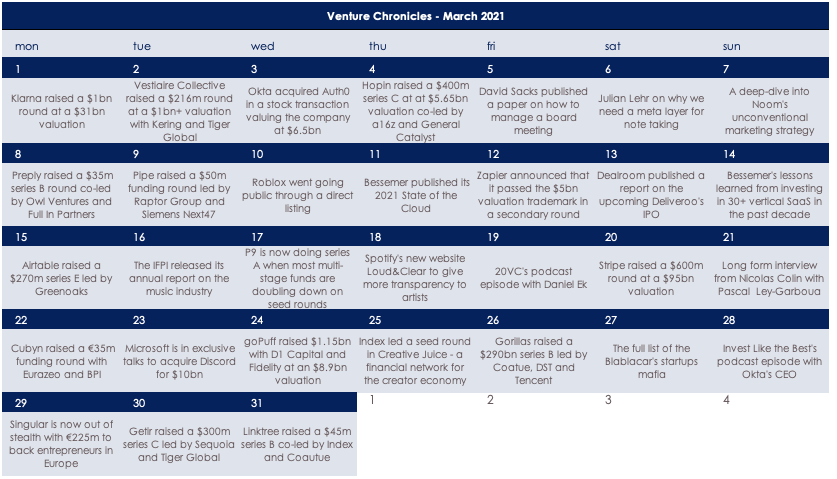

🗞 Venture Chronicles - March 2021

Overlooked #67

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful tech news of March.

Hi everyone! 👋

Two quick notes before jumping into today’s newsletter:

Idinvest/Eurazeo is rebranding into Eurazeo. Eurazeo acquired Idinvest in 2018 and this rebranding under a unique name is the next logical step to build a European private equity giant (€21.8bn of assets under management, 450 companies in our portfolio, 11 offices across the world and 300 colleagues). In venture, it means that we have a unique platform to back the best European entrepreneurs from seed to pre-IPO rounds with my team investing in seed, series A and series B and a growth team focused on series C and beyond.

I’m sorry for sending you the March’s edition of Venture Chronicles only in May. My editorial schedule was quite packed in April. To catch-up, I will publish both the March and the April’s editions this week.

For 2021, I wanted to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for March!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Monday, Mar. 1st: Swedish-based buy now, pay later startup Klarna raised a $1bn round at a $31bn valuation (3x the valuation of the previous round done 6m ago). Klarna started to go direct to consumer through a mobile app and by adding financial services in certain countries like Germany and Sweden (current accounts, saving accounts). The company is also rumoured to prepare a direct listing in 2021. - CNBC, Techcrunch

Tuesday, Mar. 2nd: Our portfolio company Vestiaire Collective (💙) raised a $216m round at a $1bn+ valuation in a round led by Kering (Gucci-owner took a 5% stake in the company) and Tiger Global. Vestiaire is a second hand marketplace for luxury goods. It has complex operations to certify all the goods purchased on the platform. The company experienced a 100% GMV growth in 2020 driven by the growth of the secondary fashion market (forecasted to reach $60bn by 2025). 21% of our closet are made of secondary pieces in 2021. This percentage is supposed to increase to 27% in 2023. Vestiaire is currently applying to become a B-corp certified business and is planning to hire 150+ people in its technology team to expand its platform. It will also launch a buy back circular solution for luxury brands. - Techcrunch, GlobeNewswire

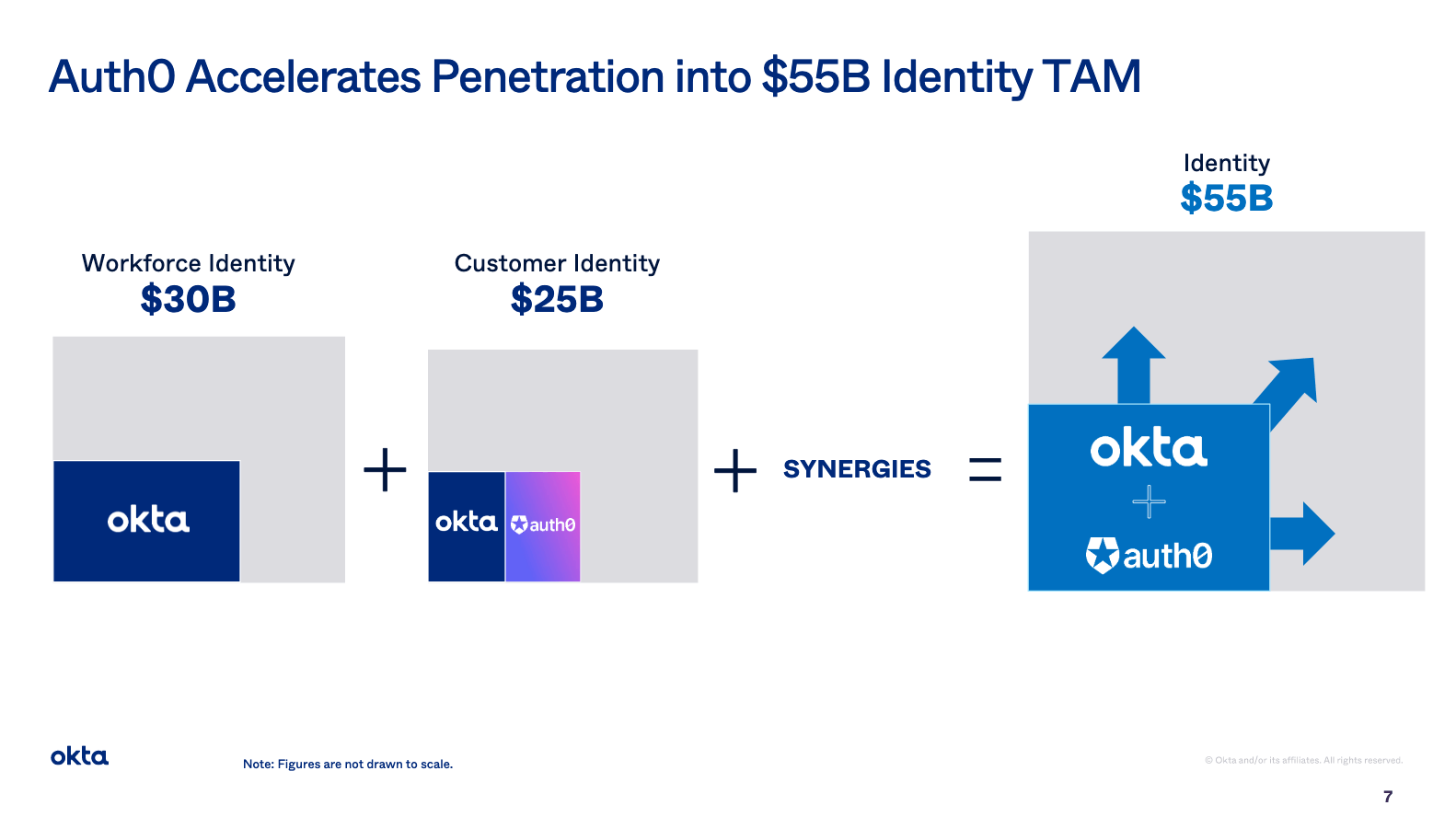

Wednesday, Mar. 3rd: Okta acquired Auth0 in a stock transaction valuing the company at $6.5bn. In Jul. 2020, Auth0 raised a $120m round at a $1.9bn valuation led by Salesforce Ventures. While Okta focuses on worker identity, Auth0's core market is customer identity. Nonetheless, Auth0 and Okta were constantly competing in tenders. The acquisition will relieve the competition pressure. Moreover, both companies have complementary go to market as Okta is a top down sales organisation while Auth0 was built on a developer first bottom up strategy. - Supertokens, Auth0, Okta

Thursday, Mar. 4th: Hopin raised a $400m series C at at $5.65bn valuation co-led by Andreessen Horowitz and General Catalyst. Hopin started to operate less than 1y ago. It has already reached $70m in ARR, attracted 85k customers (inc. 30k acquired since November), has now 400 FTEs (vs. 23 in April 2020) and has already acquired two companies (Topi and StreamYard). - Sifted, Hopin, Techcrunch

Friday, Mar. 5th: David Sacks published a paper on how to manage a board meeting when you are a SaaS founder with great insights. - David Sacks, Board Deck Template

He recommends the following agenda: CEO update (30 min), sales update (30 min), other departmental updates (20 min), financials (10-20 min), team update (10-20 min), (vi) admin topics (5-10 min)

In the CEO update, you should share what has went well and what hasn’t the past 3m, you should share your strategic learnings of the quarter and reviewed the main KPIs of the business.

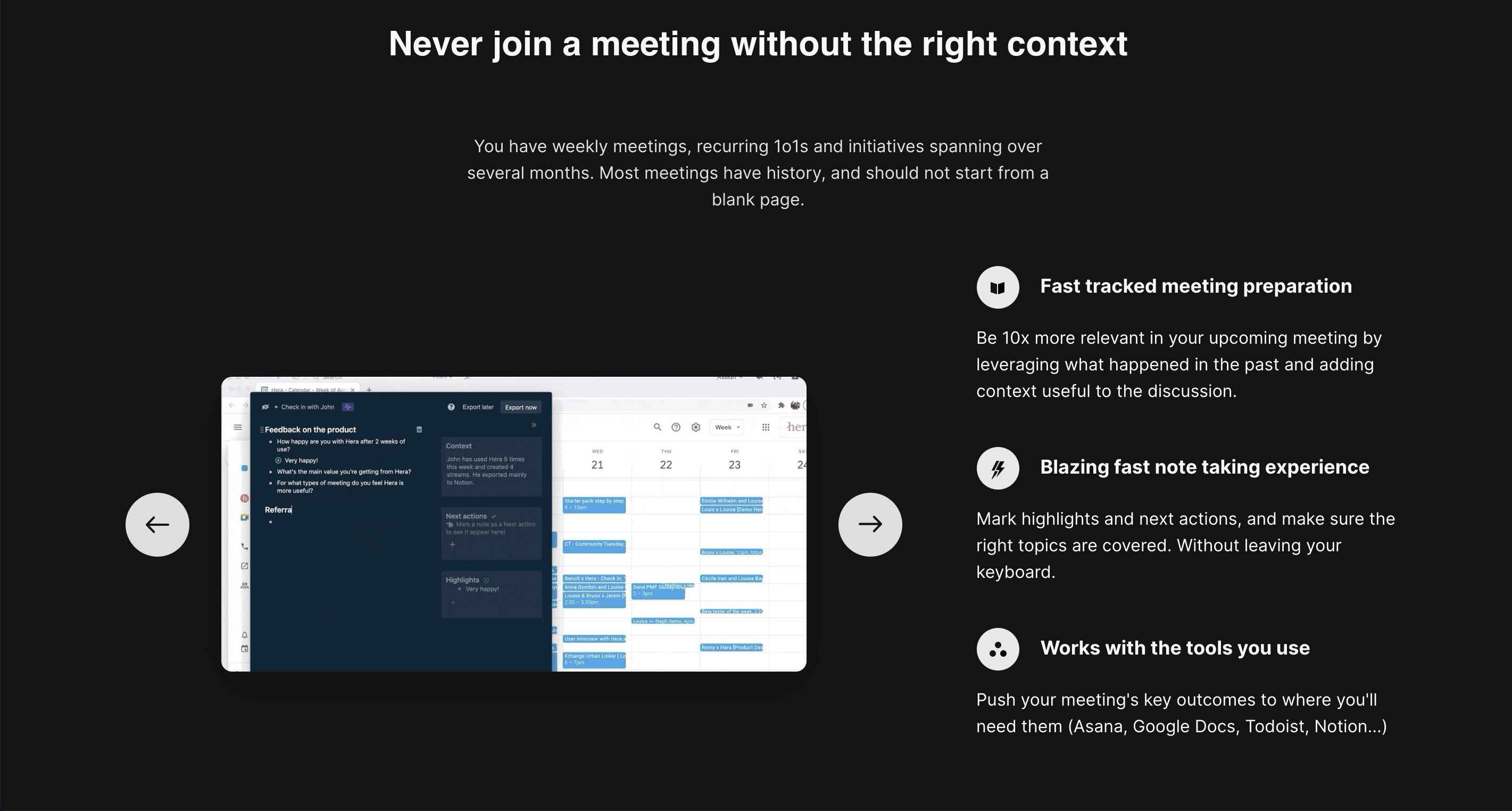

Louise and Bruno at Hera love to share with their beta users their key learnings from their favorite readings about the productivity’s space. Hera is a tool to make your meeting productive again. You can join the beta by clicking on the below button. Every month, I will give you a glimpse in the Hera’s community with an article shared in their Slack - starting with a fantastic piece from Julian Lehr on notes.

Saturday, Mar. 6th: Julian Lehr wrote a refreshing take on note-taking and why we need a meta-layer for it. - Julian Lehr shared by Hera

A lot of notes you take are actually linked to another object (a person, an email, a doc, a google sheet, a figma spec, whatever).

Taking these notes somewhere far away from the related object (e.g. in another product) is a pain and almost always implies you won’t be able to use these notes.

What makes physical post-it notes so powerful is their spatial relationship with what they are referring to.

Imagine how amazing it would be to have a tool to take notes from everywhere and see these notes next to the relevant objects. If you want to write down something about a podcast , you would see the notes next to the podcast in Apple Podcast or Spotify. Same for books in Amazon or people in Gmail.

It could also be used to leave instructions for other people in products.

Sunday, Mar. 7th: I read a deep dive into Noom's unconventional marketing strategy. Noom is a fitness and nutrition mobile app. The company was founded in 2008 but the mobile app was launched in 2016. Noom raised $117m in total and generated $237m in revenues in 2019. - Have a World

Compared to offline incumbents (Weight Watchers, Jenny Craig) targeting mainly women looking to loose wight, Noom appeals to a broader audience. Moreover, it does not rely on external support with coaches and group peer pressure. It's a digital first offering relying on building healthy habits.

Noom also has a complex pricing strategy with several tiers giving the user more value if he pays more. It's efficient in a space where you can play with users that can feel guilty if they don't engage in the long run.

Monday, Mar. 8th: Ukraine-based tutoring platform Preply raised a $35m series B round co-led by Owl Ventures and Full In Partners with the participation of existing investors P9, Hoxton and All Iron. 2020 was a fantastic year for the company: it quadrupled its GMV, its revenues, the number of active learners and tutors on the platform. 1/3 of Preply's revenues are now coming from the U.S. - a country which was launched in 2020. Preply is a marketplace connecting students who want to learn a new language with tutors. The company also has a curriculum that students can follow on their own between two sessions with a tutor. - Tech.eu, Techcrunch

Tuesday, Mar. 9th: Pipe raised a $50m funding round led by Raptor Group and Siemens Next47 with the participation of strategic investors like Shopify, Slack, Hubspot and Okta. It's a trading platform which allows companies that have recurring revenue streams to trade these revenues against upfront cash from institutional investors. It started helping SaaS companies turn their monthly or quarterly subscription into annual cash flow to fund their expansion without raising additional equity. Pipe launched publicly in June 2020 and has already attracted 3k customers and $1bn in tradable annual recurring revenues. The company will use the funding to grow outside its core U.S. market and to expand beyond SaaS to other forms of revenues like D2C subs, streaming services and even VCs selling their management fees. - Crunchbase, Pymnts, Techcrunch

Wednesday, Mar. 10th: Roblox went public through a direct listing. In Feb. 20, a16z invested $50m in the company at a $4bn valuation. In Jan. 21, Roblox raised a $520m pre IPO round at a $29.5bn valuation. 2020 was an impressive year for Roblox and going public is a well-deserved achievement. 2w ago, Roblox organized its first investor day full of insights:

As of Dec. 2020, Roblox had 32.5m DAUs, 8m active developers, 20m user generated experiences and 2.6 usage hours per day on average. Users engage with 20 different experiences every month.

In 2020, $329m were paid out to developers (vs. $112m in 2019). 1.25m developers earned Robux (Roblox’s digital currency), 1,250 earned more than $10k. 300 earned more $100k. It means that it's still hard to make a living as a developer on Roblox.

Roblox is divided into 2 key components: (i) Roblox Client: an App. Store to play games and experiences with your friends, (ii) Roblox Studio: a game engine to create both experiences and avatar items. When you download Roblox on a computer, you download the 2 components. Roblox wants to reduce the friction that exists between consuming to creating content. Roblox Client is another "low-floor, high ceiling tool": it's easy to start creating your first game or avatar item but the platform is super deep if you want to develop top notch experiences.

Roblox is compensating developers with the following schemes: (i) a 70% take rate on avatar items, (ii) a 30% take rate on experience purchases, (iii) a 30% take rate on items & dev. tools that devs are developing for other devs., (iv) an engagement based payouts based on the amount of time spent by premium subs in their experiences.

Roblox highlighted 4 growth levers for the future: (i) geographical expansion beyond the U.S., (ii) age demographic expansion beyond its core under 13 y.o. audience, (iii) platform expansion to go beyond playing to learning, to experiencing and ultimately to working together, (iv) monetization expansion (double down on Premium, reduce the frictions to pay, partnering with 3P brands).

I love the below graph. It shows the creation date evolution of the top 1k games on Roblox. You see that 50% of the top experiences were created in the past 2y. At the same time, certain experiences lasts for years.

Thursday, Mar 11th: Bessemer published its 2021 State of the Cloud and shared 7 predictions about the future of cloud in 2021. - Bessemer's PDF, Bessemer's Video

Trend n°1: Unbundling the office. Opportunity to unbundle both Microsoft and Google's office suites.

Trend n°2: Bringing SMB back with SaaS. Pandemic was a shock for small business owners and will use cloud software tools to support their business (do more, with less mindset).

Trend n°3: Diversity, equity, and inclusion software finally getting recognition. Diverse and inclusive teams are a key competitive advantage when done right and many software are helping in this space. These tools are no longer a nice to have but a must have.

Trend n°4: Data and machine learning infrastructure are accelerating to new heights. Companies are transitioning to the cloud and are generating more data than ever. Therefore, they need tools to capitalize on these data.

Trend n°5: The rise of the “citizen” developer and creator. Software development is being democratized.

Trend n°6: Fintech and crypto players are changing financial services forever. Financial services infrastructure is being rebuilt at the moment. It will change the businesses and consumers use financial services.

Trend n°7: The vertical SaaS wave is turning into a tsunami. Every industry has accelerated its transition towards to the cloud and vertical centric software will reach large penetration rates.

Friday, Mar. 12th: Zapier announced that it passed the $5bn valuation trademark in a secondary round involving Sequoia and Steadfast Financial. It also acquired no-code education platform and community Makerpad. Zapier is a no-code automation tool founded in 2011 connecting 3k+ applications with easy to set up scripts. It only raised a $1.2m seed round in 2012 with Bessemer and DJF. The company also reached $100m ARR in summer 2020 and is now above $140m ARR. - Techcrunch, Forbes

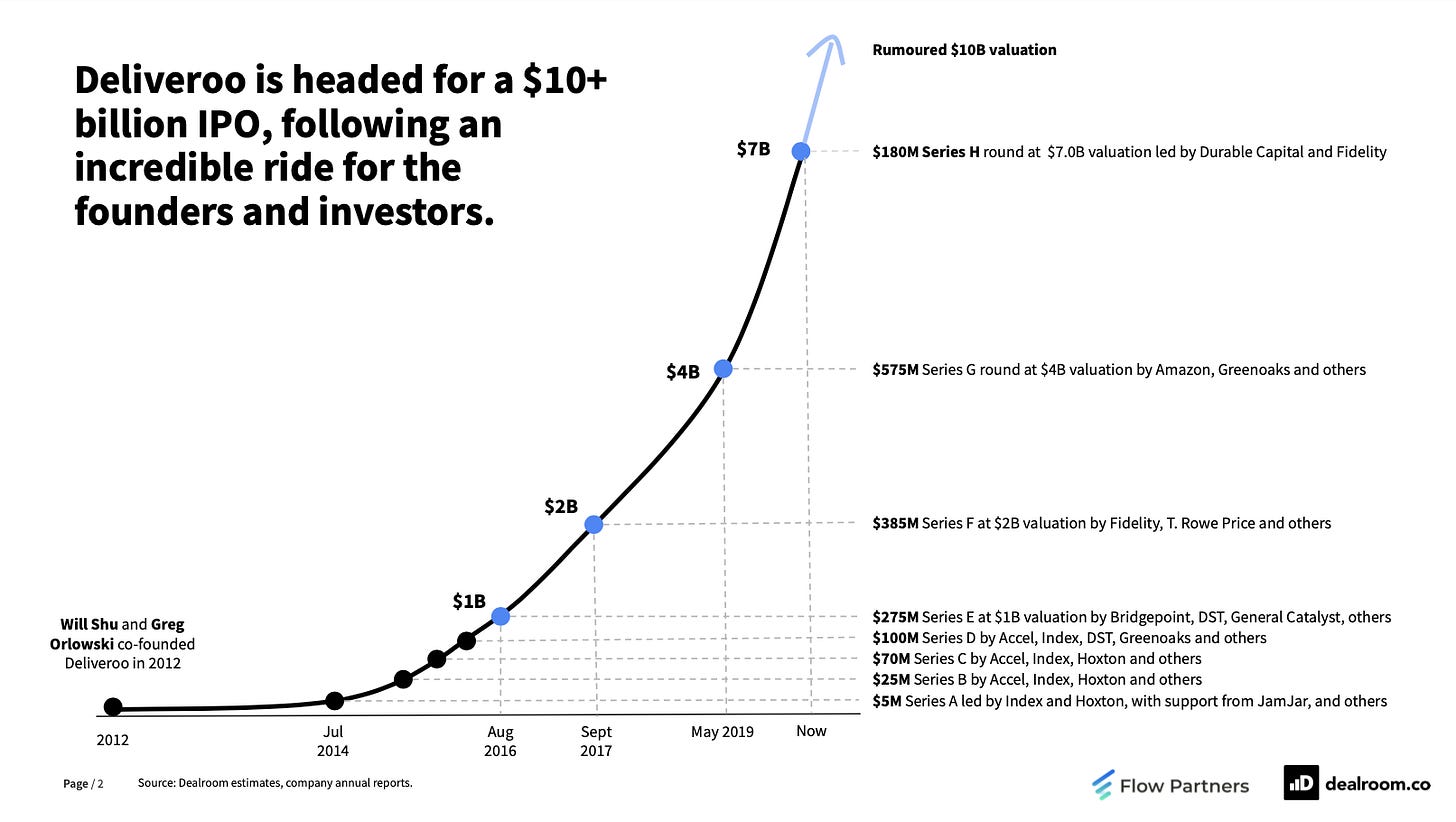

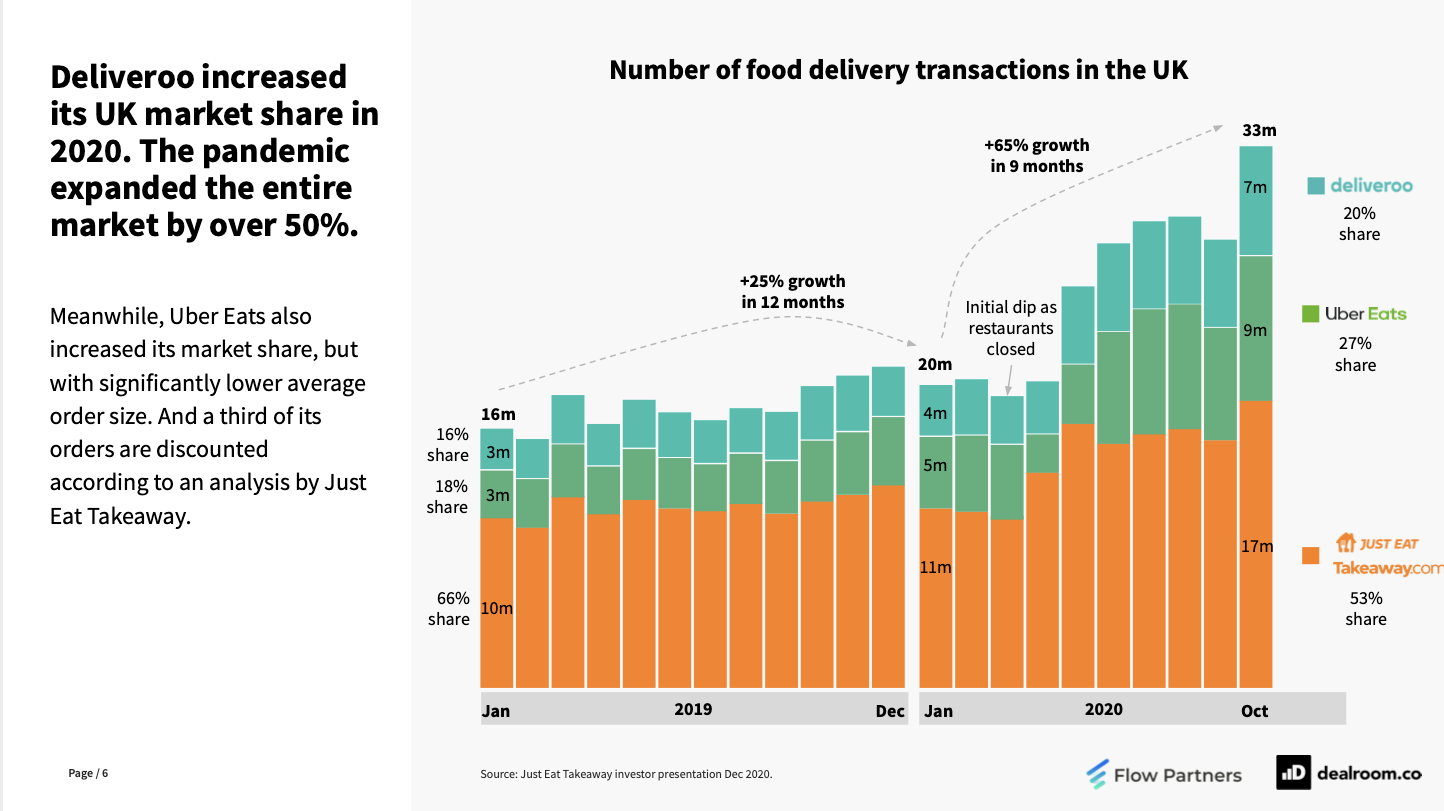

Saturday, Mar. 13th: Dealroom published a report on the upcoming Deliveroo's IPO with interesting slides on the European venture ecosystem, the food delivery market and on Deliveroo. - Dealroom

Deliveroo was founded in 2012, raised a $180m series H in Feb. 2021 at a $7bn valuation and is rumoured to target a $10bn valuation for its IPO.

I love the below graph which illustrates the feeling I have that startups valuation are increasing at a path that is really exponential after reaching the $1bn valuation threshold. For an early stage investor, it means that you must keep your stake in a company for as long as possible to benefit from this later stage value creation.

In 2020, Deliveroo increased its market share in the U.K. (from 16% market share to 20%) compared with JustEat and UberEats but remained the 3rd player.

Sunday, Mar. 14th: I read a paper from Bessemer on their lessons learned from investing in 30+ vertical SaaS in the past decade (inc. Shopify, Toast, Procore and Mambu). - Bessemer

You should aim for global leadership when you build a vertical SaaS and there are three main ways to reach success:

Addressing a new or underserved market: entering a market that does not have a good access to software. As a bonus, you can gain a strong momentum if you are also riding a technological, regulatory, or demographic catalyst.

Unseating sleepy incumbents: disrupting an incumbent with a superior value proposition (better technology, better business model).

Replacing a custom-built system: replacing customized on-premise solutions with a radically superior value proposition.

Best vertical SaaS are able to generate more revenues from their customer base by launching new products. You should always be thinking about your next act: talk with your customers, look at their tech stack, study other verticals, draw inspiration from the competition, etc.

Adding financial services to your core offering could radically expand your total addressable market (consumer payment processing, business payment processing, payroll, card issuing, lending, communication, managed services etc.).

Monday, Mar. 15th: Airtable raised a $270m series E led by Greenoaks with the participation from WndrCo and existing investors CRV, Caffeinated and CRV at a $5.8bn valuation (2x its last valuation mark back in Sep. 2020). Airtable is a mix between a spreadsheet and relational database which is much more flexible than Excel and Googlesheet when you are dealing with non quantitative data. I use Airtable on a daily basis to manage my dealflow, to screen startups, to track my book readings but also to run Appfuel's backoffice. It's a super horizontal product that has become a standard in the no-code community and that has put emphasis over the past 12 months of building an ecosystem of apps to make its database even more powerful. - Techcrunch, Forbes

Tuesday, Mar. 16th: The IFPI released its annual report on the music industry with great charts. - IFPI

The global recorded music grew by 7.4% in 2020 mainly driven by the rise of subscription streaming revenues (+18.5% YoY growth). It's the sixth consecutive year that this market grows.

I guess that I'm getting old as I don't know half of the top albums and singles released in 2020.

Wednesday, Mar. 17th: The venture world is going upside down. P9 the best European seed fund is now doing series A when most multi-stage funds are turning to seed rounds. In February, P9 participated in the $7.3m Cloudtalk's series A (a smart cloud-based phone software for businesses designed to enhance customer experience and performance) and in March, P9 invested in the $12m Whereby's series A (a video conference software). I guess that it's a great proof that that all deals in venture are exceptions. You must be willing to go outside your comfort zone if you want to generate exceptional returns. 🤷♂️ - Techcrunch, Nordic9, Christoph Janz

Thursday, Mar. 18th: Spotify released a new website called Loud&Clear to bring more clarity to artists on the economics of music streaming. Spotify shows the long tail in the music streaming industry: (i) 1.2m artists have more than 1k listeners on the platform, (ii) 185k artists are generating more than $1k in royalties, (iii) 7.8k artists generated more than $100k in royalties, and (iv) 870 artists generated more than $1m in royalties. Spotify paid $5bn to right holders in 2020 (vs. $3.3bn in 2017) and accounted for more than 20% of recorded music revenues (vs. 15% in 2017). - Loud&Clear, The Verge

Friday, Mar. 19th: I listened to a 20VC's podcast episode with Spotify's CEO and founder Daniel Ek. - 20VC

Daniel Ek is the founder and CEO of Spotify (music streaming subscription service with 345m listeners and 155m subscribers in 170 countries).

Daniel had 2 hobbies growing up in the suburbs of Stockholm: music and technology. He learnt how to use Photoshop and HTML to build websites for companies.

As an entrepreneur, you should more focused on the journey than on the destination to move forward (process vs. outcome).

His way to approach problem and delegation of problem solving is to understand:

If we are dealing with a high variance (lot of upside and downside -> new product that can change the face of the company) or a low variance problem (limited upside if you figure it out and lot of downside otherwise -> paying salaries).

If it's a one way door or a two ways door problem meaning to understand whether the solution is reversible or not. It influences the work you need to put ahead before choosing solution.

The CEO’s job is to maximise his leverage on the organisation. Pick a given problem, help to solve the problem and then move on to the next problem.

When you can argue both side of the problem you truly understand the problem. It's the best way to find a solution.

To learn about something, it’s a combination of reading and talking to people. At first, when you talk to people, you understand nothing but overtime, you start to grasp concepts. You start to understand a topic when you can be conversational about it.

How to hire incredible people when you don't know what is world class in a certain role? You should think about the actions to be done in the role beyond the current stage of the company. It changes a lot between organizations and between stages in the life of the company. You should figure out what success means for the role in 1-2y and to work backwards to determine the skills and experience needed.

It's key to have culture of trust and transparency. A transparency culture is important so that people take the best decisions. It's key to educate people on decision making. Don't just focus on the outcomes but focus on the inputs and the process to take decisions. Spotify is building a failure tolerant organisation. Spotify accepts failure but does not accept knowing that you are failing and don't telling it to the org. When you tell that you are failing, you should have a plan to correct the failure and share to the organisation the learnings failure.

It's important to create an environment where individuals should feel safe to share their failures and where failures are seen as a way to improve the organization.

How to transition from being a founder to becoming a CEO? Most founders are not always the best CEO. People are not always good in the 0 to 1, the 1 to 100 and the 100 to infinite phases. This transition should be taken seriously and founders will have to learn new skills (management, leadership, recruiting, etc.). You should be a CEO because you like the underlying tasks and not because anyone tells you to do it.

Saturday, Mar. 20th: Stripe raised a $600m round at a $95bn valuation (3x the valuation of the last round in April 2020 which was valuing Stripe at $36bn). Investors include Allianz X, Axa, Baillie Gifford, Fidelity, Sequoia and Ireland’s National Treasury Management Agency. It's an unstoppable company. Patrick said in an interview: "I think that Stripe is still early in its journey to unlock all sorts of entrepreneurship and economic activity that wouldn't otherwise have occurred." I would call any other company valued over $50bn a liar but I believe in Stripe. The company will use the funding to expand its European operations and double down on product development. - Noah Smith, CNBC, Stripe, Crunchbase

Sunday Mar. 21st: I read a long form interview from Nicolas Colin with Pascal Levy-Garboua. He was an early employee at Checkr (VP of Business Development) and he is a great business angel. - Part I, Part II

The best liquidity option for a startup is to go public. The second best option is to get acquired not by a blue chip company but by another tech startup. In the latter case, if you are paid in equity, there is a lot of upside that can be generated over time. Interestingly, Pascal views this exact option as a great outcome for business angels. Not all startups can reach a unicorn valuation but as business angel, you could also generate great return if a portfolio company is quickly acquired by a larger tech company. "Seeing a portfolio company being acquired by the likes of DoorDash, Square, or Stripe is a great opportunity because those acquirers still have a long runway for further growth, and they excel at making your capital compound".

Pascal shared his opinion on what it takes to be a successful business angel. He has a quantitative approach. He picks 15-20 companies per year that have the potential to become unicorns. He makes a parallel with Keith Rabois's strategy at Khosla to invest in 10 companies in every YC batch. "For me, the idea is that you should have enough opportunities so as to maximize the probability of having one or two unicorns a year. [...] So if you have a good deal flow and if you invest in a systematic way, then yes, you need to do 1-2 investments a month—that is, 15 to 20 a year."

In France, even if a business angel sees all the best deals it's not obvious that the market is deep enough to generate 1-2 unicorns per year out of 15-20 investments.

Pascal also noted an interesting difference between European and American founders: "What we see in Europe is people with exceptional backgrounds, the European equivalent of an Ivy League education, who pursue opportunities on markets that are not that big—typically various verticals in the SaaS industry, such as designing a SaaS tool for chiropractors, hair salons, or contractors in the construction industry. In the US, people with a similar background will go after much bigger opportunities. They won’t let themselves be confined to a narrow vertical. Instead, they will focus on a deeper technological layer, which represents a much bigger opportunity."

Monday, Mar. 22nd: Cubyn raised a €35m funding round co-led by Eurazeo (💙) and BPI Large Venture with the participation of existing investors. 18m ago, Cubyn did a pivot to launch a vertically integrated fulfilment offering that has skyrocketed in 2020 with a GMV going from €30m in 2019 to €250m in 2020. Cubyn also signed great marketplace customers including Rakuten, Mirakl, Backmarket and Fnac. The funding will be used to expand this fulfilment offering all over Europe starting with a new warehouse to cover Portugal and Spain. Cubyn is another bet that we are proud to make to reinvent the ecommerce infrastructure stack. - Adrien Fernandez Baca, Techcrunch, Cubyn

Tuesday, Mar. 23rd: Microsoft is in exclusive talks to acquire Discord for $10bn. Discord is a communication platform to chat through voice, text and videos with your friends and communities. Discord ticks all the boxes of a trendy business in 2021: communities, gaming, audio, etc. - VentureBeat, WSJ, Bloomberg

The company started and has become the standard in the gaming space. With covid, it has managed to expand its market to become an alternative to Slack for many companies.

It makes sense for Microsoft which has a strong business line in gaming (with the Xbox, Minecraft, gaming studios) and will also integrate Discord in its fight against Slack. Adding a Discord's subscription in the Xbox Game Pass would make a lot of sense like a Twitch's subscription included in Amazon Prime's subscription.

Discord has 145m MAUs, generated $130m in revenues in 2020 (vs. $45m in 2019.) and is stilll not profitable. Discord already explored a sales process back in 2018 but acquirers were reluctant to buy an unprofitable company that was not willing to monetize through advertising.

Wednesday, Mar. 24th: U.S. based instant convenience delivery startup goPuff raised $1.15bn with D1 Capital and Fidelity at an $8.9bn valuation. goPuff has a vertically integrated model with 250+ micro-fullfliment centers and a network of independent drivers to operate deliveries in less than 15 minutes while having great unit economics. The startup is now live in 650 cities in the U.S., is expanding its product line to new categories (healthy snacks, beauty, baby) and has introduced curated mystery boxes. The funding will be used to expand into new cities in North America and over the world as well as to introduce new products. Note that goPuff is aslo coming to Europe and is in talks to acquire a London-based copycat called Fancy. - Techcrunch, GroceryDive, FT

Thursday, Mar. 25th: Index led a seed round in Creative Juice which is building the financial network for the creator economy. It has launched a first product called the Juice Funds which lets creators invest in other creators. MrBeast is joining the Juice Funds and will invest $2m into the next generation of Youtube creators. Overtime, Creative Juice will release other financial tools and products to help creators run their businesses. - Index, Rex Woodbury

Friday, Mar. 26th: Gorillas raised a $290bn series B led by Coatue, DST and Tencent at a $1bn+ valuation. Gorillas is a goPuff's copycat that is now operating 40+ micro fulfilment centers in 12 cities across Germany, the U.K., and Netherlands. The startup is delivering 2k grocery SKUs at retail prices in average time of 10 minutes. Riders are full time employees. Gorillas will use the funding to open new cities and expand its team. - The Spoon, Techcrunch

Saturday, Mar. 27th: Nicolas Brusson (founder & CTO at Blablacar) shared the list of startups founded by Blablacar's alumni which raised €62.3m in total. I have now 135+ startups founded from French startups mafias including 22 startups for Blablacar. - Nicolas Brusson

"Our vision with co-founders Fred and Francis was to instill in our talent the importance of risk-taking and entrepreneurship, from day 1. We wanted BlaBlaCar to serve as a springboard for generations of startups to follow, and to encourage as much sharing and knowledge-building as possible, because that’s what serves a tech ecosystem in the long run."

Sunday, Mar. 28th: I listened to an Invest Like the Best's podcast episode with Todd McKinnon who is the founder and CEO at Okta. Okta is an identity management solution for enterprises founded in 2009 and which has now 7k customers all over the world. - Invest Like the Best

He understood at Salesforce that cloud was going to be a big deal and that cloud will impact every layer of the technology stack. A transition like this one was a perfect environment to start a new company.

He thought about the inevitable shifts that will be required by the cloud (following infrastructure moving to the cloud with AWS, collaboration apps moving to the cloud with Google and business apps moving to the cloud with Salesforce) to work on my new business. Todd started with a solution monitoring cloud applications but it did not take of. On the way, IT people told him that they were struggling with identity management which gave birth to Okta. The first version of the Okta's product made it super easy to log in into your cloud applications with a Windows password.

"Identity management is systems and processes and technologies that identify who users are and what applications they can access, or what computers they can access." Identity management has always existed but today there is an exponential explosion in the number of computers, apps and users which made impossible to have a single identity management solution for each app or each computer. Okta is built as a layer on top of this diversity of computers, apps and users to bring flexibility and ease of use while preserving security.

With Okta, "there's one system that has kind of a meta map of all of the applications that you should access and your one credential that you can use to authenticate yourself. [...] It's really moving from a distributed system to a centralized system that is integrated to all the distributed systems."

Monday, Mar. 29th: Jérémy Uzan and Raffi Kamber announced publicly their new €225m fund called Singular. Both were partners at Paris-based venture fund Alven and decided to leave to create their own fund. Singular will invest all over Europe in seed, series A and series B. It can invest up to €20m in a company and it's a generalist fund. The fund raised capital from investors like OTPP, Bpifrance, Axa, Sofina, MACSF and Mudabala. To maintain its prorata stake in its portfolio companies overtime despite the small size of the fund, Singular will raise special purpose vehicles from its investor base. Singular has already done 6 investments including Gtmbhub (series B, Bulgaria), Indy (series B, France), Soda (series A, Belgium), Moka (seed, France), Resilience (seed, France). It's amazing news for the French ecosystem to have a new super ambitious early stage fund and to have a local fund that has also pan-European ambitions. - Techcrunch

Tuesday, Mar. 30th: Istanbul-based fast delivery grocery startup Getir raised a $300m series C led by Sequoia and Tiger Global. In February, Getir started its geographical expansion opening the London market. Now, the company will expand in the Netherlands, Germany and France. Like goPuff, Getir has been working for several years on the vertically integrated grocery model and will have a strong edge compared to European newcomers to make it work in Europe. - The Spoon

Wednesday, Mar. 31st: Linktree raised a $45m series B co-led by Index and Coautue. Instagram does not allow its users to add links in post captions and you can add only one link in your bio. This constraint has been used by services like Linktree which transforms the single URL in your bio into a simple website with multiple links that you can choose. Linktree has more than 12m users (out of which 4m signed up in the past 3m) and a 88% market share in its category. - Techcrunch

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋