers etc.) or on a usage (reading, mailing, editing videos) seems to be a recurring theme. You need to constrain yourself to find the right fit in terms of market and build a product that will be better than existing solutions on the markets. Expansion beyond this initial focus should come only after, as Gong.io is now moving to build a CRM on top of its productivity tool.

Education - Bringing the ISA-innovation to the world

Education was put under the spotlight in this YC-batch. The current covid crisis is showing the limitations of our current education systems which are lagging behind in terms of innovation, are not digitized and not remote friendly.

In my opinion, the most interesting innovations are new organizations providing education based on alternative principles: customized learning, remote and digital friendly, incentives alignment, small communities etc.

For instance, Ilk is building a child care organization based on small pods of 2-5 families who will share child care in their homes. Parents, teachers and nannies take care of the kids. Using small pods is a great way to share costs but also to give a more personalized care to kids and to build small supportive communities.

Ilk’s Home Page

Organizations based on income share agreements like Strive School (Europe) and Henry (South America) is another good example. Lambda School made this financial scheme more mainstream/sexy in the US and now companies are trying to replicate and tweak the model to apply it to other geographies.

In this model, you realign incentives between students and their school. Students don't have to pay expensive upfront fees to join the school. Instead, they will pay the school a fraction of their future salary for a certain period of time. If a student does not find a job, he does not have to pay back the school. Incentives are aligned because the school will do its best to maximize the "exit" of its students. If you want to learn more on income share agreements, I wrote a previous issue on the topic here.

Looking more closely at Strive School, you can get a sense of what it really means to replicate and tweak the Lambda School model (computer science university degrees + ISA financing model + digital first school) in other geographies.

Europe is a fragmented continent. Each country has a different education system and regulation. It will take time to scale in several European countries because you will have to adapt to national specificities.

Overall, European education is less expensive than in the US and is almost free in many countries. Obviously, covering living costs must be factored in the equation making the need to have alternative financing solutions still relevant.

Exit salaries are also lower reducing the revenue potential to cover your costs. It's going to be harder to make the unit economics work.

Is there a mismatch in the job market between the skills required by employers and the skills you learn in school? Like OpenClassrooms, StriveSchool will have to bridge this gap by building a curriculum adapted to the need of potential employers. In Europe, those employers may have different needs than in the US.

That’s it for today! Thanks Julia for the feedback! 🦒

Feel free to send me any feedback on this issue or on this newsletter at ade@idinvest.com. If you find this issue interesting do not hesitate to share it with your friends.

See you next week! 👋