🛤 Stripe - The Definitive Fintech Enabler

Overlooked #81

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m diving into how Stripe’s suite of fintech products is being used to create the next generation of fintech enabled businesses.

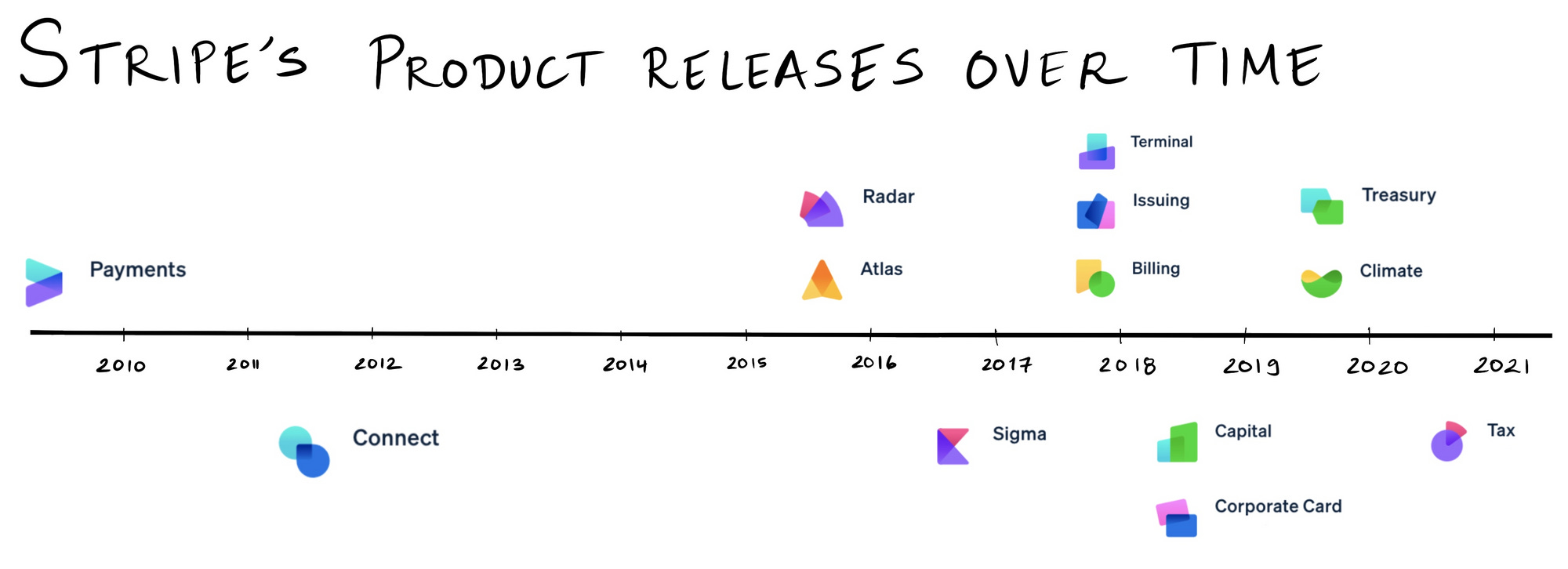

The best startups are unstoppable. They are able to continuously expand their addressable market. Stripe is the best illustration of this phenomena. In the past 5 years, it has released outstanding products that have expanded its business way beyond its payments core business.

As a result, Stripe's valuation is increasing at an exponential rate. In April 2020, Stripe raised $600m at a $36bn valuation. Less than a year after, in March 2021, Striped raised another $600m at a $95bn valuation. I'm confident that Stripe will be a trillion dollar business before the end of the decade.

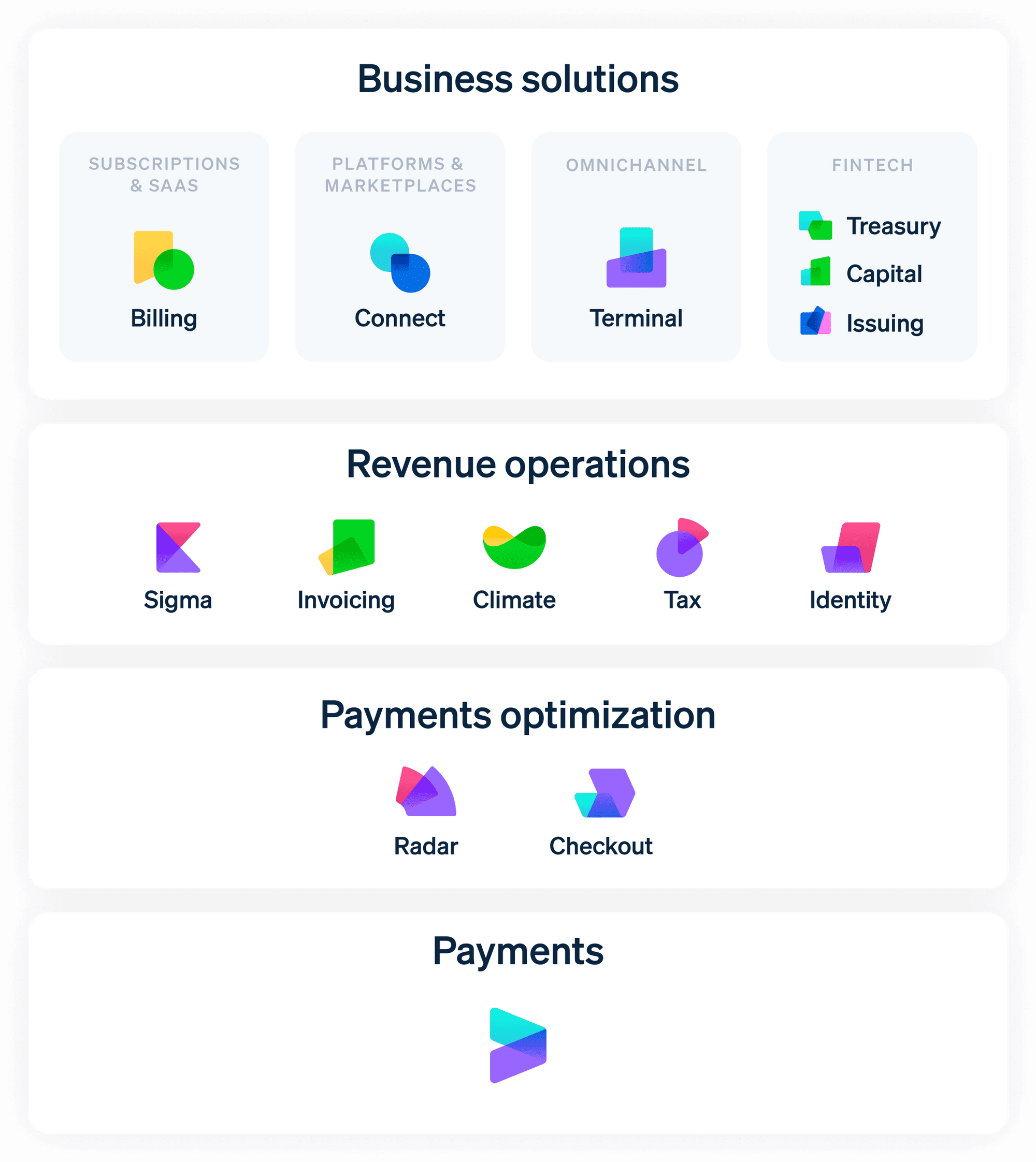

In this article, I will cover a market expansion that I'm passionate about. I believe that Stripe is becoming the definitive fintech enabler. It's building the rails to enable any business to become a fintech company with products such as Issuing, Treasury, Capital and Payments. It's impressive knowing that it's only a sub-product line in Stripe's suite of products (cf. the fintech category in the below graph).

Mapping

Sripe has four different products that can turn any business into a fintech: Payments, Treasury, Capital and Issuing. Please note that Stripe is progressively deploying these products in all their local markets and not all of them may be available in the country you are into.

First, Payments is Stripe's core product. It enables companies to process financial transactions. Most Stripe's customers use the solution to process payments for their core business but other companies use Payments to add an additional revenue stream to their core offering. Indeed, a company can use Stripe Payments to start processing transactions for its own customers and charge a premium on top of Stripe's costs.

Shopify is obviously the best example. It started as a SaaS solution to help merchants build their online shop with a fixed monthly fee. At one point, in partnership with Stripe, Shopify added a payment solution to its offering to bring more value to its customers and be able to index its revenues on the growth of its merchants by taking a cut on the transactions processed on their online shops.

If you take a step back, most vertical SaaS like Shopify can deploy a payment offering to start processing transactions for their customers and to increase instantly their addressable market. It's also a way to increase the ACV they can extract per customer and to better retain their customers. I've noticed this market expansion in several categories: SaaS selling to hotels like Mews and Amenitiz, SaaS selling to restaurants like Toast and Lightspeed, SaaS selling to the beauty industry like Mindbody, Squire and Planity.

Second, Issuing is "a set of APIs that allow platforms to create, manage, and distribute virtual or physical cards". Stripe reduces the friction for its users to create and distribute cards to their own customers. Moreover, you build specific use cases for these cards by customizing the spending rules.

For instance, Silvr is working with Issuing. Silvr is a French startup providing non-dilutive capital for SaaS and ecommerce businesses to fund their growth. Issuing is the perfect solution to make sure that the money Silvr lends to its customers is only used to fund marketing expenses.

Bench is another good example. It's an accounting services for small businesses to help them run their book-keeping, their tax filings and their reporting. Bench uses Stripe Issuing to provide its customers with a business card to combine natively their finance with their accounting. It increases Bench's service quality and customers are no longer dependent on importing their banking data from third parties.

Stripe Issuing seems to be also an obvious solution to manage employee benefits. You provide your employees with digital cards which usage is constrained by a set of rules (e.g. in France, respect the daily limitations on meal vouchers' spendings and constraint the usage to restaurants and retailers). Employers can make savings by paying only for benefits really used by employees. Employees have a greater flexibility on the benefits they pick and don't only access a restricted list of benefits' providers picked by the company.

Third, Treasury is a banking-as-a service solution. "It enables platforms to offer their users accounts to hold funds, pay bills, earn interest, and manage cash flow." With an API call, you can create a fully-featured account for your customers. For instance, Shopify is using Stripe Treasury for its Balance offering which is a business account specifically built for its merchants. As a result, Shopify's merchants can have a unified view of their business (revenues and expenses) without leaving the Shopify ecosystem. Moreover, they can access to specific benefits like cashback and rewards when they are spending on the Shopify's ecosystem.

Another example is Ambrook which is a platform to help farmers in their process of getting financial assistance for their business. Ambrook use Treasury to create business accounts for its farmers and facilitate their diverse applications for financial assistance.

Fourth, Capital is a lending API. "It enables platforms to offer access to fast and flexible financing that helps users grow their businesses." Instead of building a full-stack financial arm which requires capital and regulatory approval, you can piggyback the Stripe infrastructure to start offering lending products to your customers.

For instance, Lightspeed which is a vertical all-in-one SaaS platform for restaurants use Capital to offer loans to its restaurants. It's a similar story for Jobber which is a SaaS for home services (cleaners, plumbers and landscapers) business owners. It's a population that has been underserved by traditional lending solutions and Jobber use Stripe Capital to provide them with tailored loans and to automate the repayments based on the revenues business owners generate on Jobber.

Conclusion

As you can see, Stripe has built a suite of products (its payment core product, its API to issue cards, its banking as a service solution and its lending API) that can turn many companies into fintech-enabled startups. I mentioned many use cases in this article but the most exciting is that I'm sure entrepreneurs will use these fintech enabler infrastructure to create use cases that either Stripe and us have never thought of.

Thanks to Julia (🦒) and Maud for the feedback! Thanks for reading! See you next week for another issue! 👋