💡 Casting a Light on the Private Equity Secondary Market

Overlooked #20

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m talking about the private equity secondary market.

Have you ever heard of an asset class that has better returns that then overall private equity market but with shorter holding periods and asset with a decreased risk profile? Too good to be true? Welcome to the small world of the secondary market which has been booming in the past two decades to bring liquidity to the private equity market.

In this paper, I will (i) explain what is the PE secondary market, (ii) give you key metrics on this asset class, (iii) dig into the benefits for buyers and sellers in this market, (iv) pinpoint key trends in the secondary market and (v) look more closely at the VC secondary market.

Preliminary note: You can skip this section if you are familiar with Private Equity and its secondary market.

By design, Private Equity is an illiquid asset class. You cannot sell your stake on a public exchange like you can do with publicly listed companies. This is the case for both GPs that are investing into private companies and LPs that are investing into GPs.

The Private Equity industry is structured through funds that GPs (the investment team) will raise with their LPs (Limited Partners which are the institutions or individuals that will provide funds to the investment team).

Most funds have a 10-year lifespan. The life of the fund is divided into two c. 5-year periods: the investment period and the exit period.

During the investment period, GPs will make capital calls to their LPs that will wire them the funds to invest into companies.

During the exit period, GPs will distribute funds to their LPs when they sell their companies.

LPs get the full return on their investments only at the end of the fund’s lifespan. Before that, there are only partial liquidity events. Without secondary markets, it’s impossible for an LP to cash out its position into a GP before the end of the fund.

The infamous J-Curve illustrating the evolution of capital calls and distributions during the lifespan of a fund

A secondary transaction happens when an private equity investor sells its stake in a fund interest or in a direct interest to a third party. There are two main categories of secondary transactions:

A LP selling its stake in one or several private equity fund.

A GP selling its stake in one or several companies he invested into.

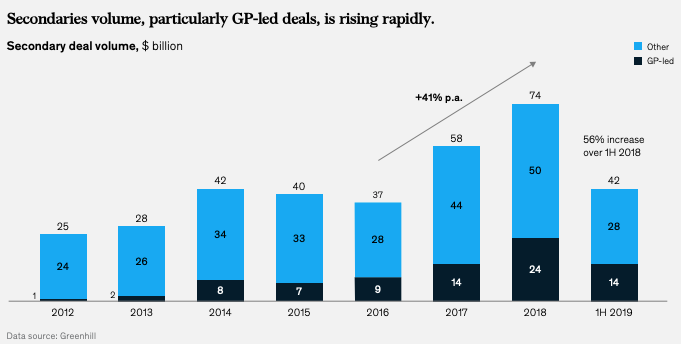

The secondary market is one of the fastest growing asset class in the private equity market with transactions volumes jumping from $2bn in 2002 to $74bn in 2018.

The funds involved in the secondary markets are serious players raising multi-billion funds (e.g. Ardian and Lexington are both currently raising a $12bn fund).

Secondary funds are outperforming other private capital funds both in terms of IRR and in terms of multiples. The main reasons are (i) shorter holding periods, (ii) discounts negotiated at entry, (iii) less competition in the secondary market.

Secondary funds are bringing liquidity to the private equity market but also more sophistication and creativity to answer the specific needs of investors in the private equity asset class. You have to keep in mind that private equity funds are also customer-driven businesses. Their customers are their LPs which have evolving needs and which are continuously raising the bar to pick the funds they want to invest in. Using secondaries markets or raising a secondary fund is a way for them to be more customer driven.

Secondary funds allow LPs to shift their investment strategy and/or to rebalance their portfolio exposure (in terms of geography, sector, sub-asset class, liquidity horizon, vintages etc.) more rapidly.

Secondary funds allow LPs to sell their stake opportunistically when the demand is high. Usually buying an asset in a secondary sale comes with a discount compared to its Net Asset Value (NAV). But sometimes when the underlying companies in the fund deliver promising performances, buyers could be willing to pay a premium to the NAV.

Investors in secondary funds have access to a different risk-reward profile compared to other asset classes in the private equity market: (i) the J-curve is mitigated because the cash will be returned earlier to investors, (ii) a vintage diversification, (iii) an easier access to tier one funds portfolio.

Secondary transactions could allow an LP to become a long term investor into a tier-one usually inaccessible GP. LP could be willing to acquire a secondary stake into a fund managed by a famous VC to be able to save its spot to invest in the next fund raised by this VC. I guess that it could be a good way to invest in funds like USV or Benchmark which have refused to increase the size of their funds over the years reducing the opportunity for new LPs to become investors in their funds.

Obviously, secondary funds also have outstanding returns - even compared to the other asset classes in the private equity market (as seen in the previous section).

Secondary sales are no longer synonymous with distressed sales. In its early days, secondary sales were often badly perceived by both GPs and LPs. It was most of the time the sign of the end of the relationship between the GP and the LP. If an LP was selling its stake into a GP, the GP could either consider the LP as a distressed investor not able to invest in its future funds or as an investor who lost confidence in its ability to manage funds.

An increasing number of GPs are raising funds for secondary transactions with a specialization in niche strategies. Private equity is a rich asset class with numerous subsegments offering almost endless possibilities to fund managers wanting to raise a secondary fund. For instance, Blackstone has launched in the past decade a secondary activity under the brand Strategic Partners and is now managing dedicated funds for the infrastructure and the real estate sectors.

Secondary funds are increasingly used by GPs to have more flexibility to manage their funds. For instance, they could (i) terminate their fund in advance to facilitate the fundraising of a new fund, (ii) extend the duration of their fund with new or existing LPs to extract more value from their portfolio companies, (iii) sell an old dated fund that has passed its life duration.

Venture Capital is an asset class of the Private Equity market and is facing the same illiquidity issue. This issue is even more prevalent because (i) the holding period in Venture Capital tends to be much longer than in leverage buyouts (5-10y vs. 3-5y) and (i) you have many more different parties around the table with founders, several VC investors and employees incentivized through stock options (not just a majority shareholder and the top management like in leverage buyout deals).

At a startup level, there are three common liquidity issues:

Founders wanting to cash out part of their stock to have a minimum financial security

Early employees who are leaving the company and have to exercise their stocks options

Business angels or early stage funds that are looking for liquidity

There are three possibilities to sell shares into a secondary sale: (i) a discrete sale between two financial rounds, (ii) a tender offer in which the main shareholders fix a valuation to the company and let all the smaller shareholders the possibility to sell their shares to external parties, (iii) a secondary sale at the same time that a new round of financing (most common scenario).

At a fund level, you have the same liquidity issues than in other private equity asset classes (fund termination, LPs seeking liquidity, fund extension etc.). Behind buyout, Venture Capital is the 2nd private equity class that investors are the most willing to divest in the next 12-24 months (H2-2019 data).

There are two growing trends in the secondary market for VC-backed assets. First, the rise of dedicated funds for secondary investments directly into startups to cash out (i) founders, (ii) early employees or (iii) early investors. The best example in Europe is Balderton with its €150m Liquidity Fund I announced in Oct. 2018. It’s a smart move because the European ecosystem needs secondary options to become more mature. It’s a way to accelerate the flywheel in which cash-out and knowledge are re-injected into the ecosystem to make it grow faster. Balderton has already invested into 9 companies (including 6 not in their venture portfolio). I guess that adding Balderton to your investor base through a secondary sales is an appealing value proposition for numerous European founders. Here are some key information about the fund:

The fund can invest up to €10m per company at Series C stage or beyond and is looking for the following company characteristics: well financed, proven business model with a clear path to profitability, strong growth. The idea is to avoid any loss in the portfolio.

In terms of valuation, sellers should expect to have their shares bought at a discount compared to the last valuation mark (10-20%) especially when you are selling common shares which have less associated shareholder rights compared to preferred shares.

They recommend founders to cash-out 10-15% of their stake. More could be perceived as a too negative signal and could break the alignments of incentives between founders and other shareholders.

Second, in Venture Capital (especially in Europe), there is a strong disequilibrium between the capital deployed and the number of exits. As a result, numerous VC funds have an increasing and ageing unrealized net asset value under management. The pressure to distribute capital to LPs is growing especially since the end of the funds are getting closer. Some VCs are exiting part or all their investment into their most successful companies (e.g. Serena during the last round of Dataiku). Other are using secondary sales to exit all their investments in a single transactions (e.g. New Enterprise Associates, Nordic Capital, Battery Ventures, TPG).

🔎Global Private Markets Review 2020 (McKinsey, Feb. 2020)

🔎Private Markets Come of Age (McKinsey, Feb. 2019)

🔎Secondary Market H1-2019 (Preqin, 2019)

🔎Growth of and Trends in the Private Equity Secondaries Market (Hogan Lovells, Oct. 2019)

Thanks to Julia for the feedback! 🙏

I would love to have a chat with you if you are actively involved in this secondary market (as a GP trying to exit a fund through a secondary transaction, as a GP managing a secondary fund or as a LP trying to exit positions through a secondary sale). Drop me an email at ade@idinvest.com

See you next week for another issue! 👋