🛍 Buy Now, Pay Later Solutions are Going Direct to Consumer

Overlooked #53

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, with Maxime, we dig into the buy now, pay later market. More specifically, we look at the rationale for Affirm, Afterpay and Klarna to build a mobile app and go direct to consumer.

The buy now, pay later (BNPL) market is booming with three companies started on three different continents leading the charge:

Klarna: based in Sweden which has become the second largest Europe VC-backed private company after a $650m round in September 2020 valuing the company at a $10bn pre-money valuation.

Afterpay: based in Australia which has been listed since 2016 and has now a market cap above $20bn.

Affirm: based in the US which started its public journey last week and is now valued above $25bn.

BNPL solutions let customers pay in instalments over time. For instance, instead of buying upfront your Peloton's bike for Christmas, you will use Affirm to split the payment overtime. You will not pay $1,895 upfront, but you will make $49 monthly payment. Peloton will be paid upfront and Affirm will take a cut on the purchase, as any credit car provider would do. For the customer, it makes the cost affordable and comparable to a gym subscription. For Peloton, it increases its conversion rate and expands its Total Addressable Market (TAM) to target more price sensitive customers.

BNPL players are riding two trends: the rise of ecommerce and the decline of credit cards (esp. in the US). Consumers (particularly younger generations) are more willing to make online purchases and have a stronger aversion to debt (in the US, only 1/3 of Americans between 18 and 29 year-old have a credit card).

Klarna, Affirm and Afterpay are all based on a business model innovation compared to credit cards. Instead of generating revenues on late fees when customers are misbehaving, BNPL solutions are generating most of their revenues from merchants. As a result, incentives are realigned between customers and their financial service providers.

BNPL solutions all went to market through a B2B2C go to market. Their initial objective was to sign as many merchants as possible to have their instalment payment solution inserted into the checkout flow. The acquisition of merchants was sufficient to drive the initial usage of the service by end customers.

But now BNPL players are all going direct to consumers through B2C mobile apps. By doing so, they have an opportunity to have a much bigger impact into both consumer finance (becoming another “lateral neobank” like Revolut, Dave or Swile) and ecommerce (becoming a contender to Shopify and Instagram Shopping).

Initial Model - B2B2C Go to Market

I believe that understanding BNPL solutions as marketplaces gives a good framework to understand their initial growth. To kickstart a marketplace, you need to identify whether you are supply (e-commerce merchants) or demand (B2C customers) constrained. BNPL solutions understood that they were supply constrained and that signing massively e-commerce merchants would be sufficient to drive the initial demand for their services.

BNPL solutions went to market by setting-up both a self-service version of the product (e.g. an API or a plugin on e-commerce platforms like Shopify) and a sales team to convince merchants to add the solution to their checkout. They came with a strong value proposition: it's just another option that you will add to your payment flow that could bring you many benefits including:

An increased average order value (AOV). For instance, merchants using Affirm reports a 85% higher AOVs when customers use the solution over other payment methods. Afterpay also reports a 25% uplift in order size.

An increased conversion rate. For instance, Afterpay reports a 20% uplift in conversion rate.

An increased repeat. For instance, 20% of Affirm users from the January 2019 did another purchase from the same merchant in the next 12 months following their initial purchase. In Australia and New Zeland, Afterpay's core users (top 10% customers) on average will use the solution 54 times per year across 26 different merchants and 11 different verticals.

An increased addressable market by addressing the population that did not have the budget to pay upfront for expensive items but can do so responsibly by splitting the payment overtime.

BNPL solutions have implemented specific strategies that have been game changer to fuel their growth:

Klarna opened its cap table to key partners to drive acquisition: H&M to have them as a merchant and Snoop Dogg to help them promote the B2C app in the US,

Affirm has signed medium-term partnerships with Shopify and Peloton (28% of 2020 revenues) that have been game-changers to drive its topline growth.

Afterpay’s go to market has been mainly focused on the fashion & beauty category while competitors have addressed a wide variety of verticals (general merchandise, electronics, auto parts, etc.).

Affirm, Afterpay and Klarna have been impressive in their merchants acquisition strategy. Klarna has 235k merchants over the world. Affirm has 63.8k merchants and Afterpay 6.5k. As these three players have reached a certain scale in their respective core markets (Europe for Klarna, Australia and New Zeland for Afterpay and the US for Affirm), they are now adding a second D2C layer to their activity in order to (i) gain the US market which seems to be the holy grail, (ii) build differentiation against their peers, and (iii) expand their initial TAM by entering the consumer finance and ecommerce marketplace categories.

New Model - Going D2C - Powered by App Fuel

App Fuel is the inspiration station for app builders. It gives you the playbooks to build successful mobile apps through three formats: (i) users flows to browse through our collection of the best patterns from real apps, (ii) a library of app screens to get UI inspiration from top-ranked apps and newcomers as well as (iii) business cases to help you to improve your acquisition, usage, retention and monetization! ⛽️

The three leading BNPL players have all released a mobile app to add a D2C layer to their activity. They are adding B2C features and services that we break down into four categories:

Personalised marketplaces,

Fast checkouts,

Loyalty and cashback solutions,

Adding adjacent financial services.

1/ Personalised Marketplaces

First, Affirm, Afterpay and Klarna are building a personalised marketplace to shop and pay products with their instalment solution directly from their mobile app. They want to control the full experience from inspiration to checkout and delivery.

For instance, Klarna has an inspiration section in its navigation bar. The first time you open it, Klarna asks your favorite brands and shopping categories. Then, you will access to a personalised feed with shopping guides, special deals and seasonal content (e.g. find the perfect gift for Christmas). This feed will get more relevant overtime as you shop with Klarna and interact with the inspiration section.

When you want to purchase an item, Klarna will embed the merchant’s website in the app. You will have to restart the shopping journey and at checkout you will be able to pay with Klarna either by generating a virtual card or by logging in with your Klarna account. It's still a deceptive experience for the user. You would expect a more native shopping experience directly into the Klarna app.

Our guess is that all these BNPL players will tend towards a user experience that is similar to Instagram Shopping. They will own the shopping journey from end to end. Moreover, you will never have to open any browser page to complete your purchase.

2/ Fast checkouts

An intermediary step to enhance the shopping experience would be to implement a user flow similar to Shop App. It's the Shopify App to track your parcels from Shopify merchants, to manage your Shop pay account and to get inspiration for your next purchase. In the Shop App, the shopping experience is also done in a browser embedded in the app but Shopify is using shortcut at checkout with its one-click Shop Pay button.

With this kind of button on merchants' shopping cart page, BNPL are likely to develop fast checkout product features within their app. BNPL would then handle the entire checkout flow. There is surely value to capture here - see Prime by Amazon, Fast or Dashlane on another vertical.

3/ Loyalty & Cashback

Cashback is a crowded market with various product types (web extensions & widgets, bank programs, apps). Newcomers are mobile-first fintech companies. They reward everyday purchases, transforming any bank card into a multi-brand loyalty card. For each sale, the merchant pays a commission to the cashback provider which is then shared with the users. Consumers are rewarded automatically, without changing their habits, with direct cashback on their bank account.

One opportunity for BNPL players is to take part in the loyalty business, which is driven by merchant network size and transaction volumes. They have several options to get there:

By creating in-house cashback solutions. One of the core businesses of BNPL companies is to build vast merchant networks. Furthermore, they already handle spending flows.

By partnering with existing providers. There are measurable synergies between their respective networks, customer usage & app retention stakes. As an example, Joko claims to have 500,000+ users in France and already partnered with 1,000+ merchants.

By acquiring such companies.

4/ Adding Adjacent Financial Services

Last, BNPL leaders are all adding financial services to their offering to augment the lifetime value of their users by increasing their retention and generating more value per user.

They all started by emitting virtual cards to let shoppers pay through instalments merchants that don't support them yet. For instance, if you can buy your new Mac in instalments even if Apple is not supporting BNPL solutions. You will generate a virtual card to pay for the product and you will pay back in instalments the BNPL provider over time.

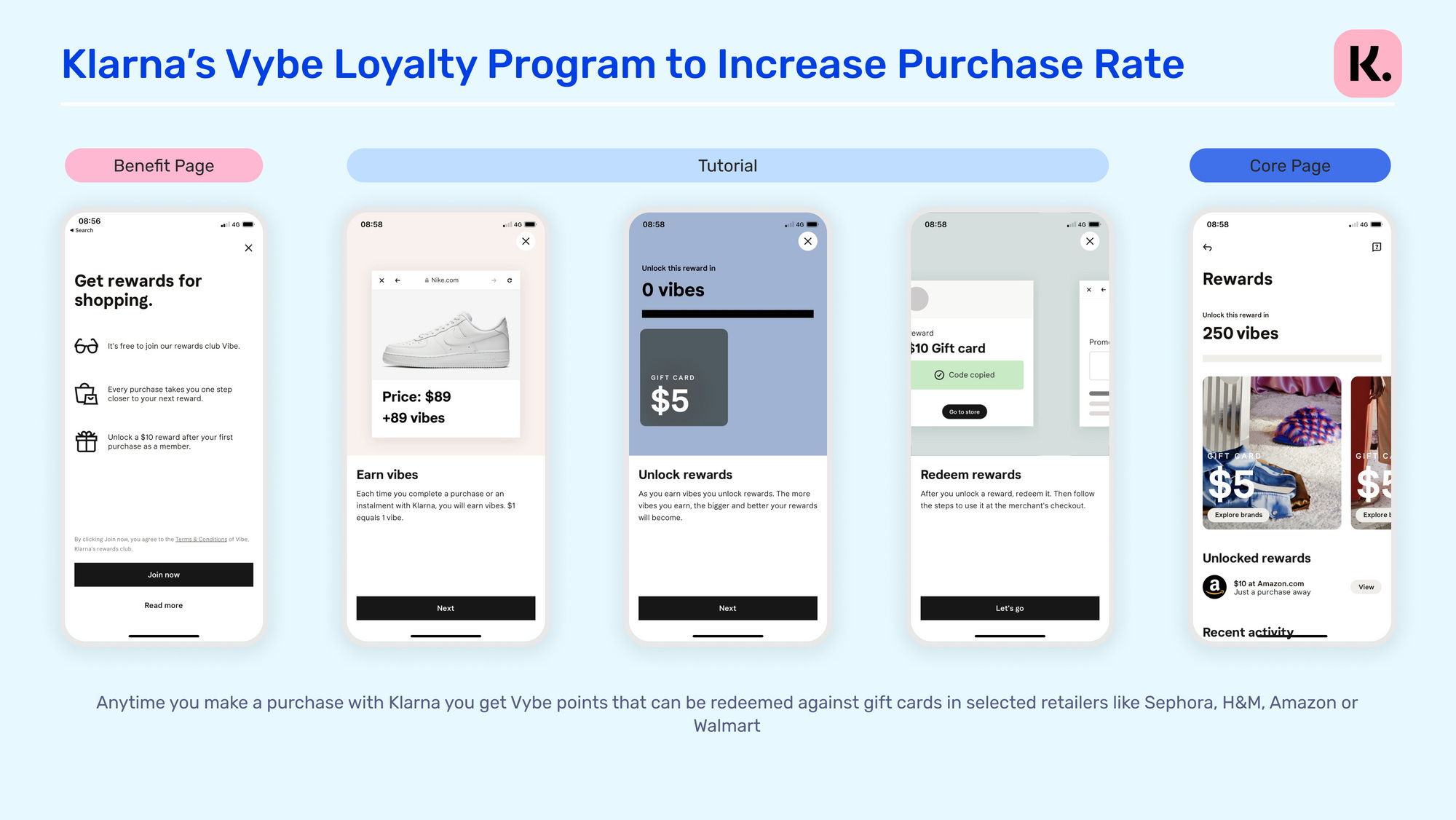

Klarna and Afterpay have added a loyalty program to get rewarded if you purchase more through their solution and if you behave correctly as a borrower. Klarna's loyalty program is called Vybe. Anytime you make a purchase with Klarna you get Vybe points that can be redeemed against gift cards in selected retailers like Sephora, H&M, Amazon or Walmart. Afterpay's loyalty program is called Pulse. It's not a pay-per-points program. It's a status that you will access when you make 30+ purchases over a six month period and you have less than 3 late payments in this cycle. You will get access to special features (reschedule an upcoming payment, pay $0 up front) as well as gift cards and special offers.

Affirm, Klarna and Afterpay have also added saving tools in their application. The basic layer is that you can view and manage all your instalment payments in a single place. Building on this, Affirm launched in 2020 an interest bearing saving account and Afterpay partnered with Westpac's banking as a service digital platform to offer money management services starting with savings and budgeting tools.

Klarna has gone one step further by launching a branded debit card and saving accounts in Germany and Sweden. In October, the company has issued 0.5m cards in these two countries. The company also obtained a fully regulated licence in 2017.

In the end, we believe that BNPL players are what we called "lateral neo-banks." We have a strong thesis that the winners in the neo-banking market will be players that will not start as neo-banks but will become ones overtime. It's too hard to win this market without a distribution hack and without addressing a sufficient number of transactions. Revolut was the first and most successful lateral neobank starting with FX for travellers before becoming a neo-bank and now building a one stop shop financial app. But we have other contenders in this category including Swile in France (meal-vouchers and other employee benefits) and Dave in the US (instant loans).

Thanks to Julia and Maxime for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋