🥏 How to Expand your Addressable Market as a Vertical SaaS?

Overlooked #88

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing a playbook to expand your addressable market as a vertical SaaS for local businesses.

You know that with Clément and Loup, we have been working on a deep-dive on vertical SaaS & marketplaces for local businesses. We will publish several papers in the next couple of weeks on the topic but as a teaser we wanted to share how do you with about market size expansion when we look at vertical SaaS for local businesses.

Historically, many investors did not want to invest into vertical SaaS for local businesses because they believe that most vertical markets were too small to generate multi-billion dollar outcomes. Most of the time, this view is wrong: vertical SaaS are uniquely positioned to expand their addressable market by adding layers that will increase the revenues they can generate per customer.

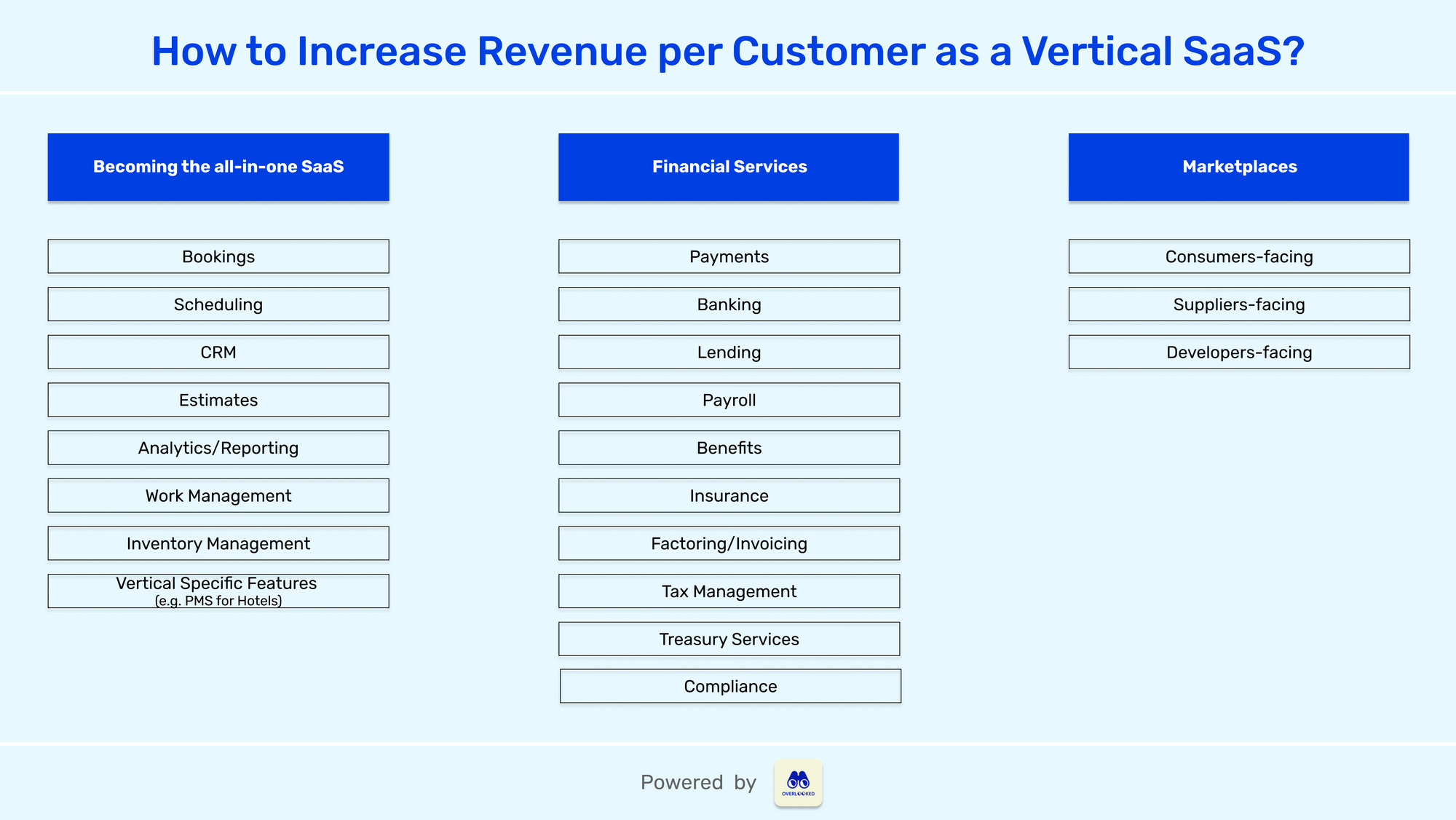

To increase the revenue generated per customer as a vertical SaaS you can:

Add product features to become the one stop shop solution when it comes to software for your customers

Embed financial services

Embed a marketplace for suppliers and/or end-consumers

Part I - Become the one stop shop software solution

Most vertical SaaS start with a simple value proposition solving a large pain point in the vertical they operate (e.g. managing bookings, complying with a new regulation, etc.). But vertical SaaS have the potential to become invaluable to their customers by developing a suite of products needed to run all the aspects of their businesses (e.g. CRM, estimates, inventory, team management, analytics, etc.). Ideally, you want to become the record system of your customers - the unique place where they store all the data related to the business. Most successful vertical SaaS end up being the last software that customers will unplug when they close the business. As a result, these vertical SaaS for local businesses are able to reach much stronger gross retention rate (90-95%) compared with horizontal SaaS targeting small business (50-70% retention rates).

Even if your SaaS is business critical and is the one-stop shop solution to run a small business, you can't go beyond a pricing threshold that depends on the targeted industry but that is generally between $200 and $250 per month. Small businesses behave like consumers. It's hard to charge a consumer an individual subscription above $10-15 per month because it's the price that will get you access to amazing services like Netflix and Spotify. It's the same for small businesses. As a result, to increase the revenues generated per customers, you need to find revenue sources that will not be a directly visible or appear as an additional cost to them - examples of such sources are fees on financial services or a take rate on a marketplace.

Part II - Embed financial services

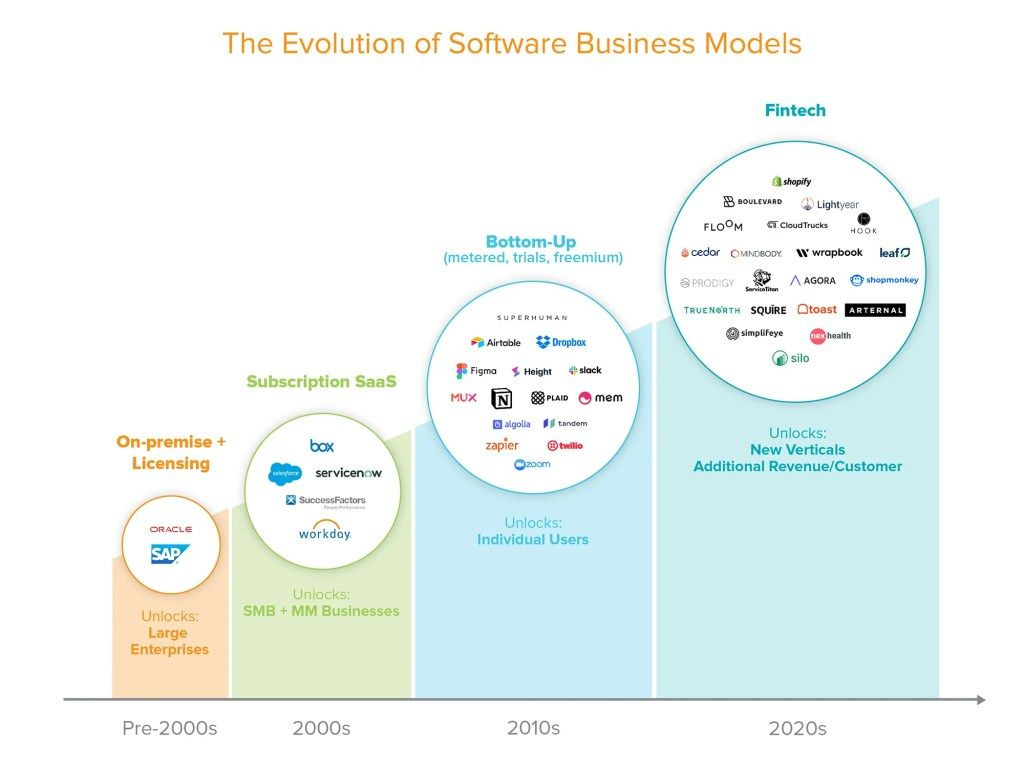

I covered in a past issue the idea of fintech enabled businesses which are companies adding one or several fintech layers on top of their core value proposition to increase their lock-in effects on their customer base and to generate incremental revenues per customers. Vertical SaaS are perfectly positioned to transition into fintech enabled businesses. They can offer superior financial products because they understand their industry inside-out and they have much more granular customer data than traditional banks.

For a16z, the combination of software and financial service is the next successful iteration of the software business model after bottom-up SaaS. It allows software to penetrate new vertical historically underserved by tech and to generate additional revenue per customer.

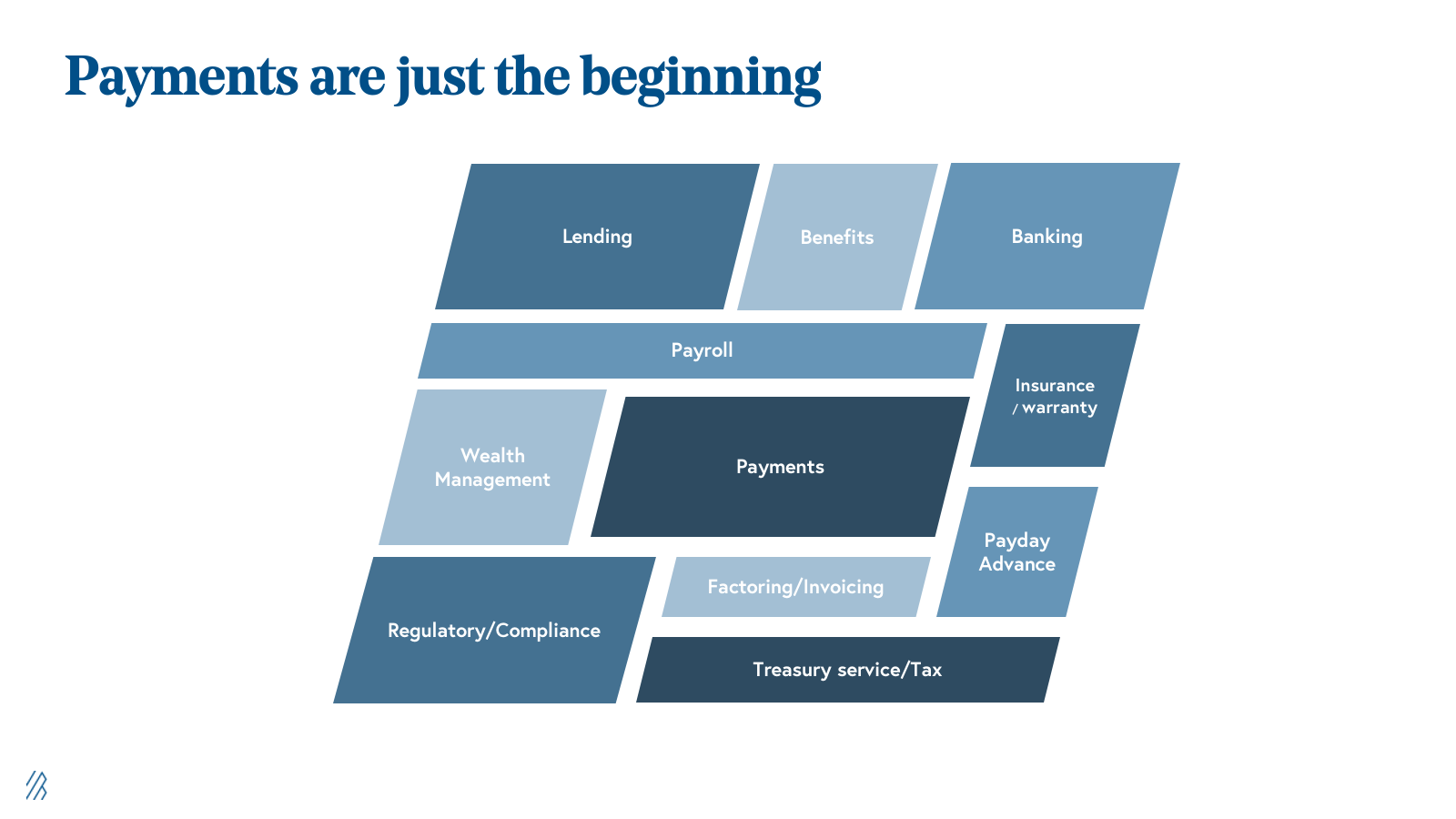

Vertical SaaS should have a broad understanding of financial services. Processing payments for customers is obviously a good starting point but companies can go way beyond that with services provided like banking, lending, payroll, taxes etc.

For instance, Mindbody, a pioneer vertical SaaS which offers an all-in-one software for local wellness businesses, was already a fintech-enabled businesses generating 37% of its revenues from payments at IPO in June 2015. Squire which is a more recent vertical SaaS also going after the wellness vertical (more specifically barbershops) went deeper in its financial services offering, with payments, banking, payroll and lending services thanks to a partnership with Stripe and a bank.

Part III - Embed a marketplace for suppliers and/or end consumers

After a certain scale, vertical SaaS for local businesses are also well positioned to launch marketplaces either for end consumers or for suppliers. They will generate incremental revenues per customer by taking a take rate on all the transactions happening on these marketplaces. On the customer front, Mindbody and Squire are again good examples as they developed a marketplace for end-customers to book a beauty service. On the supplier front, Shopmonkey which is a vertical SaaS for auto-repair shops is building a marketplace to help them find and buy parts needed to repair cars.

Sometimes, entrepreneurs consider that the marketplace is a such a great opportunity that they are willing to build a vertical SaaS for free that is distributed to both sides (supply and demand) of the marketplace. Choco and Rekki are good examples with their free SaaS for restaurants to process their orders from producers and wholesalers which is the first step of their masterplan to build a food procurement marketplace.

Thanks to Clément, Loup and Julia (🦒) for the feedback! Thanks for reading! See you next week for another issue! 👋