🏠 Opendoor - Moving House Should be Frictionless

Overlooked #114

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m writing about Opendoor. In previous issues, I covered full-stack companies disrupting consumer in categories like grocery with GoPuff and used cars with Cazoo. Opendoor is going after the real-estate sector with a value proposition disrupting how consumers are moving from one home to another.

Opendoor was founded in 2014 by an experienced team led by Eric Wu who had previously founded a real estate company sold to Trulia and by Keith Rabois who seeded the company at Khosla, discovered the founding insight behind Opendoor and contributed to recruit the core founding team.

Opendoor’s vision is to build a vertically-integrated experience to reinvent how consumer are buying and selling homes. It wants you to “buy, sell and move at the tap of a button”.

In Dec. 2020, Opendoor became a public company merging with a SPAC launched by Social Capital. At the time, Opendoor was in 21 markets in the US, had sold $10bn worth of homes and worked with 80k home-owners.

It has not always been a rosy journey. Opendoor had two-waves of lay-offs, one in 2019 to re-centralize its operations around its HQ in Phoenix and one in 2020 in reaction to the covid pandemic. Moreover, Opendoor’s stock price is suffering - even more so than most tech stocks because it’s a consumer full-stack model and it has dependencies to macro-factors (interest-rates and housing market).

I divided this post into 2 sections:

Part I - What is Opendoor?

Part II - What is Noteworthy about Opendoor?

Part I - What is Opendoor?

Opendoor's mission is to "empower everyone with the freedom to move". It innovates in the real estate market to improve the process of both selling and buying a home.

It started with the selling side by creating a new category called iBuying. In the US, 90% of the transactions are intermediated by agents.

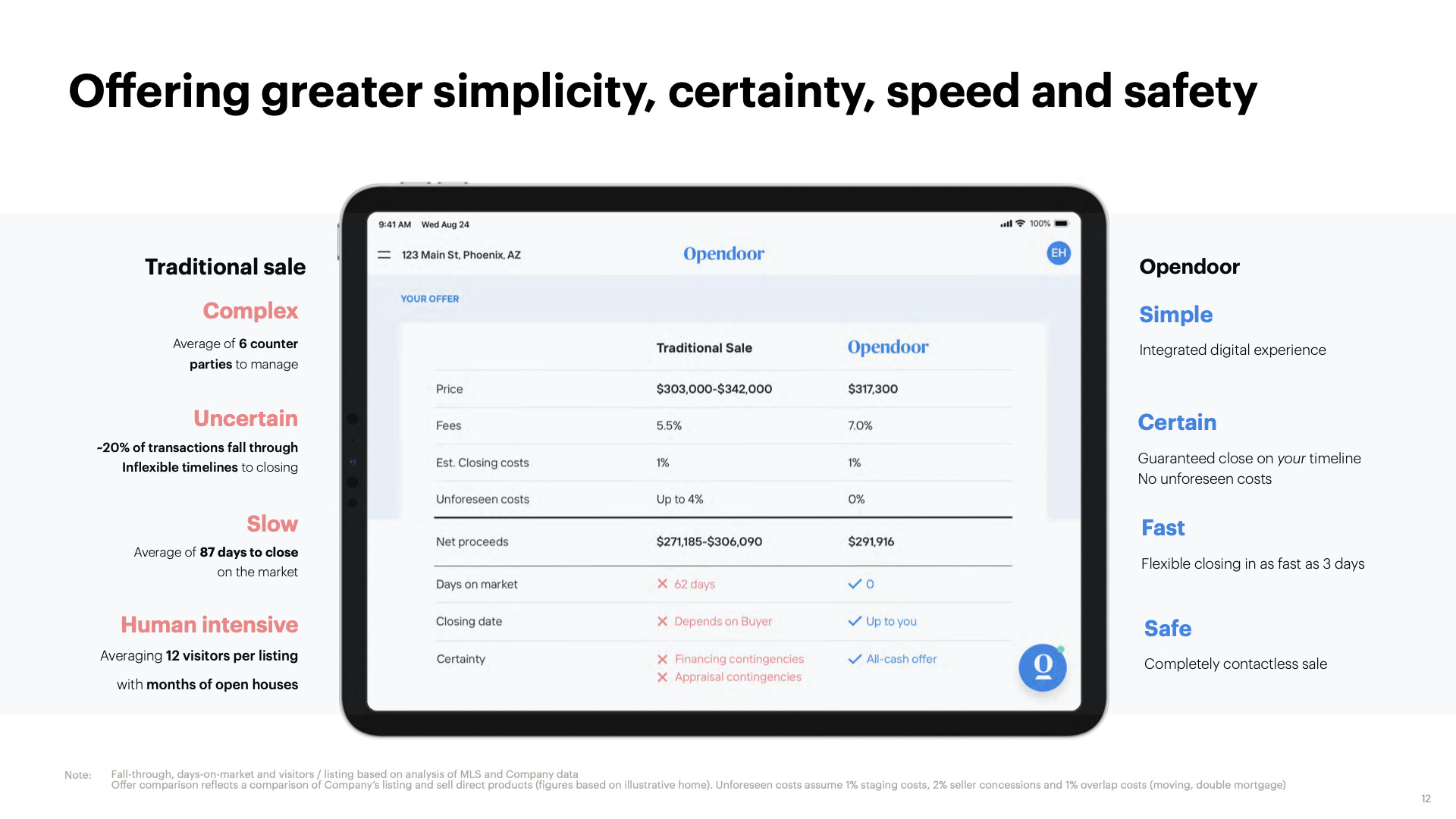

It's a cumbersome process with several core pain-points: (i) it's long as it takes on average 90 days to sell a house, (ii) it's a multi-step process (find a listing agent -> prepare home for listing -> list -> organise home visits -> receive an offer -> negotiate repairs with buyers -> wait for closing), (iii) it involves multiple stakeholders (agents for both sellers & buyers, repair companies, lenders, etc.), (iv) there are many non transparent and hidden costs (you can end up paying up to 12% of transaction in costs), (v) even after signing, there is 20% chance of failure before closing, (vi) most sellers will consecutively buy a home and they need the proceed of the sale for the down payment (vii) it's a transaction that consumers only perform once every decade and they're not aware of how everything works, the regulations and the hurdles that they’ll need to navigate.

Opendoor reinvents the selling experience. Sellers can quickly receive an online quote. To get a final offer, potential sellers perform a virtual assessment of their home and then an assessor physically comes to verify home information. This process can be done in as little as 3 days. Once the offer is accepted, sellers have nothing further to do: no need to make the repairs, to organise visits, to manage stakeholders, etc. Moreover, sellers decide when they want to move, Opendoor offers them flexibility and the time to buy and move to a new home.

Opendoor's foundational insight is that most homes are not unique and can be priced with an algorithm like commodities. As a result, you don't need to wait for a settled transaction to be confident that you’ll be able to resell a house at a similar price to the one you bought it within a couple months.

Opendoor naturally expanded to the buying side leveraging its unique inventory and bundling "selling + buying" into a single experience (2/3 of people are selling a home to buy a new home). Opendoor built a smooth buying experience with several core innovations: (i) visit homes virtually or on-demand on your own, (ii) make an offer in cash thanks to Opendoor's financial support, (iii) get a loan quickly and in an experience integrated with your buying journey.

Opendoor is also developing tools for the stakeholders in its ecosystem. It has a Scout App for field operators and a Vendor Management Platform for home vendors.

The Scout App deals with everything that happens after a preliminary offer has been made. An estimator will inspect the house to make potential adjustments before sending the final offer. Once the offer is accepted, a renovation project manager will oversee the potential repairs and field technicians will set-up hardware to secure the house and make it remotely visitable.

On the Vendor Management Platform, Opendoor matches vendor partners to home repair projects based on their current capacity and their competencies.

Opendoor has 2 main gross margin streams: (i) a commission on acquired homes and (ii) additional high-margin services & products sold during transactions to buyers and sellers.

Opendoor's commission on acquired homes is compared to the 6% fee that Americans are used to pay to brokers to sell their homes. It started to operate with a 9% fee and is slowly decreasing this fee as the company scales (5% standard fee as of today).

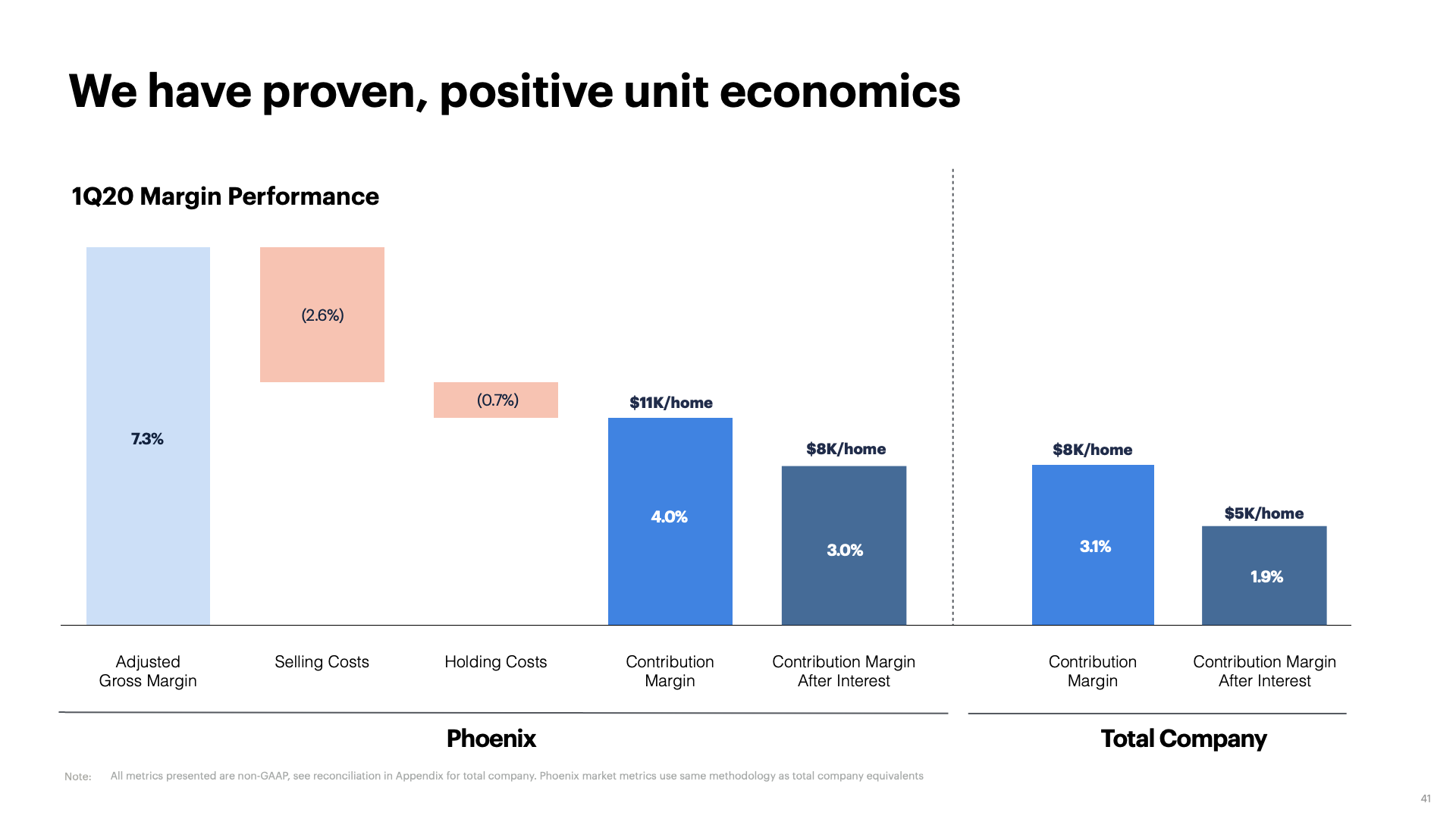

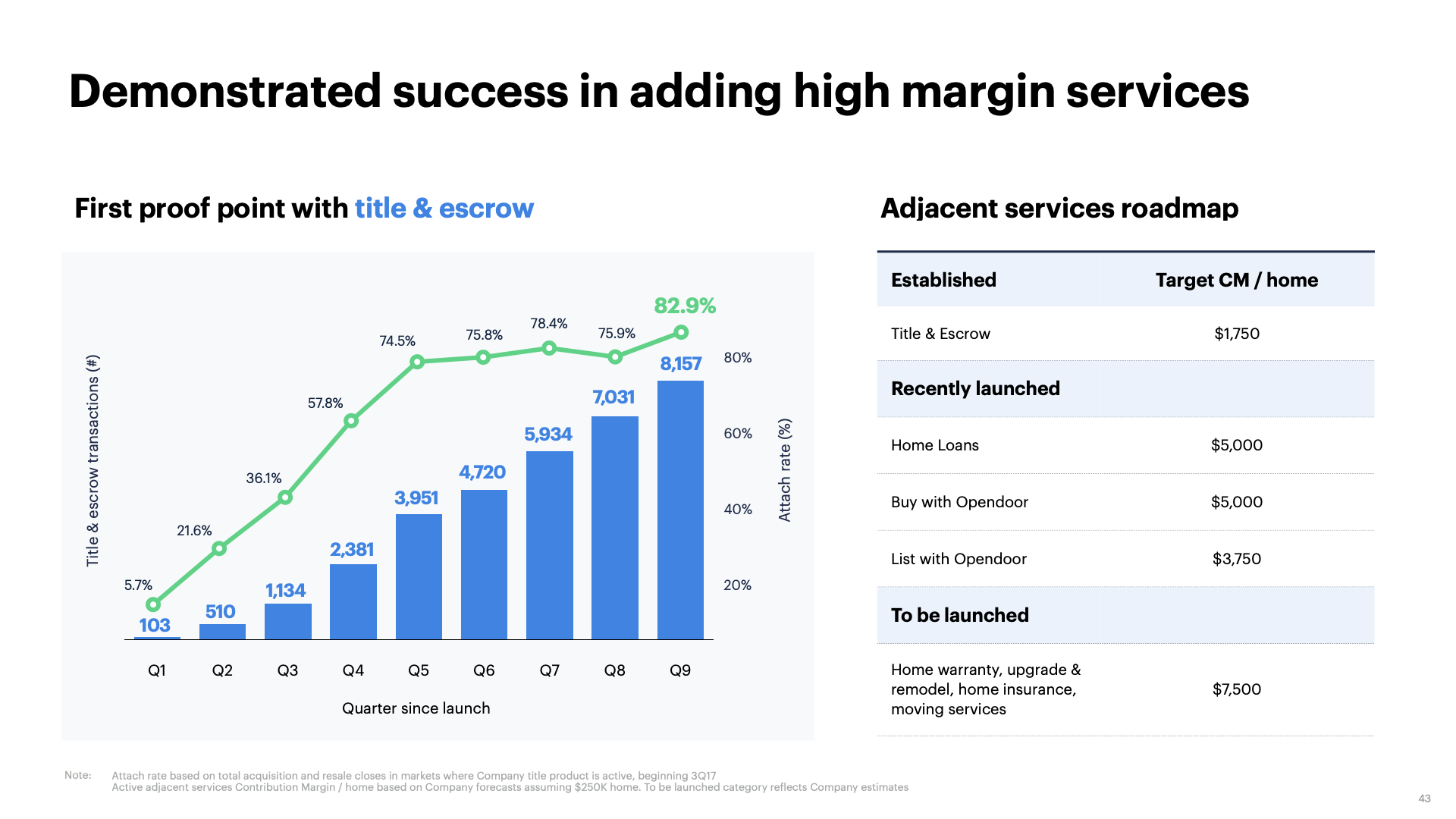

Opendoor is still in the early days on improving its unit economics with high margin products and services. It has a 1st product called title and escrow which is working extremely well with a 80%+ attachement and a $1.75k targeted additional contribution margin per home. In the past 18 months, it has also launched other products such as home loans, listing fees and buying fees.

It should be noted that Opendoor does not aspire to create value by reselling homes at a higher price than the price it bought them. Opendoor is acting as a market-maker in the real-estate market. It believes that you can determinate the price of assets with high certainty and you should not be entitled to make revenues on arbitrage. You can only charge for bringing liquidity to the market.

In the long term, Opendoor is targeting a $18k contribution margin per home driven by additional services (e.g. lending) and by cost optimisations.

Opendoor's long-term vision goes beyond the selling value proposition. Opendoor wants to be the best partner when you're thinking about moving from one home to another. Besides, it aspires to be a digital companion for home-owner to bring recurrence in the model ("Live with Opendoor").

Part II - What is Noteworthy about Opendoor?

Category creator and category leader. In 2014, Opendoor created a new category with iBuying which is disrupting the $2.1tn annual commercial real estate market in the US. Today, iBuying has a penetration rate below 1%, Opendoor has a 5% market share in its most mature markets and Opendoor has a 70%+ market share in the iBuying category. It means that Opendoor still has strong room for growth. It will also rip most of the market share and profit in this category.

Startups scaling combining debt and equity. In the past few years, many startups created models leveraging debt in categories like BNPL (Affirm, Klarna, Afterpay, Alma) or RBF (Clearco, Wayflyer, Silvr). Opendoor's iBuying model also leverages debt to fund home purchase and the holding period before reselling them. These models were created and have only functioned in a low interest-rate environment. There is a question-mark on their sustainability in the higher interest-rate environment which we're moving towards. For instance, Opendoor's interest rates on debt represent 30%+ of its gross margin. If interest rates increase, Opendoor will have no choice but to increase its 5% commission becoming less competitive to brokers' 6% commission.

Vertically-integrated models. In the past 5y, vertically-integrated models have emerged across consumer sectors like healthcare (CarbonHealth, Avi Medical), travel (Sonder), groceries (GoPuff), cars (Carvana) and in real estate with Opendoor. I've a strong conviction that in consumer, full-stack models will end up winning because they're providing a superior experience to end consumers. Nonetheless, these models are harder to finance than asset-light models because they're capital intensive and are less profitable. Moreover, it takes more time for them to unlock high-margin revenue opportunities on ancillaries products and services that can be implemented only once scaled. All these full-stack companies are following the Amazon's playbook in retail. They apply the "your margin is my opportunity" mantra to disrupt incumbents and they end up generating incremental profits on additional products that you can unlock once you've reached market dominance (e.g. ad business or AWS for Amazon).

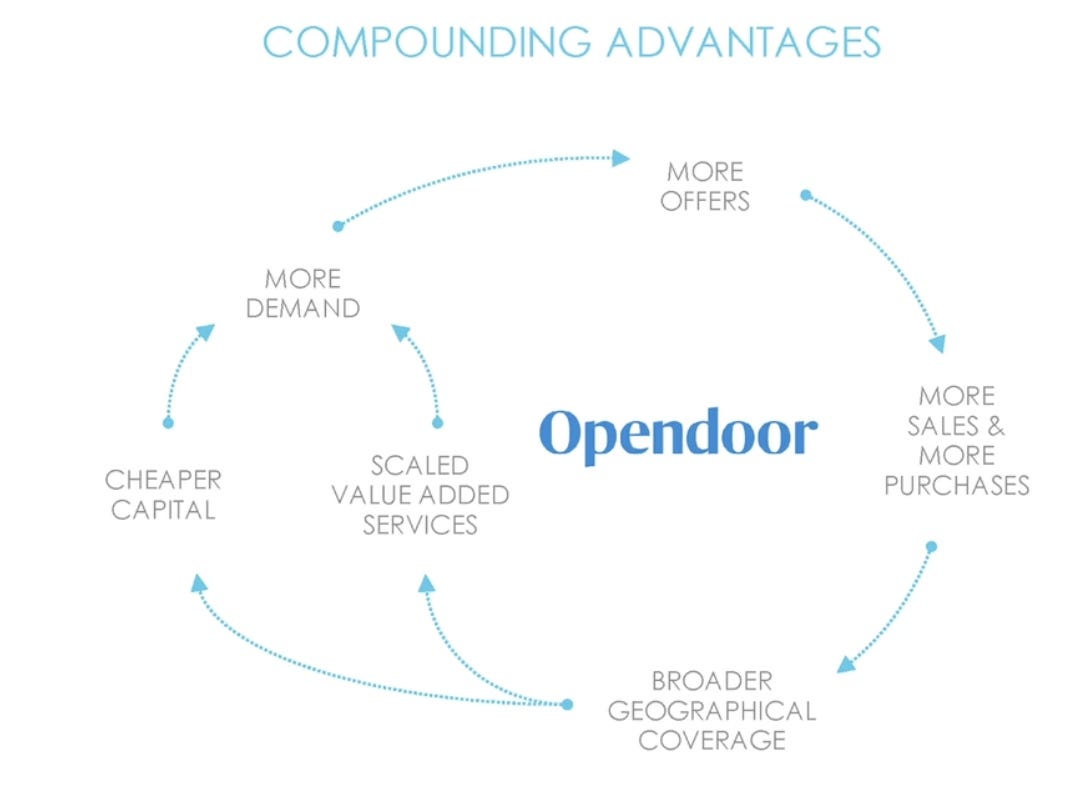

Competitive advantages in the model. Introducing Opendoor's to its SPAC's shareholders, Chamath Palihapitiya shared that the company had compounding advantages as it scales. Scaling has several benefits in Opendoor's model: it makes its pricing algorithm more accurate, it reduces the cost of operations and it reduces the cost of debt which enables Opendoor to reduce its commission. With a reduced commission, Opendoor is becoming more mainstream than brokers, becoming a no-brainer for end-consumers who want to sell their houses. Keith Rabois talks about accumulative advantages with Opendoor because the business gets easier to run as days pass.

Management principles from Eric Wu who is Opendoor's cofounder and CEO. Eric Wu is passionate about the real estate sector. He cofounded Movity a geo-data analytics startup which went to YC and was sold to Trulia in 2011 where Eric led geolocation and social products. He stayed 2 years at Trulia before reconnecting with Keith Rabois and started working together to start Opendoor. I found a couple of interesting learnings around management while listening to Eric Wu's interviews and reading about Opendoor.

When you're building a business heavy in operations, it's key to build a culture of frugality. Opendoor learnt it the hard way. It had to make several round of layoffs and to recentralize its operations in Phoenix because the company was overspending. "BPs for Breakfast" i.e. basis points for breakfast has become a core value in the company. Opendoor is on a mission to cut its real estate transaction costs and to pass these savings to end customers in order to become more mainstream.

Eric distinguishes 3 stages when you're building a business: (i) reach product market fit, (ii) figure out distribution fit to scale growth and (iii) figure out the business model fit to have good unit economics.

On recruiting, "the most important thing is talent aggregation and talent editing". On talent aggregation, you've to figure out 12 months in advance the executive that you need to hire to be successful. You've to plan to source candidates and spend more than 20 hours with them to make sure there are a good fit for the company. On talent editing, you need to identity the people who can scale within the organisation and act around this potential with external recruitment, coaching or reorganisation.

I also love the emphasis Opendoor puts on creating a world-class customer experience - at the macro level but also at the micro level. "Start and end with the customer. We invent, build and execute to improve the lives of our customers. We put in the hard work to delight customers, even when no one is looking."

"To be a great leader, I think you have to aggressively seek advice, you have to be growth oriented and you have to implement [advice and the growth mindset] which is the hardest thing to do." - Eric Wu

Company building principles from Keith Rabois who led the 1st round in Opendoor and participated actively in kickstarting the company. Keith Rabois is an investor at Founder Fund. He was previously an investor at Khosla Ventures and an operator in several high profile companies such as PayPal, Linkedin and Square. While at Khosla, he contributed actively to kickstart Opendoor. He had the initial insight that homes were commodities. He helped to recruit the core team and he led the 1st round of funding.

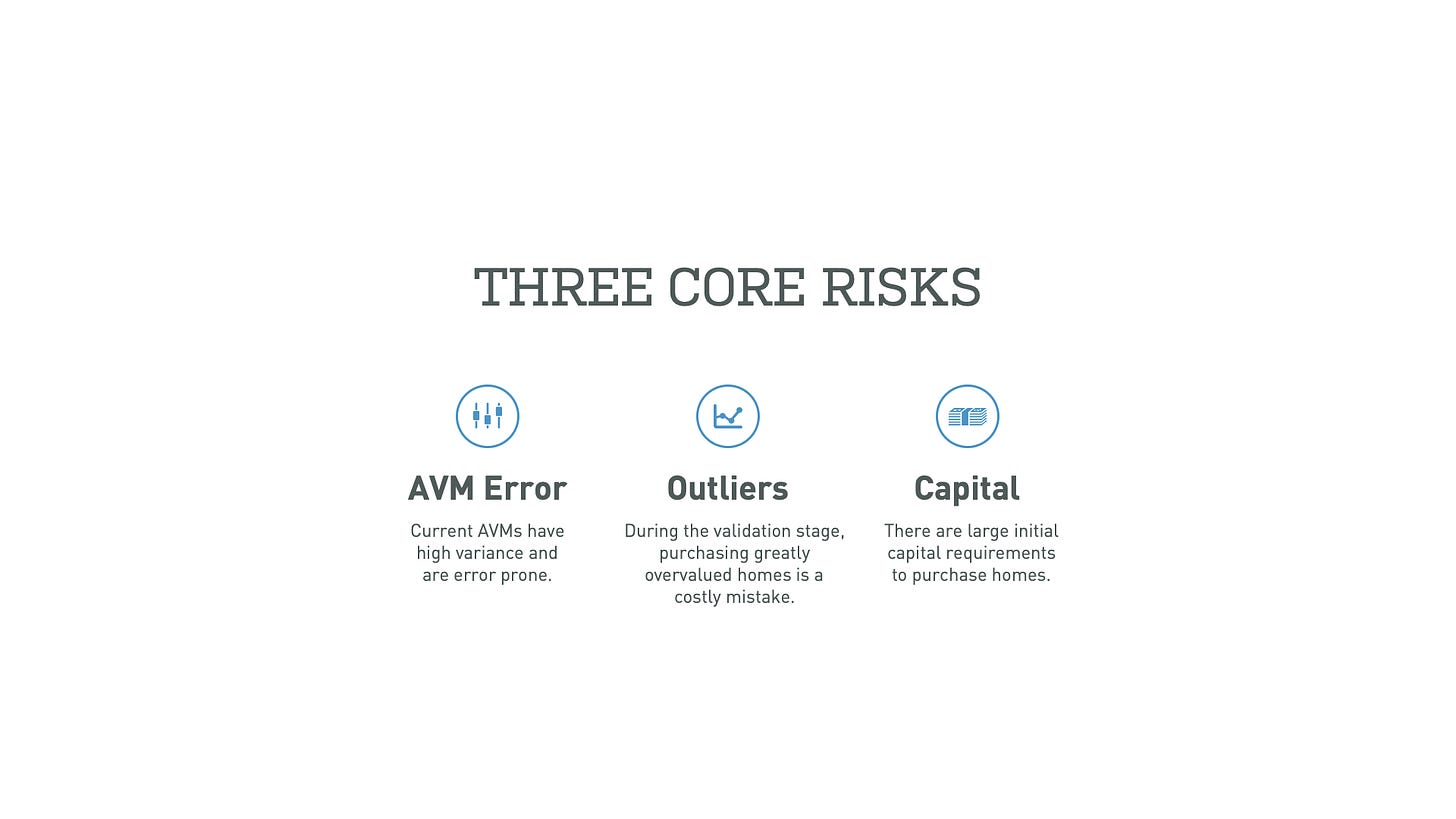

Startups are about risk reduction. At any given stage, there are 2-3 core risks per business which are 2-3 things that really matter and that you've to get right. To solve them, you should calculate the right skills set to have an unfair advantage to solve these specific risks and hire people with these skills sets. With Opendoor, 3 main risks were identified at inception (pricing, access to capital and buying overvalued applications) and Opendoor built its core team to solve them.

Fat startups are superior to lean startups. Interesting, differentiated and defensible ideas require more capital to be launched. If you really want to disrupt a sector, the lean methodology is non-sense because you won't have the means to make the big moves that are needed to build a sector disruptor.

Devil is in the details. If you execute all the details perfectly, you will end up winning. A great output is only the byproduct of details done right.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

If higher interest rates eat into Opendoor Gm’s, they can increase spread on their offers without affecting the commission charged. I don’t think increasing commission is a good strategy