🗞 Venture Chronicles - November 2021

Overlooked #94

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of November.

For 2021, I wanted to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for November!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Monday, Nov. 1st: Protocol wrote a great portrait of asynchronous video messaging platform Loom. - Protocol

Loom is successful because it reduces the friction to create, share and consume videos.

Founders started to work together in 2015. After testing several ideas, they launched a Chrome extension on Product Hunt in June 2016 to record simultaneously a video of your screen and your face to share with third parties through a simple link.

"Loom's most audacious idea is that asynchronous video offers a new type of communication that deserves its place in everyone's lives. Synchronous video (Zoom and FaceTime), synchronous text (Slack and Teams) and asynchronous text (email) already exist. But there's no way to communicate with the kind of fidelity that video allows without either hosting a meeting or jumping through a lot of hoops and apps."

Loom is now expanding to be both a platform (organize your library of Looms to become a system of record) and an infrastructure (use the Loom SDK in any app that wants a simple video recording feature).

Tuesday, Nov. 2nd: Klarna acquired Swedish price comparison site Pricerunner for €930m to add a key pillar towards its vision to become the one-stop-shop shopping platform. - Sifted, Klarna

Pricerunner has 18m MAUs in the Nordic and in the UK. It compares 3.4m products from 22.5k retailers in 25 countries. It generated €46m in revenues with a 52% EBITDA margin in the past 12 months.

Pricerunner will bring key features to augment Klarna’s consumer app experience: customer reviews, product discovery and price comparison.

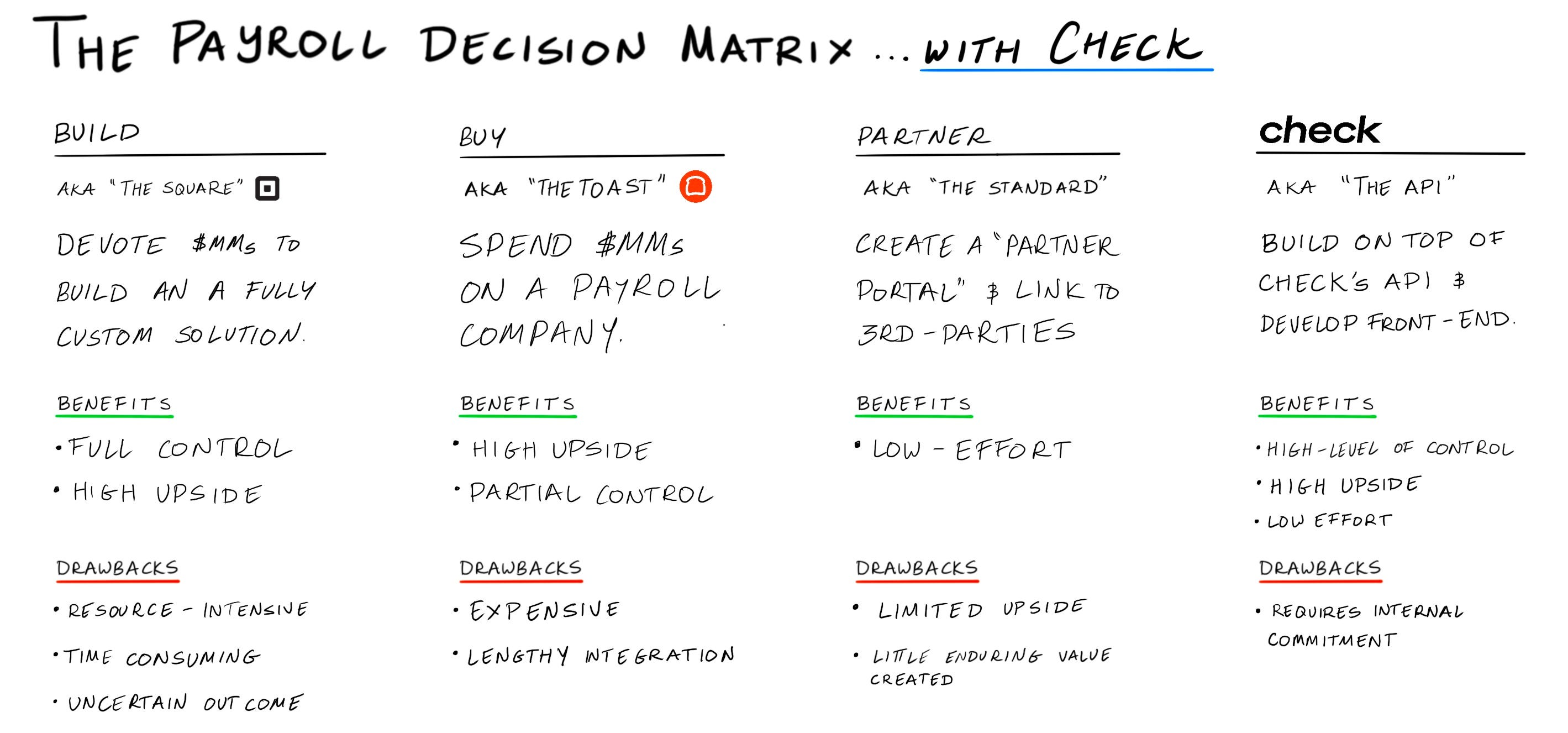

Wednesday, Nov. 3rd: The Generalist published a deep-dive on Check which is a payroll API that lets 3rd party software embed payroll in their solutions (US-based, founded in 2019, $44m raised with Thrive, Index, Bedrock and Stripe). - The Generalist

It's hard to build a payroll system because payroll is extremely technical and local (rules per country and per States in the US).

Before Check, you had 3 options to integrate payroll into your software: build a payroll engine internally, buy a payroll company or partner with payroll 3rd parties. With Check, you can embed payroll in your product with low efforts and a low upfront price.

Check's payroll engine is based on 3 key pillars: (i) tax calculations (employers and employees taxes), (ii) salary payments and (iii) tax filings.

Thursday, Nov. 4th: Cloudbeds raised a $150m series D round from Softbank Vision Fund 2. It's a company founded in 2012 in the US which is selling an all-in-one hospitality management software to the long tail of small hotels and vacation rentals combining operations, revenue and marketing features. Cloudbeds has 22k customers over the world. It will use the funding to grow its team, invest in R&D and invest in content marketing. - Techcrunch

Friday, Nov. 5th: I listened to an Invest Like the Best's podcast episode with Zack Fuss on the food industry. - Invest Like the Best

You can break down the food industry value chain: large producers, wholesalers to processors, processors, wholesalers to distributors, distributors (restaurants, grocers).

Restaurants are historically hard businesses with 10-15% EBIT margin if you are a strong operator (25-30% food costs, 25-30% labor costs, 10% rent costs). It's hard to make the unit economics work when you outsource lead generation & delivery to a 3rd party like DoorDash or UberEats which want to capture 20-30% of your sales.

Henry Ellenbogen at T. Rowe talks about second act to describe the "management's ability to innovate in such a way where they can capture whatever technological innovation or disruption is facing their industry, leverage that to become a more successful, more dominant player".

The grocery market in the US is a $1.8tn market with a breakdown between food consumed at home (45% before pandemic and 55% now) and food consumer away from home (55% before pandemic and 45% now).

With a dark store, "you lower your rent costs and you use the savings from those rent costs to fund other value-added services" which are the costs of packing and delivery. As a result, you have a different shopping experience in which consumers no longer need to go to a physical store and can just order items in a couple of minutes.

Domino's Pizza does $15bn in sales (50% in the US) in 17k locations (6k in the US). There are 3 businesses within Domino's: (i) a restaurant with a delivery arm, (ii) a supply chain business and (iii) a brand manager / franchisor. Domino's franchise unit economics are great. It costs $250-350k to open a store. An average store does $1.1-1.2m in sales and $125k in cash flow. It means that you can payback the restaurant in 2-3 years. Pizza is a great category for a restaurant because it's a low cost of goods cuisine generating 80% gross margin.

Dollar General is the largest US discount retailers after Walmart. It has 17k stores (700m2, 10k SKUs, $2m in annual sales, 6-7 people) and generates $30bn in sales. It focuses on rural areas in cities with 10-20k people and opens 1k stores per year. 75% of Americans live within 5 miles of a Dollar General.

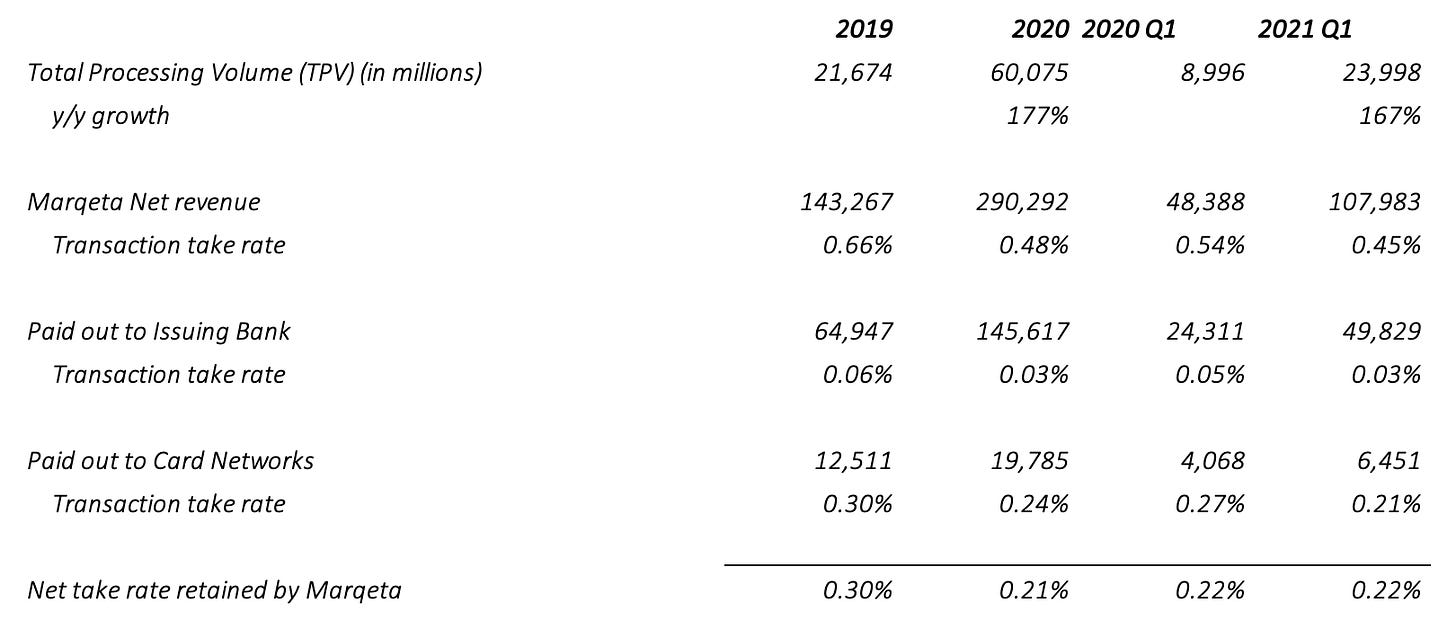

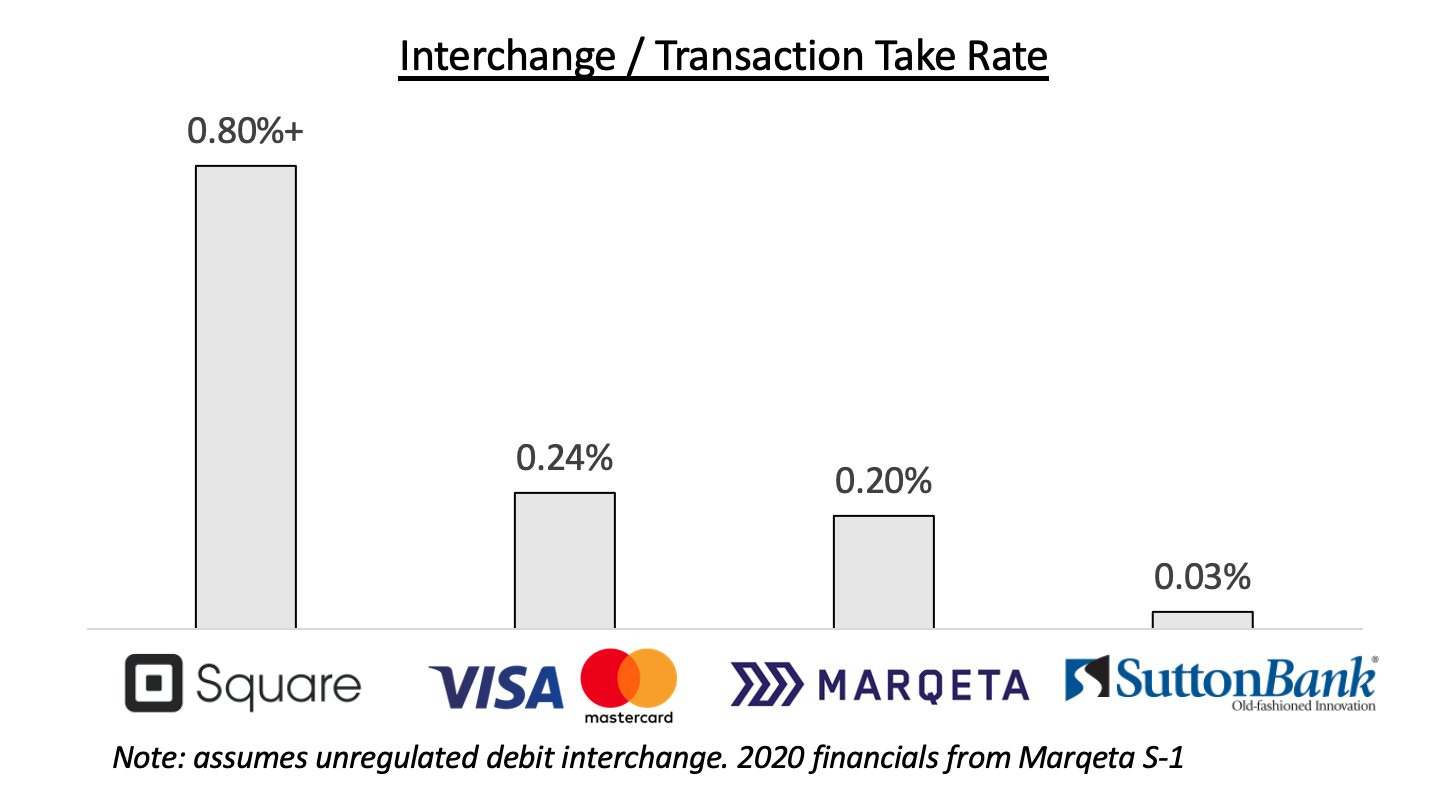

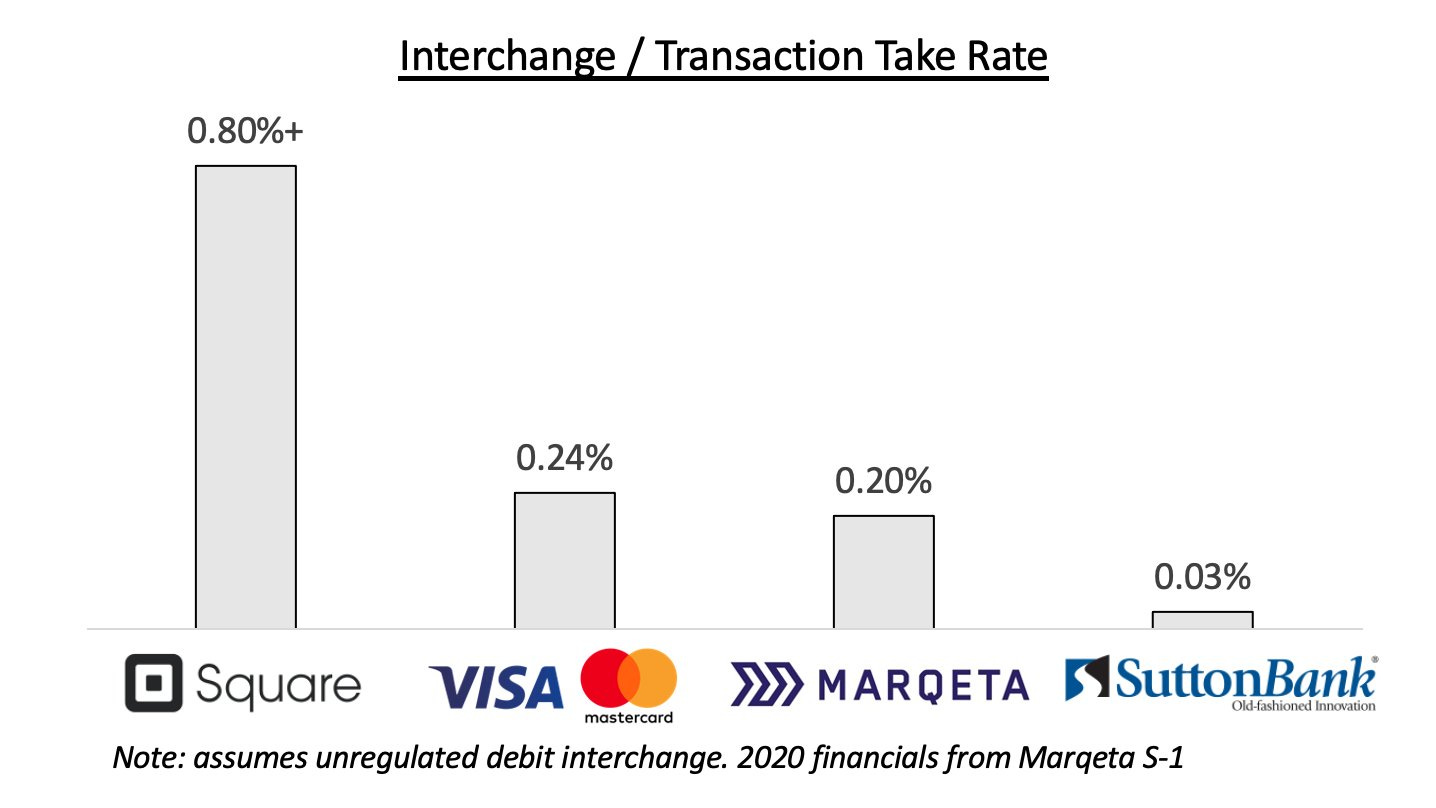

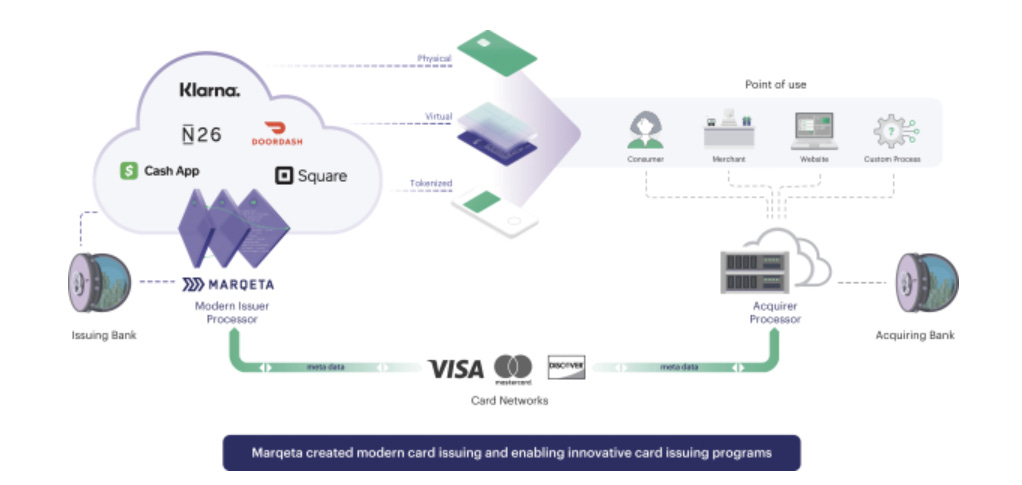

Saturday, Nov. 6th: I read Marqeta's S1 which is a modern card issuer and transaction processor that is cloud-based and API-first. It went public in Jun. 21 and raised $1.2bn at a $18bn valuation. - Marqeta, Tanay's Newsletter

Marqeta works with well-known brands like DoorDash, Affirm, Klarna, Square, Brex, Coinbase or Instacart. It enables businesses to develop modern card experiences for B2B and B2C use cases that can be either core business or adjacent business.

Marqeta's annual revenues grew by 100% in 2020 to $290m with an outstanding 200% net retention rate and 160 customers. Marqeta has 57m active cards and processed 1.6bn transactions in 2020. It has a usage based business model based on volumes processed. It generate revenues mainly from interchange fees from card transactions. In 2020, Marqeta generated 70% of its revenues from Square.

Modern customers are tech-centric companies and want to integrate card issuing seamlessly into their experience. With Marqeta, you have APIs for your developers, you can issue several types of cards (physical, virtual and tokenised) and you can scale your operations globally.

Marqeta has 3 categories of products: (i) issuing to issue cards, (ii) transactions processing and (iii) applications to augment the payment experience (fraud, chargebacks, dev. tools, admin).

Marqeta has customers in several categories: (i) on demand services (DoorDash, Uber, Instacart), (ii) BNPL providers (Affirm, Klarna), (iii) expense management (Brex, Ramp), (iv) digital banks (Square) and financial institutions (Marcus by Goldman Sachs).

Sunday, Nov. 7th: I listened to an Invest Like the Best's podcast episode with Roelof Botha who is a partner at Sequoia. - Invest Like the Best

He explained why Sequoia switched to an evergreen fund structure. The 10-year fund life does not make sense in venture capital because successful startups can create value for several decades. If you are forced to sell too early to give cash back to investors, you are leaving money on the table as asset manager.

Sequoia funds are now gathered under a unique umbrella called the Sequoia Fund. It means that the Sequoia Fund will be the only LP in all Sequoia funds and LPs will invest only in the Sequoia Fund. LPs will now have a capital account in the Sequoia Fund. Any year, they can decide the allocation they want to invest into Sequoia and the breakdown between the different fund strategy. Anytime, there is a payback, the LP can decide to withdraw or reinvest the money (fully or partially) into the Sequoia Fund.

This structure is also removing the 20% limit to invest in other assets than primary issued shares. It means that Sequoia will be able to double down in other instruments like scout funds, crypto investments or secondary investments.

5-10% of the Sequoia Fund will come from Sequoia's investment team (vs. 1-2% for most GPs).

On Roelof's first meetings with entrepreneurs. "Every meeting is both buying and selling, just like every good interview. [...] So there's this delicate balance of how do you ask questions in an engaging way so that you're going to answer some of your diligence questions, but you also build trust. And candidly, I've actually found that that in of itself is valuable. And founders come back to us and say, "You ask the toughest questions, and that's why I want to work with you, because you sharpened my thinking. You helped me think differently about my business. And that's the kind of thinking that I want for the future. [...] So it's being engaged. It's being prepared. I love to understand the eureka moment. What happened? How did lightning strike? How did you think of this problem? What did you encounter in the world? Because I encounter a lot of problems. It doesn't motivate me to start a company. Sloth kicks in. So there's something that happened where you were so frustrated as a founder with the state of the world that it motivated you to want to go and build a company."

Monday, Nov. 8th: Grocery Dive wrote a paper on how Instacart is preparing its second act ahead of its IPO. - Grocery Dive

Instacart wants to become a one-stop-shop tech platform to help retailers digitize their operations - similar to Ocado. Instacart has recently acquired two companies: Foodstorm (white label SaaS covering multi-channel ordering, order management, payment systems and fulfilment) and Caper (smart cart and checkout SaaS - acquired for $350m). In parallel, Instacart is working on solutions to help retailers optimize their fulfilment and delivery/curbside operations with technology and automation.

Instacart wants to double down on building an advertising platform for CPG brands. It recruited two top executives from Facebook: Fidji Simo (ex development and strategy for Facebook app who is now CEO) and Carolyn Everson (VP of global marketing solutions at Facebook who is now president). In May 20, it launched a self service advertising platform.

Tuesday, Nov. 9th: Linktree signed a partnership with Shopify to enable its users to promote their Shopify products directly on their Linktree's page. It keeps adding features to make its Linktree's profiles much more powerful. It previously added direct payments to creators thanks to a partnership with PayPal. - Techcrunch

Wednesday, Nov. 10th: Amenitiz raised a €6.5m seed round led by P9 with the participation of Backed and Otium. It's an all-in-one platform to help independent hoteliers and B&B manage their business (website builder, channel manager, PMS, booking engine). Amenitiz has 3k properties. In Europe, there are 170k independent hotels and 350k B&Bs. It will use the funding to add additional features like revenue management and to pursue its geographical expansion mainly in France, Spain and Italy. - Amenitiz, P9

Thursday, Nov. 11th: DoorDash announced that it was acquiring European multi-category delivery startup Wolt for €7.0bn. - EQT, DoorDash

Wolt operates in 23 countries, has 2.5m MAUs, has a $2.5bn annual GMV run rate in Q3-21 (130% YoY growth) and is present in 15 categories.

It means that DoorDash is now a serious contender in Europe. We should expect the company to double down in Europe on its key strategic priorities (be multicategory, integrate vertically with dark stores and dark kitchens, develop its advertising platform).

Friday, Nov. 12th: Anh-Tho (ex. Qonto, founder at Lago) wrote a post to criticize European VC scout programs claiming that they are not great for founders. - Sifted

When a VC firm invest in your company through a scout, you cannot leverage the brand of the VC firm to boost recruitment and commercialisation.

Moreover, it can create negative signalling effect when the VC fund is not leading the next round of financing. Another issue is that the scout does not have enough skin in the game when he invests in your company because he is not investing his personal capital.

Anh-Tho is mentioning two interesting alternatives: (i) operators who are becoming angel investors, (ii) series A/series B funds investing at seed stage with more flexible terms compared to seed funds (no need to have a 15% ownership at this stage).

Saturday, Nov. 13th: Colossus recorded a podcast on HelloFresh with its CEO & cofounder Dominik Richter. Prep Research, Colossus

HelloFresh is focused on home-cooked dinners. People spend a lot of time and money cooking dinners but the average family cooks the same 7 meals over and over again. HelloFresh allows family to bring diversity to their dinners. Every week, you choose a number of dinners that you want to cook at home across a selection of 30-40 meals and HelloFresh will deliver to your home all the ingredients needed to cook them (30-40 min preparation). HelloFresh has also expanded into ready to eat meals.

In 2020, HelloFresh generated €3.8bn in revenues with a 10% EBITDA margin and 8m active users. In 2021, it will deliver 900m meals (vs. 600m in 2020). The company has 16k employees (12k in logistics & fulfilment roles and 4k in corporate roles) and 25 manufacturing sites.

As of today, HelloFresh has a $50-60 AOV, 35% of sales in COGS, 35% of sales in fulfilment costs. It means that it has a 30% contribution margin. 15% of sales are spent in marketing and 5% in G&A - implying a 10% EBITDA margin. It's a blended number for all geographies which means that HelloFresh will be able to push further its EBITDA margin.

In terms of sourcing, HelloFresh has 300 SKUs to source every week to have 30-40 recipes on the app. It has its own network of suppliers. Some suppliers are on yearly contracts for common items (e.g. pasta). HelloFresh does not hold a large inventory. It has waste ratio under 1% (vs. 30% for the overall industry) because it only orders the items that are needed to prepare the boxes.

"It usually takes consumers between 5 and 10 touch points with a brand to actually make a purchase decision."

Covid has had a massive impact on the business. Instead of eating 50% of their dinners at home, people were forced to eat 100% of them at home. As a result, HelloFresh grew its sales by 120% (vs. 50% growth forecasted).

Sunday, Nov. 14th: I read Weave's S1 which is an all-in-one customer communication & engagement platform for small businesses. - Weave

Consumers are now used to an Amazon-like purchasing & support experience. Weave wants to bring this level of excellence when it comes to communication to SMBs.

Weave started as a vertical SaaS targeting dentists (10% market share in the US) before expanding to other healthcare practices (3% market share in professions like optometry or veterinary) and now being an horizontal solution. It has a "domino growth strategy" to launch a new vertical with a 12-18 month playbook to customize the product and to kickstart the go to market.

Overtime, Weave released additional product features to upsell its customer-base like payments in Apr. 20, analytics in May 20 and forms in May 21.

To manage customer engagement and communication, SMBs tend to rely on solutions that have the following limitations: (i) too complex, (ii) using separate tools that don't communicate, (iii) too expensive, (iv) lack of custom features to the vertical in which they operate.

In 2020, Weave added a payment layer to its platform. It has a $6.0bn annualised GMV as of Sep. 21 - this figure includes also payment not processed by Weave Payments. Weave generated $1.7m in revenues from payments in 2020 (3% of total revenues vs. 1% in 2019).

Monday, Nov. 15th: AllTrails raised a $150m round led by Permira. It’s an app and a web platform for outdoor activities (hikers, bikers, climbers). It has 300k UGC routes, 1m paying subscribers, 40m downloads and 30m registered users. AllTrails has been profitable since 2017. It will use the funding to strengthen the product, to expand internationally and to grow the team.

Tuesday, Nov. 16th: Stytch raised a $90m series B led by Coatue at a $1bn+ valuation with the participation of Benchmark, Thrive and Index. It’s an API-based passwordless authentification platform. It has 4k developers using its solution (vs. 350 in July 21). Stytch will use the funding to expand its product and to grow its team (only 30 FTEs at the moment). - Techcrunch, Not Boring

Wednesday, Nov. 17th: London-based venture firm Balderton raised a $600m generalist fund VIII to invest in European startups at seed and series A stages. - Balderton I, Balderton II, Techcrunch

Balderton has 30+ investment professionals with local teams in the UK, the Nordics, France and Germany.

It supports entrepreneurs on recruiting, marketing, finance and legal with a platform called "Build with Balderton".

In the past couple of years, Balderton broadened its investment scope with a growth fund (2021) and a liquidity fund (2018).

Thursday, Nov. 18th: US-based Grammarly raised a $200m round led by Baillie Gifford and Blackrock at a $13bn valuation. It's an AI-powered writing assistant. It has a freemium model with both a B2C ($30 per month and $144 per year) and a B2B ($25 per month per seat) subscription. Grammarly has 600 FTEs, 30k B2B customers and 30m users. It will use the funding to develop the product and expand the team. - Techcrunch, VentureBeat

Friday, Nov. 19th: Faire raised a $400m series G at a $12.4bn valuation led by Durable Capital, D1 and Dragoneer. Faire is a US-based online wholesale marketplace founded in 2017. It launched 6 months ago in Europe with incredible results: $150m in annualized sales volume and a presence in 15 countries. Globally, Faire connects 40k brands with 300k retailers, generates $1bn in annualized sales volume (3x YoY) and has 700 employees. In Europe and in the US, there are 2m independent retailers generating $2.5tn in revenue. Faire will use the funding to double its headcount in 2022, to expand into new geographies and to build additional tools for both retailers & brands. - FashionUnited, BusinessWire

Saturday, Nov. 20th: Kaavik wrote a paper on play-to-earn NFT blockbuster game Axie Infinity. - Kaavik

Axie's current business model depends on the growth of new users which increases the value of Axie's NFTs and of its in-game token. To become sustainable in the long run, Axie needs to generate revenues in a more recurring way from the current user-base with a mechanism that pleases all the players. Moreover, Axie must become more accessible to non-crypto experts and develop a gameplay that people love to play without being remunerated.

Axie has a D90 retention that is almost identical to its D30 retention. Axie topped 2m in DAUs in Oct. 2021.

Axie started to develop the game in 2017 but it really took-off in 2021 with the NFT craze. The tipping point was when Axie did a technical migration to the Ronin blockchain making it viable to trade in-game NFTs.

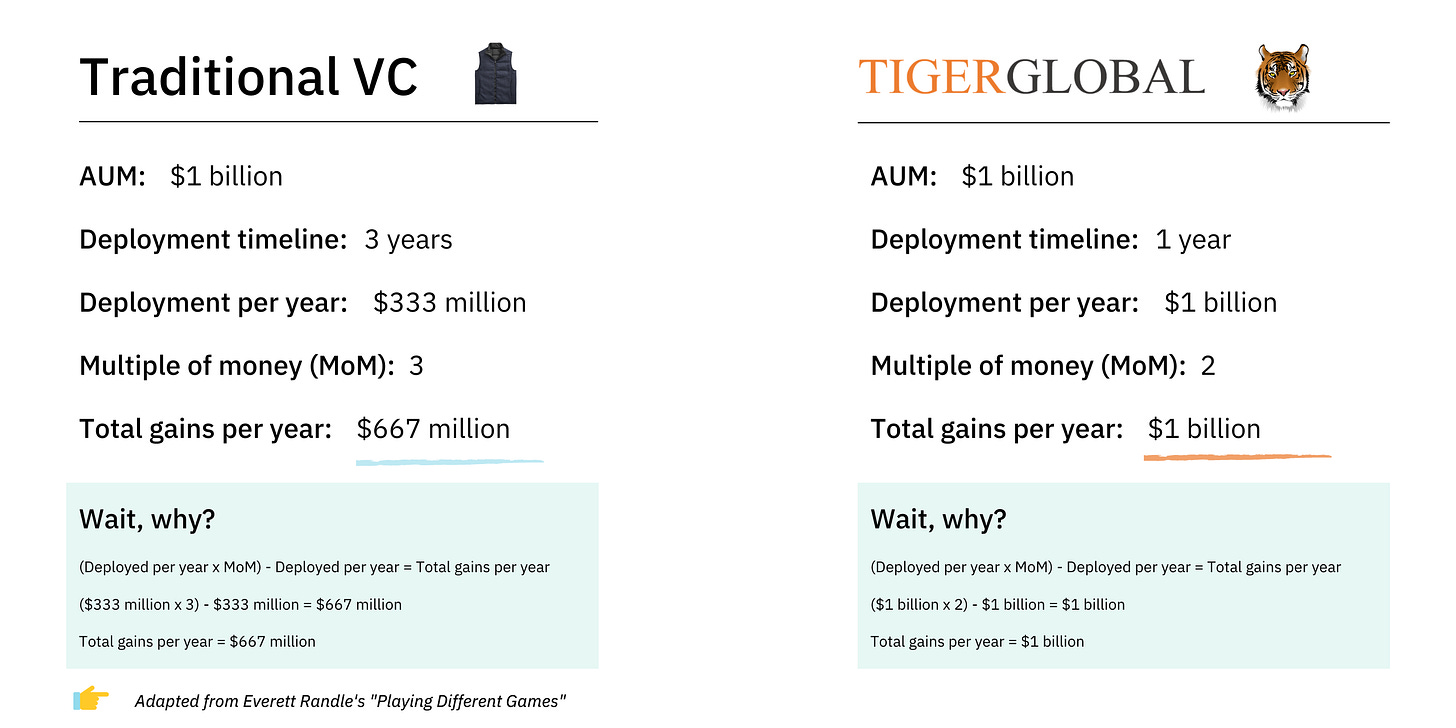

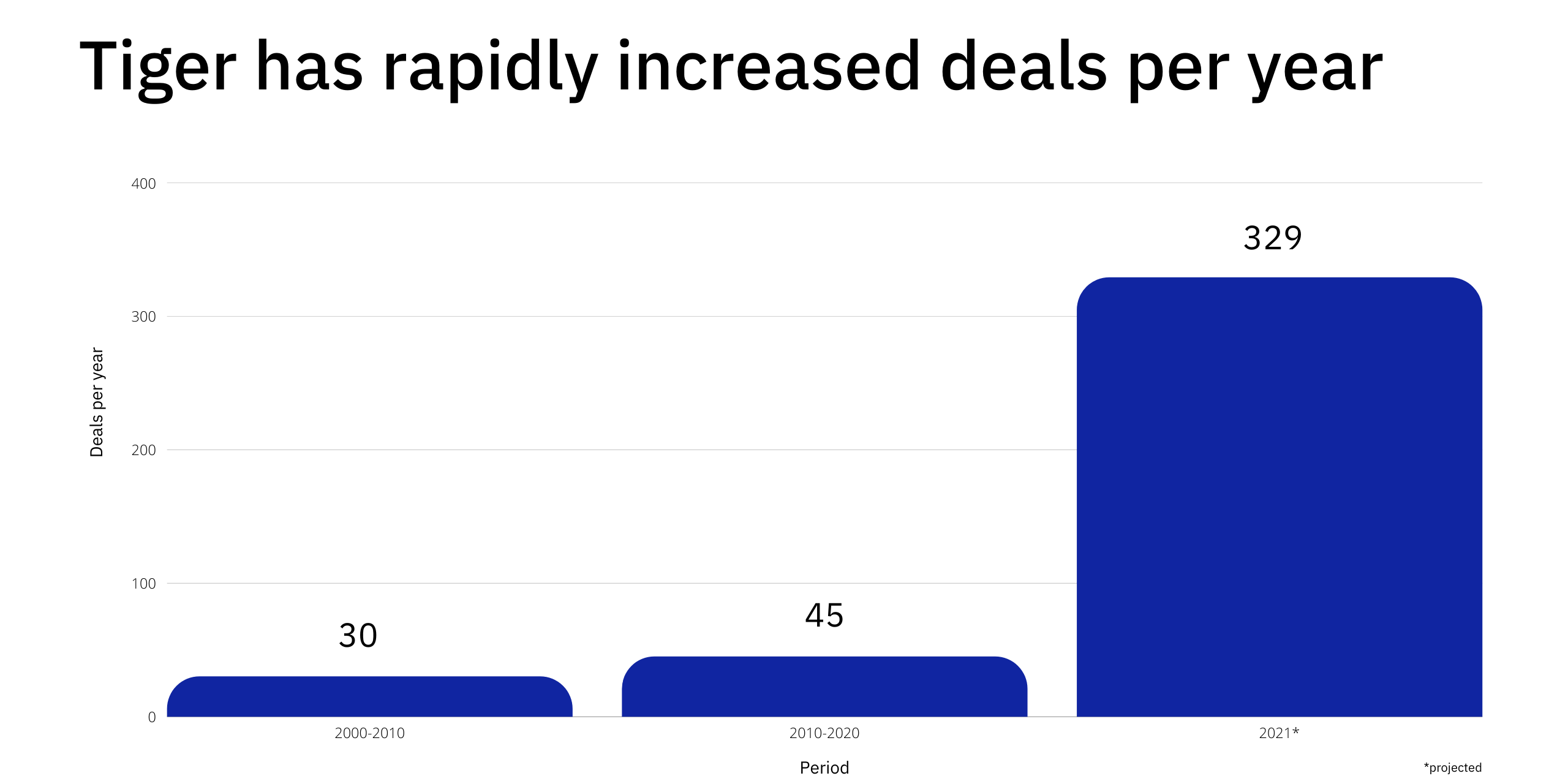

Sunday, Nov. 21th: Mario Gabriele at The Generalist wrote an extensive paper on Tiger Global which is a hedge fund currently disrupting the venture capital industry with rapid capital deployment and targeting a lower return profile. - The Generalist

Tiger Global was started by Chase Coleman who was a former investor at Tiger Management - an extremely successful long-short hedge fund which stopped operating during the dotcom bubble because of the market irrationality of the time.

Coleman introduced 3 changes in the fund's strategy: (i) going global instead of just focusing on the US, (ii) investing in private markets and (iii) indexing the top 10% of an asset class.

Tiger Global's initial success in tech was leading a $5.3m series A into Russian search engine Yandex in 2000. Over the following two decades, Tiger made several impressive bets in venture capital (Facebook, Linkedin, Zynga, Flipkart, Mercado Libre, Mail.ru, etc.) but its deal pace remained reasonable.

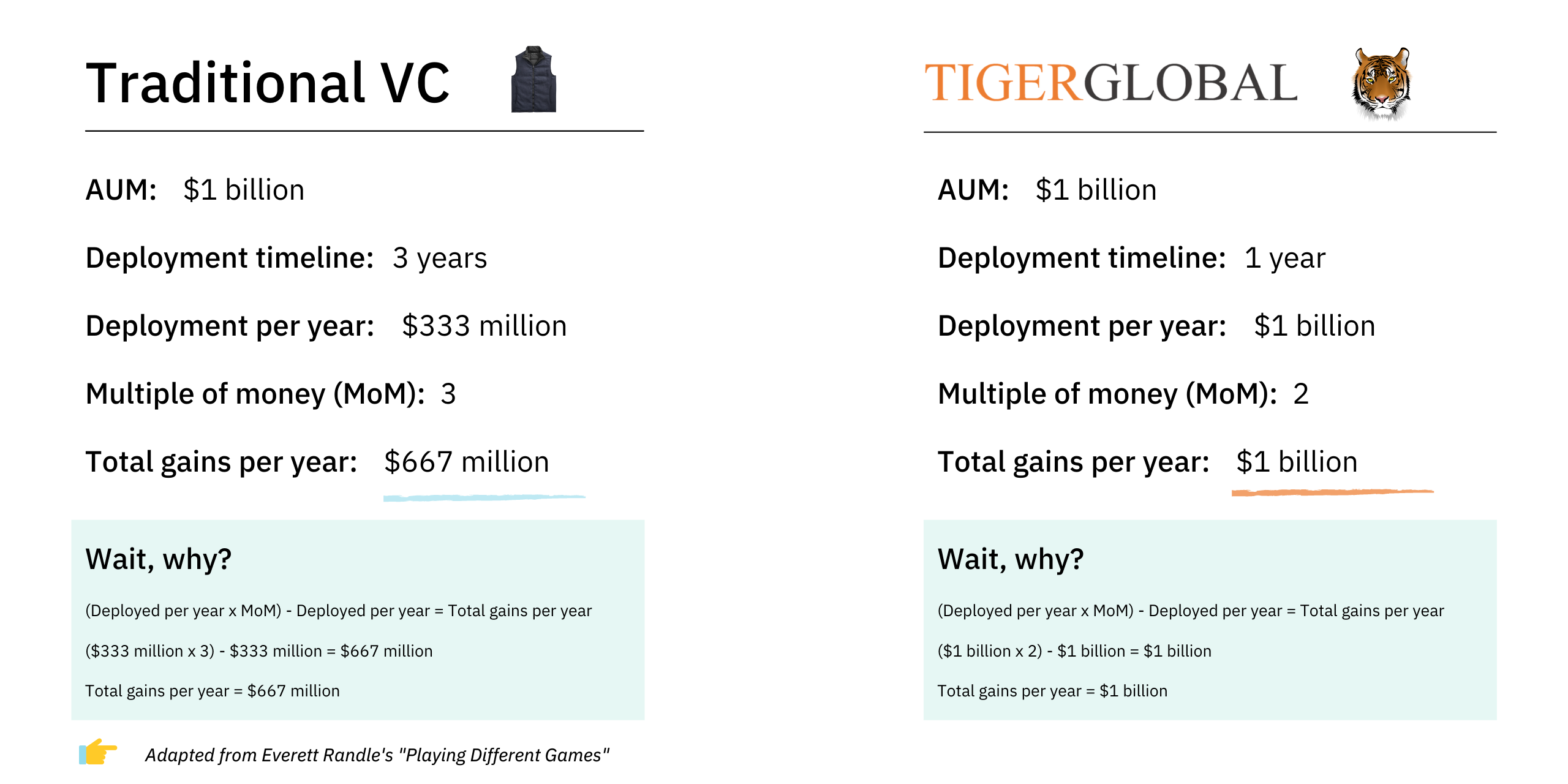

In 2019, Tiger Global revaluated its venture capital investment strategy. It stated that the "value in the software asset class was mispriced". It decided to accelerate capital deployment to be in a position to invest in the top decile of tech startups. In 2021, Tiger is on path to invest in more than 300 startups.

Tiger has a different return profile compared to traditional VC firms. "Classic VCs are often looking to clear a 30% IRR on investments; Tiger is likely hoping for something closer to 20%". Tiger only wants to index the tech industry by building a portfolio with the top 10% startups. From a LP perspective, as Tiger is deploying capital at a faster pace than a traditional fund (1y vs. 3-4y), it can return more capital annually to its investors even with a lower IRR.

To source companies, Tiger combines: (i) a strong inbound thanks to its reputation, (ii) investments as an LP into seed funds, and (iii) market-driven investments (e.g. grocery, democratization of investing).

To win deals, Tiger is ready to move faster and pay higher prices than competitors. As it has a different return profile and Tiger deeply believes that tech is undervalued, it can afford to pay higher prices.

To support companies, Tiger offers (i) Bain consulting services on demand, (ii) Heidrick & Struggles recruiting services on demand and (iii) access to its network.

Monday, Nov. 22nd: Getir acquired another grocery quick commerce competitor called Weezy which operates in the UK. - The Guardian, Sifted, Tech.eu

Weezy was the 1st player to launch in the UK in late 2019 and had raised $21m from investors like DN Capital, Left Lane and Heartcore.

The grocery quick commerce market is being consolidated with category leaders GoPuff and Getir acquiring direct competitors to reduce competitive pressure in the market and to strengthen their positioning.

Tuesday, Nov. 23rd: Yababa raised a $15.5m seed round co-led by Creandum and Project A. It's a German-based grocery delivery startup specialised in ethnic food mostly currently focusing on Arab and Turkish food. It's a company replicating the Weee!'s playbook in Europe following the path of other players like Oja in the UK, HungryPanda in the UK and AlorsFaim in France. It's an interesting category for two main reasons: (i) these players have a unique offering compared to other online grocers, (ii) you can kickstart your business by targeting the community with products they usually buy. Yababa will use the funding to expand the team and to open new cities (in Germany and Europe). - Sifted, Techcrunch

Wednesday, Nov. 24th: BNPL giant Afterpay launched a new product in the US to allow its users to pay their subscriptions (gym memberships, entertainment subscriptions, online services) in installments. BNPL players (Klarna, Affirm and Afterpay) have been all releasing financial products to be able to serve all the payment use cases that consumers may have. - PR Newswire

Thursday, Nov. 25h: Pyxo raised a €7m seed round co-lead by Eurazeo (💙) and Five Seasons to build the infrastructure for reusable food containers! - Techcrunch

Single-use food packaging is an ecological aberration. In 2023, in France, restaurants will have to ban single-use food packaging and instead use re-usable containers. Pyxo is building this infrastructure to make it happen and is already helping 2k restaurants in their transition.

Pyxo is a turn-key solution for restaurants, corporate catering services and grocery stores to start using reusable food containers. Pyxo has built a network of food containers manufacturers, carriers, collection points and cleaning centers. It has also built a container-tracking system (based on NFC chips or QR codes) and a consumer mobile app to help consumers manage the return of their containers. As a result, Pyxo reduces drastically the friction for a point of sale to start using reusable packaging.

Friday, Nov. 26th: Sword Health raised a $163m series D round led by Sapphire Ventures at a $2bn valuation. It's a Portuguese-based startup founded in 2015. It wants to solve musculoskeletal pain with a model combining physical and digital therapies. In 2021, Sword raised 3 funding rounds and has 12x its number of customers. - Tech.eu

Saturday, Nov. 27th: Xange disclosed the financial performance of its different institutional funds. - Xange

Xange 1: €64m raised deployed between 2004 and 2011, 1.6x gross multiple and 1.2x net multiple

Xange 2: €62m raised deployed between 2012 and 2016; 2.2x DPI, 25%+ IRR with a potential to reach a 6x DPI in the next 2-3y.

Xange 3: €92m raised deployed between 2017 and 2021, 0.23x DPI, 19%+ IRR.

Xange 4: €200m currently in the process of being raised).

Sunday, Nov. 28th: I read a paper written by Matt Mochary with key advice to recruit a chief of staff. If you want to learn more about this role, you can also read this post. - Matt Mochary

Background. "The best CoS's are highly organized, excellent communicators (both written and oral), and have broad strategic business knowledge. An environment that almost always ensures these skills is several years at a top management consulting firm (Bain, BCG, and McKinsey). [...] In addition, it is nice if they have 1-2 years of experience in the tech world to be familiar with current productivity tools."

Training. "The key is to give your CoS unfettered access to all the information that you receive. It would be best to have the COS sit beside you from morning till night, with full access to your emails, calls, meetings, etc. By seeing what decisions you make, based on what information you receive, she will soon be able to think like you, and then she can truly be an extension of you (and magic will happen). After several weeks of observing, your CoS can start to take tasks off of your plate. Within several months, she will be able to do all the functions that don't give you energy or that you don't have the capacity to do."

Monday, Nov. 29th: Fred Wilson (GP at USV) wrote a post on the current state of venture capital with seed rounds done at a $100m post money valuation. - Fred Wilson

It does not make sense financially to invest in seed rounds at a $100m post money valuation. If your most performing portfolio company is worth $10bn and you follow a power-law distribution for your investment, it means that you will only generate a 1.3x return (before fees and carried). You need to count on a $100bn exit to make the unit economics work - which most like will never happen.

"I think a strong case can be made for seeds in the low eight figures. If you run that same model with a $20mm post-money value, you get a 6.667x fund before fees and carry. That’s a strong seed fund, probably a tad better than 4x to the LPs, after fees and carry. If you think you can get one of your hundred seed investments to a $10bn outcome, then paying $20mm post-money in seed rounds seems to make a lot of sense."

At seed stage, 50% of investments fail completely and on average, you're diluted by around 2/3 between seed and exit.

Tuesday, Nov. 30th: I read an old interview with LVMH's CEO Bernard Arnault. - HBR

The LVMH process has one objective: star brands. According to Arnault, star brands are born only when a company manages to make products that “speak to the ages” but feel intensely modern. Such products sell fast and furiously, all the while raking in profits. “Mastering the paradox of star brands is very difficult and rare,” Arnault notes dryly, “fortunately.”

"I don’t have alarm bells when it comes to creativity. If you think and act like a typical manager around creative people—with rules, policies, data on customer preferences, and so forth—you will quickly kill their talent. Our whole business is based on giving our artists and designers complete freedom to invent without limits."

"Some companies are very marketing driven; they follow the consumer. And they succeed with that strategy. They go out, they test what people want, and then they make it. But that approach has nothing to do with innovation, which is the ultimate driver, we believe, of growth and profitability. You can’t charge a premium price for giving people what they expect, and you won’t ever have break-out products that way—the kinds of products that people line up around the block for."

"We don’t like failures. We try to avoid them. That is why, with many of our new products, we make a limited number. We do not put the entire company at risk by introducing all new products all the time. In any given year, in fact, only 15% of our business comes from the new; the rest comes from traditional, proven products—the classics."

"I would say that there are four characteristics required [for a star brand]. A star brand is timeless, modern, fast growing, and highly profitable. It is very hard to balance all four characteristics at once—after all, fast growth is often at odds with high profitability—but that is what makes them stars."

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋