🗞 Venture Chronicles - December 2020

Overlooked #52

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful tech news of December.

For 2020, I wanted to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for December!

Please note that the date picked for each event is not always the exact date of the event but the date I decided to write about the event.

Tuesday, Dec. 1st: Ankorstore raised a $29.9m series A led by Index to build the European Faire. It's a Paris-based B2B wholesale marketplace. It connects independent mom and pop stores with brands. Ankostore works with 2k brands and 15k shops and will expand in Europe in the coming months. (Techcrunch)

Wednesday, Dec. 2nd: Salesforce bought Slack for $27.7bn. On the public market, Slack was not performing as expected despite the rise of remote working caused by the covid crisis. It was struggling to compete against Microsoft. Salesforce is adding a new business line to its product offering and is acquiring a company that has been focused on being integrated in any workflow with multiple API connections to third-parties. (Techcrunch, Semil Shah)

Thursday, Dec. 3rd: Pigment announced that it raised $25m over two rounds with Blossom, Firstmark and Frst. It's a data planning company. It aims to disrupt Anaplan founded by Criteo cofounder Romain Niccoli and former Index investor Eleonore Crespo. The product has been live since October and now counts 6 customers. (Forbes)

Friday, Dec. 4th: VC-backed companies looking to acquire sellers on Amazon have raised almost $1bn in 2020 and Thras.io reached the unicorn status in July 2020. All these companies have raced to raise capital in 2020. 2021 will be the year in which they will figure out how to scale and how they will differentiate (e.g. focus on a certain category, doing minority vs. majority investments in brands, building inhouse tooling etc.) Interestingly, these players play on a multiple arbitrage: they buy businesses at 2.5-4x EBITDA and they wish that the aggregate will be valued at a much higher multiple. (Marketplace Pulse)

Saturday, Dec. 5th: Ukranian-based face-swap mobile application Reface raised a $5.5m seed round from a16z. The round also includes prominent European consumer business angels like Ilkka Paananen (CEO at Supercell) and David Helgason (founder at Unity). It's probably one of my favourite stories of 2020. 7 cofounders in Ukraine launched the app in January. 3 of them have been working on the technology for almost a decade. It went viral all over the world (70m downloads) and U.S. investors went crazy to try to invest in the company. This round combines everything I love in venture: resilience pays off, you can innovate from everywhere, exponential growth. (Techcrunch)

Sunday, Dec. 6th: I listened to an Invest Like the Best's podcast episode with Laura Behrens Wu who is the cofounder and CEO of Shippo. It's a U.S. based company backed by Bessemer and USV. Shippo has built an API and a web application to help online merchants manage their shipping and get access to the best shipping rates from multiple providers. It's a gold mine for anyone working in ecommerce or/and building an API based business. (Invest Like the Best)

Fundamentally, Shippo is an API but the product is distributed both through API and a web application. 20% of the customers use the API but make 80% of the transaction volume. 80% of the users are using the web application but make only 20% of the transaction volume. Shippo is a mix between Stripe which only sells to customers who know what an API is and Square who sells to small merchants who don't have technical knowledge and want an interface.

When you build an API aggregating other APIs (like Plaid in financial services, Impala and Duffel in the travel industry, Vivenu in ticketing), you don't control the other APIs but you will be held responsible if the calls are not working.

In ecommerce, shipping is the convergence point between the offline and the online world which is a source of numerous frictions: how do you make make sure that the shipping information is regularly updated online? how do you manage edge cases?

Shippo has a two-sided business model: (i) customers pay to get access to the API and (ii) the company resells shipping rates negotiated directly with carriers.

Monday, Dec. 7th: EQT led a $50m series B into French household insurance startup Luko. Existing investors Accel, Founders Fund and Speedinvest also participated in the round. The company has sextupled its revenues since its series A and has now 100k policyholders. It's EQT's first investment in France since the opening of a local office back in June 2020. Luko brings transparency to the insurance market. It has a clear business model in which 30% of the premium covers the operating costs and the remaining 70% is pooled to cover compensations. Any premium left in the pool is donated to charities chosen by customers. The company built its own hardware to offer its customers home management tools to reduce their consumption and prevent disasters. Another interesting fact is that Luko is also part of this wave of French startups that are B-Corp which is a certification for companies that are following strict guidelines to have a better social and environmental performance. (Tech.eu, Rania Belkahia)

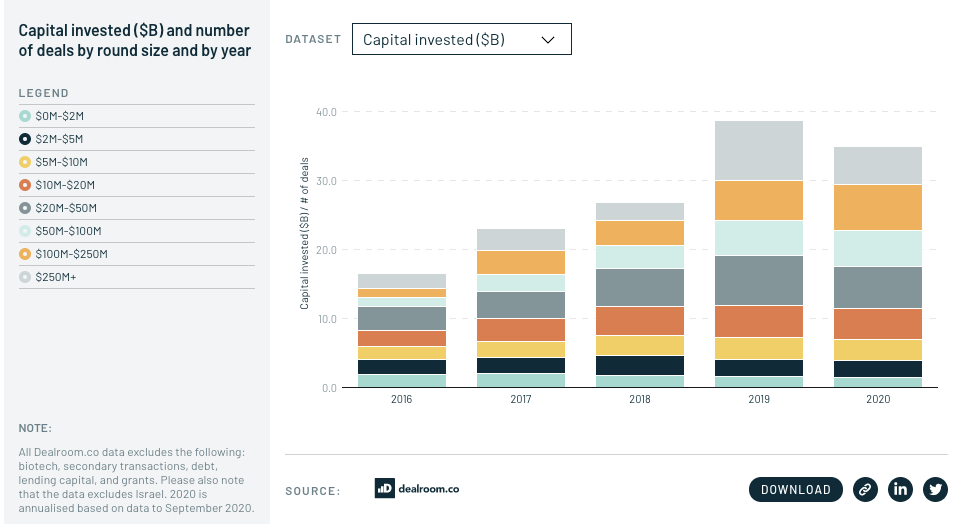

Tuesday, Dec. 8th: Atomico published its 2020 edition of the State of European Tech.

In Europe, so far $35bn have been invested into startups in 2020. At the end of the year, this amount could exceed the $40.8bn invested in 2019. It is a great sign of resilience for the European tech industry.

Looking at the breakdown per round size, we understand that capital has been concentrated into (i) seed and series A startups that will need to find product market fit or demonstrate a strong ability to grow and (ii) late-stage high quality assets that are able to raise megaround. There is a valley of death for companies that plan to raise series B/series C between $20m and $50m without strong metrics.

Median seed (from $0.7m in 2016 to $1.2m in 2020) and series A ($3.9m to $6.6m) round sizes increased. Investors are willing to fill the funding gap between early stage rounds in the US and in Europe.

More US investors than ever have invested in the European ecosystem: from 405 investors in 2016 to 552 in 2020. I don't believe that US investors are coming to Europe for price arbitrage. They come because we have world-class founders who have the ambition to build worldwide category leaders.

Atomico and Dealroom worked on the European startup funnel from seed to $1bn with 1,064 companies that raised a seed round between 2010 and 2013. In these dataset, 1.22% of Europe companies which raised a seed round have become unicorns.

In Europe, there are 115 VC-backed companies that have passed the $1bn valuation threshold including 13 companies that have done so in 2020 (Arrival, Bolt, Cazoo, Dataiku, Hopin, Lilium, MessageBird, Mirakl, Mollie, Pipedrive, Snyk, Talkdesk and Workhuman). Hopin (17 months) and Cazoo (18 months) have been the two companies that have scaled the fastest to a $1bn valuation in European tech history.

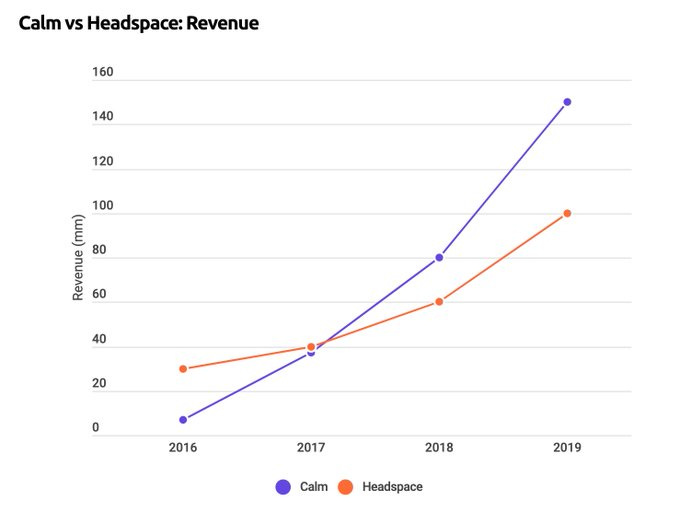

Wednesday, Dec. 9th: Calm raised $75m from existing investors Lightspeed, TPG and Insight at a $2bn valuation. Goldman Sachs and Marc Benioff are also investing into the company. Calm has 100m downloads and 4m paying users. The company has been profitable since 2016 and has doubled its number of daily downloads YoY. Calm was started two years after its main competitor Headspace but has progressively overtaken it. The company has expanded its user-base through B2B partnerships with corporations offering the premium version of the app to their employees or key services like Amex or Kaiser Permanente who are doing the same for their users. Calm was also a first mover to expand its total addressable market by going after a broader category than meditation by tackling the sleep pain point. The company plans to keep growing by (i) doing M&A and (ii) localizing its content to better serve non English speaking markets. (Jon Ma, Techcrunch, Bloomberg, Patricia Mou)

Thursday, Dec. 10th: Gorgias raised a $25m series B at a $300m pre-money valuation led by Sapphire Ventures. Existing investors Alven, CRV and Greycroft also participated. It's a verticalised customer support software for the ecommerce industry. Gorgias works with 4.5k stores and tripled its revenues in 2020. The company benefited from the rise of ecommerce during the covid crisis. It’s also another illustration of a company that has piggybacked Shopify to fuel its initial growth. (Gorgias, Alven, Techcrunch)

Friday, Dec. 11th: Tink raised a $85m round co-led by Eurazeo Growth (💙) and existing investor Dawn Capital at a $680m valuation. It has become the European reference player when it comes to open banking. Tink works with 3.4k banks in 13 countries covering 250m customers and 8k developers are using its API. The company will use the additional funding to expand its product offering with a focus on adding a smart data layer to raw banking data and on its payment initiation offering. (Techcrunch)

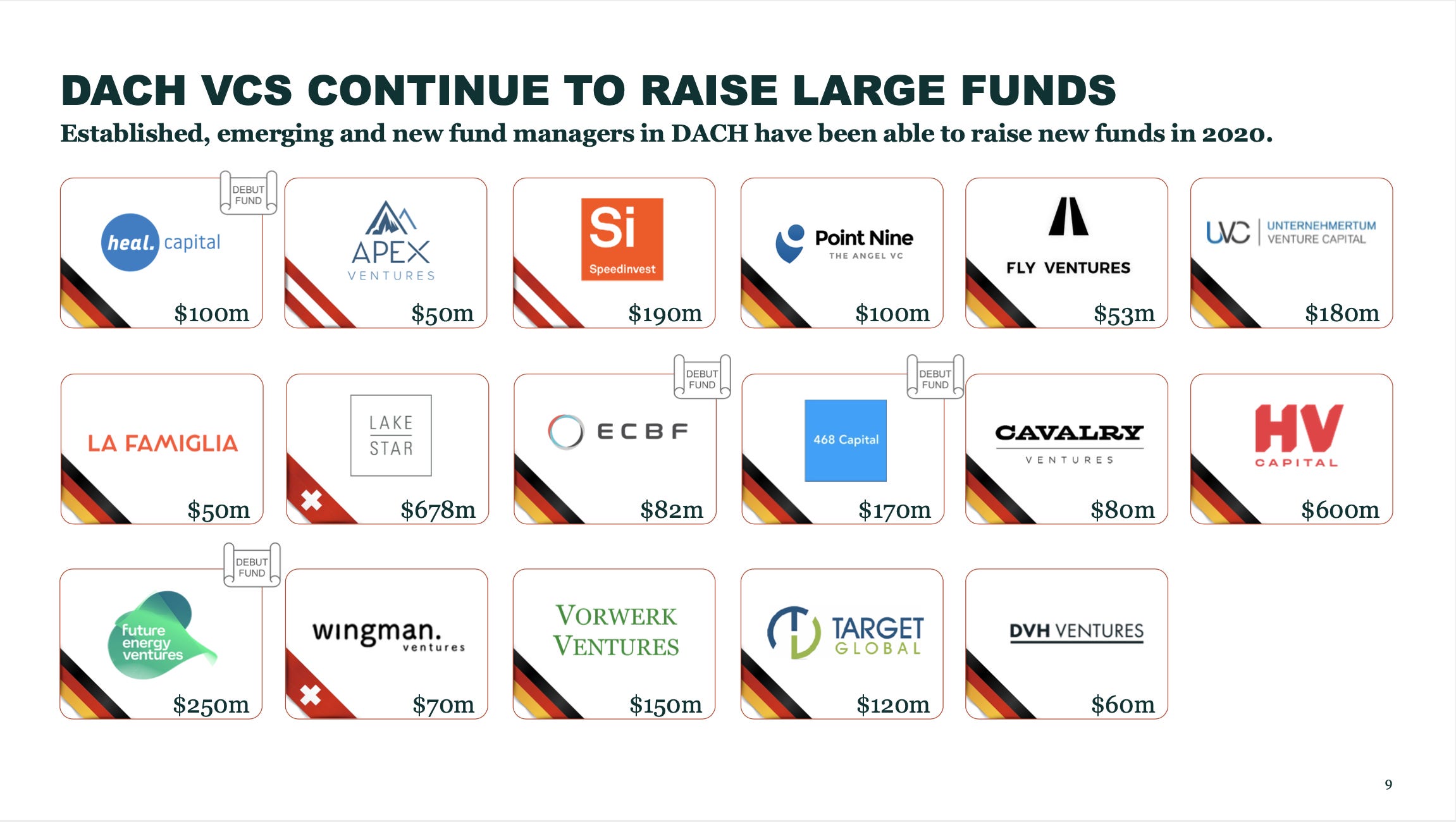

Saturday, Dec. 12th: Frontline and Speedinvest released a report on venture funding in the DACH region. (Frontline)

DACH venture houses have raised numerous new funds in 2020 including P9, Speedinvest, Target, HV and Lakestar.

They have a good snapshot of the most valued companies in the region with startups like Delivery Hero (€20.5bn), Zalando (€16bn), HelloFresh (€7.1bn), TeamViewer (€5.3bn), Veaam (€4.5bn), N26 (€3.2bn), Auto1 (€3bn) and Celonis (€2.3bn).

It's noteworthy that many covid-positively impact startups have already raised a funding round in 2020.

Sunday, Dec. 13th: German-based goPuff copycat Gorillas raised a $44m series A lat a $200m post money valuation led by Coatue. The company delivers groceries in less than 10 minutes in large cities like Berlin, Cologne and Amsterdam. Gorillas had previously raised a €1.2m seed round with Atlantic Labs back in August 2020. They have a super agressive growth plan. The goal is to be in 15 cities across Germany and Europe as well as to operate 60 fulfilment centers by the end of Q2-2021. (Techcrunch)

Monday, Dec. 14th: SBI - a Japanese financial group - acquired London-based crypto market and OTC trading desk B2C2. Back in July, SBI acquired a minority stake in the company and started to provide its customers access to the B2C2's platform. Since then, B2C2 has increased its over-the-counter volumes by 4x and has launched a prime brokerage offering. It's a great conclusion for a 2020 year that was marked by consolidation in the crypto sector. (The Block)

Tuesday, Dec. 15th: I read a long form interview with Klarna's CEO Sebastian Siemiatkowski about the history of the company and its upcoming challenges. (Techcrunch)

In May, 2010, Sequoia led Klarna's series B for a 25% stake in the company at a $100m valuation. In September 2020, Klarna raised a $650m round at a $10bn pre money valuation.

Sebastian still owns a 8.1% stake of the company. His two cofounders left in 2012 and 2015.

Klarna obtained a full banking licence in 2017 and offers debit cards and saving accounts in Germany and Sweden.

Sebastian almost took Max Levchin (ex-Paypal cofounder and CTO) as advisor before learning that he was launching a Klarna's clone (Affirm) in the US.

Klarna's initial product was an invoicing solution. The merchant was paid upfront but the customers have 30 days to settle their invoice. The idea was to have 30 days to make sure that (i) you don't have any problem with the product ordered and (ii) you are able to return it before having to pay for it. Klarna added its instalment product only later.

Wednesday, Dec. 16th: Pia d'Iribarne and Jean de la Rochebrochard are launching a new European seed fund called New Wave. Jean will continue to run Kima (Xavier Niel's investment arm) in parallel. It's a €50m fund raised in less than 3 months with prominent individuals like Yuri Milner, Philippe Laffont, Peter Fenton, Xavier Niel, Antoine Martin, Alexandre Yazdi. New Wave will sign tickets between €0.5m and €2.0m in European seed stage startups. It will also have a collaborative approach coinvesting with other seed funds and business angels. (Techcrunch)

Thursday, Dec. 17th: Lydia raised a $72m round led by Accel to build the European financial super app. The investment is led by Amit Jhawar who was Venmo General Manager before joining Accel as a partner. Initially, Lydia was a P2P payment app and has progressively added layers to become a super app. The company has now 4m users in France and transactions have doubled in the past 12 months. 30% of people under 30s have a Lydia account in France and Lydia has become a verb meaning “to wire money to a friend”, similarly to Venmo in the US. This round is an extension of the round led earlier this year by Tencent. I hope that this will be the right attelage to bring the company to the next level and eventually succeed in the vision they have been building towards since 2013. (Techcrunch, Accel, Sifted, Lydia 🇫🇷)

Friday, Dec. 18th: Uxtools published its 2020 Design Tools Survey (4k answers) with great insights on the design market. Below are my notes on the report:

There are clear winners in the designer toolbox: (i) Figma used for UI design by 66% of the respondents (vs. 37% in 2019), (ii) Miro used for brainstorming by 33% of the respondents (vs. 5%), (iii) Maze used for user testing by 13% of the respondents (vs. 5%).

It's now obvious that Figma is used by numerous designers as their primary and single platform to cover the whole design value chain from brainstorming to prototyping and testing.

Digging into the tools that designers are the most excited about for 2021, I notice several trends: collaboration (Figma, Notion), no-code (Webflow), design systems (Zero Height), UI-component builders (StoryBook) and 3D tools (Blender).

Saturday, Dec. 19th: Disney+ reached 86.8m paying subscribers (vs. 60-90m subs forecasted for 2024). The company plans to turn its model upside down to support its streaming service as key revenue driver going forward. It's a radical shift. It shows how powerful subscription is, how the streaming market is mature but also how powerful Disney IPs are. (Protocol)

Sunday, Dec. 20th: Cyberpunk 2077's release was a disaster. It's an open world in a science fiction universe published by Polish gaming studio CD Projekt (known for the Witcher games) that has been teased for almost a decade to fans. The game is almost unplayable with countless number of bugs. Xbox and Playstation have offered refunds to their users and Playstation has even withdraw the game from its store. The game had already been delayed several times. It seems that the studio set expectations for the game that were too high compared to its technical abilities and that the culture has become messy over the past few months. (The New York Times)

Monday, Dec. 21st: Mail exchanges between Instagram cofounder Kevin Systrom and Facebook cofounder Marc Zuckerberg about the Instagram's acquisition are now publicly available. (U.S. Judiciary House) Below are my favorite quotes:

"In many ways we are aligned. We both believe in the power of mobile to change the way people share information. We see the transformation happening very quickly as people adopt new products like Instagram, etc. We are both, at our core, engineering driven in vulture and vision. We both have a passion for social products, and realize that building what we're building can (and have the responsibility to) positively influence culture and the world at large." - Kevin

"I'm curious what you think you couldn't do at Facebook, given that what I offered was for you to keep building Instagram as a separate product and brand. I actually think you'll be able to do all the same things with Instagram at Facebook plus you'll have more distribution firepower behind you, so there will be a bigger chance anything your do takes off." - Marc

"The process began with you asking if we'd do this at $500m, but then you didn't end up doing it at that valuation. I am curious to know at what valuation you would do this, and then I can just let you know whether we'd do that." - Marc

"Also, just to be clear so I don't wast your time here, I can't get to $2 billion. But if you're open to doing something in the range structure we discussed last night, with an earn-out valuing Facebook aggressively etc, then I'm optimistic we can do something - especially since we both seem to want to work together." - Marc

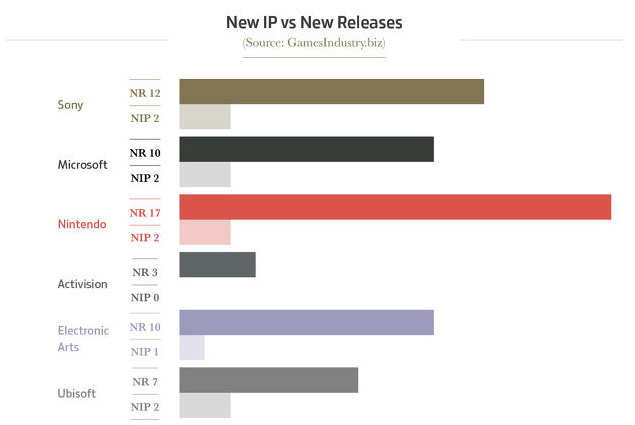

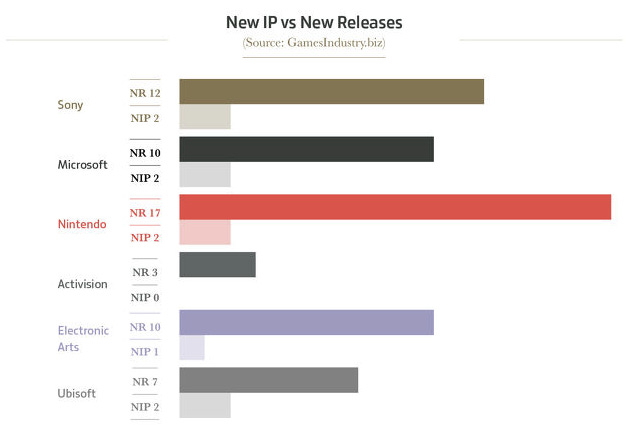

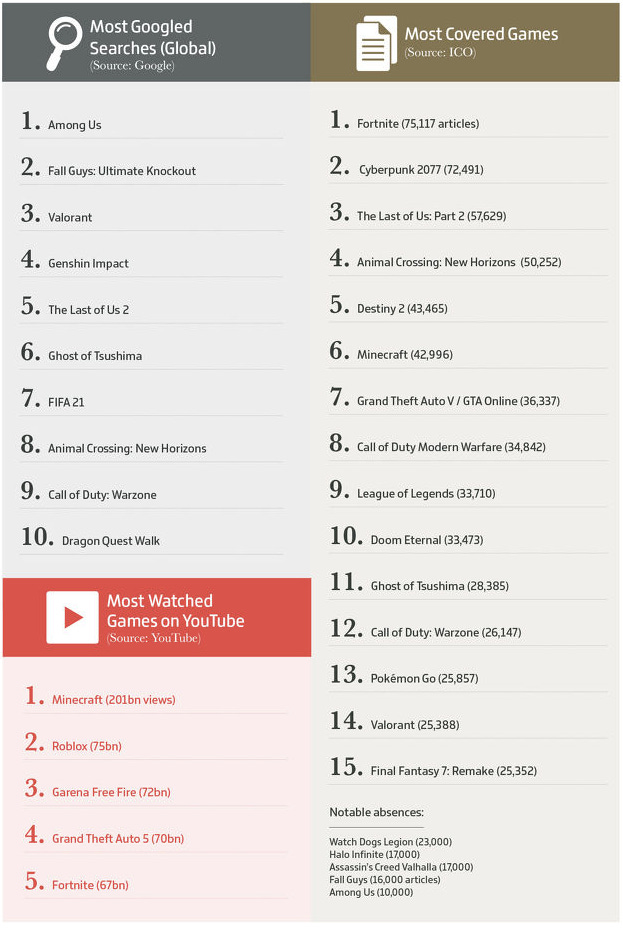

Tuesday, Dec. 22nd: Games Industry released an infographic on the gaming market in 2020. (Games Industry)

The best selling games in the US are mostly new releases of well known franchises like Call of Duty, Assassin's Creed, Final Fantasy, Mario, Animal Crossing, etc.

This trend is confirmed by the breakdown between new IPs vs. New Releases of existing IPs from main game developers.

AmongUs, Valorant, Animal Crossing and Cyberpunk were the blockbusters I have heard the most about this year and I was not completely wrong.

Hyper casual games publishers are gathering more downloads than any other player in the industry without having worldwide massive hit nor revenue generating machines. The top 5 games in terms of revenues are all mobile first and are all generating more than $1bn in sales.

Wednesday, Dec. 23rd: Top U.S. Youtuber MrBeast (48.7m subs) launched a virtual burger chain called MrBeast Burger. (Creator Economics)

MrBeast partnered with Virtual Dining Concepts. They don't rely on dark kitchens but have worked with 300 local restaurants across the countries.

You can order from MrBeast Burger on all delivery apps (DoorDash, Ubereats, Postmates etc.) as well as on the proprietary MrBeast Burger app. The difference is that the delivery radius is higher (9 miles vs. 3 miles) when you order on the MrBeast Burger app.

It was an instant hit with only one video and several post on social medias. The app was downloaded more than 1m times. The restaurants were overwhelmed by orders. They faced two main operational challenges: quality control issues with some restaurants and not enough drivers to deliver all the burgers ordered.

It's a great example of a creator leveraging his community to launch a new business line and truly becoming a "multi-SKUs" creator.

Thursday, Dec. 24th: Nicolas Brusson wrote a paper on Blablacar's startup mafia with interesting metrics: 30 startups created by former employees, 9 of them raised €23m in total, 3.75y average tenure at Blablacar, 1/3 entrepreneurs are female. He also shared what were the key success factors to build a mafia: recruiting entrepreneurial mindset, having a strong culture and fostering peer-learning. Another point is that Blablacar's founders are super involved in the French tech ecosystem as investors, mentors and members of tech associations (Fred Mazella is at France Digitale, Francis Nappez is cofounder at TechRocks). (Nicolas Brusson)

Friday, Dec. 25th: Dija raised a $20m pre-anything round led by Blossom to build another goPuff's copycat in London. Dija is cofounded by two former senior executives at Deliveroo. We don't know that much about the company expect that they will deliver both fresh food and convenience products. They will operate local fulfilment centers and offer ultra fast delivery. (Techcrunch)

Saturday, Dec. 26th: I read a brillant paper on Masterclass. The company was started in 2012. It launched in 2015 with only 3 classes (Serena Williams on tennis, Dustin Hoffman on acting and Patterson on writing). It has now 85 classes across 9 categories. With covid, both usage and downloads have increased significantly in the past few months. I love how the article frames Masterclass's targeted audience: people in their thirties who have started their careers but realized that they don't have a fulfilled life. Masterclass is a great product to find inspiration for your next career move. (The Atlantic)

Sunday, Dec. 27th: I found a table on the evolution in the usage statistics of content management systems. Guess what? Wordpress is still gaining market shares: 39.5% websites are powered by Wordpress vs. 35.4% at the beginning of the year. Shopify and Wix are also winning market shares but have still a penetration rate below 4%. Interestingly, the JAMstack (Gatsby with a 0.2% market share, Hugo with a 0.1% market share) and the no-code (Webflow with a 0.2% market share) trends are visible in the detailed ranking. (Web Technology Surveys)

Monday, Dec. 28th: Polish edtech startup Brainly raised a $80m series D with Learn Capital, Prosus Ventures, Runa Capital, MantaRay, and General Catalyst Partners. Its userbase has grown from 150m users in 2019 to 350 in 2020. Brainly is a platform allowing students and parents to ask other people with help to answer homework questions. (Sifted)

Tuesday, Dec. 29th: Seedcamp shared its 2020 annual review. They did 36 new investments in 11 different European countries (vs. 5k applications), raised a new £78m fund V and added Hopin in their portfolio of unicorns. (Seedcamp)

Wednesday, Dec. 30th: Ryan Selkis (CEO at Messari) released its 2021 crypto thesis. It's a 130-page document. It looks back at what happened in the crypto space over the past 12 months and it makes predictions for 2021. (Messari) Bitcoin, DeFi and stablecoins made the headlines in 2020:

Bitcoin has finally become mainstream in the institutional finance world. Against the covid crisis, central banks have stepped in, printing money and rising the states’ debt to unprecedented levels. Several well know money managers and financial institutions have started to include Bitcoin in their portfolio.

Financial use: explicitly geared towards financial applications such as lending, exchange, derivative / synthetic asset issuance, asset management, etc

Permissionless: open-source; anyone can use or build on top of the projects without asking permission from a third party

Pseudonymous: no need for people to reveal their identities to use the protocols

Non-custodial: not reliant on third-party facilitators

Decentralized governance: decisions and administrative privileges are not held by a single entity or a credible path exists towards removing them

The Decentralized Finance (DeFi) space has been booming this year going from $1bn to almost $15bn in value locked with several projects under the spotlight like Maker, Compound, Uniswap or Aave.

The stablecoin supply has expanded from $5bn to $20bn. If inter-exchange settlement remains the primary use case, lending has become more mainstream.

Thursday, Dec. 31st: Semil Shah (cofounder and GP at U.S. based VC firm Haystack) wrote a retrospective on 2020. It's a great synthesis for this unbelievable year. (Semil Shah)

The mindset shift in the tech industry following the covid crisis was impressive from the fear of new global financial crisis to all-time high stock prices and unprecedented competition in venture.

New consumer behaviours emerged like: ordering food on Instacart and DoorDash, buying products on Shopify's merchants websites, signing documents on DocuSign, running away city centers in countrified Airbnbs, and working and studying on Zoom.

Innovations have invaded the venture industry: (i) SPACs, (ii) rolling funds, (iii) solo GPs.

"The final 2020 stew in the cauldron is a potent mix: A public health crisis, which triggered economic crisis, social crisis, and a mental health crisis, with a side of climate change crisis."

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋