🎄 Wish IPO Analysis - Reinventing Ecommerce for the Invisible Half

Overlooked #49

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m digging into one of the most controversial tech company called Wish that went public one week ago and is on a mission to bring ecommerce to the lower-income segment of the population.

Let's talk about Christmas gifts. Do you have a distant aunt who always gifts you ill-chosen gifts that you know you’ll never use? Do you have brothers and sisters who always offer you cheap, useless gadgets? Do you have a distant family member who wants to be cool and offers your kids branded clothes of their favorite video games? Do you have a stepmother who tells you that your Christmas gift has not been delivered yet? Guess what? They are all buying their Christmas present on Wish and you don't know it.

This week, I will cover this fascinating mobile e-commerce company. Wish is a marketplace to buy mainly non-branded products from China that are super affordable but take weeks to get delivered. Wish is also a mobile first experience: you shop on Wish like you spend hours on TikTok. The company uses AI algorithms to customize a differentiated shopping experience that is not search-based like Amazon but discovery-based. Wish's founder and CEO Peter Szulczewski wants its shoppers to have the same serendipity on the app than what they have in shopping malls - except that on Wish all the items in your field of vision are relevant to you.

A Unique Value Proposition in Ecommerce

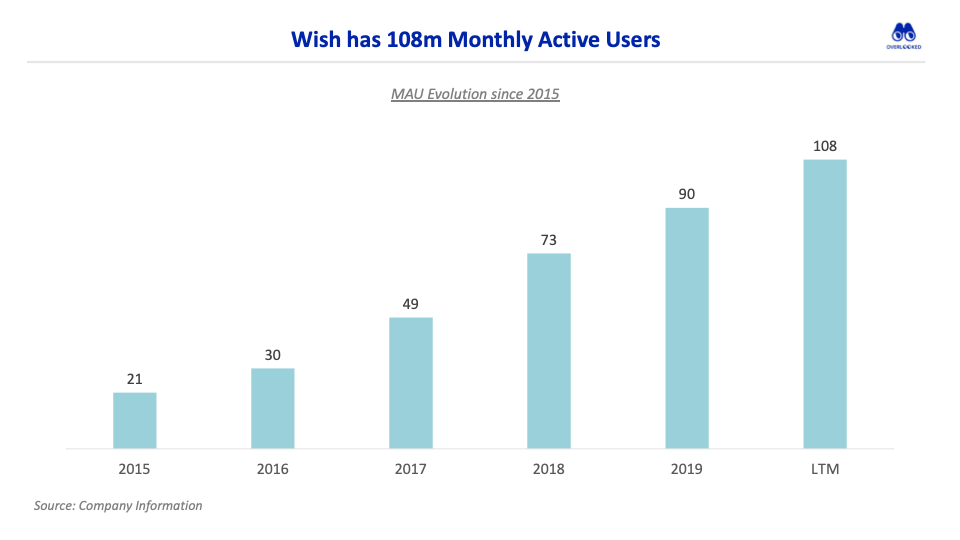

Wish is not your regular e-commerce website. It's a mobile-first experience. 90% of usage and purchases happen on mobile. Wish is not only interested in your purchase rate. is also optimized for higher usage and retention like a social app, using similar metrics. In its S1, the company discloses that it has 108m monthly active users and that an user spends on average 9 min per day on Wish. When you look at Wish demographics, it's noteworthy that the app adresses all generations and not only mobile-native generations. 53% of users on Wish are 34 years old+

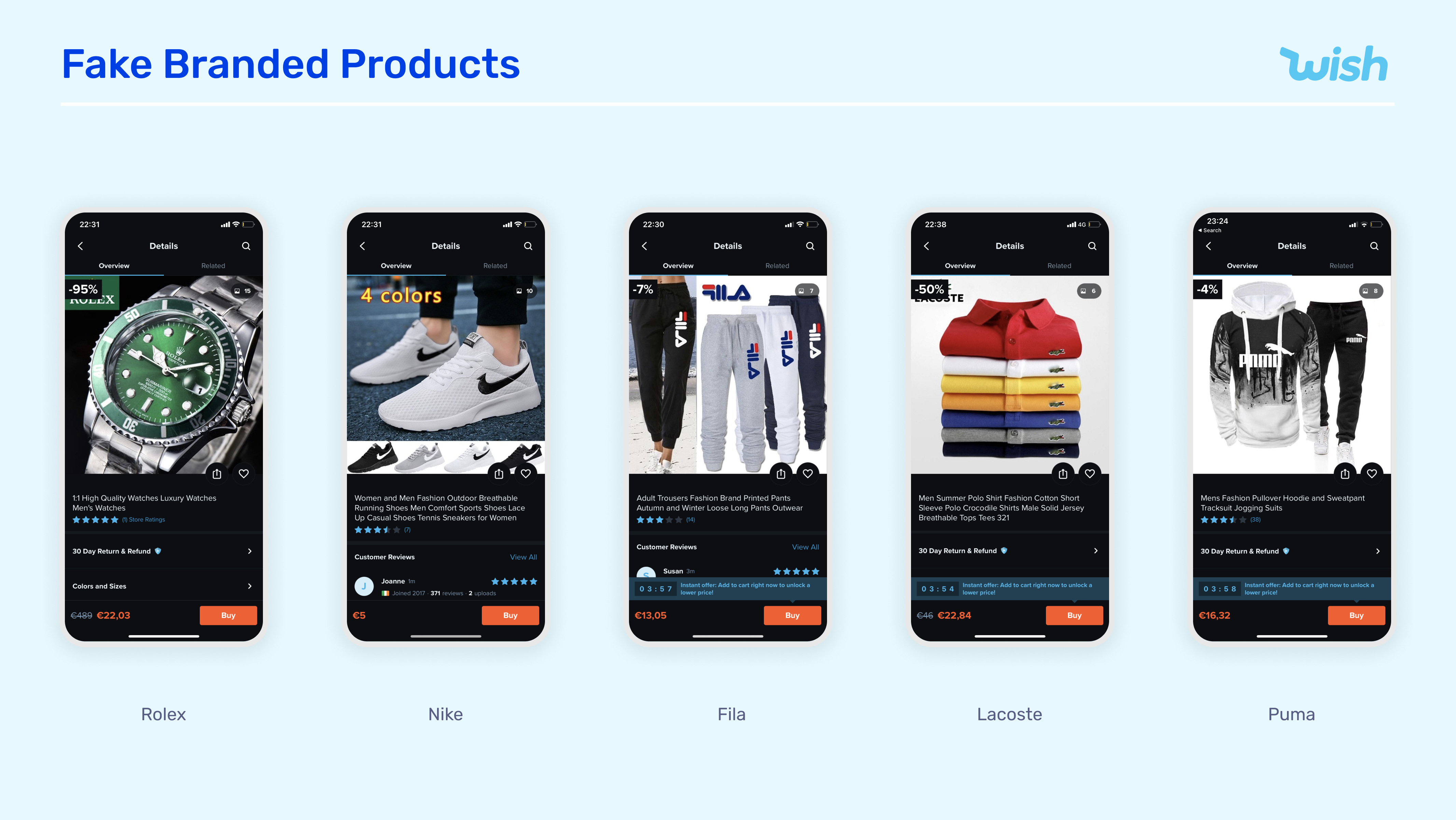

On Wish, you have three main categories of products: (i) mainstream culture products, (ii) fake branded products and (iii) life hack products. Wish has recently diversified its product offering to make the shopping experience more premium by adding branded products, products that can be delivered in a couple of days as well as products from local shops. I believe that the goal is mainly to build trust with the user-base rather than changing radically the product mix.

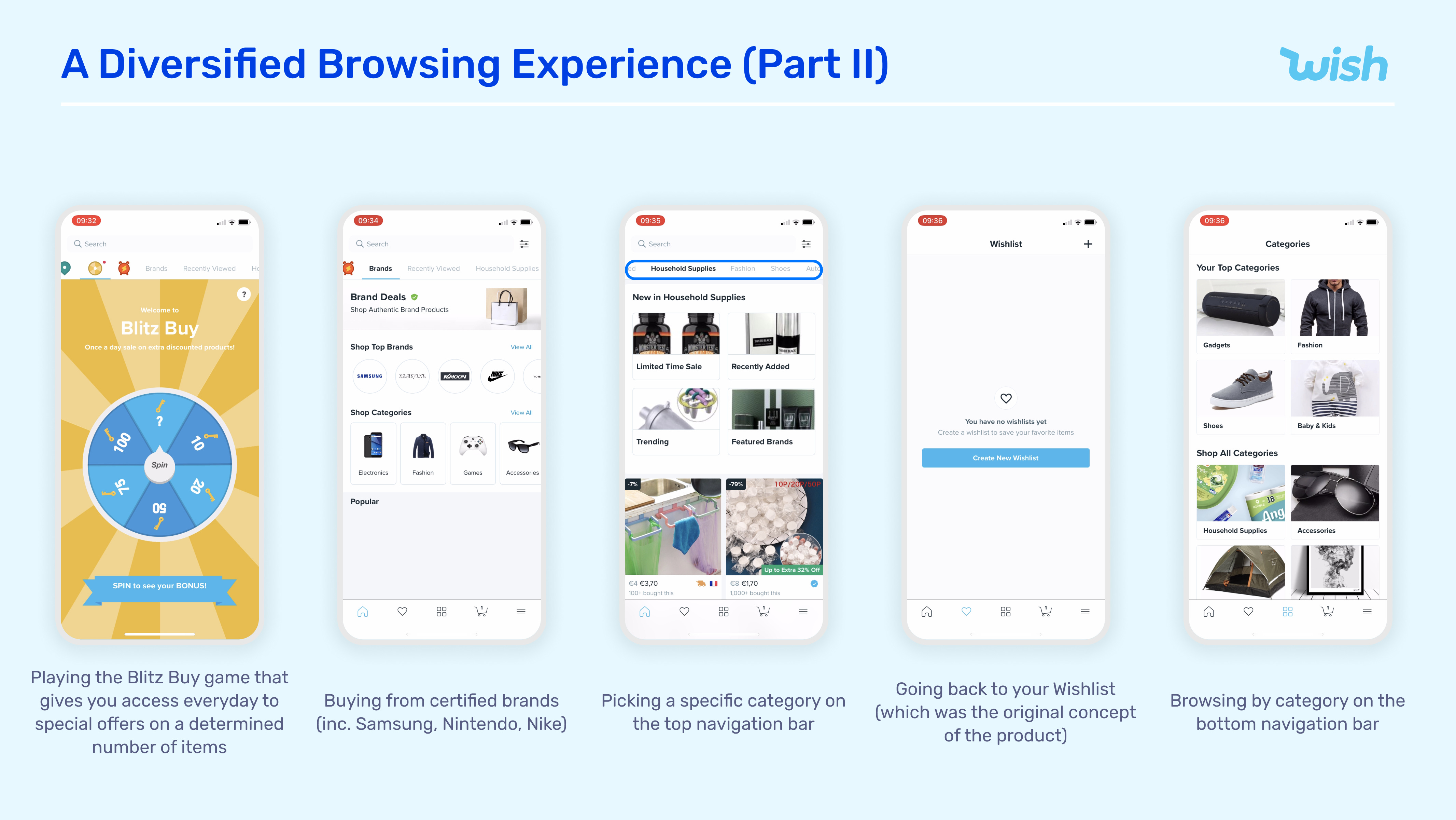

Wish is bringing two main UX innovations that make the app a unique e-commerce experience: (i) a discovery-based shopping experience and (ii) gamified features.

On Wish, more than 70% of purchases happen without a search query which is extremely different than the way we usually shop on other ecommerce websites and marketplaces. You may have an intent to buy when you open Wish but most of the time you have no idea what you want to purchase. You hang out in the app to find inspiration. You go window shopping on Wish - except that everything you see in your feed is customized based on your preferences and past actions. Almost anything is relevant for you on Wish which is not the case at all when you are in a physical shopping mall. To pull off this feat, Wish offers an extremely diversified shopping experience powered by two navigation bars and multiple entries to start shopping.

Wish has also brought gamification features into its app at an unprecedented level in the Western world. It starts in the aggressive onboarding in which you are offered free products and you are given coupons to get discounts on products for a limited period of time. You have also entire sections in the app that are dedicated to gamified experiences: you can collect stamps to be redeemed against discounts, you can spin a lottery wheel, you can access hourly (!) flash sales etc.

Wish mainly targets low-income households who value cheap price above anything else. Peter Szulczewski wrote an article in Dec. 2016 introducing the concept of the "invisible half". It's the lower-income segment of Americans that has been underserved by technology and especially by ecommerce. Many Americans cannot afford to pay an annual Amazon Prime membership (only 20% of Wish users have an Amazon Prime subscription) and don't value convenience and quality as much as price (80% of Wish users are doing their grocery shopping at Walmart). In the early years of its journey, Wish discovered that they had a strong product market fit with low-income households who were valuing price above anything else and decided to go all in to serve them. On Wish, 57% of households earn less than $50k per year. A corollary is that Wish has a stronger penetration rate in rural areas than in cities.

I'm super interested in this idea that large segments of the population are underserved by technology and capital. Entrepreneurs and investors have blinders. They are not willing to invest into thematics that are too far away from their usage and their way of life. If you are building a company targeting specifically an underserved segment, let me know. At the moment, I'm interested into the following segments: Gen. Z, old people, women and people living in rural areas.

A Controversial Bet

Wish is not Roblox or Doordash. E-commerce, gaming and food delivery are three markets than have benefited from the covid crisis but Wish does not have the same traction as Roblox or Doordash. The company is going public with (i) a slowing down 32% YoY YTD 2020 sales growth, (ii) deteriorating gross margins following a regulatory change in the US shipping policy, (iii) numerous public controversies around the products sold on the platform. On the other hand, over the past two years, Wish has set the foundations to grow more sustainably in the long term: (i) targeting emerging markets, (ii) increasing the reputation of the platform and (iii) getting involved into logistics to increase convenience. Wish is a controversial bet which makes the company more interesting than its consumer peers.

Wish’s growth is slowing down and covid has not been a game changer. Before filing for IPO, the company was known for its exponential growth. The S1 has validated this idea with a company that went from $144m in sales in 2015 to $1.7bn in 2018. But the growth has slowed down drastically in the past two years. Moreover, covid has not been a saving white knight. Wish has grown only by 22% over the past twelve months. It’s disappointing compared with the growth of ecommerce peers like Amazon and Shopify. It’s also disappointing compared with the broader ecommerce market. In fact, in 2020, U.S ecommerce sales are expected to grow 40%+ to reach $839bn on the back of the covid crisis.

At the same time, Wish is built on weak unit economics with agressive marketing expenditures and a deteriorating gross margin following a regulatory change.

Wish is famous for its bizarre ads on Facebook and Instagram - platforms on which the company regularly ranks among the top advertisers. Wish uses similar techniques than hyper casual game studios with weird, click-bait and colourful ads. For its 2016 cohort, Wish paid more than $10 to acquire a buyer and reach a LTV/CAC of only 2.6x by year 4. This economic equation is not straightforward for a B2C company. I would have expected a quicker payback ratio especially for a company that is dependent on paying acquisition.

Wish’s gross margin has declined drastically in the past two years. The company was built on a tax brake on shipping rates from China to the U.S. for small packages. As a result, it cost less to send a small parcel from China to the U.S. than it cost to ship it within the country. Following the geopolitical tensions between China and the U.S., the Trump administration decided to go after this generous subsidy and shipping costs doubled overnight in July 2020. When you combine this structurally-reduced gross margin with the dependence to paying acquisition, it’s hard to be bullish on Wish’s future unit economics.

At the same time, Wish has started key initiatives to strengthen its economic model and find other growth levers:

In 2019, the company launched Wish Local partnering with 50k local brick and mortar retail stores in 50 countries. These partners (i) are uploading their inventory on Wish allowing the marketplace to diversify its supply and reduce its dependency to Asia and (ii) have become pick-up locations for Wish orders. Retail stores can even offer delivery. If you take a step back, you understand that Wish has built a low-touch distribution network overnight.

Wish is working hard to increase the level of user trust on its platform by piggybacking on the fame of third parties. The company added branded products on the marketplace: you can now buy a Nintendo Switch, a Samsung phone or Nike AirJordan etc. Wish has also partnered with well-known influencers: Wish is sponsoring the Lakers and has done a media campaign with soccer stars in Europe like Neymar and Buffon.

Conclusion

I believe that Wish is really targeting an overlooked and underserved segment of the population. Amazon is not for everyone. People who are going to Walmart don't have the budget to shop on Amazon. Wish has noticed it and has built an ecommerce experience targeting this "invisible half" which is valuing price above convenience and even quality.

Moreover, Wish's shopping experience is unique. It's a mobile first shopping experience and not a replication on mobile of web based marketplaces that are mainly driven by search query. Wish has centered the experience around discovery with a personalized feed of products that you can scroll infinitely and gamified features.

Nonetheless, I don't believe that you can build a sustainable marketplace if you don't have the trust of your customers. You can fool users once or twice with pervasive ads and extremely low quality products but you won't retain them overtime. Wish will have to increase its minimum standards and reduce the misleading aspects of certain products/ads if it wants to prosper in the long run. It's a noble cause to serve low-income households and to offer a mobile first experience but you have to do it properly.

Additional Resources

🔎 S1 (Wish, Nov. 2020)

📹 Peter Szulczewski, CEO of e-commerce app Wish, raised $1 billion in two years (Recode, Dec. 2016)

📹 Peter Szulczewski, CEO and Co-Founder of Wish (Shoptalk, Apr. 2017)

🗞 Wish wants to be the Amazon for the rest of us, will retail investors buy it? (Techcrunch, Dec. 2020)

🗞 Should you invest in Wish? An S-1 Analysis (Napkin Math, Dec. 2020)

🗞 Wish Built An $11 Billion Business On Insanely Cheap Shipping — Can It Survive Without It? (Forbes, Jul. 2020)

🗞 What will a Wish IPO look like? We may know soon (Techcrunch, Sep. 2020)

🗞 Meet The Billionaire Who Defied Amazon And Built Wish, The World’s Most-Downloaded E-Commerce App (Forbes, Mar. 2019)

🗞 The Invisible Half (Peter Szulczewski, Dec. 2016)

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Thank you for these well researched note Alexandre!

While I would agree that Amazon may not be for everyone, I don't know that Wish is a credible alternative. As you rightfully pointed out, the product selection is vastly different. as a result, Wish's revenue per buyer looks roughly 2 orders of magnitude below Amazon's. While the buyer mix would explain a 5x difference, here we are talking about vastly different needs served. This disconnect between the explicit positioning (better catering to a different segment) and what looks to be the reality (very well executed impulse purchase capture without a low cost / proprietary user flow) is what I find most troubling