🗞 Venture Chronicles - February 2022

Overlooked #105

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of February.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for February!

Monday, Feb. 1st: Descartes Underwriting raised a $120m series B led by Highland with the participation of Eurazeo (💙) and existing investors Blackfin, Serena and Cathay. I believe that there are two new main risks that are poorly addressed by insurers: cybersecurity and climate change risks. Descartes is addressing the latter with parametric insurance products. It has attracted 200 customers. It will use the funding to expand to new business lines and to continue its global commercial expansion. - Tech.eu, Descartes

Wednesday, Feb. 2nd: Our portfolio company Withings acquired 8fit. Withings is a health wearable manufacturer (smartwatches, scales, etc.). 8fit is a fitness and nutrition subscription-based mobile app. Withings will leverage 8fit's ability to build and monetize subscription-based mobile apps and will enable access to a rich library of fitness and nutrition content to its user-base. - Tech.eu, Techcrunch

Thursday, Feb. 3rd: German-based VC firm Earlybird opened an office in Paris, recruited a local team and raised a dedicated side fund to invest in the country. It recruited a former Facebook's executive called Salomon Aiach who is joining as principal to lead the Parisian office. It will invest €1-10m tickets in seed and series A. Earlybird is another foreign fund that has understood that to cover the French venture market properly, you need to have a local team with a strong autonomy. - Techcrunch

Friday, Feb. 4th: Wayflyer raised a $150m series B round at a $1.6bn valuation co-led by DST and QED. It's a revenue-based financing platform for ecommerce merchants. It has impressive metrics: $100m financed per month (+1,000% YoY) and 65% of its customers are in North America (rest in Europe and Australia), thousands of customers raising $300-400k on average (to cover inventory purchases, shipping costs, marketing expenses). - Techcrunch

Saturday, Feb. 5th: Patient Capital published a 80-slide deck on Spotify. - Patient Capital

Spotify has 172m paid premium subscribers, 381m MAUs, €10bn in FY21E revenues, 3.2m podcast titles and 70m music tracks.

"MAUs spend on avg. ~45 minutes per day on the platform (80 minutes for paid subs vs. 25 minutes for ad supported users), which makes Spotify (SPOT) one of the most beloved apps in the world. For paid subs, the average daily usage time compares well to YouTube (60 min)/WeChat (85 min)/Douyin (90 min)/Netflix (120 min)"

"Initially market participants framed SPOT as the “Netflix for music”. Soon it became evident that NFLX’s cost structure in video is much more favorable than SPOT’s in music. NFLX pays fixed amounts for licensed or self-produced content and these costs do not grow in line with incremental revenues, whereas SPOT’s costs to music rights holders rise in tandem with incremental revenue (which puts a cap on gross margins). SPOT’s management team realized they need a business model besides music with more fixed costs. In a famous blog post (Feb 19) Daniel Ek declared that all audio — not just music — will be the future of SPOT."

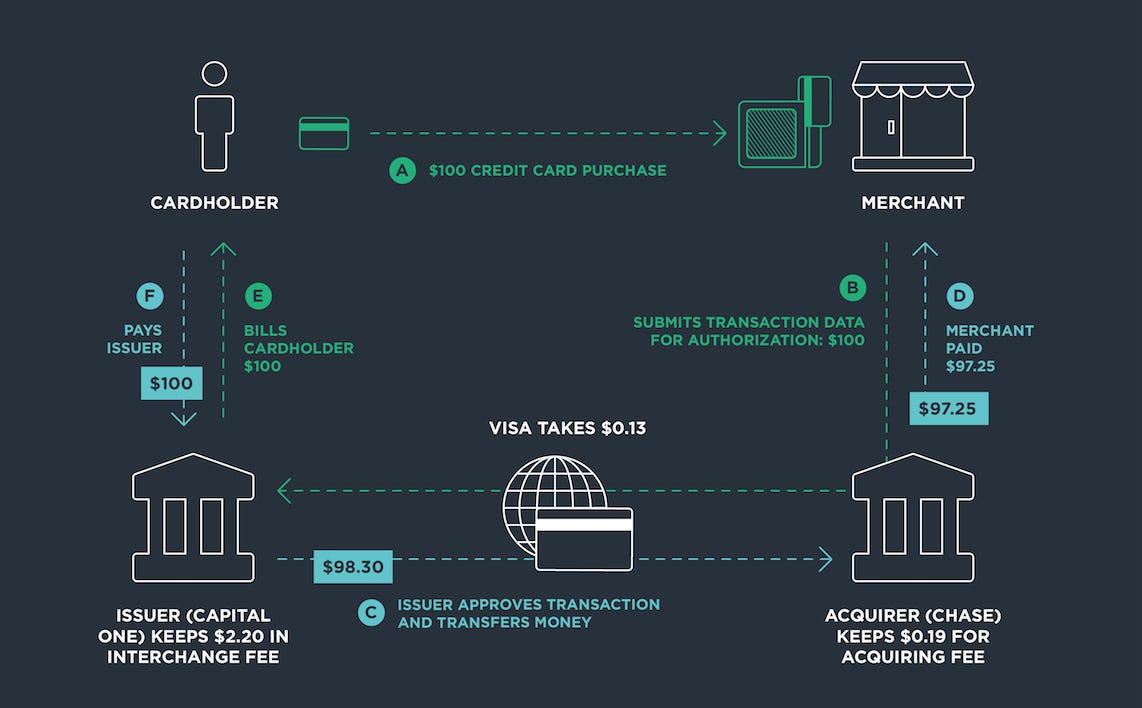

Sunday, Feb. 6th: I listened to a Colossus' podcast episode breaking down Visa's history and business model with Alex Rampell who is GP at a16z. - Colossus

What is happening and who are the key stakeholders in a single credit card transaction? A transaction happens between (i) a buyer who has a credit card from a bank called the issuing bank, (ii) a merchant who has a bank called the acquiring bank and (iii) a network (Visa/Mastercard) connecting the issuing bank and the acquiring bank. Merchants and consumers don't deal directly with card networks. Issuing and acquiring banks do.

The card network is remunerated via a transaction fee called the interchange fee that is split between the issuing bank (taking most of the interchange fee), the card network (7.5cts per transaction for Visa on average) and the acquiring bank. Depending on many factors (type of cards used, type of merchants, international or domestic transaction, etc.), the interchange fee will vary. The issuing bank will often redistribute part of the revenues generated by the interchange fee to the end consumer (e.g. with cash back programs).

Merchants hate interchange fees but they have no choice but to accept them because they cannot refuse payments via credit cards. On the other hand, issuing banks love interchange fees because they can leverage their remuneration to attract more consumers with cashback. In Europe and Australia, interchange fees are regulated but in other geographies, they tend to go up overtime because of this mechanism.

Visa was created in 1958 within Bank of America which was only in California at the time. The bank launched a card called BankAmericard and to solve the chicken and egg problem issue, it just sent a credit card to the 60k customers it had in a city called Fresno (45% of the population). It leveraged this customer base to sign merchants in the city and it took a c.6% fee on all transactions. At some point, other banks wanted to introduce a similar program but did not want to be dependent on Visa. As a result, two consortiums led by banks and operated as non profits were created: one as the successor of BankAmericard which became Visa and one which became Mastercard. Mastercard and Visa became public companies in 2008. Moreover, they managed to start generating profits and keeping them for themselves. In parallel, banks progressively sold their ownership into both companies.

For large merchants, when they generate revenues from an issuing bank that is the same as their acquiring bank, they negotiate with their bank to process transactions directly without passing by the card networks ("on us transactions").

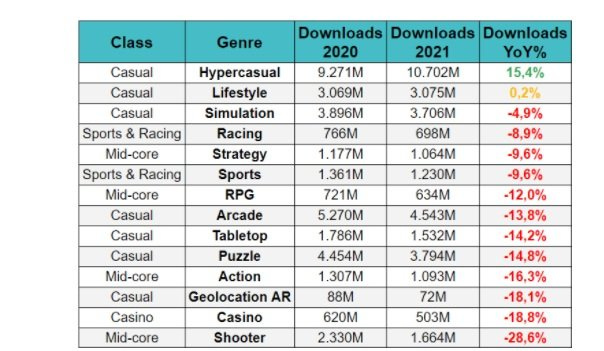

Monday, Feb. 7th: Deconstructor of Fun wrote a post with predictions on causal mobile gaming. - DoF

2020 was a record year for mobile gaming (36% downloads growth and 31% revenue growth). In 2021, it was harder to sustain this growth especially since user acquisition became more difficult with Apple's changes to strengthen user privacy. As a result, downloads stayed stable (52.7bn downloads vs. 52.9bn in 2020) while revenues continued to grow but at a slower pace (17% growth, $49bn game consumer spend).

Not as many new games were launched in 2021 for 2 main reasons: (i) it’s harder to ship new games in remote-work set ups, (ii) it takes longer to figure out the game potential to become a hit because of privacy changes.

The top 100 games generated 65% of all in-app purchase revenues and 860+ games are generating more than 10m in net annual revenues.

Casual games generated 80% of all downloads (33bn downloads) and 35% of all IAP revenues ($17.2bn). On top of IAP, casual games also generated $3.4bn of ads revenues.

"On a high level, Hypercasual seems to be chugging along despite the deprecation of IDFA. In 2021 the genre reached 13 Billion downloads and $3.4B in total estimated revenue (IAP + IAA). This is a 15% increase compared to 2020. At the same time, the IAPs in the genre increased over 50% indicating the trend of hybrid-monetization we’ve been talking about for the past years."

HCG (hypercasual games) was the most resilient genre in 2021 because (i) players reacted to privacy changes by releasing games targeting broader audience and by leveraging their existing audience for targeting, (ii) consolidation is starting (top games are staying longer in the top 100 and large game publishers are starting to consolidate the market) and (iii) game publishers are moving towards hybrid-monetization (combining ads and in app purchases).

Tuesday, Feb. 8th: Our portfolio company Silvr (💙) raised a €130m series A (€18m in equity and €112m in debt) led Xange and Otium with the participation of BPI, Isai and Eurazeo. Silvr is building an horizontal tech platform to provide financing to all tech business models (SaaS, CSS, e-commerce) in less than 24 hours. In 1y, Silvr has built a team of 25 people, launched a SaaS product on top of its ecommerce product, funded 200 loans and 100 companies and shipped a scoring model. It will use the funding to grow the team, double down on product development and expand into other European countries. - Techcrunch, Xange, Overlooked

Wednesday, Feb. 9th: Mirakl held a press conference to share a business update with partners, customers and journalists. - Mirakl, La Tribune, Mirakl's CMO

Mirakl passed the $100m ARR threshold (being valued at a 35x ARR multiple) with 300 customers.

In 2021, Mirakl added 80 new customers (e.g. Macy's), launched 66 new marketplaces (e.g. CMA CGM, UNFI, Decathlon), viewed its customers generated $4.3bn in GMV and recruited 360+ FTEs.

Mirakl acquired Octobat which is specialised into "automatic and compliant tax invoice generation" to help Mirakl's customers to be compliant while operating in multiple geographies

Thursday, Feb. 10th: Our portfolio company Alma (💙) raised a €115m series C with Tencent, Eurazeo GR Capital, Cathay, BPI, Seaya and Picus. It has become the BNPL market standard in France with 6k merchants (inc. Etam, Galeries Lafayette, Printemps, Ankorstore), a €1bn annualised GMV and an omnichannel solution (processing both offline & online payments). Alma will use the funding to expand internationally (Italy, Spain, Germany, Belgium) and to launch a B2C app! - Techcrunch

Friday, Feb. 11th: Sifted shared key criteria that some European VC funds are looking for in the founders that they want to back. - Sifted

Northzone: "They look for founders with (1) a deep drive and personal motivation to be an entrepreneur, paired with (2) a growth mindset and openness for self-development. This in turn, enables them to (3) attract talented people around them when scaling the business. Similarly they view (4) having a healthy dose of self-confidence as a positive attribute that enables founders to go through the rough patches while staying humble. Finally, in terms of skill-sets, they (5) encourage founders to identify their own superpower and evolve into a thought partner across other business functions without (6) needing to exert too much control across all areas."

EF: They look for founders who: (i) challenge convention, (ii) have a strong bias for action, (iii) can create followership, (iv) are smart with clarity of thought, (v) have technical knowledge and ability to transform it into applicability/commerciality.

Saturday, Feb. 12th: Weekend Fund’s team shared the web 3 themes they are following and investing into. Weekend Fund is a solo GP fund created by Product Hunt's founder Ryan Hoover who has partnered with Vedika Jain (ex. employee at Stripe and TrueLayer). Web 3 is leveraging 3 shifts: (i) a tech shift from closed databases to an open distributed ledger, (ii) an incentive shift from platform-owned to community-owned and (iii) a cultural shift away from trusted platforms. - Weekend Fund

Accessible blockchain infrastructure: developers should be able to build on the blockchain without learning new smart contract programming languages. If you push this one step further, everyone and not only developers should be able to do so.

Embedded crypto infrastructure: "embedded NFT, token and crypto infrastructure products that "hide" the complexity of crypto under good UX so that the user doesn't need to be crypto-native".

Squad wealth tooling: "we need a new set of tools to communicate, coordinate, incentivize, generate and manage wealth generated by online networks."

Invisible DeFi (Decentralised Finance): financial products based on DeFi but abstracting DeFi complexity to end users.

Web 3 identity & reputation: decentralization makes it harder to trust identities because they're fragmented across wallets, communities and pseudonyms. Making web 3 identities interoperable is key to rebuild this trust while preserving the user ownership's on his identity.

P2E (Play to Earn) games and infrastructure: P2E is the next business model innovation in gaming ("Arcade → In-Home → Online Multiplayer → Facebook freemium → Mobile freemium → Everything freemium → P2E") and infrastructure tools are needed to help game developers ship and manage P2E games.

Sunday, Feb. 13th: I read a post from Mine Safety Disclosure on Visa. - Part I, Part II

"Visa's value proposition is simple: integrate with us, and gain instant access to a network of 3 billion cards, 16,000 banks, and 44 million merchants in 200+ countries and territories."

Visa is generating revenues anytime a Visa card is used for a transaction. It has 3 main revenue streams: (i) a 0.10% variable transaction service fee, (ii) a fixed $0.07cts per transaction data processing fee and (iii) a c.1.0% variable transaction fee on international transactions.

Between 2008 and 2018, Visa increased its operating margin from 40% to 65%.

Monday, Feb. 14th: Dan Shipper wrote about a note-taking productivity tool called Roam. Thanks to Julian Lehr for spotting this post on Twitter. - Every

Julian argues that it's impossible to build a successful VC-backed business on a single player productivity tool. You need to build a multiplayer tool because users churn from personal productivity tools. They want to introduce a change in their workflow but most of the time, the change does not stick and users will jump on the next hyped productivity tool.

"There are probably a host of reasons why this happened: Roam’s product velocity seems to be incredibly slow, there still isn’t really a good mobile experience, they’ve had well-documented community issues—the list goes on. But there’s one main reason that I don’t use it anymore: When I write my notes the thought, ‘Where am I going to put this?’ plagues me every time. It’s a direct and immediate pain. And it sometimes gets in the way of me even taking notes at all. I have this sensation many times a day and it’s deeply uncomfortable. Roam’s job was to get rid of that pain. And it did—for a while. But now it’s back."

Roam's main product innovation is to bring bi-directional linking to a note taking app (linking a note to another one and automatically create another link from the first note to the other) to easily structure your notes into networks and leverage these networks to generate new ideas. What happened in the end was that users tend to create numerous backlinks but are not coming back to their backlinks.

To bring Roam to the next level, it misses two pillars: (i) reducing the friction to create & search content and (ii) automating note-hierarchisation & thought networking.

Tuesday, Feb. 15th: Harvard Business Review wrote a post on framing great interview questions. - HBR

"It’s time to rethink your interview questions with a focus on work-related questions that are harder to prepare for and to fake an answer to."

You should keep some time to sell the job and the firm. A good trick is to ask: "what are the top factors that you’ll use to assess a job offer?" and to provide them with specific information on these factors.

You should evaluate whether they're forward looking by asking them: (i) an action plan for their first 3-6 months on the job and (ii) to forecast the evolution of the job/industry in which they are.

"Taking a “job content” approach, by having an applicant do some of the actual work, is the best way to separate top candidates from average ones."

Wednesday, Feb. 16th: Supercell shared some metrics on its annual performance in 2021. - VentureBeat, Supercell

It generated $2.24bn in revenues (51% growth YoY) and $852m in EBIT (84% growth YoY). It published 5 titles to date: Clash of Clans, Clash Royale, Brawl Stars, Boom Beach and Hay Day.

Supercell has 250m MAUs, recorded 5bn downloads and each game has generated more than $1bn in revenues (Clash of Clans and Clash Royale have even passed the $10bn threshold).

It builds games with small autonomous teams which take more risk and move faster than a centralised gaming company. To support global launches and live operations of successful games, Supercell now increases its live game teams to 25-30 people.

Supercell's last global launch was Brawl Stars in Dec. 2018. Since then, Supercell has launched no new game but has 3 games in beta at the moment (1 building game and 2 clash games).

Its mission is "to create games that as many people as possible play for years and that are remembered forever".

Thursday, Feb. 17th: Boxy raised a €25m series A led by Serena with the participation of existing investors LocalGlobe and CapHorn. Boxy is building autonomous convenience stores in containers which are deployed in rural areas where a classical store won't be profitable. It has deployed 25 stores in Ile de France. It needs 1 central warehouse to supply 30-40 stores. A store is opened 24/7 and has 250 SKUs. You enter the store via a QR-code generated on Boxy's mobile app and you will receive your invoice automatically after leaving the store. It plans to reach 60 stores by the end of 2022 (in Ile de France, Rhone Alpes and Hauts de France) and 1k by the end of 2025. Boxy will also double its workforce by the end of the year from 50 to 100 people. - RepublikRetail (in 🇫🇷), Tech.eu

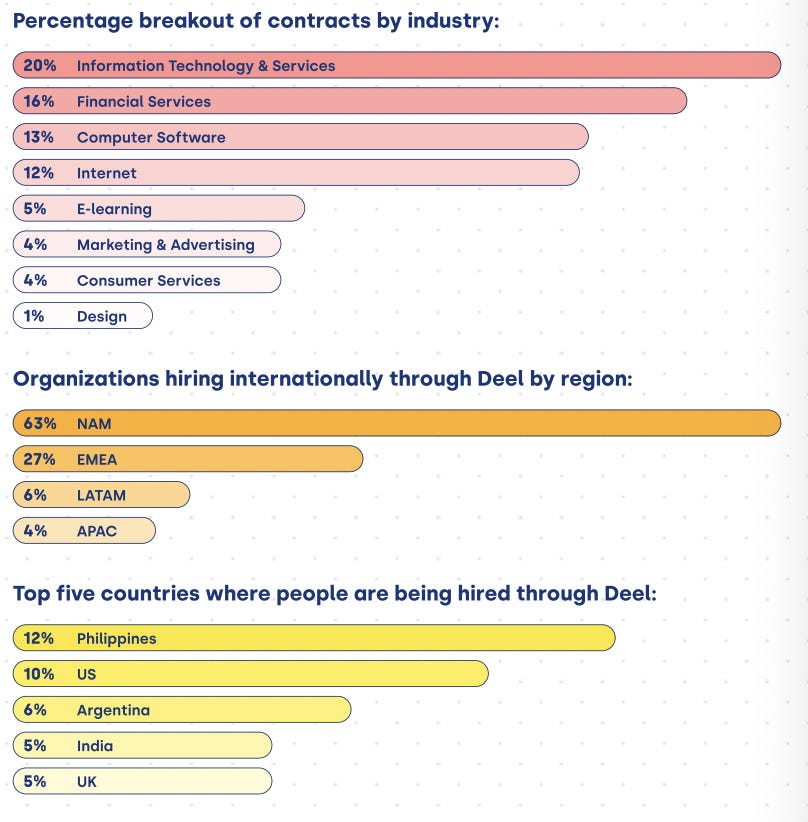

Friday, Feb. 18th: Deel published a report on the State of Global Hiring in 2021. - Deel

The top five roles hired through Deel are software engineer, account executive, quality assurance engineer, product designer and consultant.

52% of the remote workers paid in crypto via Deel live in LATAM. Crypto payments concerns only 2% of payments.

Remote work is having a real impact on salaries in certain emerging countries. For instance, in Mexico the average salary of people recruited on Deel increased by 57% between Jul. 21 and Dec. 21.

Most people hired via Deel work in the tech industry. 90% of Deel's customers are in North America or Europe. 12% of workers hired via Deel are in the Philippines and 10% in the US.

Saturday, Feb. 19th: Protocol interviewed Roelof Botha who is heading Sequoia's investing activities in Europe and in the US. - Protocol

Roelof is 48 year-old. He grew up in South Africa before moving to the US in his 20s. His first summer job was door to door salesman for Golden Products, selling products equivalent to Tupperware. He studied actuarial science and started his career at McKinsey. He joined Paypal in 2000, became CFO, took the company public at 28 and contributed to sell it to eBay in 2002. Michael Moritz recruited him to join Sequoia as a partner in 2003. At Sequoia, he invested into companies like Square, Youtube, Unity, MongoDB, Eventbrite and Instagram.

"That's part of the beauty of this business. Even though you could make big mistakes, there's another at bat tomorrow, because people are starting interesting new companies. So if you're willing to swallow your disappointment, buckle up, get back on the bicycle, get back on the horse, get back on your skis — whichever thing it is that you can identify with – you just try again.”

"Sequoia’s move, seeded by an idea from Botha, was to create the Sequoia Capital Fund, an evergreen venture model that will allow it to hold onto the stakes of its winners past the traditional 10-year VC fund clock."

"The new fund pools together LP money into a larger portfolio of publicly traded companies. The Sequoia Capital Fund then feeds a group of more traditional venture sub-funds, which return their proceeds — including shares of publicly traded companies, earned through IPOs, acquisitions or other deals — back into the main fund. Sequoia’s LPs have signed off on the idea, electing to roll over 95% of eligible balances to the new fund. After a two-year lockup, limited partners will be able to request to redeem some of their holdings twice a year."

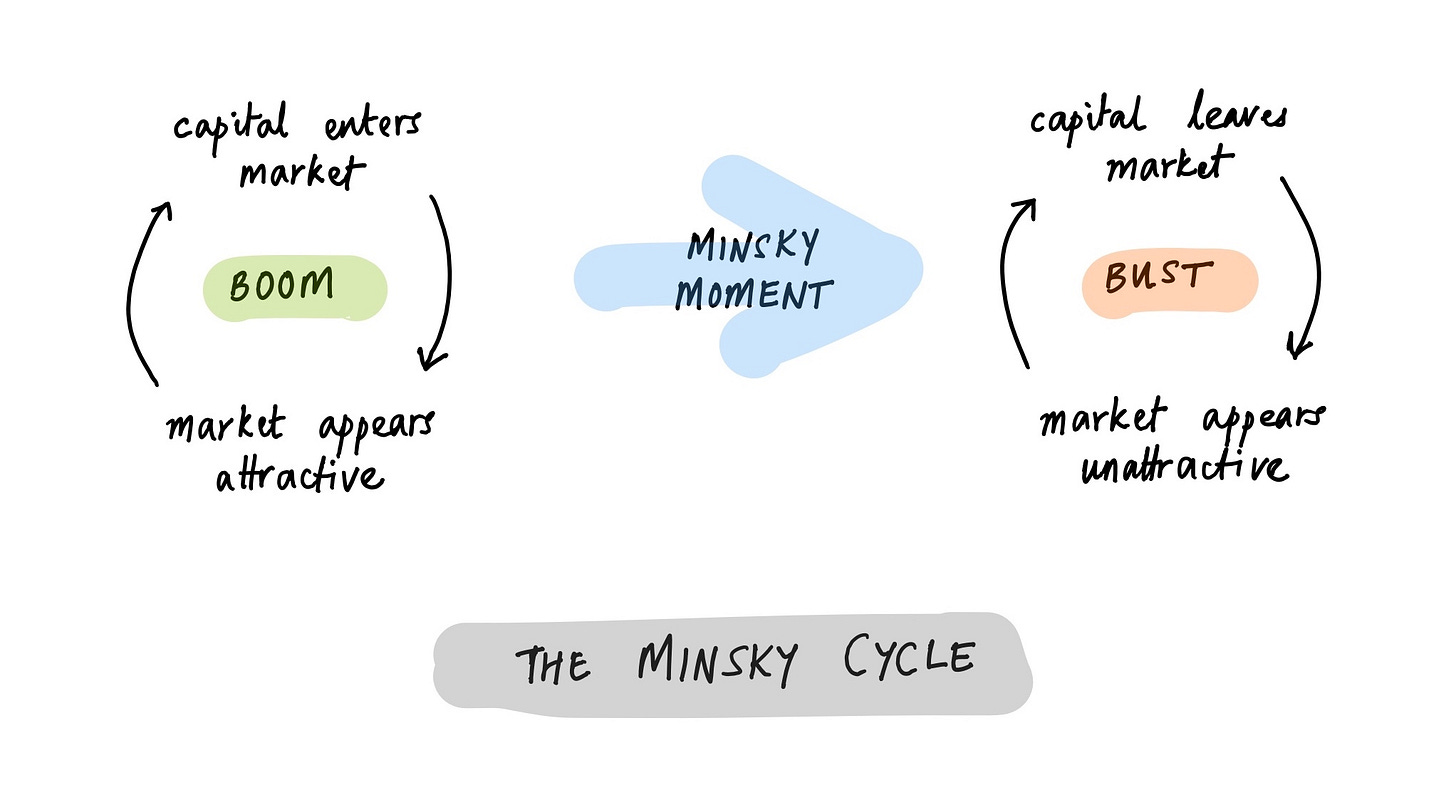

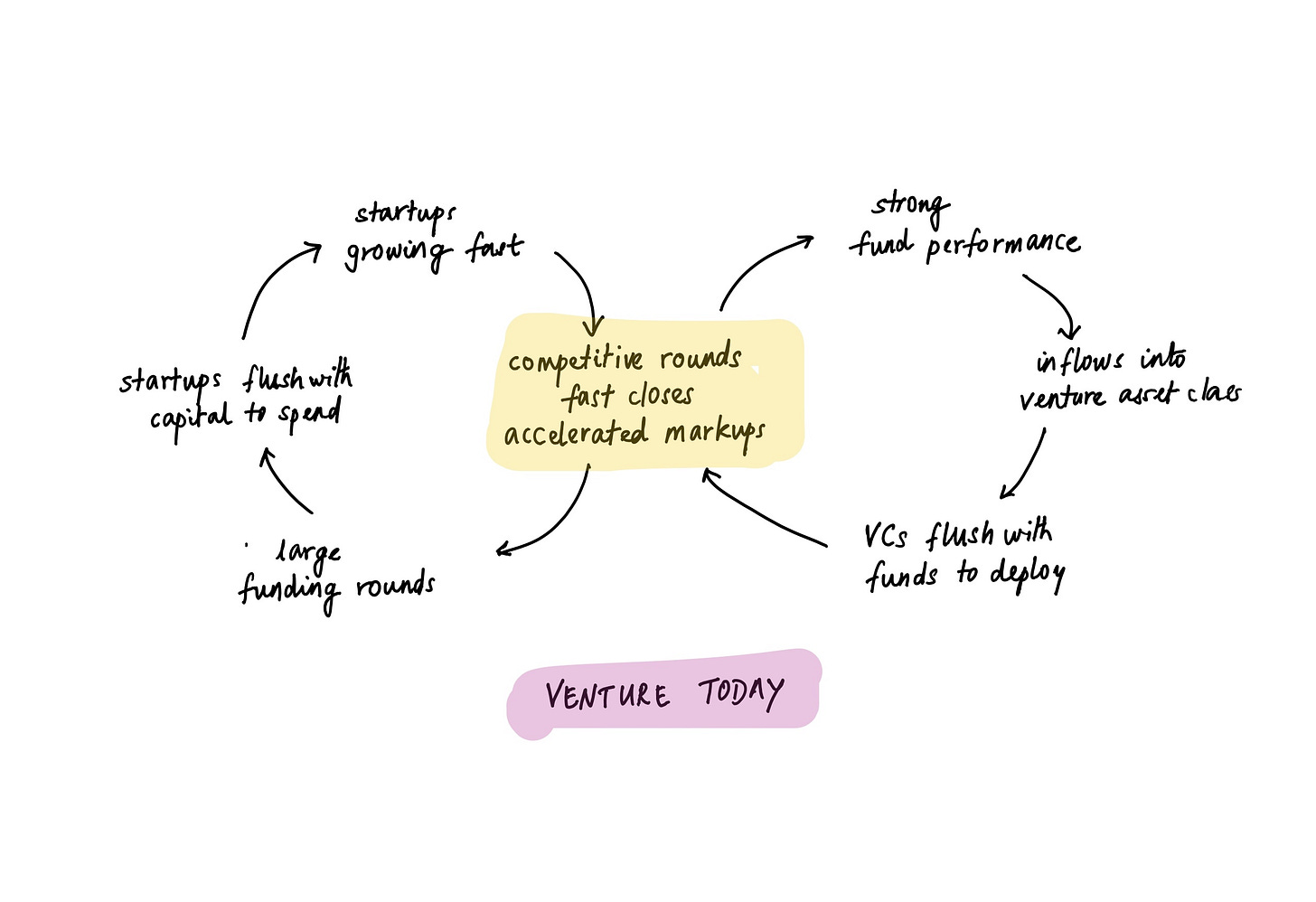

Sunday, Feb. 20th: I read a paper from Abraham Thomas (hedge fund manager) on Minsky Moments in Venture Capital. - Abraham Thomas

"Money entering a market boosts returns and reduces volatility, leading to very strong (realized) performance. This attracts more money, which improves performance even more."

"Minsky booms in an asset class that attracts a constant influx of new money, but it also needs that influx to continue marking up the price and marking down the risk of the asset class."

"The key Minsky idea is that increasing capital inflows reduce perceived risk."

Time has been compressed in venture capital: startups are marked up faster than ever, funds are deployed faster than ever and round are closed faster than ever. "Does the compression of timelines in venture change the distribution of terminal outcomes for venture-backed companies? If the answer is yes, then there’s no Minsky dynamic at play; what we’re seeing is a rational evolution of the venture industry. Maybe startups are truly less risky now; maybe the market truly has matured. More capital, lower returns, safer investments. If the answer is no, then venture is very possibly in a Minsky boom, and we’re just waiting for the moment when it turns into a Minsky bust."

"If compressed timelines are the driver of Minsky inflows into venture, then anything that delays funding cycles could precipitate a painful reversal. First some startups delay fund-raising because they need to grow into their valuations; then the VCs who invested in those startups have to delay their own fund-raising with LPs because they don’t have the requisite markups; then the LPs reconsider their (hitherto ever-increasing) allocations to venture because the latest returns are uninspiring; and before you know it, there’s an exodus from the asset class."

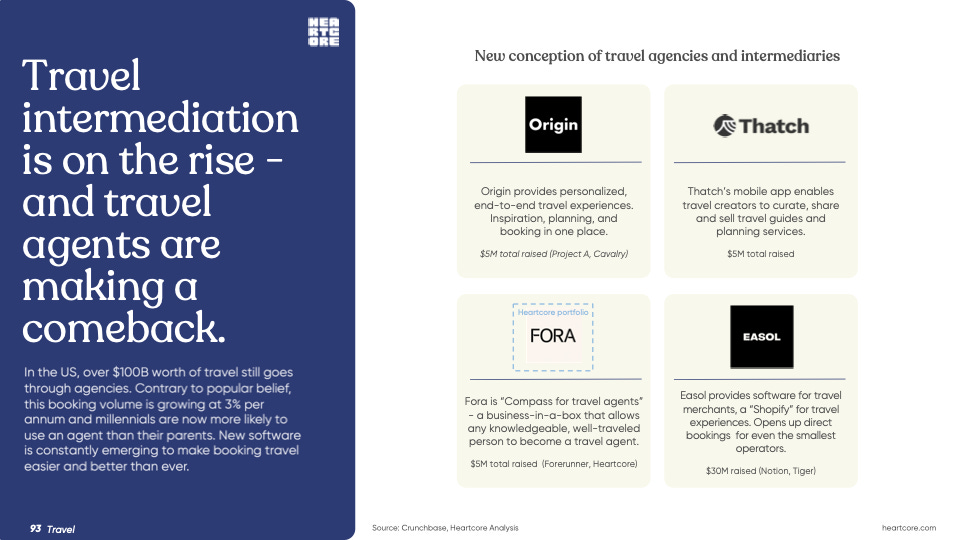

Monday, Feb. 21st: Heartcore published its 2022 annual report on consumer technology trends. - Heartcore

Keith Rabois is building OpenStore. "It aims to acquire one Shopify brand per day by using software to quickly evaluate, price and make offers to long tail merchants. It then uses its resources to bolster sales & improve margins of the acquired target. The long term vision is to ultimately combine all acquisition under one ecommerce brand."

Heartcore is bullish on digital restaurant franchises (Taster's new model) between delivery platforms and kitchen operators which is an asset light and high margin business in which you offer a turnkey solution to kitchen operators to get access to a food brand, a dedicated tech to run their operations and a easy to consume supply chain.

Tuesday, Feb. 22nd: I read a report on vertical SaaS from Fractal Software which is a startup studio specialised on vertical SaaS. Thanks Clément for sharing this report! - Fractal Software

Opportunities for a vertical SaaS to expand its TAM: increasing prices, upselling new features, adding financial services and embedding commerce.

Procore S1 data (vertical SaaS in the construction industry): $400m ARR (+38% YoY), 82% gross margin 10.1k customers, $43k ACV, 95% gross retention, 115% net retention, 29m CAC payback period on gross margin.

Leveraging M&A to expand into a new vertical: "it is more strategic for incumbents to acquire startups that have developed expertise in the area and have a foothold in the market instead of building competitive products from scratch."

I discovered a vertical SaaS for laundromats called Cents which raised a $4.3m seed round in Feb. 21 from Bessemer.

Wednesday, Feb. 23rd: UK-based pre-seed and seed fund Backed raised a €75m second seed fund and a €75m additional follow-on fund to keep investing into the best performing companies in the 1st seed fund. Backed launched in 2016. It invested into 67 companies, has 3 unicorns (SkyMavis, Thought Machine and Immutable X) and a meaningful exit (Hutch Games sold to MTG for $375m in Nov. 20). It raised from LPs like Groupe Bruxelles Lambert, Wilshire Associates, 20 family offices and 20 entrepreneurs. Backed has a 18-month founder support program "with leadership training, workshops, in-house recruiter, mental health service providers and an in-house executive coach for founders and leadership teams". It has also a scout program with 60 people across Europe. - Techcrunch, Tech

Thursday, Feb. 24th: Alloy raised a $20m series A from a16z. It builds an automation platform on top of the Shopify ecosystem. Alloy has 200 app connectors to create automated workflows (e.g. issue a refund when you receive support ticket in a given category, send a discount to loyal customers, etc.). It will use the funding to double the team size (from 20 to 40 FTEs) and expand to other ecommerce platforms beyond Shopify. - Techcrunch, a16z, Sacra

Friday, Feb. 25th: Zoomo raised a $20m series B extension led by Collaborative Fund. It's an Australian company founded in 2017 manufacturing and leasing e-bikes dedicated to the last-mile delivery industry. If you live in London or Paris, I'm sure that you've seen their ebikes on the street as Zoomo is slowly becoming a market standards for riders. It grew revenues 4x YoY in 2021 mainly driven by B2B deals with food delivery companies (UberEats, DoorDash, Gorillas, etc.). - Techcrunch

Saturday, Feb. 26th: Backbone raised a $40m series A led by Index. Gaming has massively shifted to mobile in the past decade. Backbone is a Iphone gaming controller to bring mobile gaming to the next level especially for mid core and hard core mobile games. It has also launched a subscription called Backbone+ which is a subscription offering to access additional features like recording or Twitch streaming. - Techcrunch, Index, Damir Becirovic

Sunday, Feb. 27th: I listened to a podcast interview of Alex Chesterman who is a repeat entrepreneur whose last business is Cazoo disrupting the European used cars market. - Riding Unicorns

Entrepreneurship is about attacking challenges that other people have not taken on, try to fix problems that other people did not solve because they were too hard.

Alex spent 10y in Asia and in the US opening restaurants in many cities. Alex launched 3 successful businesses (LoveFilm sold to Amazon, Zoopla which went public in 2014 and Cazoo which went public in 2021).

Starting a new business is hard work and is a long journey (7-year journey for both LoveFilm inspired by Netflix and Zoopla inspired by Zillow).

"I'm very consumer centric in all the businesses that I've started. [...] I'm attracted to the idea of using technology to improve consumer experience generally."

"In 2018, I saw Carvana in the States in online buying and selling of cars. We were not doing any of that in the UK. The experience was not a particularly great one. Carvana had a a better selection, better convenience, better quality, better transparency. It was just better on every dimensions. Carvana was a $4-5bn business when I looked at it in 2018 and today it's a $40-50bn business."

"All of [the businesses that I launched] have the same theme running through them: using a digital platform to significantly improve a consumer experience and also in a mass market (something we all do - we all rent films, we all buy properties and we all buy cars). I’m looking for a big market with a significant opportunity to disrupt what is not a brillant consumer experience"

I’m often asked: "What the hell do you know about used cars? The simple answer that I give is that I'm a consumer, I'm a customer of the business that I'm building. I'm the guy who has historically travelled 50 miles to go look at a car, to buy it, to decide not to buy it and waste half a day. Consumer businesses are the easiest to understand and to add value to because I'm the customer. As a result, if it's a problem that I try to solve for myself, I imagine that it's a problem other people are having too."

Alex has been a super active angel in the UK in the past 10y. He got into angel investing accidentally historically because nobody was funding startups in preseed and seed stages. He was giving advice to founders and telling them to raise an angel round instead of doing a roadshow with VCs. Angels were filling a void 10y ago which is no longer the case today with VCs specialised in pre-seed and seed.

"The types of businesses that I back are very similar to the types of businesses that I start which are big spaces, disruptive models and great teams."

"If I look at the investment decks of the businesses that I've started and the businesses that I ended up building, they're very different. If it's a big space, a smart team and they're doing something transformative, I don't really care about what the deck says. I want to give them time and money and oxygen to figure it out. You parachute a super smart team into an enormous space, they will figure it out."

Advice for entrepreneurs to build their business:

Keep things simple. Easier to communicate and to execute if things are simple.

Run fast. When you have a disruptive model, you often have a 1st mover advantage and land grad. The reason you beat incumbents is that you run faster than them.

Be decisive. Make decisions. Make 100 decisions per day. Hope that 90ish are great.

Monday, Feb. 28th: Insight raised a $20bn fund and has now $90bn of assets under management. Insight invests all over the world and opened a London office to cover Europe in 2016. - Techcrunch

Insight has a separate crossover fund investing in public and pre-IPO companies with a c.10 people team.

Insight has 350 FTEs inc. an investment team of 100 FTEs, a support team of 250 FTEs and 35 managing directors. In the support team, Insight has experts on all the functions needed to run a successful internet business (e.g. sales, marketing, product, pricing) that portfolio companies can access for free.

In terms of ownership, Insight tries to "own as much as they can". Insight is also not afraid to take control of companies that are not yet profitable.

"There’s so much capital on the sidelines that I don’t expect to see a total stop to investing, but it would not surprise me to see some slowdown over the next three to six months."

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋