🗞 Venture Chronicles - May 2022

Overlooked #115

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of May.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for May!

Sunday, May 1st: GroceryDive wrote a post on how ethnic grocery players like Weee in the US are using shoppable recipes. - GroceryDive

With shoppable recipes, instead of selecting one by one 30-50 SKUs to have all your ingredients for your recipes, you pick the recipes that you want to cook during the week and it will automatically generate a cart.

Weee is creating recipes on its app and is empowering its users to add & share their own recipes. It's key to inspire and ate its customer base about the next meals that they can cook - especially for ethnic food that is harder to access when you're unfamiliar with the cuisine or some ingredients. Weee incentivizes user generated content with recipe-contests rewarded with cash prizes.

Quicklly is rewarding food content creators. Anytime a recipe is purchased, the creator is rewarded.

Monday, May 2nd: Cameo laid-off 25% of its workforce (c.90 employees) to adjust to the new market conditions. Cameo is a marketplace to buy personalised videos from celebrities which had reached a $1bn valuation during a $100m series C round in Mar. 2021. In 2021, Cameo was planning to reach $200-300m in GMV compared to $100m in 2020. In the past couple of months, Cameo announced a partnership with Snap to let advertisers on Snap leverage Cameo's pool of celebrities to make ads and launched Cameo Pass which is a NFT ticketing feature to access special events or communities. - Techcrunch, The Verge, The Information

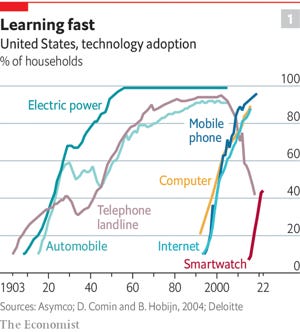

Tuesday, May 3rd: The Economist wrote its tech quarterly update about wearable devices and the "quantified self" movement. - The Economist

"In 2007, Wired magazine dubbed the “quantified self” movement: the meticulous collection and analysis of data about bodies and lifestyle that people do to hack their way to better health."

Metrics on wearables: An Apple Watch is tracking 1m data points per day. In the US, 1/4 people own a fitness tracker or an Apple Watch. In 2020, 200m smartwatches were sold globally and this figure should reach 400m by 2026. People with wearables move more (1.2k more steps per day, 49 more minutes per week of active exercise and 10 min less of sedentary time per day).

With wearables, healthcare data can be continuously monitored which is key (i) to track patients beyond the hospital (e.g. the elderies), (ii) to start making proactive and personalised healthcare recommendations and (iii) to make the healthcare system more efficient.

In Finland, you can link the healthcare data produced by your wearables to your national health record.

"In the next five years, the wearables market will split into two categories: medical-grade devices approved by regulators for people with chronic conditions who need tracking with greater care and accuracy, and devices with less sophisticated features for healthy people who want to keep an eye on their metrics and be able to spot problems early."

Wearables can measure many health variables: activity, sleep, temperature, breathing, blood pressure, oxygen saturation, blood sugar and electrical activity of the heart.

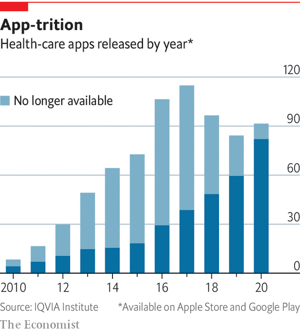

250 health and wellness apps are added everyday on the Apple and Google app stores. These apps are downloaded 5m times per day but 95% of those download are deleted within 24h.

Kaia Health (💙) is registered as a medical device in both Europe and the US. It's a digital therapist for chronic conditions like back pain which will recommend personalised exercises for patients and guide them to perform these exercices correctly thanks to computer vision. Kaia completed a clinical study that proved that its patients treated digitally improved more than the patients treated via in-person therapy.

Wednesday, May 4th: Kevin raised a $65m series A from Accel and Eurazeo (💙) with the participation of OTB, Speedinvest, Global Paytech Venture, OpenOcean and 20VC. Kevin is democratizing A2A payments which is a cheaper, more secure and more convenient payment option than credit cards when it's correctly implemented. It has 6k merchants in 12 European markets. Kevin integrates A2A into e-commerce checkouts, mobile apps but also into physical POS. - Techcrunch, Luca Bocchio

Thursday, May 5th: French online health insurance Alan raised a €183m series E round at a €2.7bn valuation led by OTTP with the participation of existing investors Coatue, Dragoneer, Exor, Index, Ribbit and Temasek. Alan is progressively broadening its vision to become a one-stop-shop health partner. It launched several non-insurance healthcare services like mental health, telemedicine, medical chat or optical treatment. It also entered new European geographies with Spain and Germany. In 2021, Alan grew by 86% to €161m in premium. It has 300k members including 15k in Belgium and 5k in Spain. Alan also has a 94% renewal rate. Its targets for 2025 are: to be profitable, have 3m members and recruit an additional 1k employees in its team. - Tech.eu, Techcrunch, Les Echos

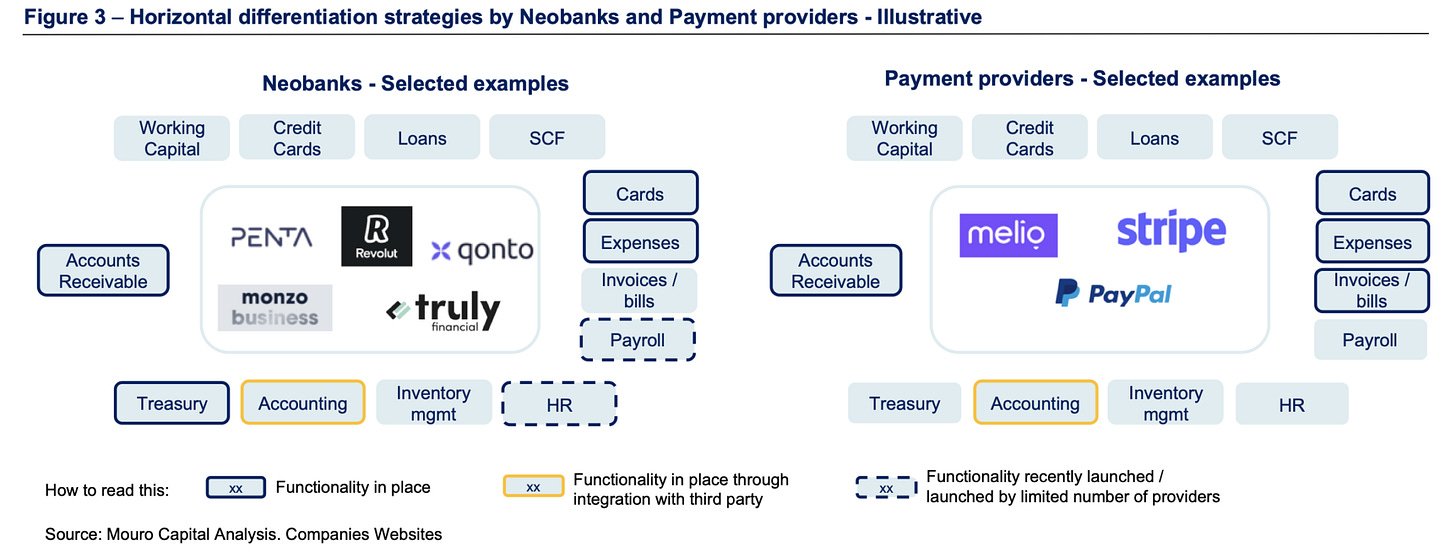

Friday, May 6th: Mouro Capital wrote a post on how corporate spend management platforms can build differentiation to win the category. - Mouro Capital

The main revenue stream for these players is interchange fees which is c.1.5% of volumes net of card network fees, processing fees and issuing fees. To generate $100m in revenues, it means that you should process $7bn in volume.

Two paths are being adopted to build differentiation: going vertical (tailor-made features to address the pain points of an industry and homogenous customer base to reduce CAC) and going horizontal by becoming an all-in-one financial platform (adding features like payment processing, payroll, invoicing, lending).

With horizontal differentiation, you increase the value you provide to customers, you open new revenue streams and you make your product much more sticky.

Mouro Capital highlights 2 key success factors in this market: (i) a strategic approach to customer acquisition beyond discounts/cashbacks which is creating a race to the bottom and (ii) an ability to identify and solved adjacent pain point beyond expense management in your customer base.

Saturday, May 7th: I listened to a The 20 Minute VC's podcast episode with Harley Miller who is the founder and CEO at Leftlane. - The 20 Minute VC

Harley started his career in Insight’s analysts program. He climbed the ladder and became partner by building a strong expertise in internet and consumer businesses - at a time when most VC investments were done into entreprise and SaaS. With Leftlane, Harley built his own fund to carve out his consumer practice and to become an entrepreneur like the entrepreneurs he funds.

The main criteria to be successful in venture in to find and fund startups before they become obvious to the market. Leftlane puts a lot of efforts into finding proprietary deals - companies that are not raising or that are not on the radar of most VC funds.

Leftlane invests in series A, series B and series C. It targets meaningful ownership from day 1 (15-20% ownership) and manages to build outsized ownership in its best performing startups by earning the right from entrepreneurs to lead/colead a subsequent funding round.

The fund is set up to act fast during the due-diligence phase. The investment team is trained to use SQL and Alteryx to generate insights from raw data. Moreover, there is a quick decision making process in which GPs are not bottlenecks.

Sunday, May 8th: I watched a 2017 lecture at MIT from Fred Wilson (GP at USV) on his career and main learnings on venture capital. - MIT

The best time to invest in something is when nobody believes in it besides you. The corollary of that lesson is that you've to totally believe in it and you've to know why.

In 14 years, USV invested into 100 companies with a slow and steady pace of 7 companies per year.

In the venture business, entrepreneurs are the center of gravity. VCs have entrepreneurs as customers and LPs are only shareholders. VCs should work for entrepreneurs and their companies - not for their LPs.

Fred Wilson looks for 3 criterion in entrepreneur: (i) charisma because entrepreneurs have to constantly convince people to suspend disbelief (investors, team members, consumers, skeptical people in the world), (ii) technical expertise (being technical enough to understand all the aspects of the business that you’re building) and (iii) integrity.

Monday, May 9th: The Information wrote about the current environment in the tech sector. - The Information

Tech companies are making hard decisions: (i) freezing hirings, (ii) laying-off employees (20% of the workforce for Peloton, 9% for Robinhood and 3% for Gopuff) and (iii) refocusing on the core business.

Reef (operator of 5k parking facilities that are transformed into logistical hubs) is about to lay-off 750 FTEs out of its 15k FTEs workforce to refocus on profitability.

Tuesday, May 10th: GetHenry raised a €10m seed round led by LocalGlobe with the participation of Visionaries Club and Founder Collective. It designs, co-manufactures and leases e-bikes dedicated to the last mile delivery sector. GetHenry operates in Germany, Austria, Italy and France. It works with customers like JustEat, Flink, Jokr, Wolt or Gorillas. It charges last-mile delivery companies a €100 monthly subscription per ebike to get access to the ebike, the maintenance service and to a fleet management system. GetHenry will use the funding to expand in new geographies and to manufacture new vehicles like cargobikes and moped. - Techcrunch

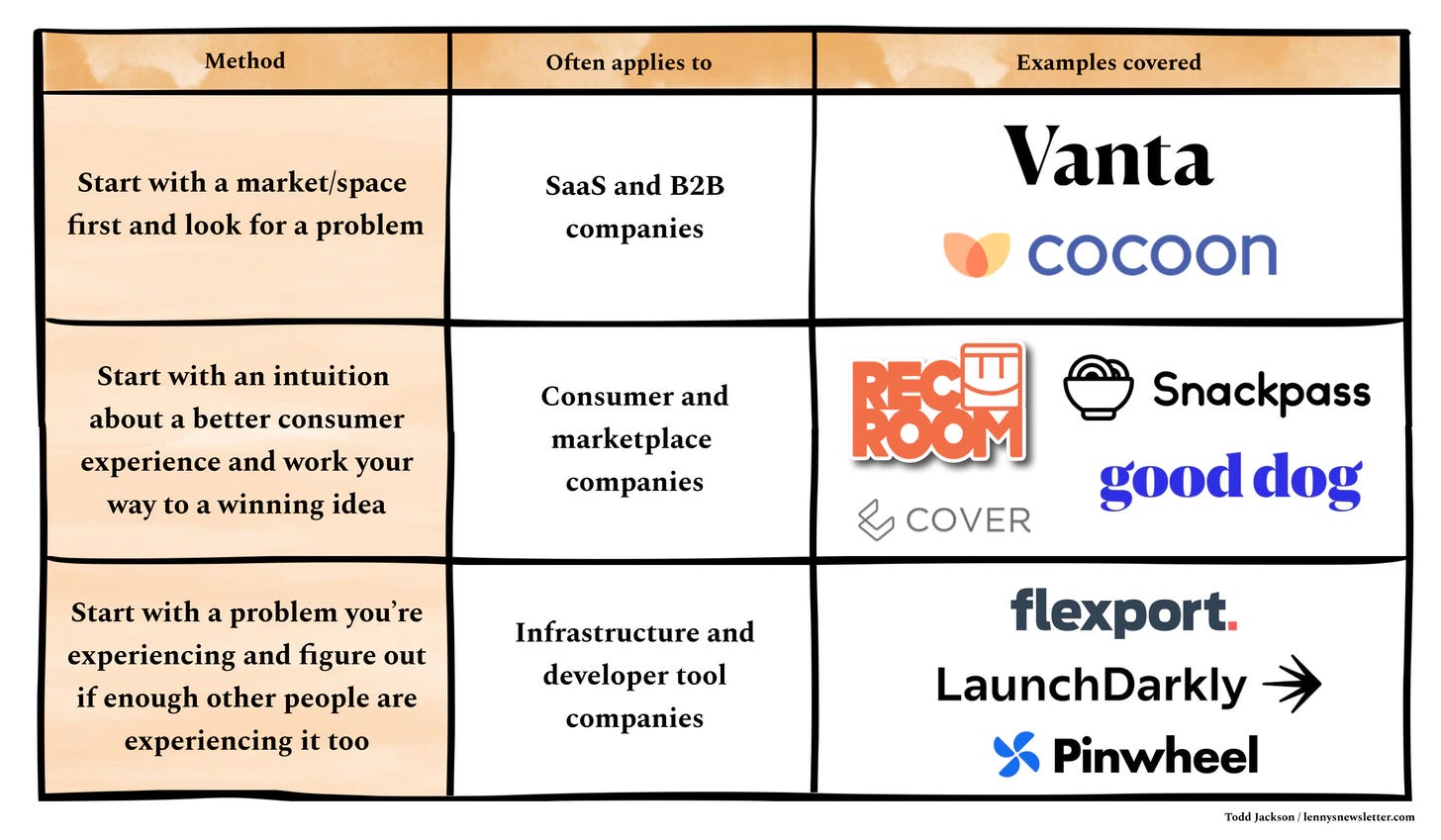

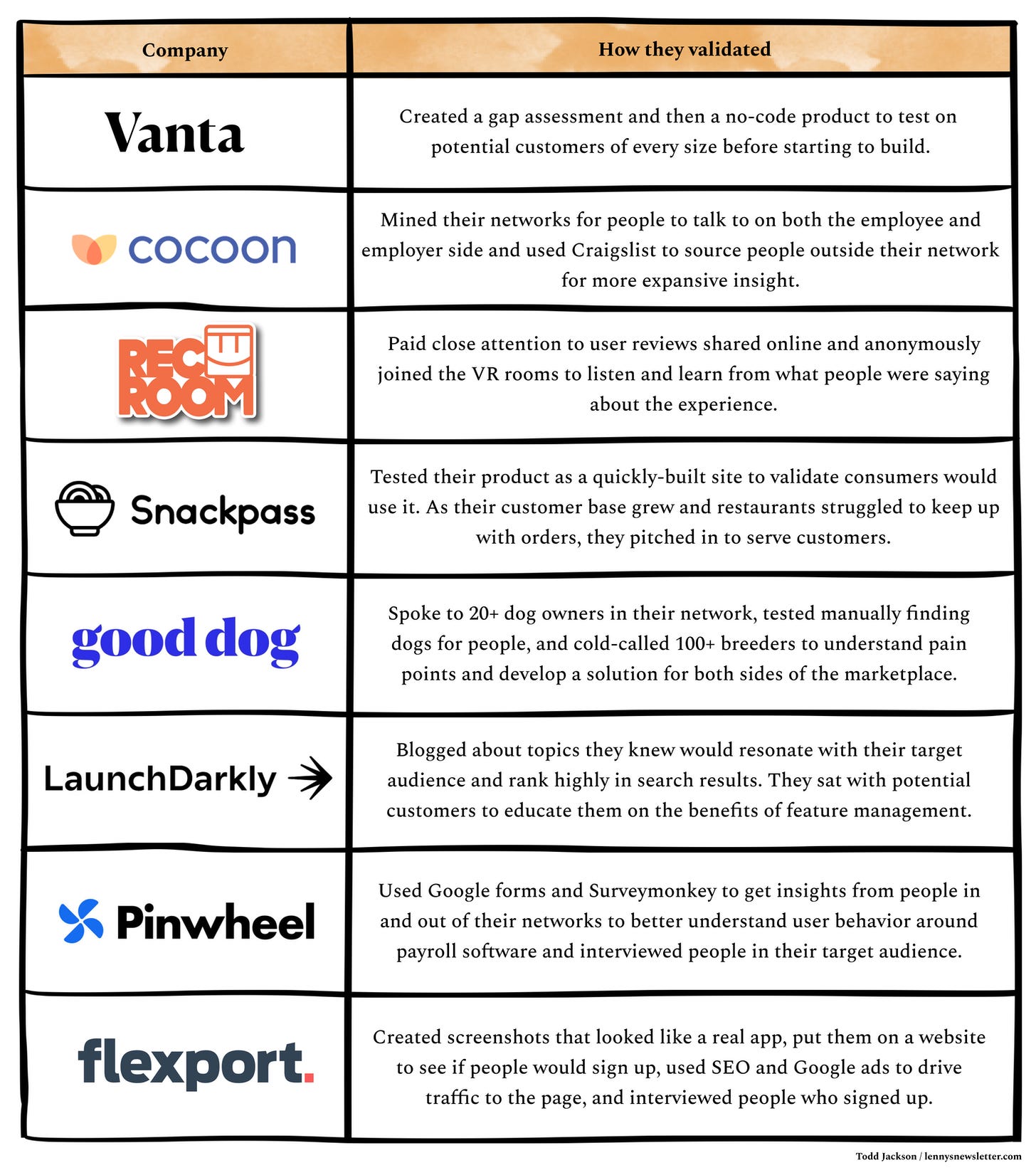

Wednesday, May 11th: Todd Jackson (partner at First Round) wrote a blog post on how to validate a startup idea. - Lenny's Newsletter

It identifies 3 main methods: (i) start with a market that you find interesting and look for a specific problem, (ii) find an area in which the consumer experience needs to be dramatically improved and (iii) start with a problem you're experiencing and validate that other people have the same problem.

Some advice shared in the article: (i) don't build a full product as long as you don't have a strong market pull, (ii) build prototypes that you show to potential customers to have feedbacks and wait for the moment they absolutely want your product, (iii) you should find a painkiller and not a vitamin

“It’s natural to think about things in trends, but there’s a great framework—the jobs-to-be-done framework—that says people hire products to get something done. That’s a more sane way to look at it than trying to map a trend.” - Kevin Tan (founder and CEO at Snackpass)

"What people never talk about is just how hard it is to actually get to product-market fit. In fact, most people never get there. Instead, all you hear about is all the breakout businesses where people magically found PMF. As Marc Andreessen said about finding PMF, ‘When you know, you know.’ Until you find it, you don’t have it. If you have to ask the question, you don’t have it. Put that as the bar you have to clear. It’s ruthless, but if you don’t look at it that way, you just won’t make it." - Kurtis Lin (founder and CEO at Pinwheel).

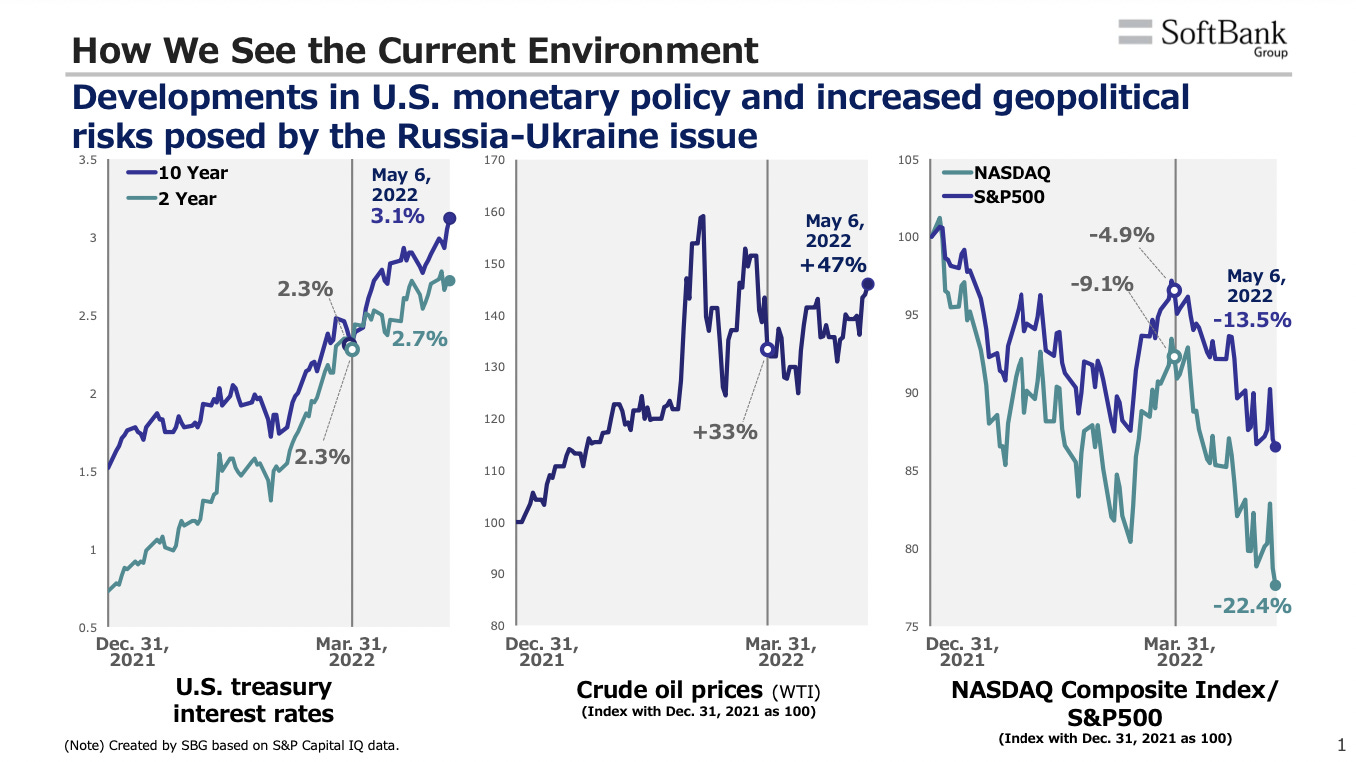

Thursday, May 12th: Softbank announced that it will reduce its investment velocity by 50-75% compared to last year. Its Vision Fund lost $27bn in its last fiscal year ending in Mar. 22. Multiple factors have impacted its performance: the Ukranian war, increasing interest rates and inflation, China's crackdown on the tech sector, etc. - Softbank

Friday, May 13th: I read Rippling's funding memo used to raise a $45m series A in Apr. 2019 with Kleiner Perkins. - Rippling, Rippling 2

"Most businesses have dozens of systems that maintain a list of their employees, and for the most part, none of these systems talk to each other or to any central system about who these employees are."

"There should be a single system of employee data that sits underneath every other business system. Companies and their employees could come to this one place, and make changes to employees in this one system, and that system would handle the propagation out to every other business system."

"If you’re the system of record for employee data, you can build adjacent products with exclusive access to your system."

"Rippling is a hybrid of 3 different software categories: (i) an all-in-one payroll, benefits, and HRIS system, (ii) an “identity” / access management system and (iii) an endpoint device management system."

Rippling is building the "supermarket for SaaS" and has network effects because the more integrations you have the more likely customers will work with Rippling to have the flexibility to connect Rippling to their other tools.

Saturday, May 14th: a16z shared a framework for startups to adjust to a bear market. - a16z

It's a 3-step process: (i) reevaluating your valuation, (ii) understand your burn multiples and (iii) build scenarios.

Reevaluating your valuation: you should consider that your current valuation is the valuation that you have when you multiply your forward revenue by public multiples in your category. You should recalibrate your startup trajectory to be in a position to at least match your last funding round valuation with the cash that you currently have in the bank.

Understand your burn multiple which is the cash burned divided by net ARR added. You can measure it quarterly. You should try to improve your burn multiple to be closer to top quartile companies (i.e. 1.1x if your ARR is between $0m and $10m).

Plan 3 scenarios: (i) a base case which is a plan that you're likely to hit while growing more efficiently than what you were doing in the past, (ii) a best case which is a plan where you're growing at a stronger pace and more efficiently that expected and (iii) a bear case where you need to slow down aggressively to preserve your runway or even reach profitability.

Sunday, May 15th: Sapphire wrote a great post about allocating funding reserves in venture. - Shapphire

In VC, to de-risk capital deployment, you will deploy 50% of your fund as 1st cheques into new companies and you will keep 50% to be re-invested in subsequent rounds of your portfolio companies.

In theory, you want to keep these reserves to double-down on your winners. In practice, it's more complicated: (i) you've to properly identity and reinvest massively in your winners, (ii) a hot market pushes companies to raise back to back rounds which are not de-risking the initial investment because the company does not have the time to reach numerous milestones, (iii) adverse selection makes it hard to maintain prorata overtime in the best companies.

"Reserves need to be very concentrated in the highest multiple opportunities to be accretive to overall fund returns. A top performing fund depends on having winners, and a fund structure and strategy where a GP can put enough dollars into these outliers early enough to drive returns for the entire fund."

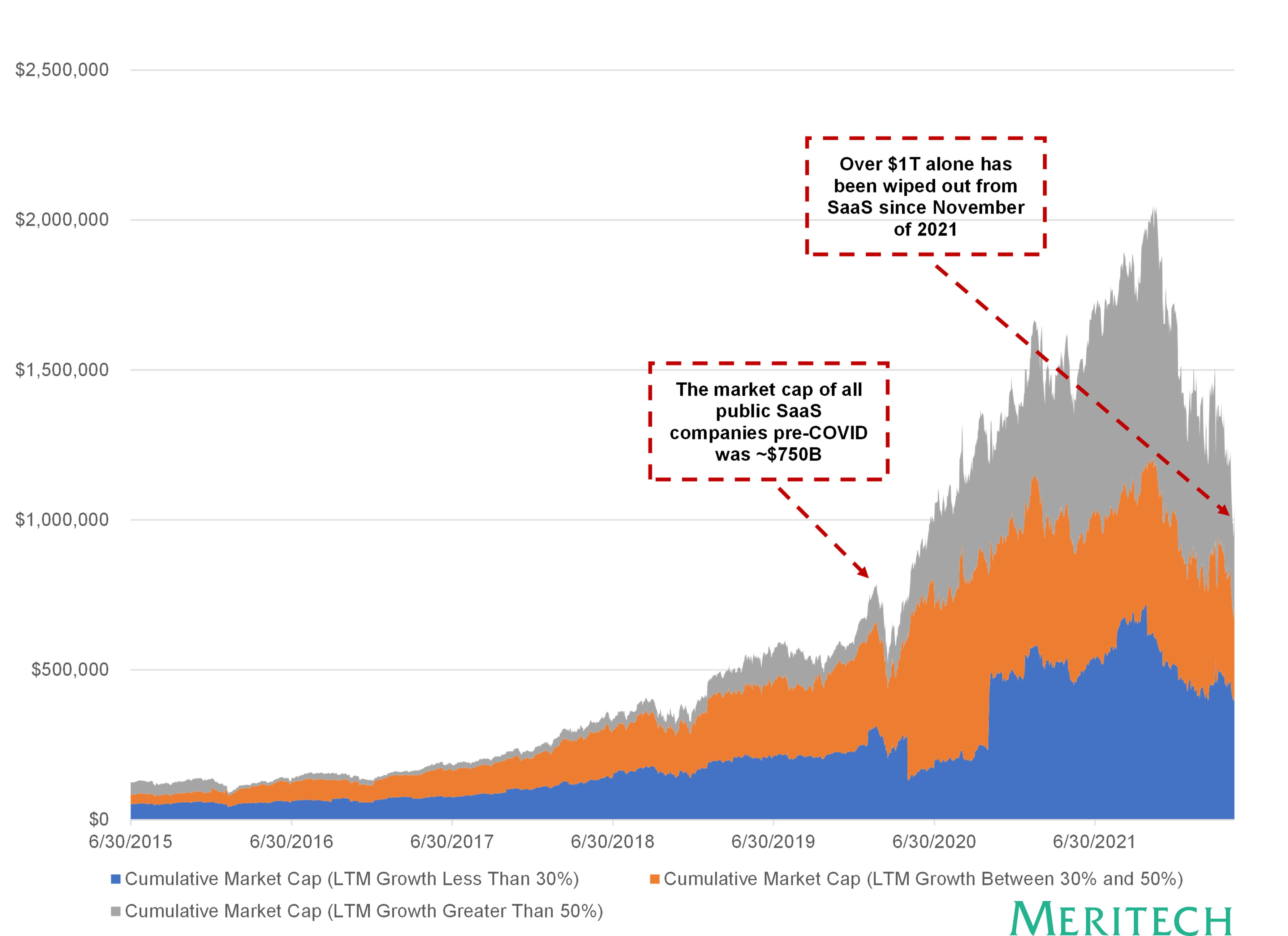

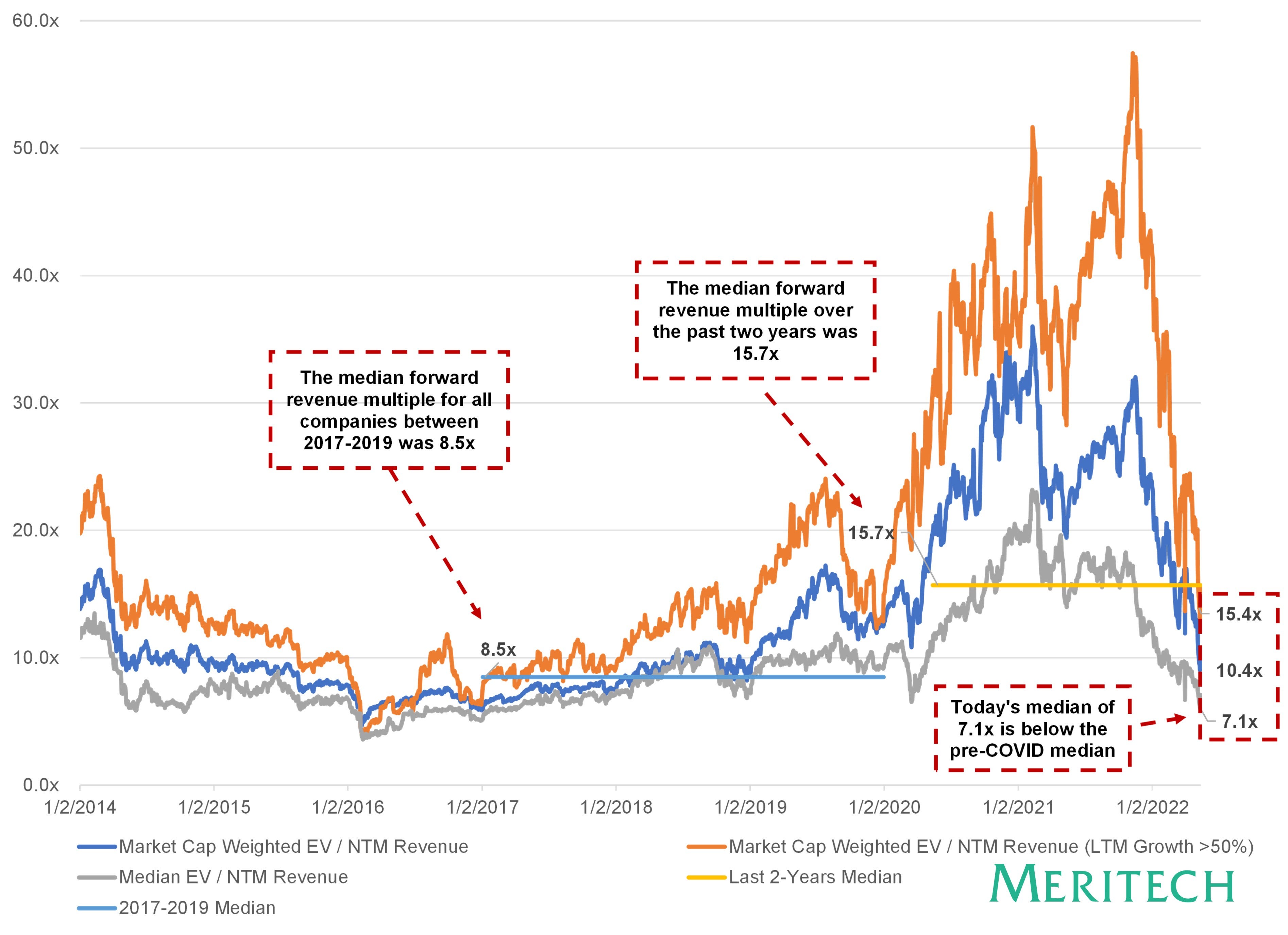

Monday, May 16th: Alex Clayton at Meritech wrote about the SaaS valuation crash in the public market. - Meritech

The market capitalization of the c.90 pure SaaS listed companies is down by 50% compared to 2021 high from $2tn to $1tn.

"The average company market cap is down 57% from its 12-month highs. Forward revenue multiples have fallen on average by 67% from their 12-month highs."

4 key factors: (i) increased interest rates, (ii) growth normalization for tech stocks post-covid, (iii) inflation & macro risk for a potential recession and (iv) war in Ukraine.

"During the past two years, median multiples reached almost 25x for all public SaaS companies (~90 in total). The median today is 7.1x, lower than the 2017-2019 pre-COVID median of 8.5x."

"Every SaaS company should prepare for a scenario in which they trade at 10x NTM revenue steady-state"

"Right now, public market investors are not valuing growth at all costs. Growth and efficiency together are the most important determinants of valuation"

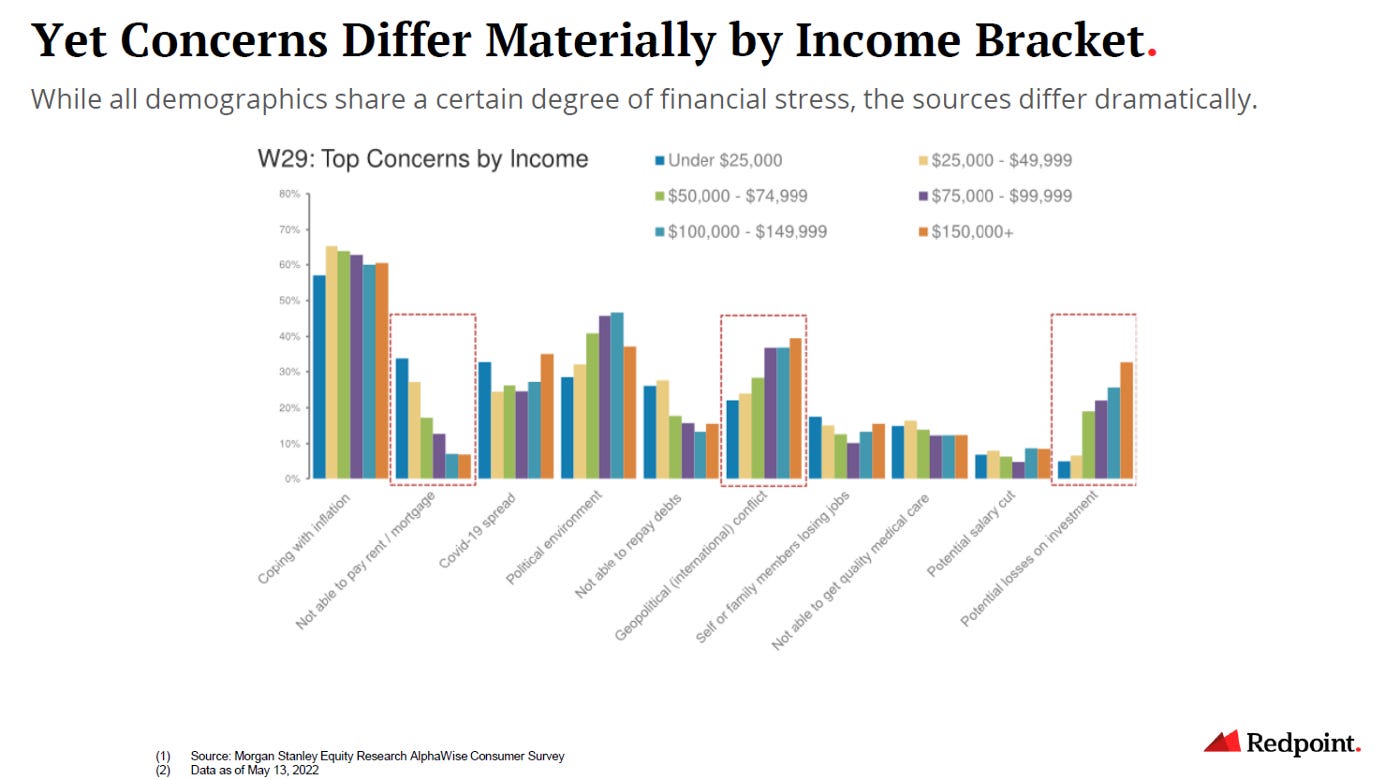

Tuesday, May 17th: Meera Clark at Redpoint wrote about the stock market decline for consumer companies. - Redpoint

"With inflation concerns accelerating, consumers are likely to be increasingly cost conscious. While spending intentions remain strong, consumers are likely to become increasingly cost conscious, electing for DIY or more grassroots offerings. This will create opportunities for both makers / creators as well as the marketplace that serve them."

Inflation has become a top concern for American households.

Consumers have different concerns depending on their income level. Lower income consumers are concerned about inflation and about not being able to pay their rent/mortgage.

For the coming months, the market will reward profitability and cash efficiency.

Wednesday, May 18th: Plaid is launching new products. Plaid started as an open-banking API to access account information. It has moved into banking payment initiation. Plaid is now expanding in several directions: identity verification, income verification and fraud prevention. I believe that bundling identity verification with account linking is a powerful play because it makes the onboarding experience more seamless. Plaid is also well positioned to launch a fraud prevention tool leveraging its network (12k data partners, several hundreds of millions of consumer accounts and 6k customers) and the information/money fluxes it processes. - Techcrunch, Plaid

Thursday, May 19th: Eric Newcomer wrote about Tiger's current situation following the public market crash. - Newcomer

Tiger has almost fully deployed the $12.7bn fund XV it announced in Mar. 22. The FT reported that the fund lost $17bn in 2022.

Tiger stopped to invest in growth stage startups and instead in refocusing on series A/B rounds.

Tiger is highly exposed to Chinese tech companies which are under increasing scrutiny from the government (e.g. Bytedance, Alibaba, Meituan). In 2021, Tiger invested $1.1bn into TikTok at a $460bn valuation.

It's interesting how Tiger categorise its investment mistakes: selling early, being too price sensitive on top assets, underestimating capital intensity, investing in a non dominant player, unsustainable unit economics and misjudged management teams.

Tiger has 4 investment strategies: crossover, long/short public fund, global public long fund, growth equity fund.

Friday, May 20th: Ben Evans wrote about newsletters. - Ben Evans

Paying newsletters have always existed. What's new is that single individuals are now able to make a living from their newsletters without setting up a heavy media corporation and by selling an accessible $5-10 monthly subscriptions to a mass market audience.

Substack has dramatically reduced the friction to publish and monetize a newsletter in exchange of a 13-16% take rate (10% commission and 3-6% Stripe's payment fee). Getting readers when you don't have a pre-existing audience is the other issue that remains unsolved with Substack.

Saturday, May 21st: David Sacks published a post on structuring compensation for a sales team. - David Sacks

An Account Executive (AE) should have a quota that represents 10x its base salary. If an AE reaches its targets, his variable remuneration should be equal to his fixed remuneration.

10% is a standard sales commission for SaaS (e.g. a $1m ARR contract should generate a $100k commission). Beyond the quota, a sales should have an accelerator capturing a 15% commission.

An AE should ramp-up in 4 months. It can be shorter or longer depending on the complexity of the product and the sales cycle.

Sunday, May 22nd: David Sacks wrote a post about burn multiple to measure capital efficiency of tech startups. - David Sacks

"Burn Multiple = Net Burn / Net New ARR" - It answers the question: "how much is the startup burning in order to generate each incremental dollar of ARR?"

Burn multiple is a good measure of product market fit (all else being equal, you will have a lower burn multiple if you have a strong market pull) and is also a proxy for other potential issues in the company (gross margin, sales efficiency, churn, etc.).

"The Burn Multiple should improve as the startup matures. For example, a seed stage company might have a Burn Multiple of 3 because it just started selling. After the Series A, it might drop to 2. After the Series B, when the sales team should be operating at scale, the expectations for efficiency increase even more. Eventually, for a company to become profitable, burn must reach 0, which implies that the Burn Multiple should also approach 0 over time"

Monday, May 23rd: Kyle Harrison wrote about the potential causes that could lead to the death of a venture firm. - Kyle Harrison

"When I was at Index we would include two sections in our memos that were popularized by Larry Summers. We would write about a company's pre-parade and pre-mortem. Not only a dream the dream scenario, but a dream the nightmare."

Sequoia is known for being constantly paranoiac to remain at the top of the venture capital industry. "That's part of why we continue to innovate. I think it's so dangerous if you become fearful. If you're successful, and you don't continue to innovate and push boundaries. Because you're guaranteed to not succeed in the future if you don't make changes. Because the world around us is changing. So we better adapt very quickly, and make smart moves, and not just rest on our laurels."

Bringing financial performance to LPs is the condition sine qua non to remain in the venture capital business.

"If VCs are too afraid to venture into contrarian categories with big risks they could miss out on the next generation of venture returns."

Poor succession management is another potential cause of death for venture funds especially when "you get a lot of imbalance in who is providing the most value to the firm vs. who is seeing the largest share of the economics and upside."

A VC product offering that becomes irrelevant with changing market conditions (e.g. Tiger's value proposition working only in a bull market with founders who want hands-off investors and attractive deal conditions).

"At the end of the day startups are competing in a bloody knife fight for every customer, every hire, ever press release, and every product launch. VCs represent "borrowed credibility" to aid in that fight."

Tuesday, May 24th: Dan Teran from Gutter Capital shared publicly an email he sent to portfolio companies. - Dan Teran

"I can tell you with a high degree of certainty the deals will get done. [...] The relevant question is will your deal get done, and at what price. [...] Panicking is not productive, but neither is carrying on business as usual. [...] Now is the time to set yourself and your business up for success in the uncertain year that lies ahead of us. The advice is evergreen, but that is the point. You will never control the macro environment, but you will always control the caliber of your own execution."

Founders should consider the following adjustments: (i) be explicit about your goals and your plans to achieve them, (ii) evaluate your team with new eyes (increase the talent bar, keep only necessary and excellent employees), (iii) focus on unit economics, (iv) delight your customers (provide them with an experience that is so great that they can stop talking about it), (v) over-communicate to investors, (vi) review your company culture and embody it in your day to day, (vii)

"Generally speaking, prior to a Series A there is no need for administrative or support personnel. All team members should either be focused on building the product or selling it. The obvious benefit to minimizing headcount is payroll, the less obvious but more significant benefit is distraction"

Wednesday, May 25th: Howard Marks published a new market memo called "bull market rhymes" about how investors behaviors patterns are repeated across market cycles. - Oaktree

"There are recurring cycles, ups and downs, but the course of events is essentially the same, with small variations. It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes." - Theodor Reik in The Unreachables

"If the stock market was a machine, it might be reasonable to expect it to perform consistently over time. Instead, I think the substantial influence of psychology on investors’ decision-making largely explains the market’s gyrations."

"When investors turn highly bullish, they tend to conclude that (a) everything’s going to go up forever and (b) regardless of what they pay for an asset, someone else will come along to buy it from them for more (the “greater-fool theory”)"

"The excess to the upside makes for a period of above average returns, and the swing toward excess on the downside makes for a period of below average returns."

"The most important thing about bull market psychology is that, as cited in the final bullet point above, most people take rising stock prices as a positive sign of things to come. Many are converted to optimism. Relatively few suspect that the gains to date might have been excessive and borrowed from future returns and that they presage reversal, not continuation"

"When there’s too much money in the hands of investors and providers of capital and they’re too eager to put it to work, they bid too aggressively for securities."

“What the wise man does in the beginning, the fool does in the end.” People who buy in stage one of a bull market, when prices are low because of prevailing pessimism, have the potential to earn high prospective returns with little risk: the main prerequisites are money to spend and the nerve to spend it. But when bull markets heat up and good returns encourage investors’ optimism, the traits that are rewarded are eagerness, credulousness, and risk-taking. In stage three of a bull market, new entrants buy aggressively, keeping it aloft for a while. Caution, selectivity, and discipline go out the window just when they’re needed most."

Thursday, May 27th: The Information accessed to a 50-slide deck that Sequoia shared with its founders on how they should adapt to current market conditions. - The Information

"We believe this is a Crucible Moment, one that will present challenges and opportunities for many of you. First and foremost, we must recognize the changing environment and shift our mindset to respond with intention rather than regret."

"It will be a longer recovery [compared to the covid crisis] and while we can't predict how long, we can advise you on ways to prepare and get through to the other side."

"Belt tightening and priority reassessment will have second- and third-order effects, as one company’s costs represent someone else’s revenue or purchasing power."

The Nasdaq is down -28% since November 2021. But the reality in tech is gloomier. Mega tech capitalisations (Facebook, Amazon, Google, Apple) are less impacted because they are perceived as safer assets. Besides them, "more than 60% of all software, internet, and fintech companies trade for below their pre-pandemic 2020 stock prices."

In the long-term, companies with durable growth and improving profitability are the most rewarded by the public market but at the moment, if you're unprofitable, you're heavily sanctioned.

In order to survive, companies must be adaptable, must move quickly (avoid the death spiral), must get the discipline of a company running out of cash, must seize opportunities to win their market in the long term.

Friday, May 28th: Gorillas is struggling. It's a European quick commerce startup which raised more than $1bn in funding including a $1bn round raised in Sep. 21 at a $2.1bn premoney valuation. Gorillas is running out of cash. It's said to have $300m left in the bank and to burn $50-70m every month. Gorillas is on the market to raise additional funding. It won't be easy in a market downturn over-indexing profitability over growth and extremely harsh against vertically integrated model. In the meantime, the company had to take drastic decisions like laying off 300 employees in its HQ and closing 4 markets (Italy, Spain, Denmark and Belgium). I'm adding quotes from the letter sent to the company by Gorillas' CEO. - Techcrunch, Sifted, Business Insider, FT

"Two months ago in March, the markets turned upside down, and since then the situation has continued to worsen. Very rapidly, greed in the markets was replaced with cautiousness. And tech companies, especially low or negative margin tech companies, are facing a very strong headwind. The result of this new reality is that wealth and money are being transferred to low risk profitable businesses. This will kick-off a natural selection process in our q-commerce industry."

"In January 2020 there were 30 players in our industry. In January 2021 only 15 remained In January 2022 you can count 4. And now the stage of the final 4 begins, where one year from now there will be only 1-2 players remaining. Gorillas will be this player. And this requires a new plan."

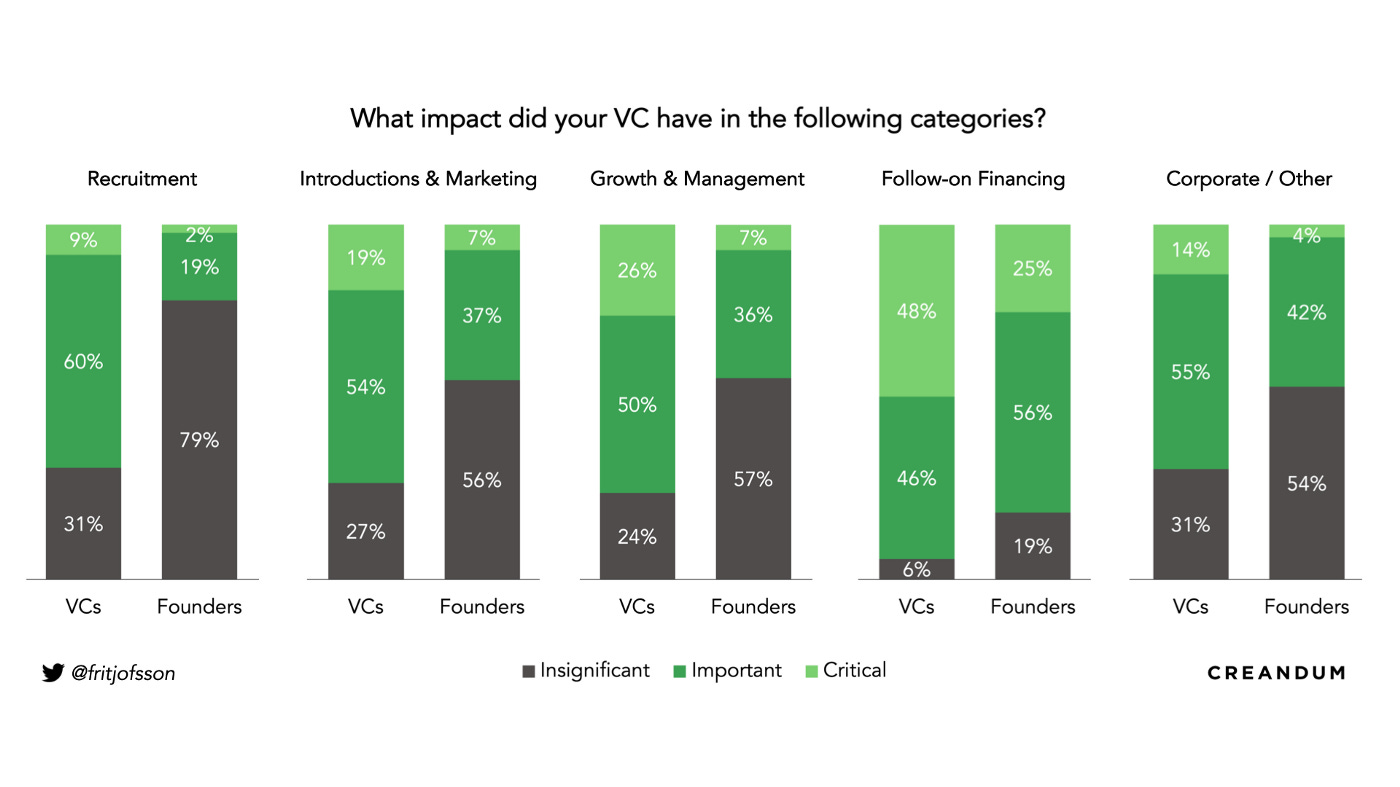

Saturday, May 27th: I read a thought provoking article from Carl Fritjofsson at Creandum asking founders and VCs about the value added by VCs to their portfolio companies. - Creandum

VCs overestimate the value they provide to founders by a 35% difference. When we dig into categories, the largest mismatch is around recruitment and the smallest around fundraising.

Founders expected to be supported by VCs on 3 main topics: fundraising, founder coaching and hiring.

The 3 most important criteria for founders while evaluating VCs are: personal chemistry, sector experience and speed.

There is also a difference on the perception of how of frequent is the communication between founders and investors. Most VCs say they communicate weekly or biweekly with founders. Most founders say they communicate monthly or quarterly with VCs.

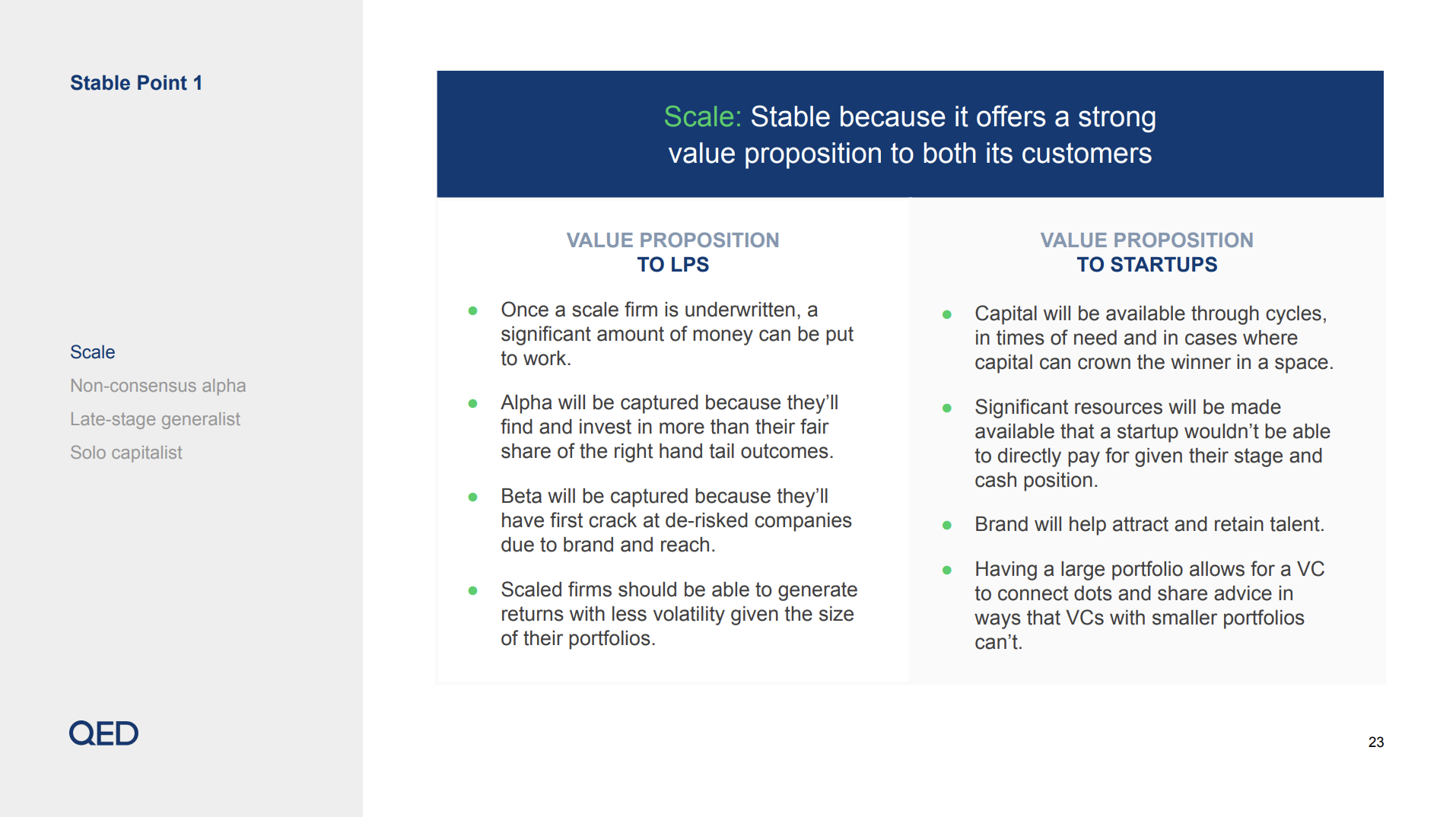

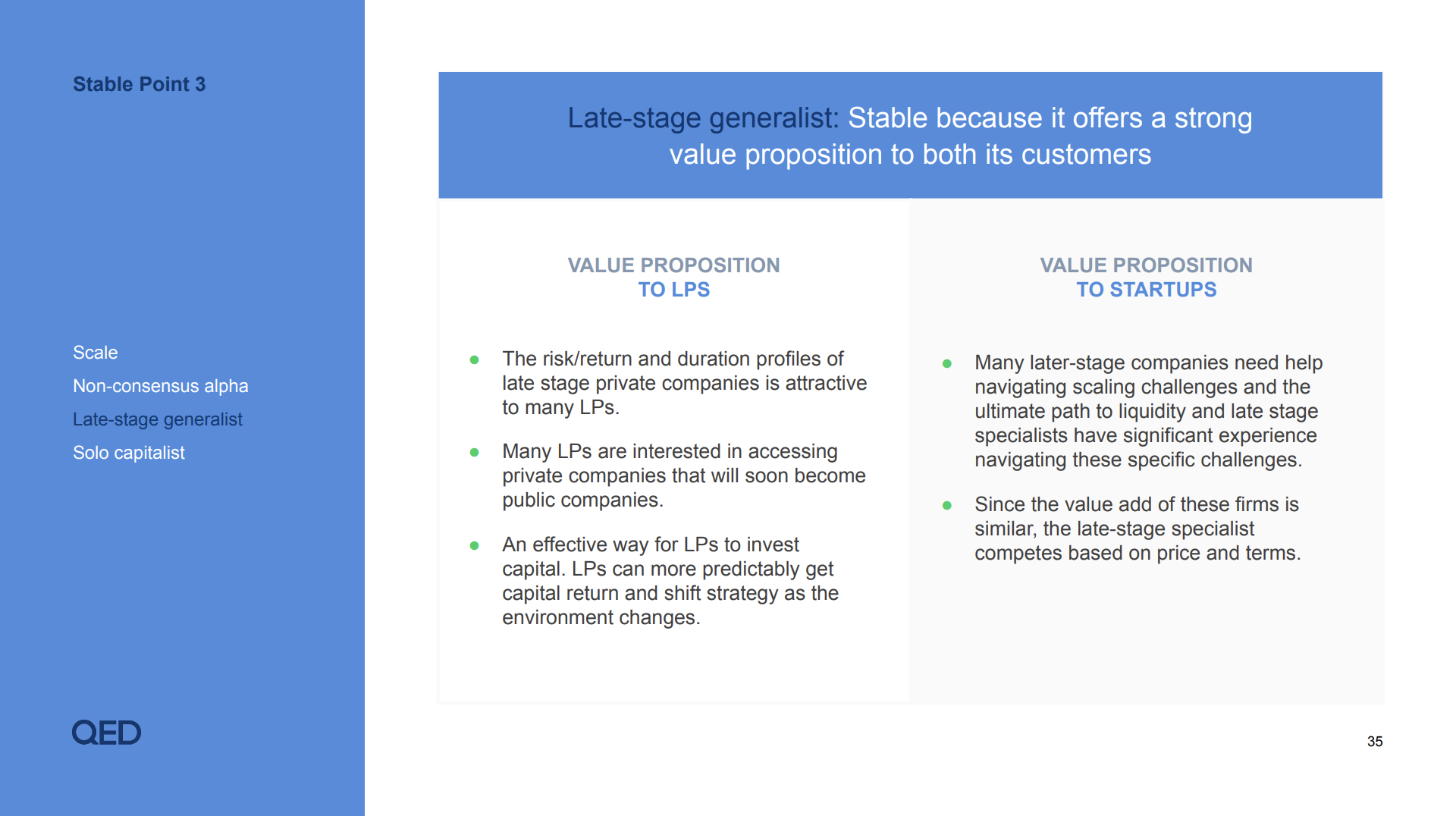

Sunday, May 29th: QED wrote about the 4 winning strategies in venture capital: scale (multi-stage and multi-geography, platform strategy to support entrepreneurs, co-existence of speed and thoroughness in due diligence), no-consensus alpha (1st check-in, investing in overlooked teams/ideas/markets, support to make the company more consensual to customers/employees/investors), late-stage generalist (100% coverage of their stage, derisked assets, ability to remain price disciplined), solo capitalist (proprietary dealflow, higher value per dollar invested). - QED

Monday, May 30th: Jamin Ball who is an investor at Redpoint wrote about the state of SaaS public companies. - Clouded Judgement

SaaS multiples are now probably too low compared to historical average. Nonetheless, forecasted earnings may be wrong if we enter a recession (budget cuts, longer sales cycles). In that case, multiples on forward earnings could be only artificially too low. "if estimates get revised down, then today’s real multiples are higher than current consensus based multiples".

"For a clearing event to “rebound” we’ll need the Fed to start acting dovish + companies proving numbers were artificially revised down too low. For the former, I don’t foresee this happening before July. For the latter, we won’t have data on who’s fundamentals are still strong until Q2 or Q3 earnings."

Software is better positioned to outperform in a downturn than it was in the 2 previous downturns (global financial crisis and tech bubble) because SaaS companies provide more value and are easier to sell/deploy.

Tuesday, May 31st: Zip raised a $43m series B round at a $1.2bn valuation from YC Continuity. It's a SaaS to streamline the procurement process. It's "the new concierge for procurement". On the one hand, procurement teams are able to build complex approval workflows on Zip while having a centralized platform to follow all procurement requests. On the other hand, employees will log their procurement requests on Zip and will have full transparency of where their requests sit in the approval process. Zip was founded in 2020 and has already attracted 100 customers including blue-chip logos like Canva, Snowflake, Roblox, Coinbase, Airtable, Toast, Webflow and Databricks. - Techcrunch

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋