🗞 Venture Chronicles - June 2022

Overlooked #118

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of June.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for June!

Wednesday, Jun. 1st: Growth Capital published a report on the Italian venture ecosystem. - Growth Capital

In 2021, Italian startups raised €1.25bn in 262 funding rounds (inc. 50 series A, 19 series B, 5 series C and 1 series D) compared to €528m raised in 2020 across 179 funding rounds.

BNPL (Buy Now Pay Later) was under the spotlight in Italy: Scalapay reached an unicorn valuation. BNPL is a €1.1bn market in Italy. It has a 3% penetration rate as an ecommerce payment method and is forecasted to grow by 30% in the next 5 years.

Italy also has a local quick commerce player called Macai which raised a €3m pre-seed round in Nov. 22 from Plug&Play, Lumen and Cats.vc.

Thursday, Jun. 2nd: Alex Taussig from Lightspeed wrote a blogpost about the key success factors to launch a B2B wholesale marketplace. - Alex Taussig

"The most challenging aspect of wholesale marketplaces is how you fight disintermediation. If two businesses continually work together, they will have low willingness to pay to a marketplace that connects them."

"Creating a repeatable purchase pattern between two recurring buyers is therefore the main challenge and opportunity for a wholesale marketplace. Extracting a 10-20% take rate is only possible when each transaction has more value than the matching itself."

Several strategies can be implemented to capture transactions between stakeholders who are used to working together: (i) remove risk (e.g. Faire's offering free returns on new brand orders), (ii) provide logistics (reliable logistics at a scale that an individual participant in the marketplace will never reach), (iii) give away a free vertical SaaS to one side of the marketplace.

Increasing buyers' share of wallet should be the north-star of any wholesale marketplace. It's the equivalent of net dollar retention for SaaS businesses. Usually, wholesale marketplaces will start with a high purchase frequency, low margin SKU before expanding into less frequent but higher margin purchases.

Friday, Jun. 3rd: I listened to a Colossus' podcast episode about investing and current market conditions with Aswath Damodaran who is a finance teacher at NYU. - Colossus

Expected inflation is priced in financial assets. Unexpected inflation is the delta between current inflation and expected inflation. Unexpected inflation is dangerous because investors have not priced it. Today, we have unexpected inflation because most investors entered the market in the past 20 years and they have only worked in a low and stable inflation environment.

When inflation is high, it becomes extremely volatile and therefore uncertain which will kill most long term investments.

When you have inflation, non-discretionary companies have the pricing power to pass inflation into price increases to their end customers which is not the case for discretionary companies. Many modern products like a Netflix's subscription or an Iphone that you upgrade every 2 years have been created into a low inflation environment and we don't really know if they are discretionary or non-discretionary.

"In the last decade, Microsoft has shifted away from a software upgrade business to a subscription business. Subscription businesses by their very nature tend to be less discretionary. For whatever reason, people are far less likely to cancel a subscription than they are to just not upgrade"

Companies well positioned against inflation have the following characteristics: (i) non discretionary, (ii) dependent on subscriptions, (iii) flexible cost structures and (iv) dependent on short term and reversible investments. Tech companies tick more of these characteristics than other companies.

"I described Amazon now as a disruption machine. It's not an online retailer, it's not a logistics company, it's a company that basically targets any business which has softness in it and goes after the status quo, which means everybody's fair game. And they have an army every time they want to disrupt a business, that army is called Amazon Prime."

Saturday, Jun. 4th: Alven raised a €350m Fund VI to back European entrepreneurs in seed and series A with tickets between €100k and €15m. Alven invests predominantly in France but plans to become more pan-European with this new fund. It had already opened an office in London. Alven has an internal People Operations team to support founders on recruitment. It's one of the most successful VCs in France having invested into companies like Qonto, Dataiku, Algolia or Ankorstore. - Alven, Techcrunch

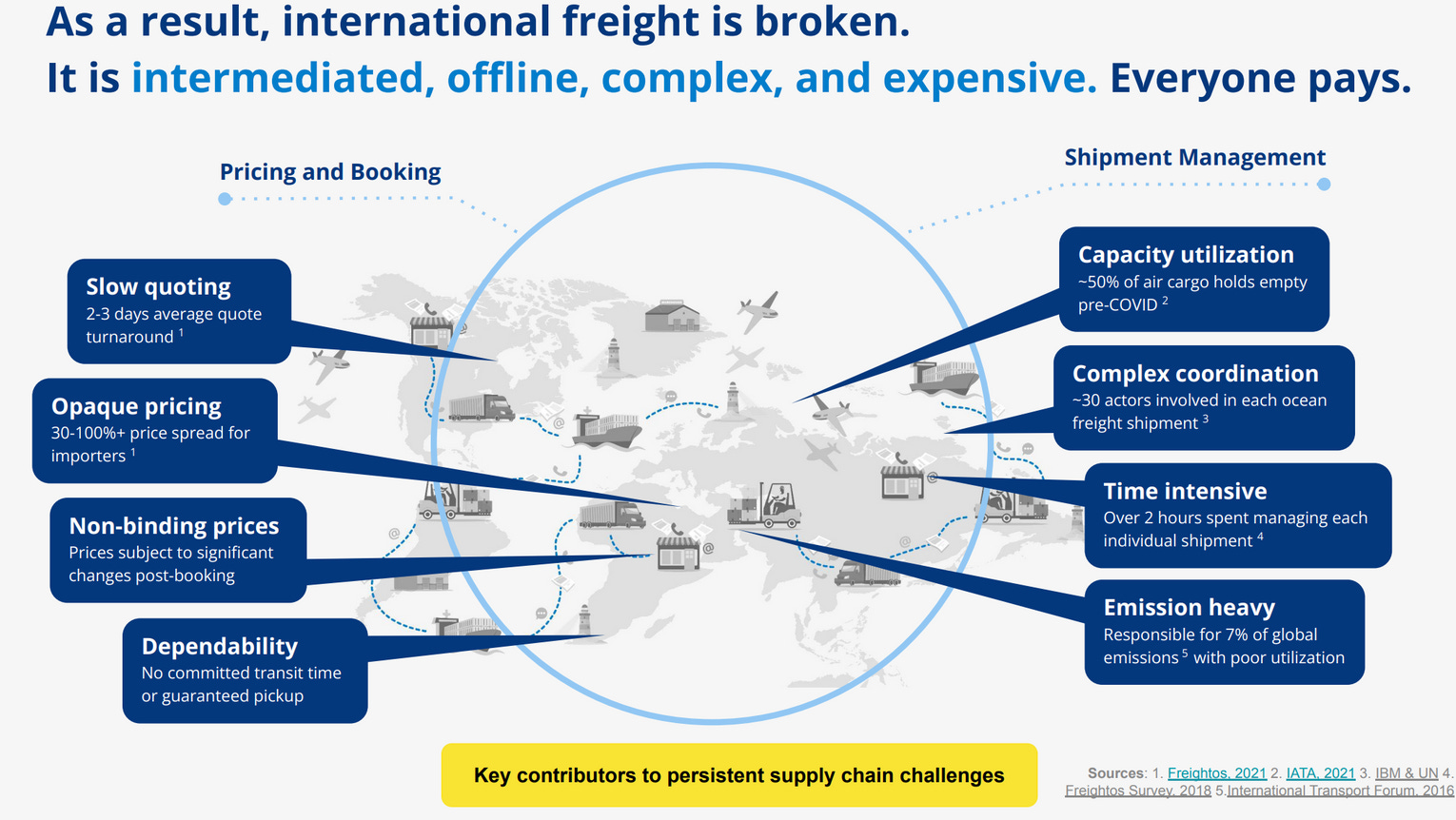

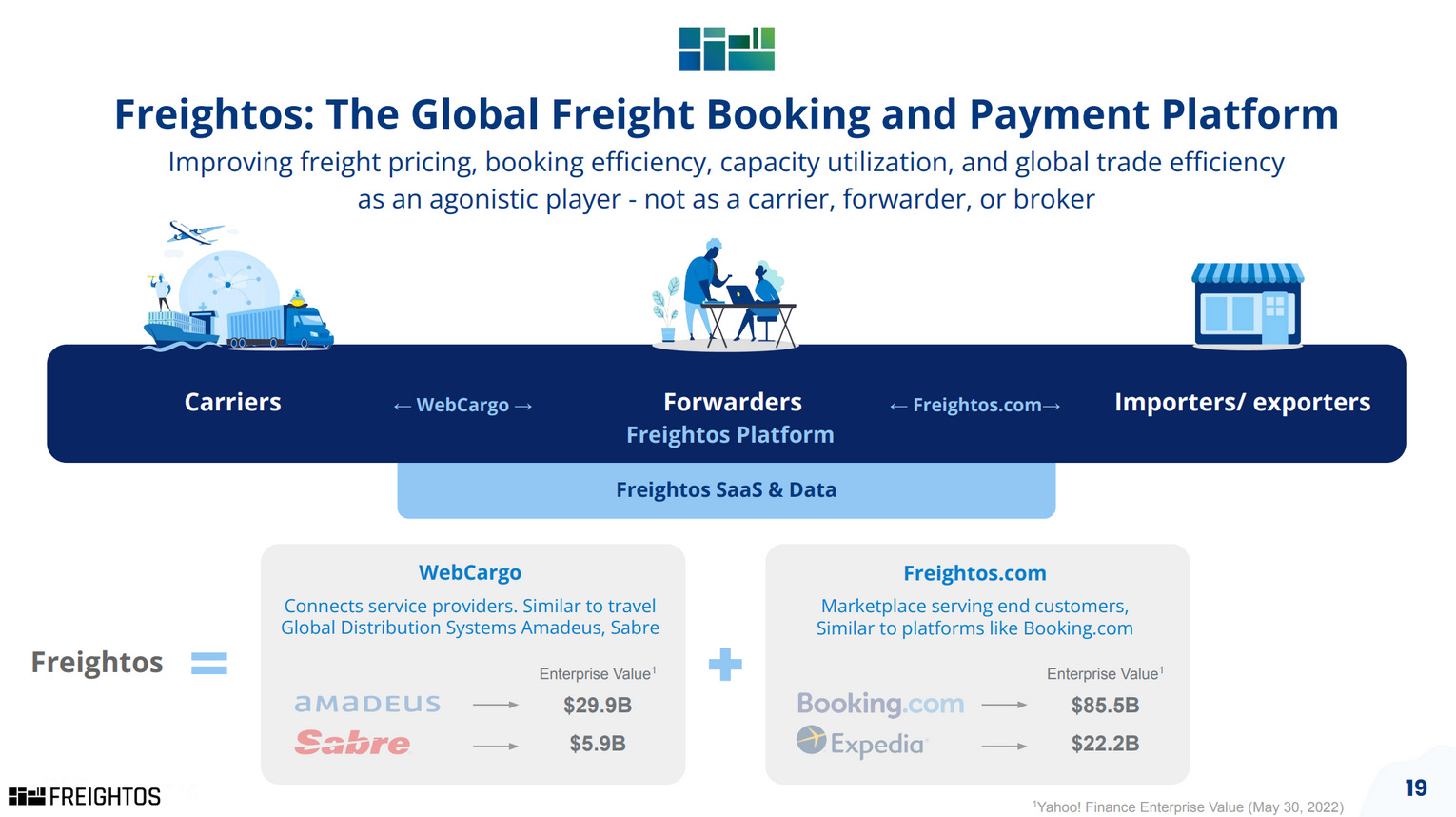

Sunday, Jun. 5th: Israël-based freight-forwarding platform specialised in air and ocean shipping Freightos is going public via a SPAC to raise a minimum of $80m at a $435m entreprise value. Freightos is "a Booking.com for the travel of goods". - Freightos I, Freightos II

Freightos previously raised from corporate investors like Fedex, Qatar Airways, IAG and Latam Airlines Group.

It works with 10k importers/exporters, 3.5k forwarders and 200 carriers. Contrary to Flexport which is also a freight forwarder, Freightos has a vendor neutral platform without misaligned interests with stakeholders on its marketplace.

In 2022, it will generate $2bn in GMV. It has a 60% gross margin level on its take rate

Carriers (airlines and ocean liners) only started providing APIs for instant price quoting, capacity availability, booking and tracking after 2019.

Freightos was started in 2012. It previously raised $120m and has a team of 330 people. It has two main products: WebCargo which is a GDS for freight forwarding between carriers and forwarders and Freightos which is a marketplace for importers/exporters needing to book freight.

Freight forwarding is a broken industry: 2-3 days to get a quote, opaque and non binding pricing, complex coordination with 30+ actors involved in each ocean freight shipment, etc.

Freightos monetizes via a take-rate on its freight forwarding marketplace and a SaaS platform sold to freight forwarders to price and book air cargo space from airlines. In the long-term, Freightos believes that it can reach a 10% take-rate.

Monday, Jun. 6th: Forbes interviewed Stripe's cofounders - Patrick Collison and John Collison. - Forbes

In 2021, Stripe processed $640bn in payments. It generated $12bn in gross revenues and $2.5bn in net revenues. Stripe is also EBITDA positive. It raised $2.4bn in total including a $600m round led by Fidelity and Ireland's sovereign fund in Mar. 21 valuing Stripe at $95bn.

Stripe is expanding into new geographies like Southeast Asia and Middle East. It launches products adjacent to finance like crypto products (also rumoured to explore accounting) and goes deeper into financial services (credit cards issuing, loans to SMBs).

In 2010, Michael Moritz led Stripe's seed round for Sequoia together with angels like Max Levchin, Peter Thiel and Elon Musk. Sequoia also led Stripe's series A in 2012.

Stripe's founders were famous at YC for “the Collison installation”. Instead of sending an email or a Slack message to ask other startups to start using their product, the brothers would pitch the product to their peers and set up straight away Stripe on their computer.

Tuesday, Jun. 7th: Felt raised a $15m series A led by Footwork. Felt is a tool to create and share interactive maps on the internet. Felt enriches maps with 50+ data layers (e.g. bicycle lanes, timezones, etc.) and offers drawing tools to personalize maps. - Felt, Techcrunch, NBT

"When we founded Felt, we set off to do what Google did for Docs, and what Figma did for design. We believe anyone, anywhere should be able to create and share a map on the internet."

It enables "anyone to create a map, working with datasets that can be overlayed on maps, with easy sharing and real-time collaboration built into the platform."

Besides the team, Footwork invested into Felt for two main reasons (i) mapping software is an enormous opportunities as using maps is critical in many industries (education, agriculture, construction, media, government) and (ii) Felt's product has built-in network effects which can create a strong competitive advantage in the long-term.

Wednesday, Jun. 8th: The Economist wrote about the potential shape of the upcoming recession in the US. - The Economist

Instead of trying to find parallel between the current situation and precedent downturns, we should study the current state of the US economy (real economy, financial system & central bank) which suggests that we should have a relatively mild recession.

For households: household debt is 75% of GDP (vs. 100% in the global financial crisis), 9% of income is used to service debt (low thanks to the low interest rates environment), $2tn added in savings during the covid crisis (spendings reduced & stimulus payments).

For banks: more liquidity and stronger balance sheets thanks to Basel 3 capital standards.

Non banks lenders issued 70% of all mortgages vs. 30% one decade ago.

"The Fed is embarking on a journey with a clear destination (low inflation), an obvious vehicle (interest rates) but hazy guesses about how to get there (how high rates must go). It will know the correct path only by moving forward and seeing how the economy reacts."

"Given the strengths of the economy today—flush consumers, solid businesses and safe banks—the next downturn ought to be mild. But even a mild recession must be followed by an upturn for the economy to return to full health. And with fiscal policy on the sidelines and monetary policy badly hobbled, the chances are that America would face a painfully slow recovery. After two years of focusing on high inflation, low growth may move back to centre-stage as the economy’s principal problem."

Thursday, Jun. 9th: I love SaaStr Fund's presentation. It's a $100m fund to invest in seed and late seed stage SaaS companies. It invested in companies like Talkdesk, Gorgias, Front, Intercom, Pipedrive, Algolia, Revenue Cat, Sqreen or Salesloft. "Our investments are at 15x+ over history, and 5/6 of our first seed investments become unicorns and decacorns." - SaaStr

Investment Criterias:

"SaaStr Fund invests in 4-5 awesome SaaS start-ups a year, generally in the $0.1m to $2m ARR range. Before $10k MRR is usually a bit too early for us, and after $2m ARR or so is usually a bit late and Series A."

"We prefer Outsiders + Outliers. Folks that didn’t go to those schools, or worked at that hot tech company. The ones that did it on their own, that earned it, and got to 10+ unaffiliated customers on their own."

"Pre-revenue is too early. We can only invest if you have at least 10 unaffiliated customers, and ideally, $10k+ or more in MRR."

Supporting Portfolio Companies:

"Find your next round investor for you (assuming you deliver the results). If you hit your numbers, we will get you funded."

"Find, attract and help build your first management team, especially VP of Sales and Marketing"

"Be your mentor and advisor forever. This is half the fun. Then, the day comes when you know more about SaaS that we do, and that’s a good day."

Friday, Jun. 10th: I watched Apple's 2022 WWDC. - Apple

iOS16

New version of the lock screen. You can make it more personal with the possibility to edit your picture, the font and the colours. You can add widgets. You can switch between pre-defined lock-screens. Apple also added a "live activities" section to the lock screen so that users can follow things happening in real-time directly from the home screen (e.g. running, listening to music, following your Uber driver)

New version of focus. You can pair a moment in the day with a given lock-screen. Focus is going deeper into what you can filter (e.g. websites, emails, content within applications).

Shareplay is being upgraded. It allows users on Facetime to share experiences like watching a series or listening to music. With this new upgrade, Shareplay will be more apparent on Facetime and will be also available on iMessages.

In certain US States, you can digitize your ID card into Apple Wallet. You can use it for security checks and to make your KYC for certain apps.

On Apple Pay, Apple is launching Tap to Pay in the US to enable merchants to accept contactless payments on iPhone without additional hardware or payment terminal. Apple is also launching a BNPL offering called Apple Pay Later to split a purchase into 4 equal payments spread over 6 weeks. It will be available everywhere Apple Pay is accepted in apps and online. For developers and applications, no additional integration is needed as long as you have ApplePay.

Home & Car

Apple is joining other industry leaders (e.g. Google, Philips, Netatmo, Schneider, Legrand) to work on a smart home connectivity standard called Matter which enables smart home accessories to work together across platforms.

CarPlay is available in 98% of cars in the US. CarPlay is being more integrated with your car. In some cases, you will be able to turn on the radio or change the temperature of your car without leaving CarPlay. The long term vision for CarPlay is to power the entire instrument cluster of cars.

WatchOS & Health

Apple is releasing 3 additional metrics to track how you run thanks to your Apple Watch in the Workout app: vertical oscillation (a measure of how much you move up and down), stride length and ground contact time.

On iOS 16, the Fitness app will be available to all iPhone users and not only Apple Watch users.

A Medication app is launched on the Watch to track your medications. You can set-up reminders. You can see if there are interactions between several drugs that you're taking.

Mac

M2 will be launched. It's the second generation of chip designed by Apple specifically for the Mac. It's focused on power efficiency to increase performance while maintaining low energy consumption.

A new Macbook Air powered by M2 will be released. 18-hour battery life. $1,199 as starting price. 1.24 kg and and 1.13 cm thin.

Saturday, Jun. 11th: I read a report from The Economist on a potential upcoming global food crisis. - The Economist I, The Economist II

The Ukraine war is putting at risk a global food system that was already weakened by several factors (covid 19, climate change, energy shock).

The war is impacting the Ukrainian food production (e.g. Russian army destroying grain elevators or fertiliser plants) and export system (e.g. Odessa's ports which are usually responsible for 98% of grain exports are blockaded). In April, Ukraine exported only 1.1m tonnes of grain compared to 5m usually.

"In 2021 Russia and Ukraine were the world’s first and fifth biggest exporters of wheat, shipping 39m tonnes and 17m tonnes respectively—28% of the world market."

"According to the UN's Food and Agriculture Organisation (FAO) nearly 50 countries depend on either Russia or Ukraine, or both, for more than 30% of their wheat imports; for 26 of them the figure is over 50%."

"The countries hit worst, though, are poor ones, because its population spend a greater share of their income on food." In emerging countries, people spend up to 25% of their budgets on food (40% in Subsaharan Africa) and governments cannot afford to subsidise food purchases (high debt burdens).

26 countries are implementing restrictions on food exports. It's dramatic because our food system is extremely dependent on global trade with 80% of the population living in countries that are net food importers.

Sunday, Jun. 12th: The Economist wrote about the world's supply chain reshuffling. - The Economist

Globalisation is being challenged by events such as the trade war between the US and China, the covid crisis and the war in Ukraine. It impacts the supply chain that is becoming more decentralised, more redundant and even renationalised on certain activities judged as strategic.

In certain industries, Europe and the US have become dependent to autocratic countries like China (chemicals, electronics, textiles) or Russia (gas, food).

Companies have several options to adjust to this new reality: (i) vertical integration, (ii) diversifying the supplier base, (iii) reshoring certain activities, (iv) secure inventory.

"The world economy could become less vulnerable to shocks at a time when climate change and geopolitical tensions are increasing their frequency and intensity"

Monday, Jun. 13th: Entrepreneur First (EF) raised a $158m series C with investors including founders like Patrick & John Collison (Stripe), Tom Blomfield (Monzo), Taavet Hinrikus (Wise) or Reid Hoffman (Linkedin). EF started 10 years ago. It’s a great innovation in venture capital. EF creates cohorts of strong talents who will work together for 6 months to test potential founders collaborations and startup ideas. 600+ companies have been created via EF. 450 are still alive (e.g. Tractable, Omnipresent or Cleo) and are collectively worth more than $10bn. EF’s founders are 27 years old on average, have a solid previous work experience but are still full of the youth needed to not be jaded and are ambitious enough to build a company from scratch. EF runs 2 cohorts per year in 6 locations (London, Paris, Berlin, Singapore, Bangalore and Toronto). - Sifted,

Tuesday, Jun. 14th: Pave raised a $100m series C led by Index with the participation of a16z, YC, LocalGlobe, Craft and Contrary Capital. It also acquired a company called Advanced HR from Morgan Stanley which has compensation products like Option Impact, Option Driver and the Venture Capital Executive Compensation Survey. Pave is a real-time compensation benchmark SaaS. It allows employers and employees to have data-backed conversations about compensations leveraging Pave’s compensation benchmarking database. It started in 2019. Today, it has 150 employees and 2.5k customers. Pave is interconnected with many ATS (Lever), HRIS (ADP, BambooHR, Workday) and equity management tools (Carta, Ledgy). Pave will use the funding to expand in Europe. - PR Newswire, Pave

Wednesday, Jun. 15th: Michael Wolfe (cofounder at Gladly and portfolio advisor at P9) wrote about the importance for startups of having a great cadence to run their business. - Michael Wolfe

Execution pace is a key success factor for startups. It’s not only about working hard at an individual level. It’s also about coordinating an organisation to maximise the global output of the team.

“The cadence of a company is the set of habits and practices that it repeats on a set timeframe — daily, weekly, monthly, or quarterly.”

To cadence execution, startups implement weekly routines (weekly executive team meetings, weekly team meetings, one-on-ones, weekly all hands meeting) which are coordinated with longer timeframe planning (quarterly or monthly planning).

It’s key to stay consistent (don’t skip routine meetings) and to constantly improve your cadencing.

Thursday, Jun. 16th: Rui Ma wrote about Shein. - Rest of World

Shein cracked “the perfect production scenario, where a company can 1) quickly onboard lots of new styles at 2) low prices, while 3) being hyper-efficient in managing massive volumes of inventory.”

Shein focused on building a supply network instantly able to adapt to demand changes when traditional fashion retailers’ core capability was more around sales & marketing.

Shein developed a Manufacturing Execution System for its manufacturers in which it manages the production process end-to-end from design selection to sampling and full scale manufacturing. It’s a system of record in which everything is tracked (materials, prices, quantities, chat logs between Shein and manufacturers).

It has extremely strict deadlines for its manufacturers: maximum 3 days to send a sample to Shein and 9 days for reorders. Knowing that it takes at least 8 business days to ship in the Western world, it means that it will take about 1 month between design and arrival in the US.

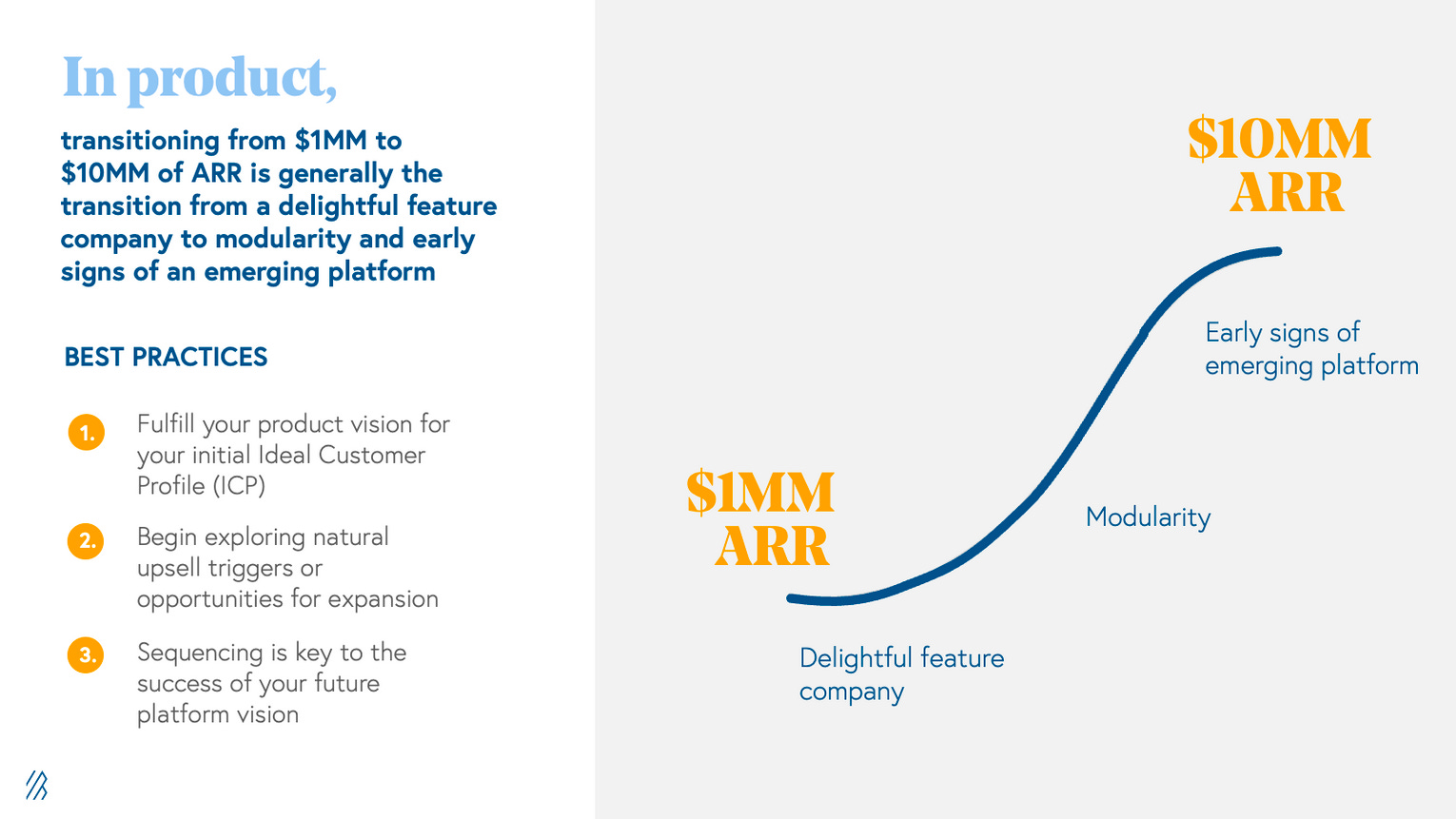

Friday, Jun. 17th: Bessemer shared a good framework with best practices on scaling a SaaS company from $1m to $10m ARR. - Bessemer

Saturday, Jun. 18th: Fred Wilson (GP at USV) wrote a great post on why a small partnership is the best model in early-stage investing to produce consistently top-decile returns. - Fred Wilson

“A real partnership is where everyone is equal, not just in terms of economics (which is critical to sustaining this model), but also in terms of influence and stature.”

“At the early stage, investors must bet on teams and ideas that have not been proven. The biggest winners almost always come from the investments that are the most controversial and “out there”. A small tight partnership where there is a lot of trust between the partners is a place where you can make a lot of these kinds of investments.”

“It is very hard to make an investment that will produce over a billion of proceeds. You need to get and keep double digit ownership and the company needs to be worth over $10bn at exit. […] I think a quarter billion is probably where it starts getting really hard to produce a high return on capital fund. This means you need a small partnership and a small firm.”

Sunday, Jun. 19th: Europe has a new VC fund founded and led by former entrepreneurs. It’s a $250m fund called Plural led 4 partners: Taavet Hinrikus (Wise), Sten Tamkivi (Teleport), Ian Hogarth (Songkick), Khaled Helioui (Bigpoint). It will invest in early stage companies (up to $10m tickets). Each partner will make 4-5 deals per year. Plural has already invested into 14 companies including Feather, NFT Port, Field, Ready Player Me and MOS. - Techcrunch

“We’re the investors we would have liked to have when we were building our own companies. Founding a company is a craft and the best way to learn that craft is to work alongside those who have done it before.”

“We call experienced founders ‘unemployables,’ because once you’ve experienced the intense authorship that comes with creating something new it’s hard to work for anyone again. We created Plural to give unemployables a place to call home and put their entrepreneurial energy behind missions and founders they deeply believe in.”

“The only VCs are all spreadsheet junkies, bankers, consultants, they have no idea what it means to run a company, how to build a company. So that’s the problem we’re solving. We’re building an investment platform, where all the GPs are former founders. And we’re going to scale this to a large number, an irresistible army of ‘unemployables’, who will be your side when you’re building your company”

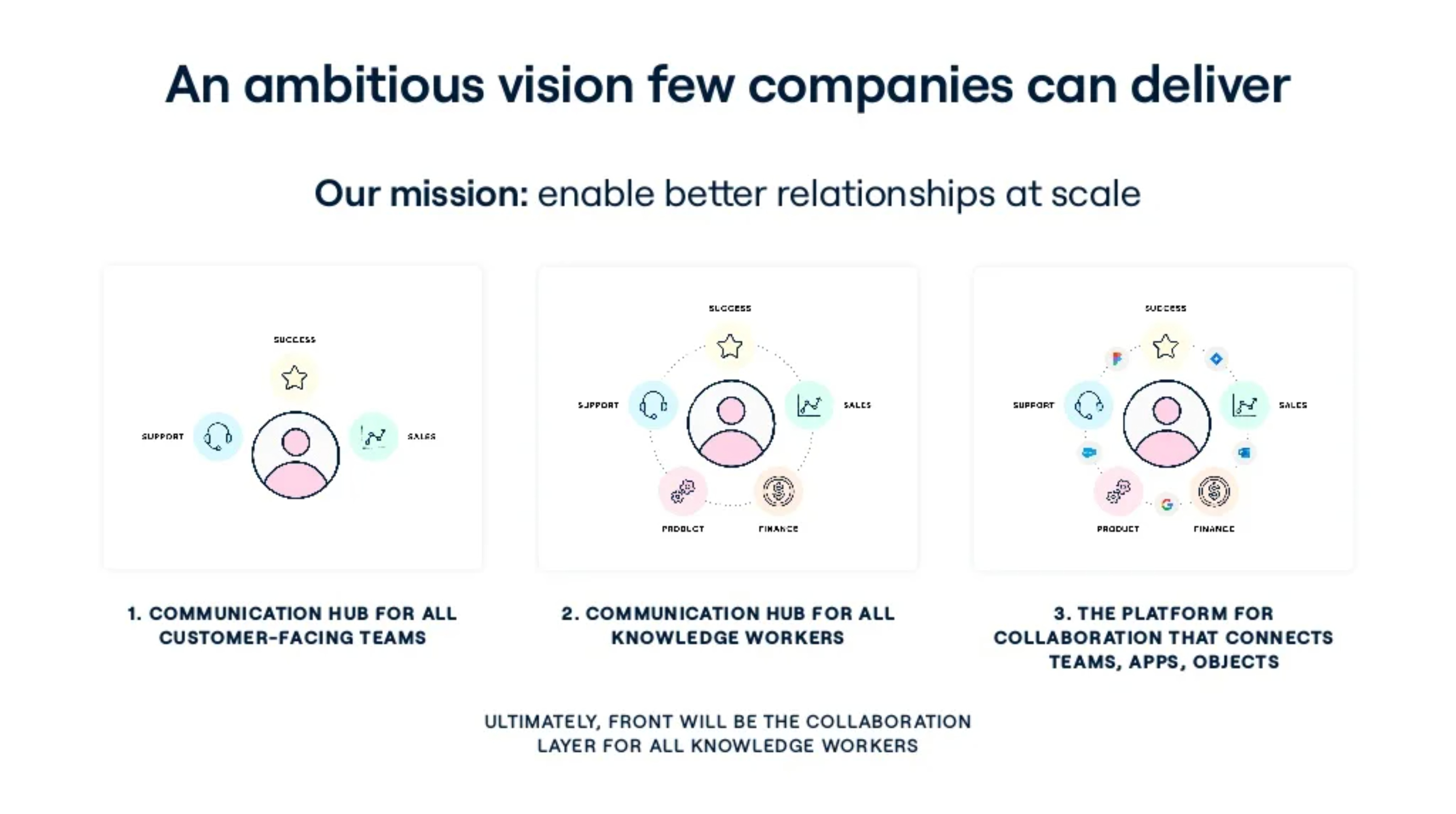

Monday, Jun. 20th: Front raised a $65m series D valuing the company at $1.7bn led by Salesforce with the participation of Battery and of existing investors Sequoia and Uncork. Front was started by Paris-based startup studio eFounders. It’s a customer communication SaaS. It has 8k customers including Shopify, Airbnb and Lyft in 100 countries. - Front 1, Bloomberg, Front 2

“My goal is to push more women over the edge to take risks, believe in themselves, and pursue every idea they want to grow.”

“[To raise a round], it's important to have achieved a significant milestone and have your sights on the next milestone you intend to reach with the additional funding.” (e.g. series A: have proof of product market fit with a $1m ARR)

Tuesday, Jun. 21st: Paris-based Stoik raised a €11m series A led by a16z. It previously raised a €3m seed round co-led by Anthemis and Alven. Stoik will use the funding to strengthen the team and expand into new European markets. - Tech.eu

Stoik is a cyber-insurance product for SMBs distributed via brokers and putting technology at each step of the customer journey (a scan to evaluate vulnerabilities, a specific underwriting process, a CRM for brokers, etc.).

It’s a16z fourth in France in less than 18 months after Bereal (series A), Rtftk (seed, sold to Nike) and Angle (seed).

Wednesday, Jun. 22nd: Erez Druk built a framework to think about Product Market Fit (PMF). - Erez Druk

PMF is neither binary (you have it or you don’t have it) nor a spectrum (iterating slowly towards it).

There are 3 situations when you’re evaluating your PMF: (i) PMF desert (nothing works consistently, zero PMF → make bold moves to walk away from the desert), (ii) PMF mountain (something objective is starting to click even if small → listen to your users and iterate quickly to grow your PMF), (iii) PMG mountain peak (you created something valuable → time to replicate it cheaply and quickly).

Thursday, Jun. 23rd: The Generalist wrote a deep-dive Union Square Ventures. - The Generalist

“We made a fortune and we lost it in the blink of an eye” said Fred Wilson about the dot-com crash that killed its previous fund before USV called Flatiron. Fred spent 2 years “licking his wounds and internalizing the lessons” learnt during this market crash before starting USV.

It took Fred Wilson and Brad Burnham 18 months to raise USV’s initial fund. It was a $125m fund raised in 2004.

USV’s funds have consistently achieved excellent returns - always 1st quartile and always over 5x returns. Its 1st fund returned 14x of the invested capital with companies like Zynga, Twitter (USV led a $5m series A and took a 33% stake into the company), Tumblr, Indeed and Etsy.

USV is thesis driven. It develops a broad investment thesis in which investors invest and build expertise on.

USV has a strong timing sense both to identity new market trends before anybody else (e.g. social media and crypto) or to exit portfolio companies at a favourable timing (rule to liquidate 10-30% of the ownership in pre-IPO round, ability to sell Tumblr and Zynga before the decline of these companies on the public stock exchange).

Friday, Jun. 24th: Morgan Stanley (MS) published a broker note on the on-demand grocery sector (grocery delivery in less than 30 minutes) which is entering into a consolidation phase due to the current market turmoil.

MS makes distinction between 1st party model (vertically integrated with dark stores, GoPuff/Gorillas/Getir) and 3rd party model (partnership with grocery stores, Deliveroo/DeliveryHero/DoorDash). The 1P model can have better unit economics at scale (4% EBITDA margin on sales) than the 3P one but it’s more capital intensive and harder to execute on because it requires operational excellence.

With the end of covid, rising inflation and declining subsidies, we’re going to see if there is a real market for convenience grocery delivery.

Grocery is a $1.7tn market in Europe with €560bn spent in supermarkets and €210bn spend on convenience (mostly offline). Ecommerce penetration is 5% in the grocery sector compared to 31% for apparel and 17% for home/garden. MS forecasts that online on-demand grocery could account for 21% of the online grocery space by 2026 implying a €16bn market size.

Increasing AOV and achieving order density (a store needs to reach 400-500 orders per day) are 2 key success factors to achieve profitability.

“Typically in downturns, consumption patterns in grocery change. There may be (1) downtrading in store from one category to another, for example in animal protein (steak to hamburger); (2) downtrading in store towards private label items; and (3) downtrading from one store to another.”

Dark stores operators are able to reach 4-4.5 deliveries per hour in their most mature markets. Deliveroo says that it can do 5 orders per hour for a dark store compared to 3 when it partners with restaurants.

On gross margin, wholesalers achieve a 32-35% margin, Delivery Hero a 26.7% margin with clear path to increase by 5%pts, Weezy a 14% margin and offline convenience stores a 27-36% margin (Tesco Express, Co-Op, 7 Eleven).

Weezy and Gorillas say that they have a £25-30 AOV in the UK compared to £11 for an average convenience store.

Saturday, Jun. 25th: I read The Economist’s Technology Quarterly deep-dive on the energy transition. - The Economist

We’re facing an energy supply crisis (inflation, war in Ukraine, decommission of nuclear plants, etc.). We must react appropriately to combine “security of energy supply” and “climate security”. The easiest reaction would be to re-accentuate our dependency to fossil fuels but it’s not the right move for the long run.

To reach net-zero emissions by 2050, annual investment needs to double to $5trn per year.

It’s key to electrify processes which require fossil fuels as of today (powering cars, heating homes, heating steel foundries).

Wind and solar powered energy is crucial to transition towards a clean energy system but we need back-ups because this energy is intermittent (e.g. complemented with nuclear, better batteries, ability to diversify the location of wind/solar energy plants, reduce demand easily when supply is declining).

Long-duration energy storage technologies are important complements to intermittent renewables especially if you want to avoid fossil fuels and nuclear plants.

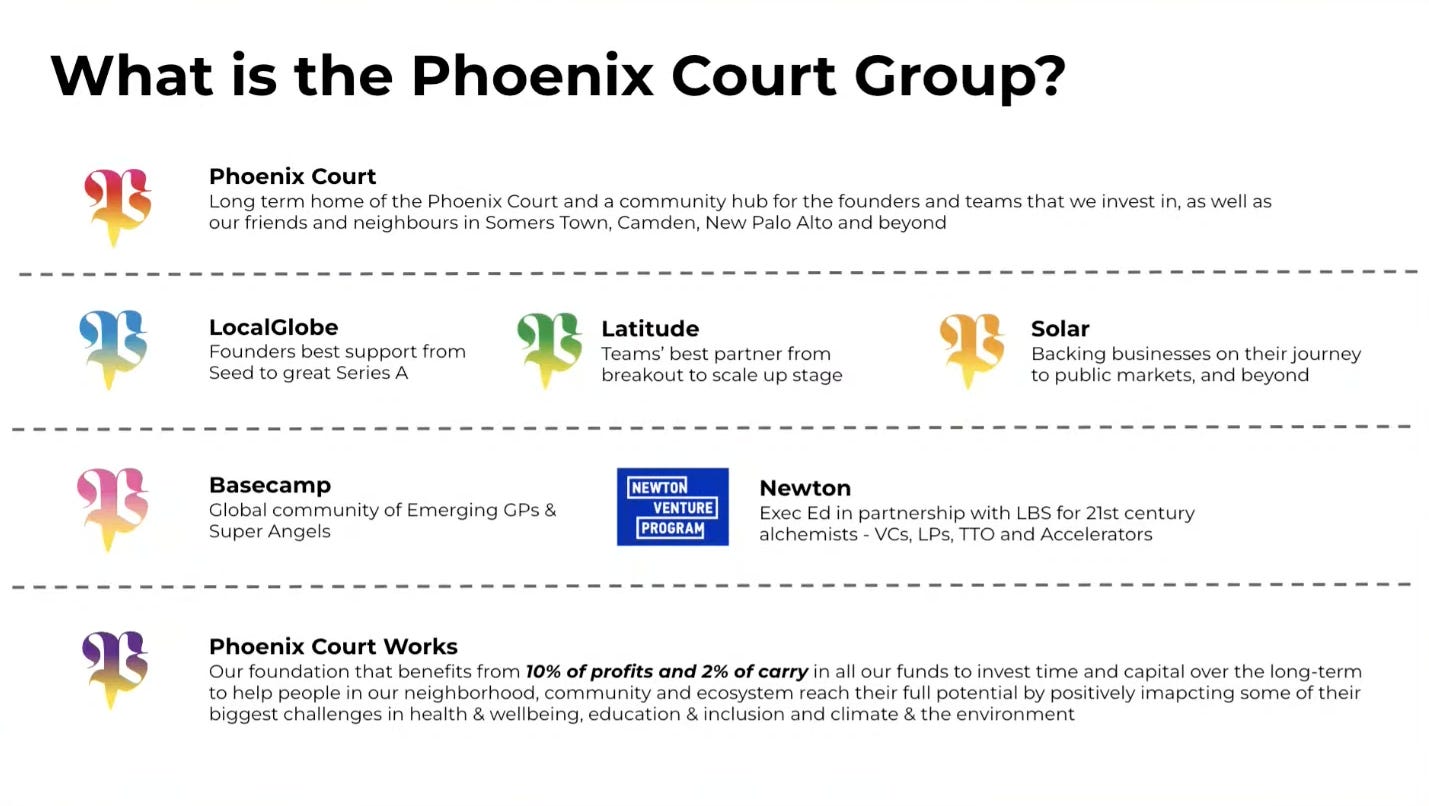

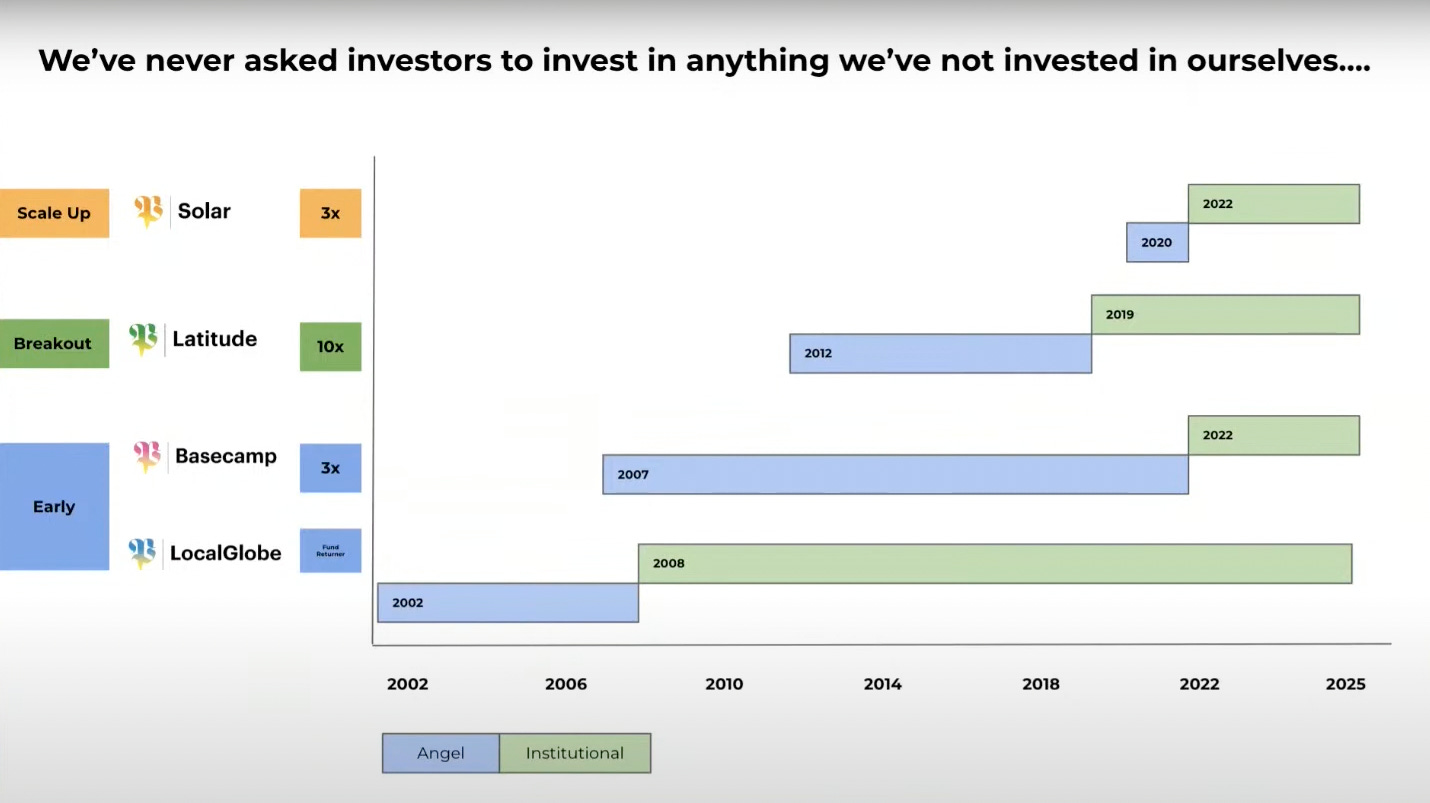

Sunday, Jun. 26th: I watched Phoenix Court Group’s (which is LocalGlobe’s new name) annual general meeting. - LocalGlobe

LocalGlobe is rebranding into Phoenix Court Group to showcase a stronger ambition going beyond LocalGlobe’s seed fund. LocalGlobe has now 4 investment strategies: backing super-angels/emerging GPs (Basecamp), backing pre-seed/seed companies (LocalGlobe), backing early growth companies in follower (Latitude) and backing pre-IPO companies (Solar).

Phoenix Group has always kickstarted its investment strategies with their own capital before raising money from institutional investors.

Overall, Phoenix Group has a bottom-up investment strategy building a super strong geo/thematic foothold at pre-seed/seed stages with LocalGlobe and Basecamp and leveraging this position to co-invest at later stages with top investors (either new companies or portfolio companies) with Latitude and Solar.

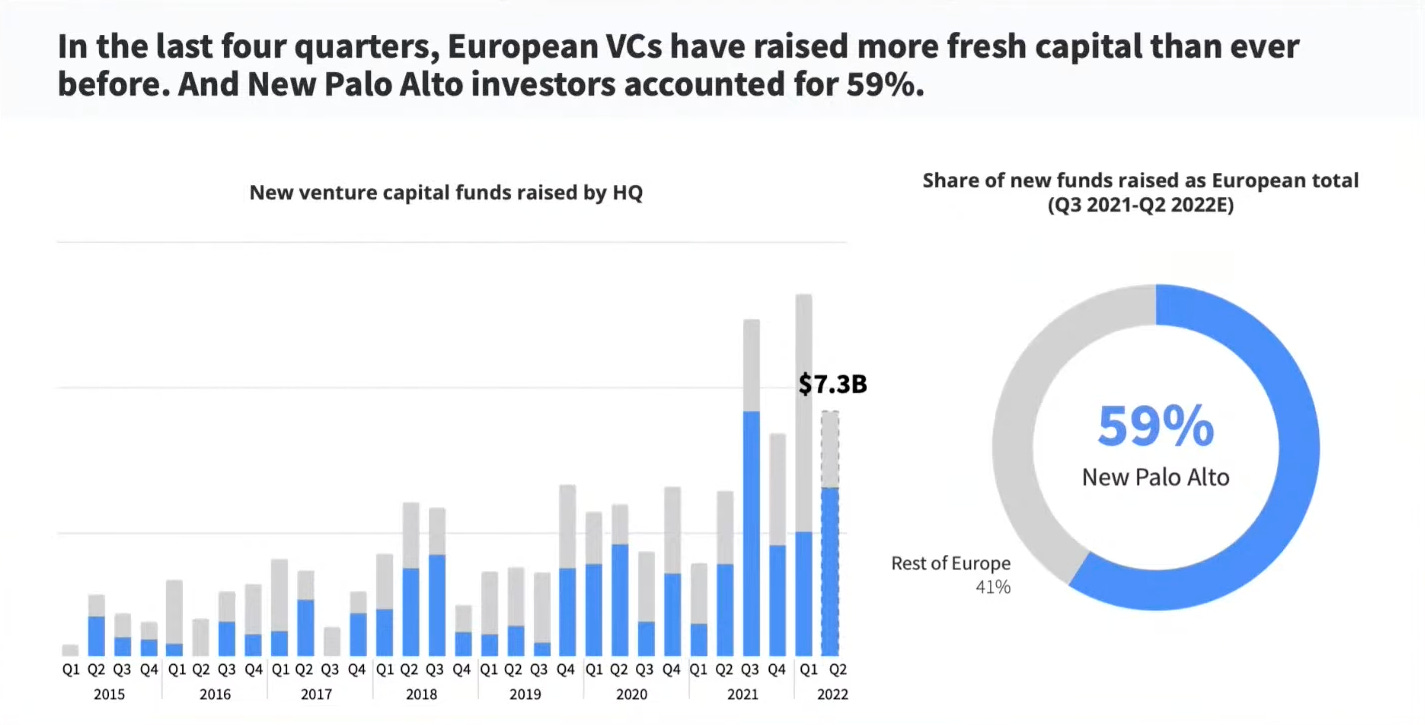

Phoenix Group invests predominantly in the New Palo Alto Area (a triangle between Amsterdam, Paris and London) where cities are interconnected within a maximum 4 hours rail trip and in which there is a strong density of knowledge and capital.

In Europe, there are 402 unicorns in 65 cities. Great companies can be created from anywhere and it brings a unique diversity compared to other tech hubs (China/US).

In the past 12 months, European funds have raised massive amount of capital that will be deployed over the next 3-4 years - even if we enter a recession.

Monday, Jun. 27th: The Economist wrote about Telsa’s full-stack approach to win in the car industry and reduce its dependency to supply chain turmoils. - The Economist

“Having outsourced much of the manufacturing process in the past half-century to focus on design, supplier management and parts assembly, car firms want greater control over their value chain—from the metals that go into EV batteries to the software those EVs run on and the shops in which they are sold.” Historically, the core competencies of a car manufacturer were: managing suppliers, design, marketing and assembling parts.

Elon Musk says that Tesla is “absurdly vertically integrated.” It has internalized all aspects of production. It has long term contracts to source materials such as lithium, graphie and nickel. It makes core EVs components inhouse (batteries, motors, electronics). Downstream, Tesla operates its own network of stores. Tesla has a 50-50 split between what is manufactured inhouse vs. purchased from suppliers (vs. 30-70 for Mercedes and 15-85 for Stellantis).

“Integration represents a strong competitive edge in an environment of structurally tight supply chains.”

By 2030, most of the revenues in the car industry will come from software vs. selling vehicles ($1.9trn vs. $4.1trn global car industry).

Tuesday, Jun. 28th: Accel announced a new $4bn global late stage fund to either double down on Accel’s portfolio companies or invest in new late stage companies. - Accel, Techcrunch

A pioneer at building a global VC firm. Accel was started in the US in 1983 but expanded in new geographies relatively early on compared to other US funds: it opened an office in Europe in 2000 and in India in 2008.

The prepared mind’s approach. “They also cultivated a deep sense of curiosity coupled with the discipline of preparation and research which enables us to move quickly across our global team once we identify founders whom we believe are building category-defining companies. […] Through this prepared approach, we can strip away competing distractions and focus on helping these exceptional teams build defining companies.”

Wednesday, Jun. 29th: Klarna is rumoured to raise a new round at c.$6.5bn valuation from internal investor Sequoia. Klarna is a BNPL global leader together with Affirm (stock price down 90% compared to its all-time high) and Afterpay (sold to Square). It’s a significant down-round as the company was previously valued at $46bn in 2021 in a $640m round led by Softbank. Klarna laid-off 700 people (10% of its workforce) earlier this year. Several factors could impact the BNPL sector in the coming months: (i) lower discretionary spendings, (ii) higher default rates, (iii) increasing interest rates reducing margins, (iv) increasing pressure from competitors (e.g. PayPal, Apple), (v) increasing pressure from regulators. - FT, Reuters

Thursday, Jun. 30th: Substack is laying-off 14% of its employees (13 out of 90 FTEs). In 2021, it raised a $65m funding round at a $650m valuation but only generated $9m in revenues (cut on subscriptions from writers monetizing the content they put on the platform). Substack needs to buy time to either reach profitability or grow into its valuation in order to raise capital on relatively good terms. Media has historically been impacted by downturns: (i) advertisers are cutting ad budgets and (ii) consumers tend to churn more because media is seen as a discretionary spending. - The New York Times, Chris Best

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋