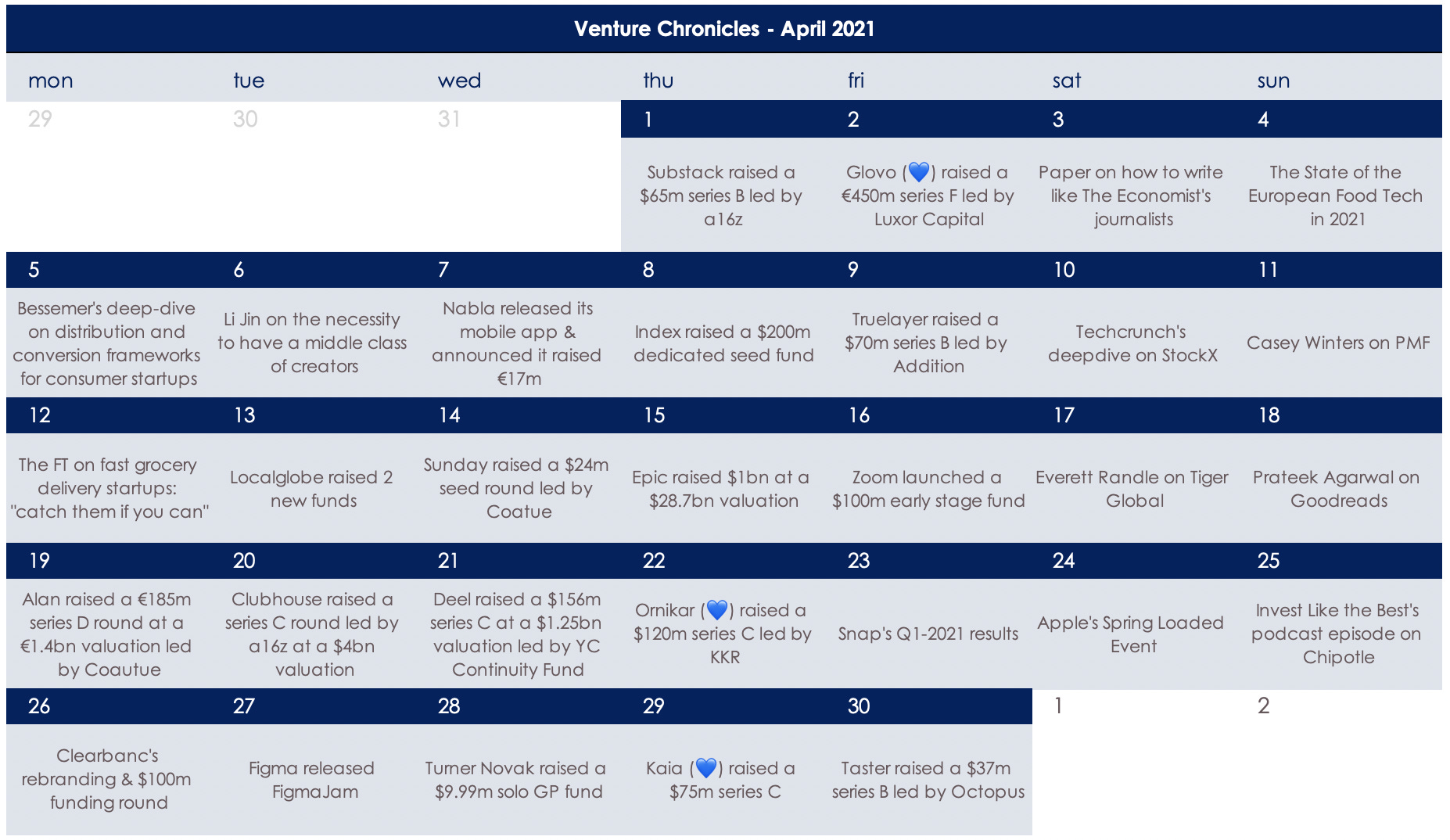

🗞 Venture Chronicles - April 2021

Overlooked #68

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful tech news of April.

For 2021, I wanted to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for April!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Thursday, Apr. 1st: Substack raised a $65m series B led by existing investor a16z (Andrew Chen) at a $650m valuation. The company started in 2017 proved that (i) people were willing to pay a subscription for a newsletter and that (ii) the media industry had a shot at rebuilding its business model around subscriptions and away from advertising. 500k people are paying for a newsletter on Substack and the top 10 writers are generating more than $15m in revenues per year. Substack will use the funding to support its writers with better publishing and monetization tools as well as with financial support to grow the next generation of writers. - Substack, Andrew Chen, FT

Friday, Apr. 2nd: Our portfolio company Glovo (💙) raised a €450m series F led by Luxor Capital with the participation of Delivery Hero, Drake Enterprises and GP Bullhound. Glovo has 10m users in 20 European markets. From day 1, Glovo chose multi-category positioning. You can order anything from Glovo as long as it fits in the bag of a rider. The company talks about "q-commerce" i.e. the delivery of items to urban consumers in less than 30 minutes. Glovo was also a dark stores pioneer in Europe. It operates dark stores to sell items on the behalf of large retailers like Carrefour or Continente with Glovo's delivery network. - Techcrunch

Saturday, Apr. 3rd: Ahmed Soliman wrote a paper on writing lessons learned from The Economist's journalists. - Ahmed Soliman

When you write, you should clearly state the main idea of a paragraph in the first sentence and expand on it in the following ones.

You should use precise words. "The Economist’s choice of verbs, nouns, and adjectives creates a strong mental picture and explains exactly what’s at stake."

You should play with the rhythm in your sentences. "Similar to when people shift their attention to a satisfying beat, adding a rhythmic structure captures readers and tickles their brains"

Sunday, Apr. 4th: In partnership with Five Seasons, Dealroom published "The State of the European Food Tech in 2021". - Dealroom

It divided the grocery delivery market into 5 categories: food delivery companies entering groceries (Deliveroo, Takeaway), personal shoppers (Everli, Wolt), online grocery retailers (La Fourche, Ocado, Pic Nic), meal kits (Gousto, HelloFresh) and instant grocery (Dija, Cajoo, Gorillas).

It broke down the cloud kitchen market into 3 categories: (i) virtual restaurants, (ii) real-estate partners, (iii) virtual franchises.

Monday, Apr. 5th: Bessemer wrote a deep-dive on distribution and conversion frameworks for consumer startups. - Bessemer

Most successful consumer startups have reached massive scale mainly through organic acquisition. Your distribution cannot only rely on the three largest digital advertisers which are Google, Facebook and Amazon (90% of U.S. digital advertising). Distribution is not everything. You should have an efficient conversion to turn your new users into engaged and successful users.

"Social proof is a well-observed consumer behavior where people mirror the actions of others in an attempt to reflect correct behavior for a given situation". -> Linktree, Lu.ma

"“The Etsy Effect” is a phenomenon that occurs when a seller promotes their own content or product from a marketplace, and in turn, organically brings in new consumers that purchase not just from the seller but also from the entire marketplace." -> Etsy, Poshmark

Desintermediate advertising platforms by working directly with influencers to promote their product. -> Gymshark, Cameo

New platforms are always a source of opportunities. You can have either a mega platform shift (going from radio to TV to mobile) or alternative online advertisers which start to have an interesting userbase (e.g. Snap, Discord, Clubhouse, TikTok, Pinterest etc.)

First order irrational, second order rational. "A company can disrupt a market by doing something that seems completely irrational at face value but has some second order result that is extremely beneficial to the company and creates an exceptional business model." -> Robinhood

"Consumer companies can leverage scarcity and hype around product launches to leverage the well-studied psychological behavior of fear of missing out." -> Clubhouse, Roam

Tuesday, Apr. 6th: I took the time to read Li Jin's paper in HBR about the need to create a middle class for the creator economy. - HBR

"On Patreon, only 2% of creators made the federal minimum wage of $1,160 per month in 2017. On Spotify, artists need 3.5 million streams per year to achieve the annual earnings for a full-time minimum-wage worker of $15,080, a fact that drives most musicians to supplement their earnings with touring and merchandise."

"On Spotify, the top 43,000 artists — roughly 1.4% of those on the platform — pull in 90% of royalties and make, on average, $22,395 per artist per quarter. The rest of its 3 million creators, or 98.6% of its artists, made just $36 per artist per quarter."

"In 2018, the top game on Roblox accounted for 8 to 10% of concurrent users, whilst in 2020, the top game accounts for upwards of 20 to 25% of concurrent users."

"Streamloots enables gaming livestreamers to monetize their superfans to an even higher degree: The average buyer spends $26 per month on digital interactions with streamers on Streamloots vs. $6 on Twitch subscriptions. For streamers who use both platforms, Streamloots accounts for 62% of total earnings, yet only 27% of purchasers."

In the creator economy, most earnings and engagement are concentrated amongst the top creators. We need a middle class of creators to drive innovation and make the creator's journey less volatile. Platforms should play a key roles to promote this middle class and Li is sharing strategies to do so: empowering niche content, add randomness in recommendation algorithms, reduce the friction to the rise of collaboration and communities, provide capital to emerging creators, help creators to capitalize on their superfans who have a higher monetization potential and invent a form of universal basic income for creators.

Wednesday, Apr. 7th: Nabla released its mobile app to help women in their healthcare journey and announced it raised €17m in funding from Xavier Niel, Artemis, Rachel Delacour, Julie Pellet, Marc Simoncini and Firstminute. Nabla offers several healthcare services to women including the ability to chat with doctors, community content, a place to centralize all you medical data. In the future, Nabla will also offer telemedicine appointments. Nabla's founder Alexandre Lebrun is part of a French mafia that I've recently discovered with the Virtuoz's journey. It was a AI-based chatbot for retailers way before chatbots were something. - Techcrunch, Simon Dawlat

Thursday, Apr. 8th: “We never say it’s too early for Index” has always been a motto at Index which has signed the first cheque in companies like Robinhood, Figma, Deliveroo and Wise. Index is now doubling down on this stage and raised a $200m dedicated seed fund called Index Origin. - Techcrunch, Index

In the past 18m, Index made 35 seed investments. All if Index's partners are entitled to sign seed checks. The fund is generalist and will be invested mainly in Europe and in the United States.

Index will have a collaborative approach at seed stage partnering with other seed funds and/or with business angels.

Index will offer dedicated services to seed companies including: (i) support to make the first hirings, (ii) access to a network of potential customers to accelerate towards product market fit, and (iii) a network of sector specialists.

Friday, Apr. 9th: TrueLayer raised a $70m series B led by Addition with the participation of existing investors including Anthemis, Connect, Northzone and Temasek. TrueLayer is a developer-first open banking platform. The company will use the funding to launch additional services beyond open banking like account payments and embedded financial services. I'm convinced that account to account (A2A) payments will become a standard in the coming decade and Truelayer has done a great job at implementing its payment API with customers like Revolut, Trading 212, Freetrade and Nutmeg. Truelayers is seeing this paradigm shift from cards to A2A in its data with cohorts of users that shifted permanentely to A2A once they tried the solution.- Techcrunch

Saturday, Apr. 10th: Techcrunch published a deep-dive on StockX, a marketplace to buy or sell premium sneakers and streetwear. - Techcrunch

StockX is a "stock market of hype" enabled by the rise of ecommerce and social media.

"Its online-only marketplace is used for buying and selling sneakers, streetwear, electronics, collectibles, handbags and watches that are primarily sneaker and streetwear culture-adjacent, are in high demand and only available in low quantities. Sellers post their asking price and buyers share the price they want to pay anonymously. The platform makes all transactional data completely available to anyone that visits the site, and it authenticates every product by hand, acting as a safeguarded, price-regulating middleman"

StockX is riding several trends: (i) unbundling eBay and Craiglist which were inefficient at managing transactions around sneakers as both platforms had no authentification procedure between sellers & buyers, (ii) the evolution of the sneaker industry towards a high end segment with a voluntary limited supply that transformed sneakers into an asset class, (iii) Instagram as the go-to-place to share to the world your collection of sneakers.

StockX started in 2012 as a side project called Campless. It was a up-to-date sneaker secondary market pricing guide based on eBay transaction data initially. Campless became a proper company called StockX in 2016 selling sneakers with a stock market-related user experience.

In 2017, StockX expanded in the watches, streetwear and handbags categories. In 2019, the company expanded internationally with an authentification center in Netherlands and an office in Japan.

StockX has 9 authentification centers around the world and 300 authenticators. The company has built a detailed procedure to authenticate all the products on the marketplace. "Each sneaker has over a 100-point checklist to get through authentication."

StockX employs a senior economist called Jesse Einhorn who studies market price trends on the marketplace. As you can guess, the release Netflix's documentary on Michael Jordan had a strong impact on Air Jordan sales. “After it premiered and every day a new episode came out, we saw a huge spike in Jordan prices on average. Jordan sales went up over 40% because of the documentary and prices also really took off,” he says.

75% of users are under 35 y.o. and 50%+ of mobile app users are under the age of 25.

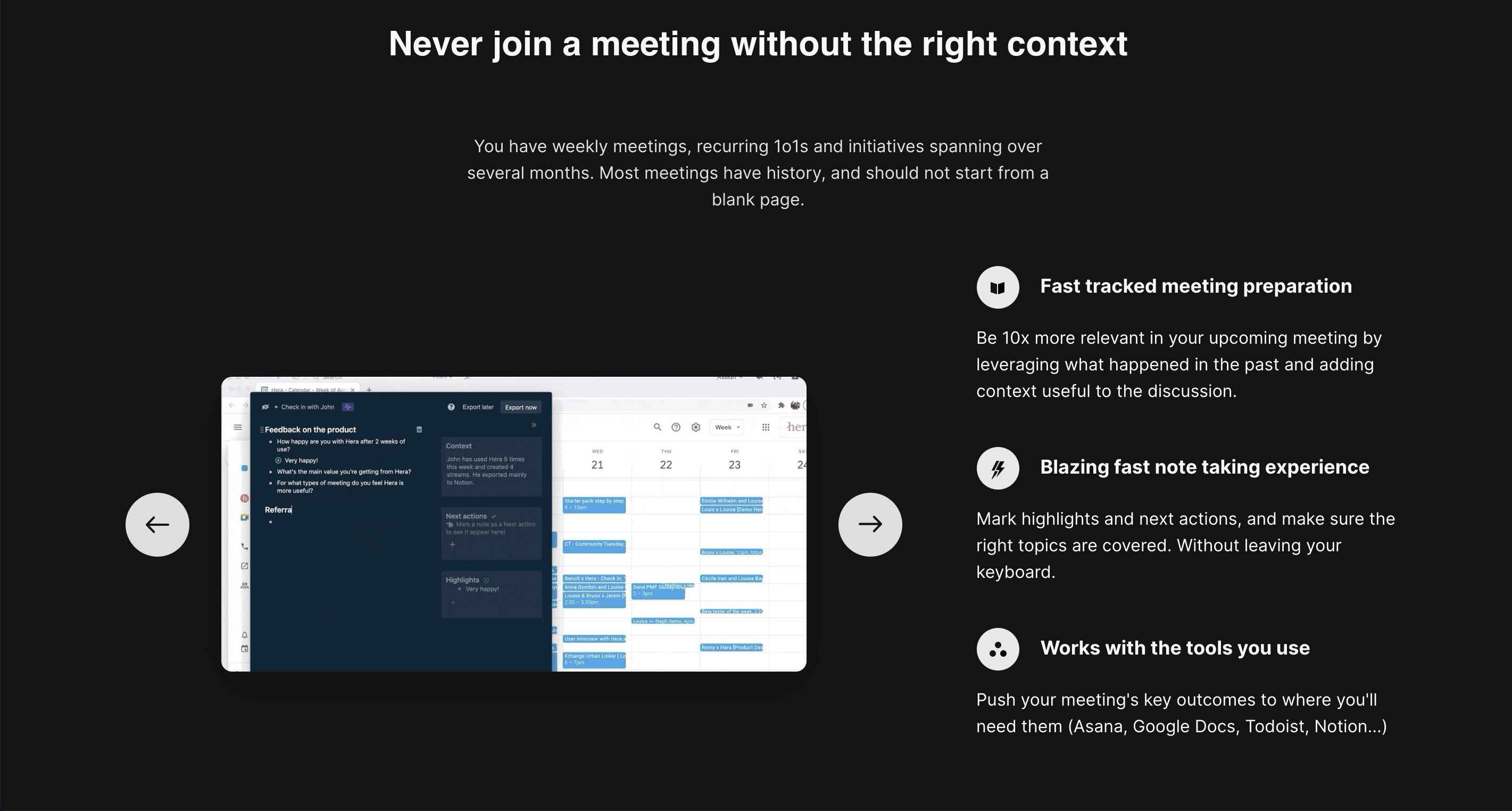

Louise and Bruno at Hera love to share with their beta users their key learnings from their favorite readings about the productivity’s space. Hera is a tool to make your meeting productive again. You can join the beta by clicking on the below button. Every month, I will give you a glimpse in the Hera’s community with an article shared in their Slack.

Sunday, Apr. 11th: Casey Winters (CPO at Eventbrite) wrote a guide on reaching product market fit. He defines product market fit as a "satisfaction that allows sustained growth." - Casey Accidental shared by Hera

There are two phases when you build a startup: the "0 to 1 phase" to find product market fit and the "1 to n phase" to scale this product market fit. It's important to nail its product market fit before investing in growth.

Customer expectations are increasing overtime. Customers will never be satisfied and will keep complaining about the product. You have product market fit when customers stop leaving. As a result, you should not measure satisfaction but you should measure retention.

Measure your retention's evolution overtime on the "key action the customer takes in a product that best represent product value"' and on "the natural frequency to product use".

Grubhub: ordering food online + once per month

Pinterest: saving a piece of content + once per week

The rate of retention matters too because if this rate is too low, you will never grow efficiently. The rate depends on the business you are in. Some acquisition loops can make you scale with a 10% retention rate and others need a 40% retention rate.

Casey also distinguishes two opposite ways to move towards product market fit (cf. infra): (i) "building enough of the product vision so that the product is valuable and ready for customers" and (ii) "getting customers to understand and receive the value you’re targeting for them".

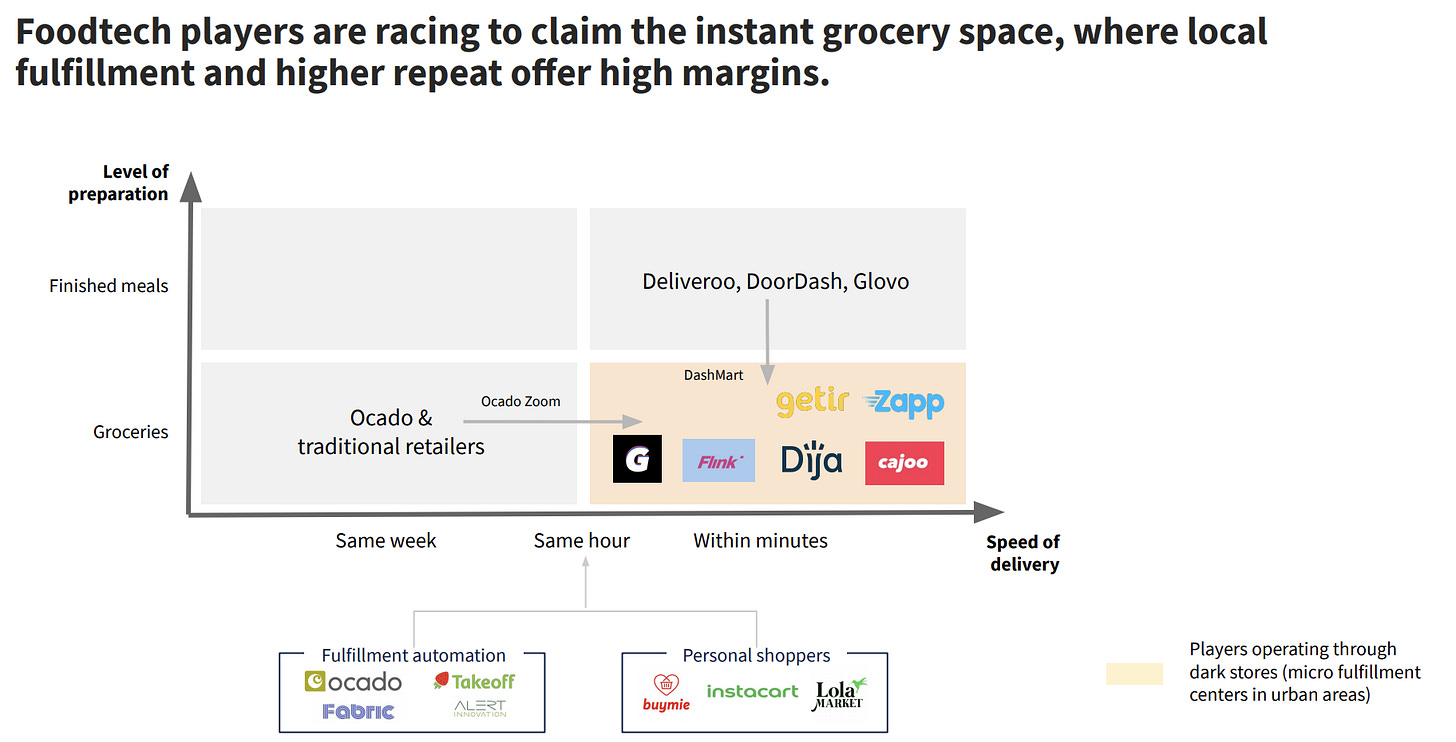

Monday, Apr. 12th: The Financial Times published a great paper on the rise of fast grocery delivery services titled "catch-them if you can." - FT

The grocery market is estimated at $1tn in the US €2tn in Europe.

Getir does not charge a delivery fee on orders above £10.

Ocado proved that there was an online grocery market for regular weekly deliveries. These players want to prove that there is a market for online deliveries for smaller purchases by being faster than going to your local convenience store.

“It produces that ‘wow’ moment that [makes] people start talking about you. [...] It’s the disruption you create when you do something shocking. You don’t create electricity by incrementally improving the candle.” - Alberto Menolascina (ex. Deliveroo and Dija's founder)

GoPuff achieves profitability in 18m in the markets it starts to operate into and has 300 warehouses between 8k and 12k square feet.

In the U.S., DoorDash has an hybrid model between Instacart and GoPuff. Gig workers can either pick grocery items for existing convenience/grocery stores or from DoorDash's network of dark stores called DashMart.

“One warehouse can make €1m a month in revenues.” - Kagan Sumer (Gorillas's founder)

“It’s not easy . . . we have worked a lot to make the unit economics profitable. The margin you make on the products ends up paying the rent, the pickers and the delivery people.” - Oscar Pierre (Glovo's founder)

And my favorite quote: “Many of the youngest crop of companies are going to get a brutal education.” - Michael Moritz (Sequoia's boss who invested before anyone else in Getir from his personal financial holding)

showing Venture capital investment in rapid delivery apps so far this year has already surpassed 2020 levels")

Tuesday, Apr. 13th: LocalGlobe raised 2 new funds: a $150m LocalGlobe pre-seed and seed stage fund and a $220m Latitude growth stage fund. Latitude is both (i) an opportunity fund to back at later stage LocalGlobe portfolio company and (ii) a fund able to back scaleups in which LocalGlobe did not invest into before (e.g. Monzo and Cazoo). I love the investment themes that LocalGlobe is going after: new native APIs (Yapily, Impala), tools for indies & SMBs (Melio, Libeo, Rekki), finance & insurance (Tide, Cleo, Wagestream, Zego), business automation (Rossum, Tessian), health & wellbeing (AccuRx, Awel, Apheris), human capital & collaboration (Modulz, Lunchclub). - LocalGlobe, Techcrunch

Wednesday, Apr. 14th: Sunday raised a $24m seed round at a $140m post money valuation led by Coatue with New Wave participating. Big Mamma's founders Tigrane Seydoux and Victor Lugger partnered with Christine de Wendel (ex. ManoMano's COO) on Sunday to offer restaurants a tool for customers to order from the menu and pay without touching anything thanks to QR codes. Sunday is also connected to cash registered systems to process the transactions. For restaurants, it increases the table turnover rate as customers don't have to wait 15 min to pay with a waiter. The service is free to use for restaurants and Sunday just takes a cut on transactions processed through their service. The startup has raised capital to seize the opportunity before the end of strict lockdowns in Europe. It's signing and onboarding restaurants in France and in the UK. Sunday is not a revolution. Just an execution play. Managing restaurants is probably the hardest entrepreneurship journey you can start, so I trust BigMamma's founders for the execution part of the plan. - Techcrunch

Thursday, Apr. 15th: Epic raised $1bn at a $28.7bn valuation from investors including Sony, T. Rowe Price, OTPP, KKR, Blackrock and Altimer. The funding will be use to build deeper experiences around their hit games (Fortnite, Rocket League, Fall Guys) and to expand Unreal game engine capabilities. - Techcrunch

Friday, Apr. 16th: Zoom launched a $100m Zoom Apps investment fund to support the rise of its platform's strategy. The fund will invest between $250k and $2.5m mainly between seed and series A into Zoom Apps, integrations and hardware compatible with the Zoom's ecosystem. - Zoom, Techcrunch

Saturday, Apr. 17th: Everett Randle (principal at Founders Fund) wrote a great article on Tiger Global. Tiger is a cross-over fund investing both in public and private markets which has been investing aggressively in growth stage startups around the world. It has 4 characteristics: (i) pre-empting aggressively funding rounds, (ii) paying high prices compared to industry standards, (iii) performing light due diligences, and (iv) light support to portfolio companies. Tiger Global has built a differentiated flywheel in the venture/growth market based on a higher capital deployment velocity and a better/cheaper/faster value proposition. - Everett Randle

Sunday, Apr. 18th: I read a brillant paper from Prateek Agarwal on Goodreads which is a community for book readers acquired by Amazon in 2013 for $150m. TL;DR: anyone is using Goodreads (195m visits per month) but nobody likes the product (poor recommendation engine, broken search functionality, poor UX etc.). - UXDesign

There are two ways to find your next book to read: passive discovery and intentional discovery. In reality, most of the time your readings will be driven by passive discovery. Goodreads is strong in SEO and is highly ranked by Google when you type the name of the book that you have passively discovered.

As a result, users are hooked into Goodreads when they want to decide whether they want to read the book that they have discovered. If they want to read the book, Goodreads will activate them with its "to read list". This loop is so powerful that it builds a brand that sticks in the mind of users. On the rare occasions a reader intentionally look for a book on the internet, he will end up on Goodreads.

Monday, Apr. 19th: Alan raised a €185m series D round at a €1.4bn post-money valuation led by Coautue with the participation of Dragoneer, Exor, Index, Ribbit and Temasek. - Partech, Alan, Les Echos

In 2020, Alan passed the €100m threshold in annual contracts with 155k members (2x on both metrics).

In Dec. 2020, the French market was deregulated, giving customers the possibility to cancel their contract at anytime without having to wait 12m.

The company has started its geographical expansion in Spain and Belgium and has expanded its vision to build the European healthcare super app.

Tuesday, Apr. 20th: Clubhouse raised a series C round led by a16z at a $4bn valuation with the participation of DST and Tiger Global. - Techcrunch, a16z, Clubhouse

The $4bn valuation mark was rumoured to be the price that Twitter was willing to pay for the company.

It's the 3rd round led by a16z in the company.

The funding will be used to (i) expand internationally (localisation features, growing the team), (ii) new programs and features for their creators, (iii) enhance the discovery experience in the app.

Wednesday, Apr. 21st: Deel raised a $156m series C at a $1.25bn valuation led by YC Continuity Fund with the participation of existing investors a16z and Spark. With Alan, it's the second French startup to pass the $1bn threshold this month. Deel is an all-in-one solution to hire and manage administratively remote workers. The company experienced a 20x growth in 2020, grew the team from 7 to 120 people and is now working with 1.8k customers (vs. 500 in Sep. 2020). Deel will use the funding to expand into 80 new countries and to add product layers to its offering including salary-based loans, insurance and benefits. (Deel, Techcrunch)

Thursday, Apr. 22nd: Our portfolio company Ornikar (💙) raised a $120m series C led by KKR. It's an online driving school to prepare and take both the theoretical and practical parts of the driving licence's exam. The funding will be used to expand into other European countries starting with Spain and to expand vertically in the insurance business. 420k customers joined Ornikar in 2020 (0.8-1m people take their driving licence every year in France to give you an idea of Ornikar's market share) and the startup offer driving lessons in 1k cities. I passed my driving licence with Ornikar. I'm proud to work for a fund that has led both Ornikar's series A and series B as I believe that it's a transformative company. It has completely reshaped the driving school industry in France breaking down the driving school oligopoly and status quo. (Techcrunch)

Friday, Apr. 23rd: Snap released its Q1-2021 results with interesting insights. Snap reached 180m DAUs and generated $2.8bn in revenues in the past 12m. (Snap)

For the 1st time in its history, Snap's Android user base is now bigger than its iOS's one. It's an achievement proving the hard work that the product team has put in rebuilding from the ground up the Android app in the past few years.

Snap's AR capabilities are becoming the standard in consumer applications. Snap is giving its partners access to its AR capabilities through Camera Kit. Snap is also super bullish on the use of AR in e-commerce to reduce the purchase friction by letting users try style and size with AR-based clothes and accessories.

Snap shared metrics on Spotlight: 125m MAUs in March, 40% growth of videos submitted between January and March, 70% growth in the number of viewers watching Spotlight for more than 10 min.

Snap has also doubled the revenues of its gaming partners building games.

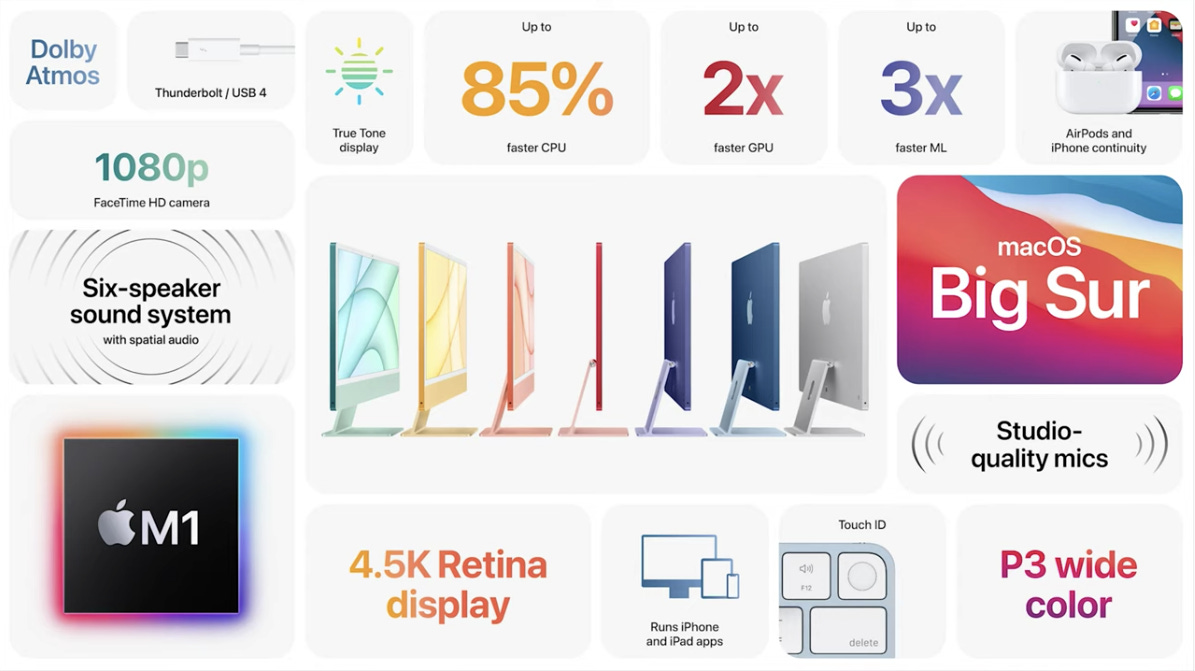

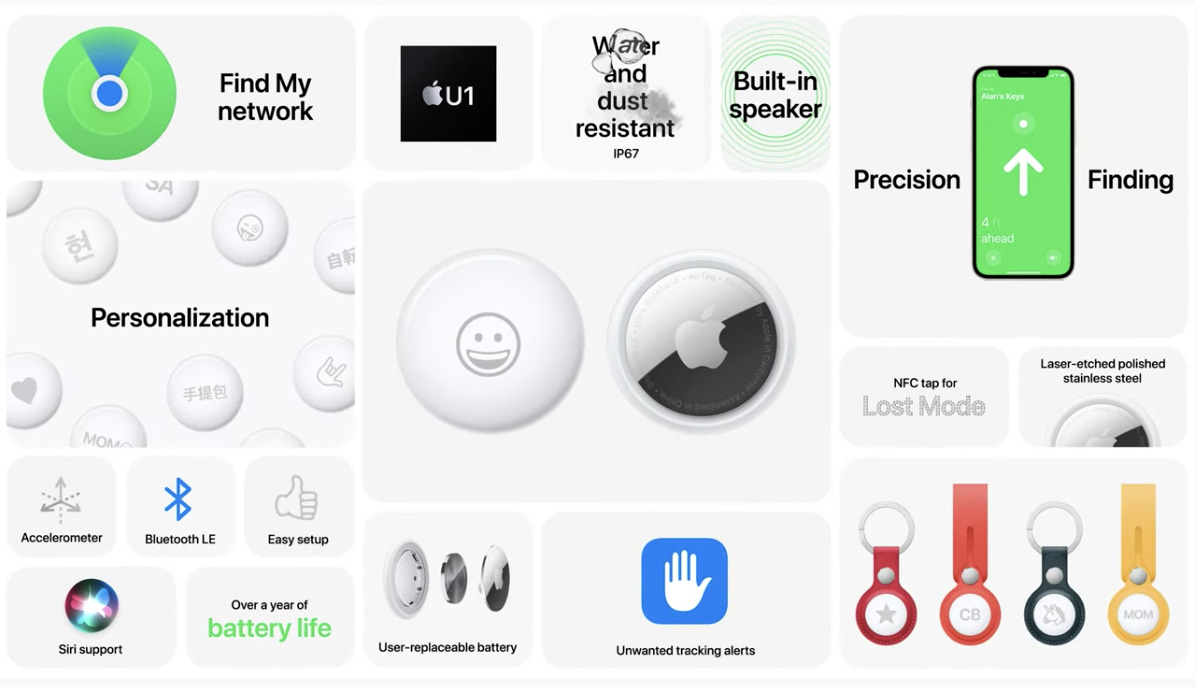

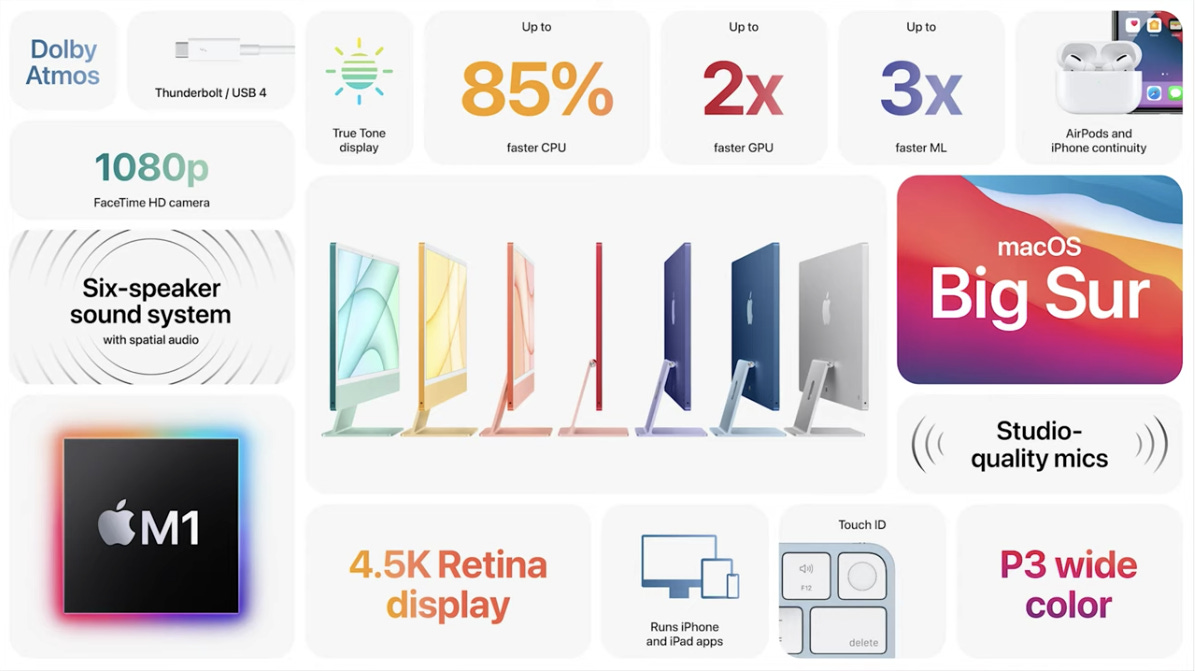

Saturday, Apr. 24th: I watched Apple's Spring Loaded Event with announcements focused on the Apple Card, Apple Podcast, a new accessory called FindMy and the new iMac. - Apple

Apple is carbon neutral for their global corporate operations including their offices, stores and data centers. By 2030, Apple will be 100% carbon neutral across its entire footprint including the supply chain and the use of their products.

Apple Card's vision is to reinvent the credit card and enable people to live a healthier financial life.

Apple noticed a lack of fairness in the way credit score are calculated in the U.S. for couples and decided to merge and share their credit line so that they build credit history equally.

Apple made the Card available for kids over 13 y.o. with the Apple Card Family.

Apple helped launch the podcast industry 15y ago. Apple redesigned its Apple Podcast app with channels to find new shows, rebuilt show pages to make it easier to listen to your favorite show and introduced a Podcast Subscription to support podcast creators (exclusive content, ad-free listening experience, early access).

FindMy is an app to find all your Apple's products and even 3P products which partnered with Apple. Apple released AirTag which is a small hardware that you can add to to a keychain or a bag to make them ring when needed. ($29 for 1 Airtag and $79 for 4 Airtags) AirTag can be personalised and combined with accessories.

Apple started a two-year transition towards Apple Silicon. M1-powered Macs has been prized by the press and users for being much more powerful. Apple announced a new iMac. It's incredible to see the impact that the M1 chip has on the shape of the new iMac compared to the previous generations. With M1, apps are becoming cross-platforms and the connectivity between your phone and your computer is super smooth.

Sunday, Apr. 25th: Colossus published a deep-dive episode on Chipotle which is a fast casual food chain in the US known for its burritos. - Colossus

Chipotle was started in 1993. The company went public in 2006 and was founder led until 2017. It has now 2.8k+ owned and operated stores (no franchise) generating $6bn in sales ($2.2m per store).

It introduced the assembly line process in the food industry. "You go into the store and the restaurant, you move down the line, selecting a base, add-ons like beans and salsa."

The goal of a restaurant is (i) to generate the most sales in the square footage it's using and (ii) to run the operations as efficiently as possible. Fast casual is a market positioning in which you serve premium food at a higher price point compared to fast food chains but you still run your restaurants as efficiently as possible. You want to produce a high quality experience at the lowest possible price.

Opening a Chipotle costs between $800k and $1m. Most restaurants are leased (don't own the real estate) and at its peak Chipotle restaurants had a 26% EBITDA margin. When you dig into the costs, 25% of sales are COGS, 25% are labour costs, 5% are real estate costs and 15% are the general costs of running a restaurant (sanitation supplies, electricity, waste). Restaurants have a 2-3y payback period ($600k in EBITDA implying a $400k cashflow if you remove taxes and maintenance Capex).

Monday, Apr. 26th: Clearbanc rebranded into ClearCo and announced a $100m series C at a valuation close to $2bn. Since inception, Clearco has invested $2bn+ into 4.5k different businesses. The rebranding aims at proving that Clearco’s offering goes beyond funding as it’s also a product that supports companies and founders. It has now 3 different products: ClearAngel which is an initial equity kicker to start a business, ClearCapital dedicated to fund ecommerce ad and inventory expenses and ClearRunway for SaaS startup to convert future recurring revenues into upfront cash. - PR Newswire, Techcrunch

Tuesday, Apr. 27th: Figma introduced FigJam which is a collaborative online whiteboard for team brainstorming sessions. Figma is pushing forward its platform strategy to become the one-stop shop for design. This whiteboard is another proof that Figma is not targeting only designers but all the individuals in a given team who are interacting with design. - Techcrunch, Figma, MUO

Wednesday, Apr. 28th: Turner Novak raised a $9.99m solo-GP consumer venture fund called Banana Capital to invest $25-300k tickets into pre-seed to pre-IPO companies (with a focus on pre-seed to series A). Several tier-one venture capital investors like Dan Rose, Andrew Chen, Semil Shah, Erik Torenberg, Evan Moore and Sriram Krishnan are LPs in the fund. Turner has made 15 investments including Powder, Commonstock, JOKR and Wellnest. - Turner Novak, Techcrunch

Thursday, Apr. 29th: Our portfolio company Kaia (💙) raised a $75m series C. It's a mobile app to treat chronic pain effectively through a digital program therapy with daily exercises. It does not require hardware and uses computer vision to guide patients in their exercices. Kaia experienced a 600% growth in bookings in 2020 and reaches more than 60m patients globally. - Techcrunch

Friday, Apr. 30th: Taster raised a $37m series B led by Octopus with the participation of existing investors Battery, LocalGlobe, Heartcore and GFC. Taster is a dark kitchens’ operator and has built a portfolio of food brands only available through food delivery platforms. In Paris, Taster is delivering 5k meals per days on Deliveroo and is the 3rd biggest restaurant group on the platform after McDonald's and Burger King. Taster will use the funding (i) to go direct to consumers through its own mobile app, (ii) to franchise its brands to expand quickly in other cities (1k cities targeted by 2025). - Techcrunch, CNBC

showing Venture capital investment in rapid delivery apps so far this year has already surpassed 2020 levels")

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋