🎧 Warner Music IPO - The Streaming Renaissance

Overlooked #24

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m discussing the Warner Music IPO and the music label business.

I found music labels fascinating. Partly because music labels and venture capital funds have similarities.

Both are looking to find the next rising stars, lock them up into long-lasting marriage contract and share the benefits along the journey.

Both are blockbuster businesses: you sign 10 artists, you invest in 10 companies and you make your returns on only 1-2 investments.

Both are challenged. You have bootstrapped startups that refuse to raise money from venture capital funds and you have artists going independent rising to a global fame without labels. PNL is the Zapier of the music industry. No need to work with a music label to be invited to Coachella. No need to raise more than $3m to reach $50m in Annual Recurring Revenues.

Last week, Warner Music made a comeback to the stock exchange raising $1.9bn at an initial $12.8bn equity valuation. With Universal and Sony, Warner is part of the oligopoly that has been controlling the music label industry for decades. In this paper, we will take the IPO as an excuse to dig into the music business and think about the future of music labels.

The streaming renaissance

It's hard to find a better illustration to demonstrate the impact technology could have on a certain industry and the idea of creative destruction inherent to capitalism.

Music industry was declining sharply with the rise of piracy concomitant with the decline of physical sales. In the first place, digitalisation seemed to have an harsh impact on the industry,

In 2011, streaming started to grow slowly thanks to the rise of Spotify and other streaming players allowing the whole music industry to reach an inflection point in 2014,

Since then the industry has been growing again at an healthy 4.1% CAGR mainly driven by streaming (36.8% CAGR) which was the digital innovation brought to the music industry,

Music streaming growth is starting to slow down from a 67.9% growth peak in 2016 to 23.9% growth in 2019 - justifying Spotify's active strategy to reduce its dependency to music streaming.

The music label business is an oligopoly

The music recording and publishing market is an oligopoly dominated by the three majors (Universal, Sony and Warner) capturing c.70% of the market. Independent labels account for 30% of the market. Those three majors are competing to attract and retain the top worldwide artists and are an agglomeration of labels from everywhere in the world.

Labels have two main activities: music recording and music publishing

Music recording is a business in which you will discover and develop the career of recording artists. The goal is (i) to discover and sign the next generation of artists, (ii) to match these artists with the right people to work on music projects (master recordings), (iii) to promote their projects once they are released, (iv) to maximise the use of these projects beyond the initial release. You will earn royalties when master recordings are sold or consumed. In 2015, it was a $23.8bn market expected to grow at 15.8% CAGR until 2030 to reach $56.3bn.

Music publishing is an IP business focusing on generating revenues from the use of a musical composition. You will earn royalties when the musical composition is used via a master recording or elsewhere (retail consumption, TV, radio, series, advertising, live performance etc.) In 2015, it was a $5.4bn market expected to grow at 11.5% CAGR until 2030 to reach $9.3bn.

What is Access Industries (Warner Music’s owner)?

Access Industries is Leonard Blavatnik's business holding founded in 1986. Access invests with a long term horizon in seven categories ($20bn AUM):

Media and telecommunications: Warner Music (music label), Deezer (music streaming), AI Film (film financing and production), Amedia (film and TV studio), DAZN (sports streaming video), Ice Group (internet and telco in the Nordics),

Natural resources and chemicals: Calpine (energy company), Clal Industries (industrial investment group), Lyondellbasell (chemical company),

VC and technology ($2bn AUM focused on pre-IPO investments): Adyen, Alibaba, Amazon, Ant Financial, Facebook, Chime, Lazada, Spotify, Square, Snap, Open Door, Rocket Internet, Yelp, Zalando, Pinduoduo, Zynga, Digital Ocean,

Real estate with luxury hotels and housing properties (Faena Group in Miami, Grand Hotel du Cap Ferrat in France, The Ocean Club in The Bahamas, Sunset Tower Hotel in Hollywood),

Entertainment: cofinancing movies with Warner Bross (Godzilla, Mad Max, Ready Player One, It, Wonder Woman), the Theatre Royal Haymarket in London, investment in live theatrical production in London and Broadway,

Biotechnology: PassageBui, Dicerna, Eliem Therapeutics, Pandion Therapeutics, Day One Biopharmaceutiacals,

Invest in private equity funds with an endowment-style approach.

Leonard Blavatnik is the perfect illustration of the American dream. Born in the Soviet Union in 1957 in the middle of the Cold War, he left its home country to go to the US in 1978 and complete a computer science degree at Columbia. He became US citizen in 1984 and built his fortune during the fall of communism by acquiring privatized companies in the oil and industrial sector. Since then, he has shifted his investment scope towards real estate, entertainment and technology.

Warner Music History

1958: foundation of the company to support the music production of the film studio Warner Bros

2004: Time Warner sold Warner Music Group a group of investors led by Edgar Bronfman Jr. for $2.6bn to deleverage its balance sheet

2005: 1st IPO

2011: Access Industries is taking the company private for for $3.3bn

2013: facing antitrust issues following the acquisition of EMI by UMG, UMG sold certain EMI divisions to Warner for $765m (Parlophone, EMI Classics)

2018: Uproxx acquisition (an entertainment and pop culture website) and EMP Merchandising acquisition from Sycamore Partners ($180m deal)

2020: second IPO valuing the company at $12.8bn in equity value

Warner Music performance overview

At the end of last week, Warner Music traded at a $18bn enterprise valuation implying a 33.7x EV/EBITDA (trailing 12m) multiple to be compared with the 27x multiple paid by Tencent to acquire a 10% stake in Universal from Vivendi at the beginning of the year.

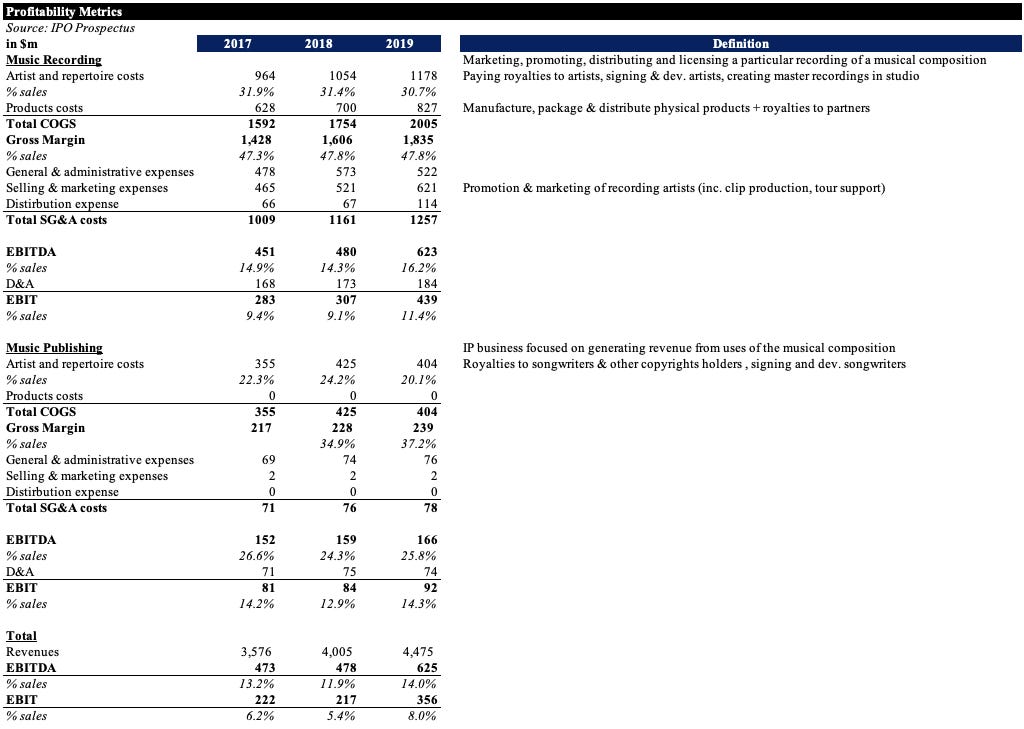

Looking at the past 3 years revenue metrics, Warner is following the main trends in the musical label industry: (i) double digit growth in the past two years to reach $4,475m in sales (86% recording & 14% publishing), (i) digital sales are driven revenue growth and (ii) physical sales are decreasing. It seems that Warner’s market in the recording segment has increased from 16.8% in 2015 to 18.1% in 2019.

Looking at the past 3 years profitability metrics, Warner has a 14.0% EBITDA margin (vs. 13.2% in 2017 and 15.7% EBITDA margin for UMG in 2019). Publishing is a smaller segment but with an higher EBITDA margin (16.2% vs. 25.8%) mainly due to the absence of product costs compared with the recorded music segment.

What's Warner pitch to promote the IPO?

Music is booming. Global consumer listen to 18h of music per week on average and the market is driven by strong growth factors:

Increasing music consumption on mobile,

Younger demographics listening to more music,

Device innovation (smart speakers increasing at a 38% CAGR to reach 440m global devices in 2023),

Format innovation (TikTok: changing the path to stardom and offering a new revenue stream for music labels).

Streaming is the main music boom’s growth driver (54% of the 35-64 y.o. have used a music streaming service in the past month in 2019 vs. 46% in 2018) but we are still in the early days. There is room for global adoption, higher penetration, and there are opportunities to improve streaming pricing.

Only 8% of smartphone holders worldwide are paying streaming subscribers (255m people in 2018 vs. 176m in 2017 vs. 3.2bn smartphone holders)

The countries with the highest streaming penetration are proving that there is a strong room for growth: in Sweden, 30% of the population is paying for streaming, in the US, 25% and in Japan 16%

Warner is well placed to benefit from the music boom thanks to its competitive advantages:

Good positioning in emerging geographies,

Diversified portfolio and dominant positioning in the top 3 worldwide labels,

Strong ability to identify and nurture music artists all around the world,

Capabilities to make strategic acquisitions: 15 acquisitions under Access ownership.

Looking at the financial performance and the IPO pitch, I’m skeptical on this pitch and the level of valuation. I get the point that Warner Music is a unique trophy asset giving public investors a unique exposition to the music label business. But I’m struggling to see the true differentiations with the two other majors that have higher market shares and Music Warner has not an appealing strategy to thrive in the music industry that is turned upside down (by streaming and the decreasing barriers to entry to become an artist). Moreover, Warner Music is not over-performing UMG in terms of profitability and business growth. Access Industries is the clear winner in this IPO being able to realize the value of an asset bought during depressing times for the music industry. I’m eager to see how the business will evolve in the coming years.

Why an IPO now?

Access wanted to realize part of the value generated in its investment in Warner Music. The label is not raising capital but selling existing Access shares to third party. Access is cashing out $1.9bn (13.7%) for an asset bought at $3.3bn while maintaining a controlling stake in the company.

We are at the acme of music streaming for music labels. Music streaming growth and labels' balance of power with artists will both decrease in the coming years.

Covid is bringing uncertainty to the music industry. Most music concerts for 2020 have been cancelled and uncertainty remains on the state of the live entertainment market for 2021. Moreover, artists have been also struggling to record their new albums. An IPO today is a way to sell a stake before these potential downsides are materialized in Warner Music sales and profitability.

Music players have a strong momentum in terms of valuation. Vivendi was able to sell a 10% stake into Universal Music to Tencent for $3.4bn (with an option to acquire another 10% stake at the same price before Jan. 2021 and Vivendi is planning to list UMG before 2023) at the beginning year and Spotify is outperforming the stock market.

The back catalogue is more important in the music industry compared to the video industry providing music labels a better balance of power with streaming services compared with film producers. People watch movies or series only once. People listen music tracks dozen of times per year. A music streaming service without the depth of historical tracks is not relevant. Even is Spotify started to sign new artists directly bypassing music labels, it will always have to strike deals with music majors to maintain this back catalogue. In the film industry, the back catalogue is less important. You don't need to have a universal coverage of all the movies and series released. Having a regularly updated catalogue is sufficient to keep users paying for the services.

Artists are pressuring music labels revenues on both ends. On the one hand, top worldwide artists have bargaining power to renegotiate with much more favorable conditions their contract with majors (Taylor Swift). They don't hesitate to renegotiate, to become independent or to sign with a competing labels. On the other hand, emerging artists are getting more reluctant to sign with labels and are setting their own structure to remain independent (Angèle and PNL in France).

Music is increasingly a diversified D2C business. The barrier to record, publish and promote music tracks has never been as low as it is today. As a result, music label value added is being questioned by artists. Artists understand that they can go direct to their fans without the need of a third party. Moreover, music artists revenues are increasingly diversified. New revenue streams make them much less dependent on their royalties: selling merchandising through a e-commerce website, organizing virtual concerts in video games, making videos for their fans on Cameo etc.

Music is mainly a national phenomenon... but sometimes it becomes a global phenomenon. In the future, music labels will be mainly used to capture this international upside. Louis Fonsi and Aya Nakamura are artists that were able to reach an international audience easily thanks to their music label which have the international footprint an artist cannot have with just an independent structure. Most artists will have a direct to consumer independent approach and will resort on labels only to get this incremental international reach.

🗞 Music Revenue to Drop 25% in 2020, but Long-Term Outlook Is Good: Goldman-Sachs (Variety, May 2020)

🗞 Where the Music Business Is Going in 2020 (Rolling Stone, Jan. 2020)

🔎 Music is in the Air Reports (Goldman Sachs, Oct. 2016)

🔎 IPO Prospectus (Warner, Feb. 2020)

🎧 Daniel Ek: The Future of Audio (Invest Like the Best, Nov. 2019)

Thanks to Julia for the feedbacks! 🦒

Thanks for reading! See you next week for another issue! 👋