🗞 Venture Chronicles - November 2020

Overlooked #48

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful tech news of November.

For 2020, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for November!

Please note that the date picked for each event is not always the exact date of the event but the date I decided to write about the event.

Sunday, Nov. 1st: I listened to a podcast with Stir's CEO, from Li Jin and Nathan Baschez. Stir is a platform that helps creators manage their business. It has recently raised a $4m seed round with Homebrew, Ludlow and XYZ Capital. (Means of Creations)

Stir has a unique brand building and lead generation's strategy built around the concept of drops. The drop marketing model was created in the 80s in the sneaker industry when Adidas and Nike started to release limited edition of their models that were available for sales on a defined day. The date was hyped by the brand and when the stocks were sold, it was done. Stir is using this concept to create products in small quantity that are hyped and that are solving an identified pain point in the creator economy. For instance, they released OnlyTweet (a private Tweet feed behind a paywall) and Presubscribe (a platform to pledge that you will donate funds every month to a creator if he goes independent). The strategy was a game changer for the company to build awareness in the creator economy.

Stir's core product allows creator to have an overview of their business on a unique platform with a dashboard aggregating all revenue sources, a calendar to know when you are going to be paid. But Stir also includes features for collectives of creators that are working together on projects and want to split the revenues generated. I'm super bullish on this notion of creators' collectives which can become the new dominant organisation in the 21st century: you would work in small groups, comprised of independent and complementary workers. You learn from each other. You collaborate together on projects. Being part of a collective will also help people to be independent.

Monday, Nov. 2nd: Nathan Benaich raised $17m for his venture fund called Air Street Capital. It will be dedicated to AI early stage startups in France and in the US. Nathan has a strong expertise in the field: he has a PhD in experimental and computational cancer research, he founded a community around AI, he is publishing a yearly report on AI and did several deals in the space including Mapillary, Tractable, LabGenius and Thought Machine. (Tech.eu)

Tuesday, Nov. 3rd: Under Armour sold MyFitnessPal to a private equity firm called Francisco Partners for $345m - 5y after acquiring the company for $475m. Under Armour is selling the company at a discount claiming that it needs to refocus on the core strategy of the firm. MyFitnessPal had 80m users in 2015 and has now more than 200m users. (Techcrunch)

Wednesday, Nov. 4th: US fast convenience-delivery startup goPuff is acquiring BevMo for $350m from private equity group Towerbrook. It's a physical retailer selling alcohol and which operates 161 stores across three US States. GoPuff will leverage BevMo's customer base to promote its delivery services and will convert certain stores into micro-fullfilments for its delivery operations. It's fascinating to see startups acquiring retailers to expand their businesses and become true hybrid player working on both offline and online channels. (Techcrunch)

Thursday, Nov. 5th: Hummingbird raised $200m across a fourth €40m early stage fund (seed stage with tickets between $500k and $5m) and a second opportunity $140m fund (up to €20m). Humminbirg is one of the best performing fund worldwide: all of its early stage funds are in the top 1% and 3 of their 19 seed investments have generated more than $100m in net profits. Hummingbird has partnered with companies like Deliveroo, Peak, Kraker, Showpad or Brigit. The team is investing all over the world with a special focus on emerging markets. (🇩🇪 Tidj, Hummingbird)

Friday, Nov. 6th: Business Insider is acquiring a majority stake into Morning Brew, valuing the company at $75m. Morning Brew operates four-business focused newsletters distributed to 3m subscribers with an average open rate of 40%. The company has been profitable since 2018 and generates $20m in sales and $6m in profit. It's really a great example of what it's like to build a media company nowadays. (Axios)

Saturday, Nov. 7th: Techcrunch wrote a paper on the rise of B2B marketplaces in the e-commerce space like Mirakl or Faire. Contrary to B2C marketplaces, B2B marketplaces must offer much more that just being a transactional platform. They must work on ancillary services like financing, bulk discount, contractual pricing, logistics, insurance, compliance etc. (Techcrunch)

Sunday, Nov. 8th: I did a deep-dive on Sequoia's history this weekend by (i) listening to AcquiredFM's episodes on the firm, (ii) watching Don Valentine give a speech at Stanford and (iii) reading a long form interview done by Don Valentine with Berkeley's oral history project on the early history of venture capital. It was a super insightful experience that gave me many topics to work on to be a better investor. (AcquiredFM, Stanford, Berkeley). Below are some quotes from Don and learnings that resonated with me:

"In the business I’m in, it’s all about figuring out which questions are the right questions to ask, and since we don’t have a clue what the right answer is we’re very interested in the process by which the entrepreneur gets to the conclusion that he offers." Obviously with a degree in philosophy, I love the idea that investors must be as good as Socrate to ask questions to entrepreneurs.

"The ground rules governing investment selection at Sequoia: must be a very big market; must be in Northern California; must be in advanced technology; must have high gross margin ability; must have the potential for Sequoia to make $100m; must be positively responsive to our active participation" These were the original investment rules at Sequoia. They have changed overtime but some points remain striking: (i) Sequoia invests only in very large markets (more on this below), (ii) despite investing early in the companies, you should understand the unit economics at scale, (iii) entrepreneurs should be willing to be supported by the Sequoia team.

Don is always talking about investing in big markets and about the fact that markets beat entrepreneurs. "In a sense, you can augment management, you can help them with more people that are highly qualified. [...] We invest on the size and dynamics of the market. I don’t care if Genghis Khan is running the company; we’ll give Genghis Khan some help. And give me a giant market—always." I believe that we should also understand that Don loved investing into ecosystems. His first investments were all applications from the semi-conductor innovation (e.g. Apple, Atari, Electronic Arts). Investing in big markets also means that you should identify growing tech ecosystems and deploy capital in several companies that are contributing to its growth. It's what has been called the aircraft carrier strategy.

"This stability is part of why we have had the same limited partners for almost 40 years. Stability and returns is how Sequoia is positioned." Sequoia has also remained a top notch investor overtime because it has perfectly managed several transitions in its partnership.

"I look for people that are as far as possible different than I am, because we do things here on the basis of consent among the partners. And I don’t like having a homogenized set of opinions. I want as much confrontation and different thinking as possible."

Monday, Nov. 9th: Sophia Bendz sat down for a long-form interview with Scandinavian Mind. Sophia has recently joined Cherry Ventures as partner. She previously was at Atomico and was leading marketing at Spotify before joining the investment world. I'm impressed by her journey and I admire what she is standing for: having more women in tech both as entrepreneurs and investors, investing into companies that are making our world a better place, raising the next generation of European angel investors. (Scandinavian Mind)

Tuesday, Nov. 10th: Hopin raised a $125m series B round at a $2bn pre money valuation led by IVP and Tiger Global. The company went from $0m to $20m ARR in just nine months, from 1 person to 215 in under a year, has 50k customers, has been used by 3.5m people and is profitable. It's completely stellar. Hopin has released a discovery platform to let attendees find new events. It will also add 800 new employees in 2021. (Techcrunch)

Wednesday, Nov. 11th: Seedcamp raised £78m for its fifth fund from an interesting mix of investors: institutional LPs (British Patient Capital, OMERS, LGT), venture funds (Northzone, Index, Atomico, Sequoia) and angels (Shakil Khan from Spotify, Daniel Dines from UI Path, David Helgason from Unity). Seedcamp invest into pre-seed and seed companies. Seedcamp has invested into 5 European uniocorns including UiPath, Revolut, Transferwise, Hopin and Wefox. It's impressive how they managed to scale sourcing, picking and support at a truly pan-European scale. (Techcrunch, Sifted)

Thursday, Nov. 12th: We have now three European Thrasio copycats! Thrasio is a US-based company acquiring and optimising D2C brands that mainly sell on Amazon. The company has passed the $1bn valuation threshold earlier this year. Thrasio is acquiring performing brands that are using the "Fulfilment by Amazon" to be distributed on Amazon. Most of the times, these brands are built by independent founders who become overwhelmed by their success and don't have the tools and the knowledge to grow the business internationally. Thrasio provides these founders with an exit and will use its infrastructure and team of experts to bring their business to the next level. The European counterparts are called Heroes ($65m raised in a debt and equity round led by 360 Capital and Fuel Ventures), SellerX (€100m raised in debt and equity with Cherry, Felix, TriplePoint and Village Global) and Razor Group (€25m raised with Redalpine, Rocket and 468 Capital) (Techcrunch, Tech.eu)

Friday, Nov. 13th: Private equity fund Vista Equity is taking a majority stake into Pipedrive valuing the company at $1.5bn. Pipedrive is an Estonian-based self-served CRM specifically targeting SMBs and developed from a salesperson's point of view. The company was founded in 2010 and raised €80m from investors like Bessemer, Insight and Atomico. We see more and more PE funds acquiring tech companies, giving them another exit option beyond M&A with a strategic acquirer and IPO. (SiliconCanals)

Saturday, Nov. 14th: Strava raised a $110m series F led by TCV and Sequoia to add new features to the product and to grow its user base. Strava is a sport activity tracking mobile app and I believe that it is also a vertical social networks for runners and cyclists. The company has 70m users over 195 countries and has added 2m new users per month in 2020. (Techcrunch)

Sunday, Nov. 15th: Habr raised a $38.5m series A co-led by Dawn and Tiger Global. It's a London-based startup founded in 2017 and seeded by Boldstart. Habr is building an online data marketplace. For now, the startup is focused on targeting large data vendor to help them package and monetize their data more efficiently but the end-vision is to enable any business to sell its data as a byproduct. (Techcrunch)

Monday, Nov. 16th: Klaviyo raised a $200m series C led by Accel at a $4bn valuation. It's a marketing automation and customer data platform mainly for ecommerce that is known for having piggybacked Shopify to fuel its growth. The company has 50k customers across 125 countries. Klaviyo will use the funding mainly for product development and to double the team from 500 to 1k employees. (Techcrunch)

Tuesday, Nov. 17th: Autodesk acquired Spacemaker for $240m. Spacemaker is a software for architects, urban designers and real estate developers to help them take better design decision using artificial intelligence. The company had raised a $25m series A in 2019 co-led by Atomico and Northzone. (Techcrunch 1, Techcrunch 2)

Wednesday, Nov. 18th: Yubo raised a $47.5m series C with Idinvest (💙), Iris, Gaia and Alven. It's a youth mobile app to socialize online through direct lives to watch or stream with other people. We wrote a detailed post on the funding that you can find here. Yubo is building a worldwide leader in the social category and will use the funding to grow the team, double down its product development efforts and keep expanding its user base. (Techcrunh)

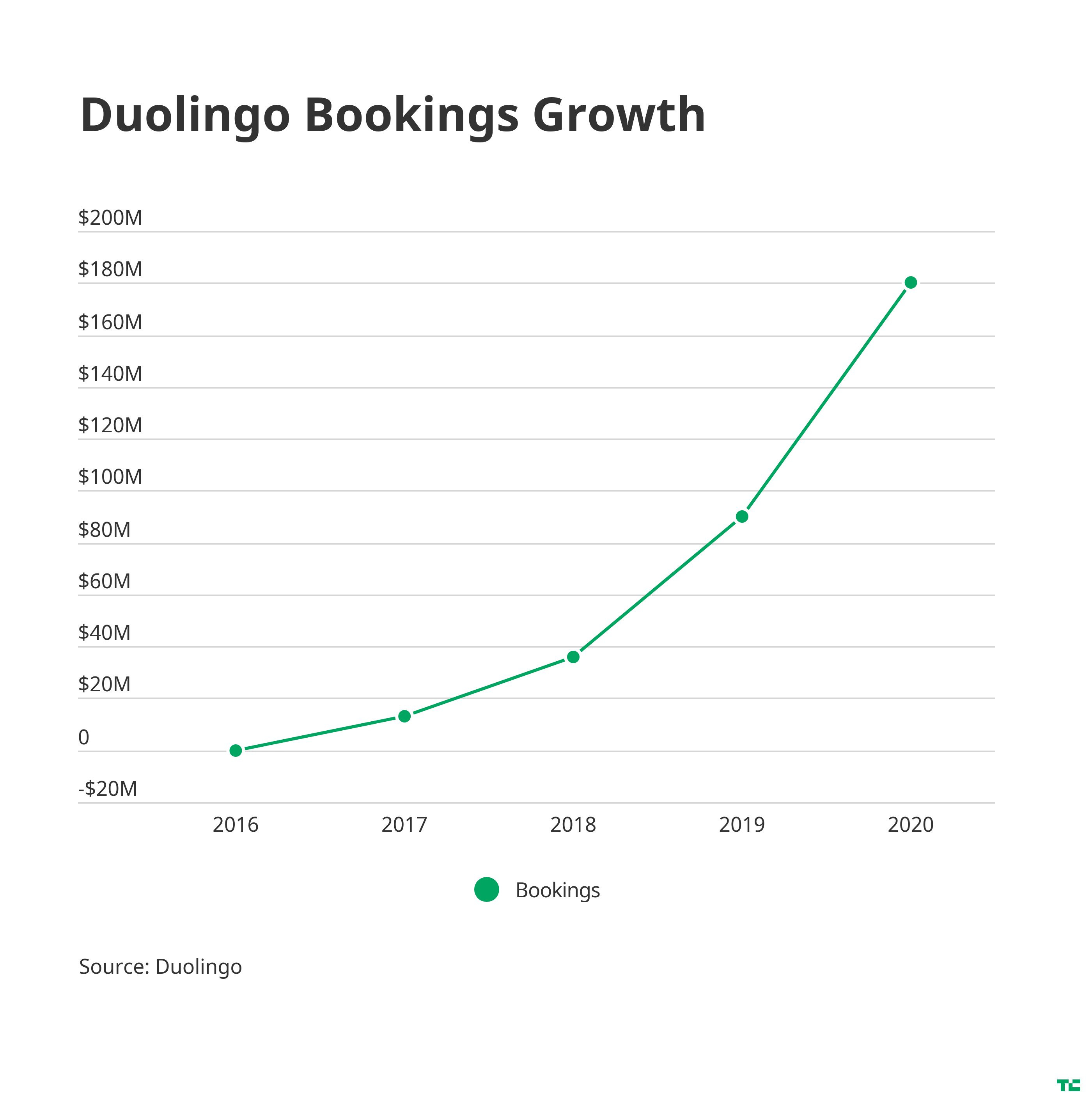

Thursday, Nov. 19th: Duolingo raised $35m at a $2.4bn valuation from Durable Capital and General Atlantic (vs. $1.7bn valuation in April 2020 when General Atlantic put a $10m cheque into the company). The app to learn foreign languages has 42m MAUs, has reached $180m in bookings (vs. $90m in 2019), has a 3% conversion rate between free and paying users and is now profitable. (Techcrunch)

Friday, Nov. 20th: Snap acquired two European startups: (i) Voisey which is a UK based app to create stylish music tracks based on your own vocals and (ii) Voca, an Israeli-based startup making AI-based voice agents for call centers. Snap has been acquiring strong teams and technical abilities to build the next chapters of its product development. It's going to be interesting to see what will be done from these two acquisition in voice capabilities. (Techcruch)

Saturday, Nov. 21st: a16z wrote a paper on adding a top down sales layer to your sales operations for bottom-up and product-led growth startup. You should start adding this layer when the bottom up flywheel is working (reaching $20-30m in ARR and having a strong penetration in individual accounts with several teams using the product) and you have an increased business demand for a top down solution (enterprises pushing you to develop enterprise features). (a16z)

Sunday, Nov. 22nd: Ben Issenmann wrote a paper on tiny products which are products that are built quickly in two weeks, generate income and don't require any maintenance. It's a growing trend amongst digital product builders to launch small projects following this playbook. I love many ideas around this philosophy: (i) you have the necessary tools with no-code to build and ship project in a short timeline, (ii) as you move forward, you are building an expertise and an audience that will compound overtime, (iii) the deadline pushes to be creative without getting stuck into a topic. (Supercreative)

Monday, Nov. 23th: Sequoia gave more insights on its plans to expand into the European market. I'm excited to see them in Europe. European funds will have to step up their game to remain relavant and this is great for every founders building a VC-backed business. (Techcrunch, Slush, Forbes)

It's always good to remember that Sequoia has already built a strong track record in Europe investing into companies like Klarna, UiPath, Unity, Dashlane, Tessian, Graphcore, Tourlane, Wunderlist etc. Many European venture funds would die to have a portfolio like this one.

The firm is now accelerating its expansion by opening an office in London and setting up a dedicated team led by former Accel's partner Luciana Lixandru. On the mid term, the vision is to build a leading European venture franchise with a team of 20 local people with both investors and operators to support portfolio companies.

Sequoia will invest in Europe with the same fund the partners use to invest in the US. It's an equal partnership in which all the incentives are aligned between European and US partners. It's a different set up than in Asia where Sequoia's partners are investing from dedicated funds.

The fund will now move earlier in the investment cycle compared to what it used to do in Europe (series B and later) investing into companies even at a seed stage. Sequoia has built a network of scouts all around Europe to source the best companies in their early days.

Tuesday, Nov. 24th: Marie Ekeland announced her new fund called 2050. It's a new chapter in her life after having worked at Elaia where she invested into Criteo and at Daphni where she invested in companies like Shine, Swile, Holberton and Lifen. 2050 is an evergreen fund that will only invest into five key areas that have the potential to reshape the world we live in: food, healthcare, education, cities and in building trust onto media and financial institutions. Investors will invest whenever they want into the fund. GPs will have no pressure to sell their portfolio company before 2050. This brand new fund has already invested alongside Idinvest into healthcare wearables manufacturer Withings. (Techcrunch, Marie Ekeland 🇫🇷 )

Wednesday, Nov. 25th: Apple announced that it will reduce App Store fees from 30% to 15% for small developers (i.e. developers who are generating less than $1m in annual revenues) starting next year. It's a reaction to all the recent criticism around Apple's monopoly on its store from developers, consumers and governments. Apple is giving away 3% of its AppStore revenues to buy peace of mind. (Bloomberg, The Verge)

Thursday, Nov. 26th: To promote their new startup program, The Family shares every day through newsletters golden nuggets on their learnings on entrepreneurship. It's a Bible with many unique and thoughtful pieces of advice for entrepreneurs. (The Family) You should read them all but here are my favorite ones so far:

Friday, Nov. 27th: David Sacks (investor at Craft Ventures, ex. founder at Yammer and Paypal) wrote a paper to help B2B companies measure their product usage. User engagement a great indicator to understand the health of your product, to predict and prevent churn as well as to better convert users from free to paid plans. David explains that you should start with the DAU/MAU and DAU/WAU ratios used in the B2C world. You should make ajustements to make these metrics fit for the B2B world (take out the weekends and separate paying customers from free users). You have excellent engagement rates when you reach 40% DAU/MAU and 60% DAU/WAU on paying users after adjusting for the weekends. (David Sacks)

Saturday, Nov. 28th: Successful creators will be "Multi-SKU Creators" generating revenues from multiple sources (newsletters, podcasts, videos, merchandising, advertising, books, consulting, speaking etc.). It's wrong to believe that creators should solely focus on one activity (a SKU which is a Stock-Keeping Unit which is the identifier used in the retail industry to distinguish products). They can work on several activities at the same time with different intensity and different business models. (Hunterwalk)

Sunday, Nov. 29th: Facebook acquired Kustomer for $1bn. Kustomer is a CRM that differentiates itself from older players by giving customer agents with a unified view of the customer data. The company previously raised $174m in funding from tier one investors like Coatue, Tiger Global, Battery and Boldstart. It's always good to remember that Facebook's customers are businesses which are paying for advertising on its platforms. Facebook has been adding tools beyond advertising to better serve them and this acquisition is going in this direction. (Techcrunch, Wall Street Journal)

Monday, Nov. 30th: Stockholm based e-scooter startup Voi raised $160m in both equity and debt from The Raine Group, VNV Global and existing investors Creandum, Balderton and Project A. It's interesting to note that the debt is an asset-backed debt facilities in which the funding are secured against Voi's scooters and e-bikes assets. It's a proof that this market is maturing. We know how the economics work and the competition is slowing down as most cities are now giving an oligopoly to 2-3 providers. The funding will be used for market expansion, bringing its last e-scooter model to the market, increasing safety and further investing in technology. (Techcrunch)

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋