🗞 Venture Chronicles - July 2022

Overlooked #120

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of July.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for July!

Friday, Jul. 1st: I watched Christoph Janz’s talk at SaaStr about balancing growth and efficiency for SaaS startups in bear markets. - SaaStr

High growth at all cost is no longer rewarded by investors.

If your growth slows down and you don’t adjust spendings, you end up in a vicious cycle with higher burn, shorter runway, less ARR than expected and less investors’ interest.

When you’re evaluating your performance against your plan, you should focused on new ARR added and not on total ARR. It’s key to focus on the right KPI to better react.

You need growth to raise in venture capital - even in this environment. It’s no longer growth at any cost. You have to find the right balance between growth and efficiency.

If you cut spendings, it should be specificly based on your situation (e.g. not cutting on sales & marketing but more on R&D and G&A if you have a great sales efficiency).

Saturday, Jul. 2nd: The Economist wrote about how the tech industry is being impacted by the stock market meltdown. - The Economist

Several negative signals are accumulating: less IPOs, 68% of VC funds are reporting markdowns of valuations in their portfolio, tourist startups investors are out (hedge funds, corporates, sovereign funds), 7% YoY decrease in the number of funding rounds in the US between March and May 22, secondary shares of top private companies are trading at a discount compared to Jan. 22, 1st down-rounds (Klarna) or self repricing (Instacart).

Private startups are adjusting their burn rate. Growth is no longer favoured at all-cost. Investors want to see a good balance between growth and efficiency.

3 categories of companies are more at risk: (i) companies in super competitive markets (cyber, fintech, instant delivery), (ii) startups who did not raise in 2021 and (iii) startups sensitive to consumer demand (e.g. Epic Games, Bytedance, Blockchain.com).

Local capital will remain in Europe (no dependency on the US/Asia).

Sunday, Jul. 3rd: Deb Liu shared Facebook’s marketplace back-story. - Lenny’s Newsletter

Facebook Marketplace is the world 2nd largest marketplace with 1bn+ MAUs only behind Amazon.

Facebook only started to work on a marketplace in 2015. People were naturally using Facebook to buy and sell things - especially in emerging markets were social and commerce are more naturally tied together than in the Western world.

Commerce started organically in Facebook Groups. Facebook fosters this behaviour by (i) enabling admins to reference their Groups as commerce Groups, (ii) structuring groups so that items for sales are classified as listings and not just discussion posts or (iii) sorting content to make items for sale more visible.

The Groups system was too constraining. People were still struggling to find the items that they were looking for. Facebook decided to add a marketplace tab within the app. It started in several US cities in which Facebook was measuring weekly buyer retention. To kickstart the liquidity on the marketplace, Facebook allowed sellers who were used to Groups and were posting on them, to tick a single box to also showcase their listing on the marketplace.

Monday, Jul. 4th: I read a post from Sarah O-Connor on gig economy tech companies (ride-hailing, restaurant food delivery, quick commerce grocery delivery). - FT

“To have people at your beck and call is not a new idea. In countries like Britain, it used to be commonplace for affluent households to have servants.”

“On-demand apps have enabled a mass-market version of the luxury of having people at your disposal to do things for you — albeit an atomised collection of people you don’t know and probably won’t see again.”

The gig economy is the symptom of rising economic inequalities with a low income class without better options. It has also been powered by venture capital money which enabled startups to sell services for less than it costs to provide them.

With capital drying up in public and private markets, gig economy companies are under pressure to reach profitability. They can do so by either paying their workers less (but low unemployment, increasing fuel prices, regulatory pressure to give social benefits to workers) or by charging their customers more (but inflation is hurting non discretionary spendings). Both options are problematic in the current environment.

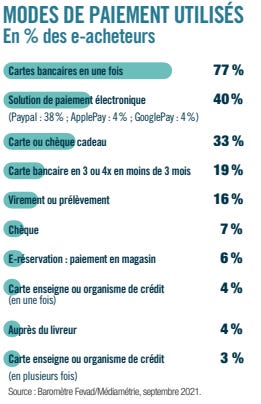

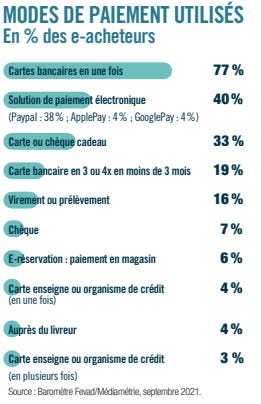

Tuesday, Jul. 5th: The FEVAD (French Federation for Ecommerce) published its annual report on ecommerce in France. - FEVAD

In 2021, the ecommerce sector generated €129.1bn in sales (15.1% YoY growth) across 2.14bn transactions (16.0% YoY growth, €60 AOV).

41.8m French people made an online purchase (62% of the population) in 2022. 22.3m made an online purchase via mobile (53% of online buyers).

200k ecommerce websites are active in France (+11% YoY). Most sales are generated by top ecommerce websites: 2.4k websites generating more than €10m in sales account for 75.8% of total sales in ecommerce.

36% of ecommerce merchants sell their products on marketplaces.

19% of consumers used BNPL as a payment method online. Cards remain the dominant payment method used by 77% of consumers.

Wednesday, Jul. 6th: Headline raised $954m for its early stage funds (North America VII, Europe VII and Brazil III). - Headline, Sifted, Techcrunch

“Our goal is to find people who are designing companies that don’t yet make sense to most, and then commit to them until their vision becomes a reality the whole world can see.”

Data and global first positioning. “One of our guiding principles is “be different, together” and it took time to validate our very own approach to venture. We use our own data platforms beyond personal networks and referrals to find companies. And, we’ve taken a global approach to investing from the beginning–some of our earliest investments spanned from Sao Paulo to Berlin.”

Headline raised a €320m early stage fund for Europe to back 10 seed/series A companies with €1-15m tickets. It wants to back “generational companies” and companies which have a strong international ethos from day 1.

Thursday, Jul. 7th: Xange raised a €220m fund 4. It invests in seed/series A in France and Germany with tickets between €300k and €10m. Xange also launched a €80m web 3 fund called Digital Ownership Fund able to invest in both tokens and equity. - Xange, Sifted

Xange 4 already made 15 investments including companies like Join, Dogami, Qubit Pharmaceuticals, Core Biogenesis, Aerospacelab, Silvr, Dattak, Popsink or Request.

Xange is expanding its presence in Germany (30% of investments targeted for Xange 4, offices in Berlin and Munich).

Xange wants to invest in the following sectors: digital health, decentralised finance, Web3, developer tools, bio sourcing and bio production.

Friday, Jul. 8th: Elad Gil wrote about the current startup market environment. - Elad Gil 1, Elad Gil 2

“Many areas (hiring plans, valuations, time venture capital raised lasts, etc) are roughly reseting to 2018/2019 norms, which themselves were all time highs prior to the COVID era.”

“Valuations will continue to drop and are not stable yet. Private markets tend to lag adjustments in public markets by 3-9 months and tend to adjust from the later stage, pre-IPO companies first to the pre-seeds last”

“Down rounds and structured rounds (where investors are "guaranteed" certain payouts if the company survives) will likely accelerate in 6-18 months.”

“Many companies are doing quick top-up rounds to add 6-18 months of runway and ensure the company has 36 months of cash to outlast any economic downturns or recessions. These rounds may be anywhere from $1M to $30M in size. Valuations on top ups have increasingly gone from slightly up to flat with the prior round.”

“Fundraises are likely to slow from 2021’s level, a company raising a new round every 6-9 months will go back to the historical norms of raising a round every 12-24 months. Companies with a valuation that far exceeds their product/market fit may not raise for 24-36 months, and many of them have the cash to last that long.”

“Some companies have also started getting more aggressive in performance cycles and letting go of 10% or so of their employees who are underperforming relative to their peers. In this case it is not a layoff but simply tightening performance criteria. GE famously would do this performance based approach annually, and McKinsey similarly had an "up or out" policy on an annual or every 2-4 year basis.”

“In 2021, VCs invested their venture funds in a single year. […] Now LPs are asking VCs to go back to 2018 standards and invest over a 2-3 year period.”

“We will see more layoffs in the next 1-3 months and then again in 6-9 months. Many will not cut enough and will need to do a second layoff 6 months later.”

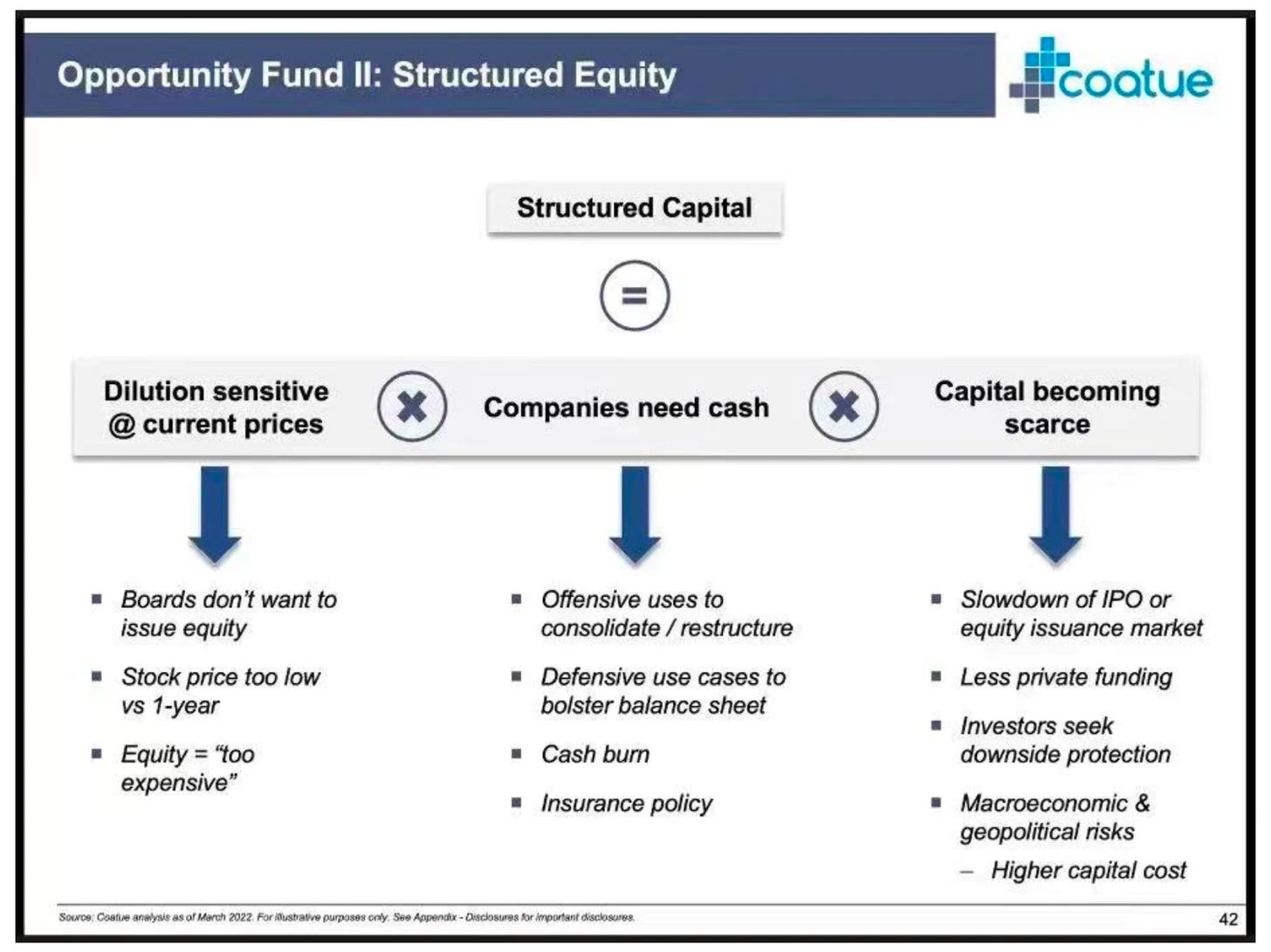

Saturday, Jul 9th: Eric Newcomer wrote about how hedge-fund Coatue is analysing the current market environment. - Coatue I, Coatue II

So far, Coatue has outperformed hedge funds rivals in 2022 because it sold more positions than its rivals in Q1-22. Coatue is down 17% YTD compared to 52% for Tiger Global, 35% for Altimeter and 22.5% for D1.

“The market can head fake rebound significantly on the way down.” “Bear markets are regularly marked by abrupt upward swings, only to get erased by a further downturn.”

“The market is failing to differentiate between good companies and bad ones.”

Coatue is raising a $2bn structured debt/equity fund to capitalize on the current market situation.

Healthy startups have 36 months of runway and a strong product market fit (customer love, scalable sales motion and a quality business model).

Sunday, Jul. 10th: I listened to a Colossus’ podcast episode on Berkshire Hathaway (BH). - Colossus

In 1965, Warren Buffet acquired BH which was a textile company in decline for several reasons: (i) capital intensive business, (ii) commoditisation of the textile industry and (iii) intense competition.

Warren Buffet diversified the group away from the textile industry starting with two insurance investments (National Indemnity in 1967 and GEICO in 1970) which were key to provide the capital to acquire other companies.

BH has the following acquisition criteria: (i) management in place, (ii) simple businesses, (iii) un-leveraged businesses with good returns on equity, (iv) demonstrated and consistent earning power.

Today BH’s value is mostly concentrated around 4 main pillars: (i) insurance with GEICO (auto insurance), BH Primary Group (casualty & property policies for commercial accounts) and BH Reinsurance Group, (ii) Apple in which BH has a 5.6% stake, (iii) BNSF Railway which is a railway network for goods transportation in the US and (iv) BH Energy which produces and distributes energy.

“Buy commodities, sell brands has long been a formula for business success…On a smaller scale, we have enjoyed good fortune with this approach at See’s Candies since we purchased it 40 years ago. When we bought See’s Candies, we didn’t know the power of a good brand. Over time we just discovered that we could raise prices 10% a year and no one cared. Learning that changed Berkshire. It was really important.”

BH is using the float of its insurance businesses to fund new acquisitions. Float is composed of insurance premiums that have been paid upfront by insurers and that have not yet been paid back in form of indemnities.

BH did not want to invest in tech because it was outside Warren’s circle of competence. When BH invested into Apple, it was because it was a consumer company with a brand that brought unprecedented competitive advantage like Coca Cola. Once you’re locked in Apple’s ecosystem, you never churn.

GEICO is a consumer auto insurance business in the US. It has a low cost positioning with an excellent consumer satisfaction. It advertises and sells directly to consumers, avoiding brokers (6.4% of premiums spent in acquisition in 2013). It has a 70-75% loss ratio compared to 65-70% for the industry average. It has a 15% expense ratio compared to 25% for industry average.

Monday, Jul. 11th: Goldman Sachs interviewed Howard Marks about investing and the current market situation. - Goldman Sachs

Howard does not believe in forecasts but in market cycles. It’s hard to predict the future but it’s not that hard to predict the present. You can take the market temperature and see if people are bullish or bearish. Once done, if investors are pessimistic, you want to buy.

Oaktree set up a debt fund to invest into companies below investment grade. There are two conclusions to be drawn from this activity: (i) it’s not what you buy but it’s what you pay and (ii) success in investing does not come from buying good things but from buying things well.

In order to be a successful investor, you should dare to be different by making investments into assets that seem unpopular. Moreover, you should dare to be wrong. Otherwise, you should just invest into an index fund. Outperforming the market implies behaving differently from the market and hence taking the risk to underperform the market.

Consistent batting average vs. Swinging for the fences. There are 2 routes for market outperformance: (i) slightly over-performing the market consistently by cutting off the bottom tail, (ii) accepting high variance in your performance and hoping that on average you over-perform the market.

The past has relevancy but it’s not absolute implying that risk cannot be quantified. It’s the probability of a bad event happening in the future which cannot be quantified in advance and even a posteriori.

You can’t succeed if you don’t survive. You should arrange your affairs so that you can survive in the bad days.

Tuesday, Jul 12th: Tuesday, Jul. 12th: Derek Thompson wrote about the Millennial Consumer Subsidy. Urban millennials will have to change their lifestyle which was powered by consumer tech startups subsidising consumption with venture capital money. - The Atlantic

“With markets falling and interest rates rising, start-ups and money-losing tech companies are changing the way they do business.”

"It was as if Silicon Valley had made a secret pact to subsidize the lifestyles of urban Millennials. As I pointed out three years ago, if you woke up on a Casper mattress, worked out with a Peloton, Ubered to a WeWork, ordered on DoorDash for lunch, took a Lyft home, and ordered dinner through Postmates only to realize your partner had already started on a Blue Apron meal, your household had, in one day, interacted with eight unprofitable companies that collectively lost about $15 billion in one year.”

“The Millennial Consumer Subsidy is over, and for the foreseeable future, metro residents will have to go about living the old-fashioned way: by paying what things actually cost.”

Wednesday, Jul. 13rd: The Economist wrote about TikTok. - The Economist I, The Economist II

TikTok is disrupting the social media industry worrying both direct competitors and regulators. In Sep. 21, TikTok reached 1bn users - a milestone reached in 4 years when it took 8 years for other social media giants like Facebook, Youtube and Instagram.

In the US, 44% of TikTok’s users are under 25 compared to 16% for Facebook and users spend 46 minutes per day on the app compared to 30 min for Facebook and Instagram. In China, users spend 100 min per day on Douyin/TikTok.

The Economist highlights the following success factors for TikTok: (i) no need to have a network of friends to enjoy the app, (ii) video editing democratisation, (iii) AI discovery algorithm promoting creators with viral content over creators with massive existing audience.

In China, Douyin/TikTok has become a large e-commerce player thanks to live-streaming. The company is trying to replicate this playbook in the West.

TikTok is eating market share away from other social media giants by replicating some of their core features (e.g. extending the length of videos to 10 min to compete with Youtube or launching live monetised via subscriptions to compete with Twitch).

Governments and societies are afraid of China’s government potential influence on TikTok. In theory, China could access TikTok users’ data and could leverage TikTok to promote political ideas favourable to its political regime.

Thursday, Jul. 14th: Deconstructor of Fun wrote an outstanding paper on the rise of Battle Passes as a key monetization driver in gaming. - DoF

A Battle Pass is a monthly subscription to access exclusive ingame content and to accelerate progression within a game.

What are the benefits of Battle Passes? (i) Improving retention and engagement. (ii) Great value product making it a no-brainer purchase for engaged players. (iii) Bringing recurrence to monetization. (iv) Monetizing a broder base of gamers (vs. generating most revenues a small number of players).

Battle Passes are priced between $5 and $15 per month. It provides: (i) faster progression, (ii) instant exclusive rewards, (iii) premium only reward, (iv) access to time-limited events in the game. To work, Battle Passes should be generous providing 10-20x value of rewards compared to the price to make it a no-brainer.

Friday, Jul. 15th: Dan Frommer published a 2022 mid-year update on consumer trends. - Newconsumer

Saturday, Jul. 16th: Sensor Tower published Q2-22 data on mobile apps. - Sensor Tower

35bn downloads on iOS and Android in Q2-22 which is a 2.5% YoY decline.

TikTok is the most downloaded app. Interesting to see apps like Whatsapp Business, Capcut (photo/video editing app by Bytedance) Shein (fast fashion ecommerce app) and Meesho (social commerce app in India) in the list. In the US, BeReal was downloaded more than 4m in Q2-22.

In the US, consumers are shifting their spending to non-gaming apps mainly driven by subscription apps. For the 1st time, non gaming apps represent more than 50% of US app store spending.

“400 apps had more than $1 million in consumer spending on the U.S. AppStore in Q2 2022, eight times the Q2 2016 number”.

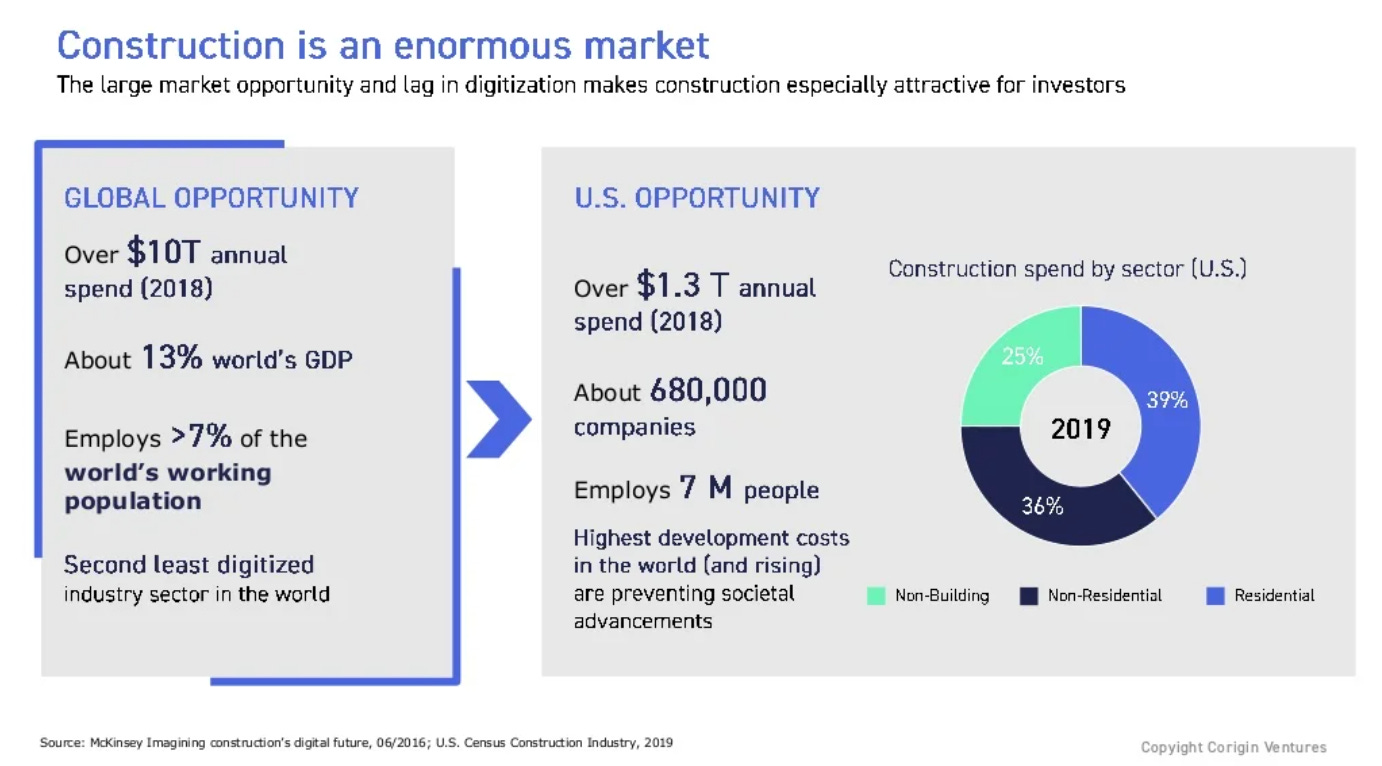

Sunday, Jul 17th: I read several posts from the Alpaca’s team on construction. - Alpaca I, Alpaca II, Alpaca III

In general:

On financial services:

Construction has a tech adoption problem. To solve it, it’s key to have (i) a verticalised product embracing the industry’ specificities and (ii) a team with a previous experience in the industry.

Construction costs are booming for both labour and materials.

Alpaca shares a playbook to build a verticalised fintech startup in the construction industry: (i) digitize an outdated component of business workflow, (ii) leverage the digitized experience to collect data across ecosystem, (iii) create additional value by providing insights and analytics and (iv) develop and expand products by broadening the range of fintech services offered across the business.

On materials procurement:

“On the demand side, contractors are managing 10+ supplier relationships for a given project due to the high level of fragmentation, and each supplier and material has its unique nuances and logistics. Delayed material delivery drives up to a ~30% increase in construction material costs, while a lack of transparency results in companies overpaying by up to 15%.”

“On the supply side, a lack of technology adoption results in an inability to provide accurate delivery estimates, streamlined ordering and invoicing workflows to customers. Fulfilling deliveries is challenging, and most suppliers are unable to fulfill same-day orders. Further, fulfilling large orders often requires financing, which increases the time required to fulfil orders.”

Monday, Jul. 18th: GoPuff reduced its workforce by 10% (1.5k employees) and shut down 12% of its warehouses (76 warehouses). In Europe, GoPuff may exit France and Spain to refocus on the UK. GoPuff is stopping its extreme expansion strategy in a market that is no longer rewarding growth at all costs. On average, GoPuff makes $0.88 cents in EBIT per order and up to $3 in top locations. It takes 6 months to reach profitability on a warehouse. GoPuff has $2bn in cash and a 4y runway that is going to be sufficient as the company expects to reach profitability by 2024. - Bloomberg

Tuesday, Jul. 19th: I listened to a Colossus’ podcast episode on Rolex. - Colossus I, Colossus II

It’s a Swiss-based luxury brand selling high-quality and built-to-last watches. It has a vertically integrated model acquiring all its suppliers (e.g. it creates machines to test both their watches and the machines making watches).

It’s owned by a foundation called the Hans Wilsdorf Foundation and run as a non profit organisation. Most of its earnings are funding charities. It’s also a super secretive company.

It distributes its products exclusively via its network of branded stores. It pushes customers to purchase offline to build a personal connection with them.

It generated €8bn in sales in 2021 ($7k wholesale AOV) representing a 29% market share of the Swiss watchmaking industry. It produces 1m watches per year and it takes c.1y to produce a Rolex.

It sponsors sporting events practiced by people with high net worth like The Australian Open (tennis), Formula One or The US Open (golf). It has also top sportsmen as ambassadors like Roger Federer (tennis) or Tiger Woods (golf).

Wednesday, Jul. 20th: Microsoft-owned Minecraft is banning NFTs from its game which were starting to be used either to access Minecraft servers or as in game content (e.g. skins, items, etc.). - Minecraft, Wired, Coindesk, Chris Dixon

“Each of these uses of NFTs and other blockchain technologies creates digital ownership based on scarcity and exclusion, which does not align with Minecraft values of creative inclusion and playing together. NFTs are not inclusive of all our community and create a scenario of the haves and the have-nots. The speculative pricing and investment mentality around NFTs takes the focus away from playing the game and encourages profiteering, which we think is inconsistent with the long-term joy and success of our players.” - Minecraft

“It’s a good reminder of why you shouldn’t build on corporate-owned (web2) networks. They change the rules on developers on a whim.” - Chris Dixon (GP at a16z crypto)

This decision is jeopardising NFT Worlds which is a company building tools to make Minecraft compatible with web 3. More broadly, it also shows the opposition between traditional gamers who hate NFTs and web 3 believers who champion them.

Thursday, Jul. 21st: Unity is acquiring IronSource. - Unity 1, Unity 2, Stratecherry

Unity is acquiring IronSource to create a single platform to create and grow 3D experiences (which are mainly mobile games).

It’s a $4.4bn acquisition fully financed in shares. SilverLake and Sequoia are also funding the combined entity with a $1bn convertible note (2% interest rate per year, due date in 2027 and $48.89 conversion price). Unity’s share price has fallen by 70% in 2022. It had a $12bn market cap when it announced the merger. Ironsource went public via a SPAC in 2021 at a $11.1bn market cap. and its its market cap plummeted to $2.28bn at the time of the acquisition.

IronSource was founded in Israël in 2010. It generated $623m in revenues (60% YoY growth) and $213m EBITDA (34% margin) in the last 12 months with a 98% gross retention and a 153% net dollar retention.

“Monetization, in particular advertising, are critical to the creator economy. Performance-based ads in particular are central to the gaming ecosystem and we believe they will continue to grow. Ads are a data-driven, scale business - together, Unity and IronSource will provide more scale to empower creators.”

IronSource is an ad mediation platform for mobile games. Game publishers install IronSource’s SDK to get access to multiple ad networks. Unity has its own ad network. It was trying to launch an ad mediation platform but it was struggling to release it.

“IronSource’s main product is ad mediation for mobile apps — mostly games. The goal of publishers is to fill as much of their ad inventory as possible with ads that have the highest rates as possible, all while controlling their own cost and complexity. These two things work against each other: a publisher could work with only one ad network, but then they are limited to whatever ads and rates that ad network can achieve; alternatively, they could work with multiple ad networks, but then they have to manage multiple SDKs, figure out how to run ads from which ad network when, etc. Ad mediation platforms solve this problem: publishers only need to install one SDK from the ad mediation provider, which incorporates multiple ad networks. Publishers can then control their ads via the ad mediator’s dashboard, or let the ad mediator handle everything automatically (publishers are often wary of this, particularly because ad mediators are liable to favor their own ad networks). The two leading ad mediators in the market are AppLovin (Max) and ironSource (LevelPlay), with Google (AdMob) in third.”

“Reducing the barrier to entry for making games means there is far more competition when it comes to actually making money from games. […] This is a dynamic you see everywhere on the Internet: making it far easier to make and produce any product, whether it be news, analysis, podcasts, music, games, t-shirts, etc. reduces the value and power of those who were capable of making and producing those products previously. The positive spin on this is the removal of gatekeepers; the negative spin is a collective race to the bottom where success is a function of cost structure, not quality. […] The winners in this world are the Aggregators: “democratize _____” is another way of saying “reduce the bargaining power of suppliers”, leaving everyone dependent on the Aggregator for revenue from a business model — almost always advertising — that only works when all of those suppliers are bundled together and monetized at scale. That is how you have Google effectively monetizing the whole web, Facebook monetizing user-generated content, and Unity’s ambitions for growing its ad business by being a one-stop shop for games.”

Friday, Jul. 22nd: FT Partners published a detailed presentation on B2B Payments. - FT Partners

In the US, paper checks still account for 47% of B2B payments and 81% of all firms are still using paper checks. Paper checks have major pitfalls: (i) long settlement period (2 business days to clear a deposited check and 5 days for the bank to receive the funds), (ii) high mailing & processing costs ($4-20 to process a check), (iii) fraud.

c.60% of companies are transitioning their B2B payment methods.

Issues around B2B payments: manual processes (prone to errors and not productive), not enough payment methods, need to be integrated with business workflows (purchase orders, invoices, payment terms, AR/AP).

Saturday, Jul. 23th: Amazon is acquiring One Medical for $3.9bn in an all-cash transaction. One Medical is a network of c.200 digitised primary care clinics. It has a dual go to market strategy B2C and B2B2C as an employee benefit tool for companies. OneMedical went public in 2020. - Amazon, NPR, Techcrunch

In 2018, Amazon acquired online pharmacy company PillpPack for $753m and launched Amazon Pharmacy in 2020 as a prescription delivery service. Amazon also tried unsuccessfully to create a non-profit organization with JP Morgan and Berkshire Hataway to improve primary care and reduce healthcare costs for their employees. Amazon has also a telemedicine offering called Amazon Care which was released nationwide in 2022.

“We think health care is high on the list of experiences that need reinvention. Booking an appointment, waiting weeks or even months to be seen, taking time off work, driving to a clinic, finding a parking spot, waiting in the waiting room then the exam room for what is too often a rushed few minutes with a doctor, then making another trip to a pharmacy – we see lots of opportunity to both improve the quality of the experience and give people back valuable time in their days.” - Neil Lindsay, SVP of Amazon Health Services

Sunday, Jul. 24th: The New York Times wrote about retailers massively selling their inventory to liquidators at steep discounts. - The New York Times

With inflation, consumer spending is decreasing especially for discretionary products (clothing, gardening equipment, electronics). Moreover, product returns have increased from 10.6% in 2020 to 16.6% in 2021. On top of this, retailers over-order from suppliers because of global supply chain issues and because e-commerce penetration seemed to have accelerated. As a result, retailers have too much inventory on their hands representing $761bn of lost sales in 2021.

“While some retailers are discounting the surplus within their stores, many would rather avoid holding big sales themselves for fear of hurting their brands by conditioning buyers to expect big price cuts as the norm. So retailers look to liquidators to do that dirty work.”

In 2021, 10%+ of returns involved fraud (people wearing clothing and sending it back, stealing goods from stores and returning them with fake receipts).

Liquidators have several options: (i) reselling goods with at discount to consumers, (ii) donate goods to charities, (iii) return products to manufacturers, (iv) recycle goods, (v) burning goods into incinerators generating electricity.

Monday, Jul. 25th: Ghost raised a $13m series A led by USV. It’s a marketplace to help brands and retailers discreetly liquidate excess inventory. - Techcrunch, USV

“The platform handles the messy backend too – Ghost automates the posting, sale, and shipment of unsold inventory while offering immediate payment to credit-worthy sellers.”

Excess inventory is a massive pain point in ecommerce with brands overproducing more than $500bn in goods and some categories having over 30% of their inventory unsold after one year.

In Europe, massive businesses like VentePrivées or ShowroomPrivé have built massive businesses out of excess brand inventory with a closed marketplace and a flash sales model.

Tuesday, Jul. 26th: Shopify decided to cut its workforce by 10%. With covid, Shopify over-expanded believing that e-commerce penetration would permanently leap ahead by 5-10 years. Unfortunately, it has not been the case. E-commerce penetration has reverted back to its historical strong but steady annual growth. Shopify was impressive at accelerating its product roadmap in the past 2 years to empower merchants to ride the covid wave (i) releasing new products like Link in Bio, Shop Pay Installments, Subscriptions, Post Purchase Upsell, Shopify Balance, POS and (ii) announcing massive partnerships with Youtube and TikTok (to make shoppable e-commerce stores in TikTok and Youtbe for Shopify’s merchants) or Meta (to release Shop Pay on Instagram or Facebook). - Shopify

Wednesday, Jul. 27th: Alan published its Q2-2022’s letter to shareholders. - Alan

Alan is moving forward in its vision to become a one-stop shop healthcare partner for companies and their employees after having started as a health insurance.

Alan has now 325k signed members (inc. 298k in France) and has reached a €204m ARR (inc. €198m in France). Besides France, Alan is present in Spain and Belgium.

It launched Alan Silver “allowing retiring members to remain covered by Alan.”

Alan is upselling its mental-health offering called Alan Mind to its customer base.

Thursday, Jul. 28th: Capital Group estimates that Instacart is now worth $14.7bn in its books which is significantly lower than Instacart’s own valuation repricing from $40bn to $24bn in March. Instacart repriced its valuation to become more attractive for employees and to prepare its IPO. - Bloomberg

Friday, Jul. 29th: Frederik Gieschen wrote about how Warren Buffet was balancing reading with networking to come up and refine investment ideas. You need both to be a successful investor. - Frederik Gieschen

“I’m sure he spends a lot of time reading. But always remember that his wealth was built on the balance of compounding wisdom and relationships. In fact, the two reinforced each other. Go and do likewise.”

Networking was detrimental in Buffet’s career evolution. For instance, (i) without meeting Charlie Munger, he may have never pivoted towards quality investing and (ii) he was convinced to buy GEICO’s stock as a student only after traveling to meet the financial VP in GEICO’s Washington office.

Saturday, Jul. 30th: Firstmark raised $1.1bn for its First Mark Capital VI and First Mark Capital Opportunity IV funds. It’s an early-stage generalist investor based in New-York. Firstmark sees venture as a craft with a small group of experienced partners leading rounds, deploying capital at a steady pace and supporting entrepreneurs during ups and downs. - Matt Turck, Fristmark

Sunday, Jul. 31st: Ramp is still growing at an exponential pace having double its revenue run-rate since the beginning of the year. Ramp started with SMBs but has now a strong growth amongst mid-market and enterprise customers. It counter-positioned industry incumbents with a corporate card to help businesses spend less. Today, Ramp has 7k customers who are making $1m in cost savings daily or are lowering their spendings by 3.5%. - Techcrunch, Eric Glyman

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Ghost is one of the most promising new model I've seen during the H1 of this year!

I'm absolutely shock about pay-check % in the USA !