📚 A Step by Step Guide to Raise a Series A

Overlooked #116

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing a step by step guide on how to raise a series A.

When asked for advice on preparing a series A roadshow, I used to share a long list of articles and generic best practices. In the past couple of months, with Roméo, we took the time to read and watch everything we could on raising a series as well as to gather the best practices we learnt in our job.

As a result, we’ve crafted the 1st iteration of a step-by-step guide to raise a series A. We tried to make it exhaustive and illustrative with real deck examples. we hope that you’ll enjoy it. We’d love to have your feedback to bring it to the next level (e.g. you feel something is missing or you’ve a better illustration for a certain argument).

On this topic, we’re doing an event on Thursday evening in partnership with SISTA for female founders in our office to talk about fundraising. You have more information here and if you want to join, you can send me an email at adewez@eurazeo.com.

We divided the paper into 2 sections:

Prepare your deck with advice on how to address the main topics (pain point, solution, why now, execution, vision, etc.)

Run your fundraising process (active vs. passive fundraising modes, preparing your list of potential investors and reaching out to them, running the process, etc.)

Part I - Prepare Your Deck

There is no such thing as a unique and standardised deck format. We even believe that the best decks are the ones which are able to tell a singular storyline. However, across decks, there are recurring sections and best practices on how to handle them.

Before working on a slide deck, a good practice is to do a brainstorming session on a whiteboard to break down your business into pieces answering questions like: what are my unique moats? what are the pros and weaknesses of my case? what are the key parts of my business? what have I achieved since inception and in the last 12-18 months? what do I want to achieve in the next 12-18 months and in the long term?

Once you’ve done this brainstorming session, you can draft a memo with the storyline that you want to pitch to investor. In this way, you will be able to tell a unique story and avoid the constraints of a standardised deck with scholar sections expected by investors. In your memo, you will be able to convert every section into a slide.

A- Executive Summary

You can start you pitch deck by highlighting the 4-5 core strengths of your company that you’ll have identified during your brainstorming session and while writing the outline of the story you want to tell.

B - The Triptych: Why Now? What Problem? What Solution?

1/ Why Now?

You should demonstrate that there is a market pull towards what you’re building, that there is currently a unique momentum to build your company. The market is craving the solution that you’re building and it will be easier for you to sell your product to customers.

You need to answer the following question: why will your product have a perfect product market fit right now - not within two years and not two years ago?

The more precise your answer is in terms of specific trends and in terms of timeline duration, the stronger your case is. For instance, Sunday has a compelling why now: with covid-19 QR-code have become mainstream for consumers and restaurants struggling to survive are keen to implement anything to increase their margins. The timeline is short: covid-19. The trends are specific: QR-code going mainstream and restaurants on the verge of bankruptcy.

Below is a list of potential candidates for a good “why now”:

Macro-trends: shift towards cloud, increasing concerns around sustainability, rising inflation, etc.

Tech trends: rise of freelance, rise of creators, remote working, etc.

New rising platforms: iPhone, web 3.0, Shopify, etc.

Technological breakthroughs: computer vision, NLP, etc.

b/ What Problem?

You should explain that there is something wrong with the current state of the world. A great way to do it is to introduce your targeted persona and tell the key pain points that she had before discovering your product. You want the investor to put himself in the shoes of your persona and to feel horrified by the life she has.

“Payer au restaurant ca fait chier tout le monde. C’est un cauchemar. Mais personne ne s’en est jamais plaint parce qu’on nous n’avait dit qu’il y avait une alternative. [...] On lève le bras. On se casse l’épaule. On arrête de parler pendant 3 minutes le temps que le serveur nous voit. [...] On a tous vécu ça et on vit tous ça quand on va au restaurant. Le serveur arrive. Puis on lui demande l’addition. Il dit bien sûr et part chercher l’addition. Mais entre temps la table d’à côté demande du vin et celle d’encore à côté son steak tartare. Il revient 5 minutes plus tard avec l’addition et là on lui demande si on peut avoir la machine. Il répond encore “bien sûr” et il se repasse 5 minutes.” - Victor Lugger (CEO at Sunday), GDIY (🇫🇷)

"What the hell do you know about used cars? The simple answer that I give is that I'm a consumer, I'm a customer of the business that I'm building. I'm the guy who has historically travelled 50 miles to go look at a car, to buy it, to decide not to buy it and waste half a day. Consumer businesses are the easiest to understand and to add value to because I'm the customer. As a result, if it's a problem that I try to solve for myself, I imagine that it's a problem other people are having too.” - Alex Chesterman (CEO at Cazoo), Riding with Unicorns

“It all started one Christmas, when Frédéric wanted to get home to his family in the French countryside. He had no car. The trains were full. The roads, too, were full of people driving home, alone in their car. It occurred to him that he should try and find one of the drivers going his way and offer to share petrol costs in exchange for use of an empty seat. He thought he could do it online, but no such site existed.” - Frédéric Mazella (CEO at Blablacar), Accel

Other problem’s examples include:

Qonto (neobank for startups): long, tedious and expensive process to open a new bank account

Uber (ride-hailing app): uncertainties around ordering a cab on the street on the possibility to find a cab, on the time to get to your destination and on the price to pay

Backmarket (marketplace for refurbished electronics): uncertainties on the second hand items bought on generalist marketplaces like Ebay with no guarantee on product quality

c/ What Solution?

You should introduce your solution with a simple sentence and you should highlight 2-3 key attributes that answered the pain points previously mentioned. You can resume the story of your persona by telling how your solution has improved his live with qualitative and quantitative data.

In this section, you should answer the following questions:

Who are the personas that you’re targeting in the organisation - users, beneficiaries and buyers?

How is your product being used? What are the main use cases? What has changed in the workflow of your user (workflow before and after using your product)?

What are the main benefits of your products (time gains, revenues generation, cost cutting)?

To prepare this section, you can make a table with your different personas, your use cases and the main product’s benefits.

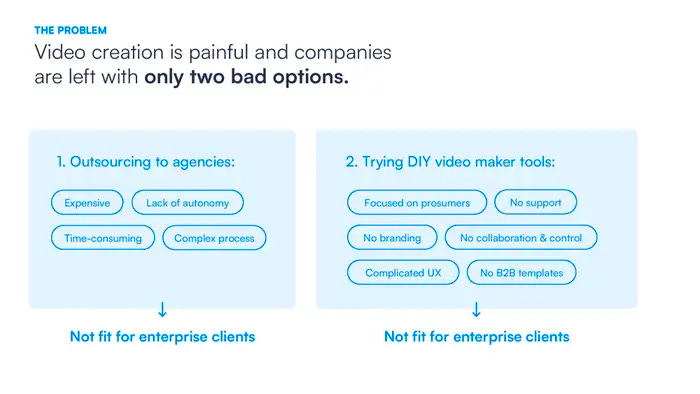

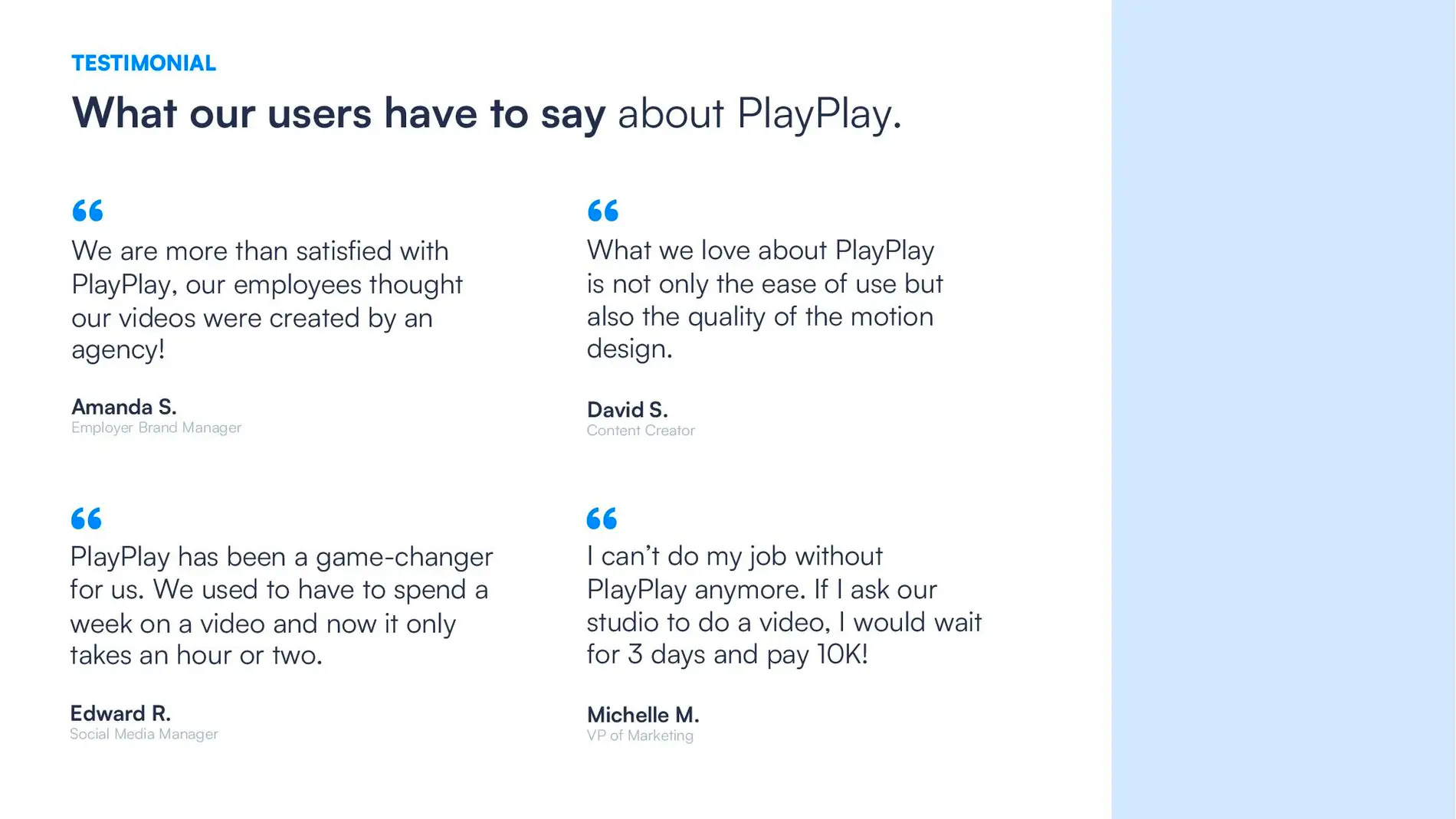

On (1), you should describe the 2-3 main personas who will be power users of your product. For instance, PlayPlay democratize communication which was a topic usually reserved to the communication/marketing department to all the functions in the organisation (finance, HR, sales, etc.). You can resume the story of your persona by telling how your solution has improved his life

On (2), you can talk about how your product is most frequently used. For instance, Pennylane is an all-in-one accounting and financial hub for SMBs. It has the following use cases: book-keeping, cash monitoring, accounts payable & accounts receivable, automated quotes.

On (3), you can introduce the 3-4 largest benefits of your product. You should highlight the benefits with quantitative and qualitative data. For instance: CFO saved x hours per month using Pennylane, merchants using Alma increased their conversion by y% and their AOV by z%.

d/ PlayPlay’s Series B Deck Example

C - Market & Competition

1/ Market

In this section, you need (i) to size your market, (ii) to discuss the future evolution of the market and (iii) to present the main characteristics of your market. As a rule of thumb, VCs want to invest in large and attractive enough markets to reasonably build a $100m gross margin business (with the rationale that a $100m gross margin business will often be a $1bn valuation business).

Reasonably means that you should reach this threshold without having to capture 100% of the market. Most of the times, it means that you should be there with a market share below 10-15% (implying a $0.7-1bn market). If your business has winner takes all dynamics (e.g. a marketplace or a vertical SaaS), this figure can be increased to 30-40% (implying a $250-350m market).

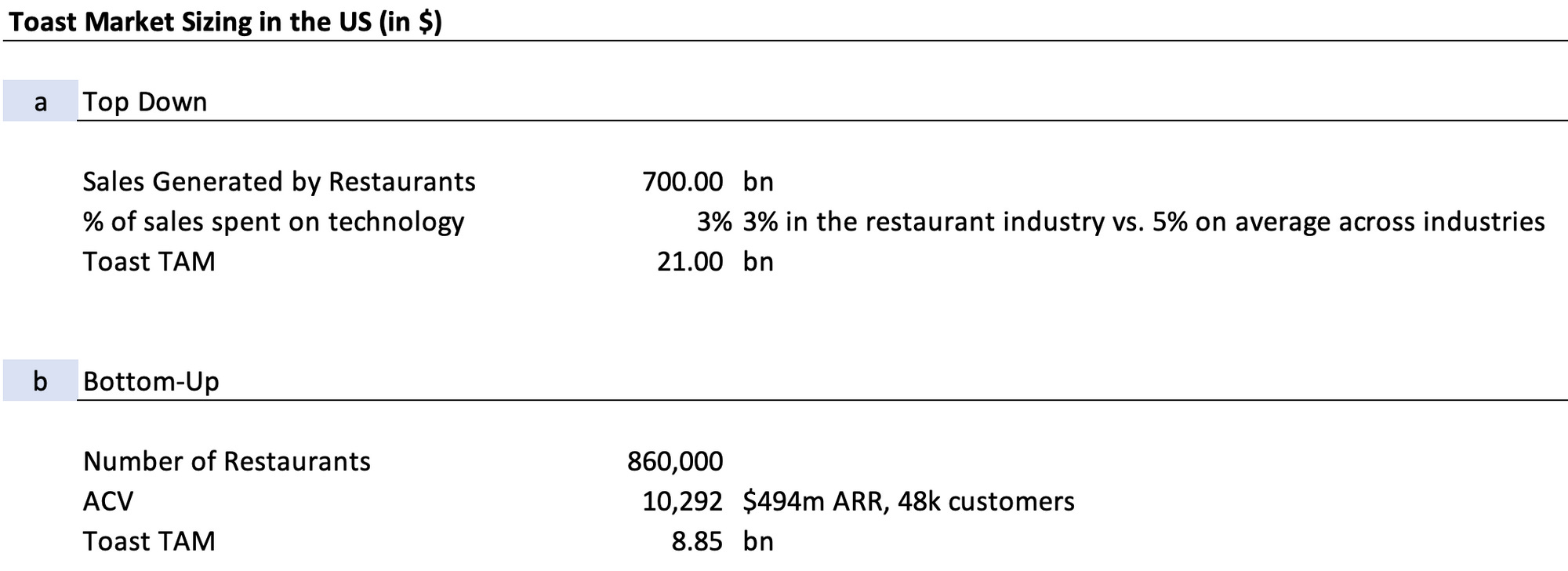

To size your market, you have 2 approaches:

Top-down approach: you start with general industry figures and you break them down until you reach a realistic subset of the market in which you’re operating.

Bottom-up approach: you multiply the number of customers in your different segments in the geography in which you operate by their potential potential ACV.

It’s better to present the bottom-up market sizing which is easier to rationalise. Besides your TAM in your core market (i.e. in the geography in which you operate and with the product that you have today), it’s also worth sharing your future TAM when you will have expanded into new geographies and when you will have expanded your ACV (with new product features, new revenue streams, etc.).

You should also discuss the evolution of the market that you’re addressing answering questions like: is it a growing or shrinking market? what are the main drivers behind the market’s growth? how would you segment your market?

Porter’s five forces model is a good framework to evaluate the key characteristics of your market. You can evaluate successfully the different forces at play in a market: (i) bargaining power of buyers, (ii) bargaining power of suppliers, (iii) threat of new entrants, (iv) threat of substitutes, (v) rivalry amongst existing competitors (cf. infra). While presenting your market, you can highlight 2-3 characteristics that make it specifically attractive.

2/ Competition

Don’t show a 2x2 matrix in which you’re at the top right but show a broader illustration of the ecosystem in which you’re evolving (direct/indirect competition, substitute/status quo).

When you talk about direct competitors, a good practice is to have a table with a comparison on 5-7 criteria (e.g. foundation date, amount raised, FTEs, revenues, geography targeted, key differences in terms of features, go to market strategy, etc.)

D - Traction

When you’re raising a series A, you should demonstrate that (i) you have reached product market fit and (ii) you’re growing exponentially.

1/ Usage: You Have a Strong Product Market Fit

You should demonstrate how much your customer use / love your product with 3 categories of metrics: (i) low gross churn rate / negative net churn rate, (ii) high usage of your solution (e.g. amount of time spent per day for a social media or a game) and (iii) strong qualitiative customer satisfaction (high NPS, survey results).

2/ Growth: You’re Growing Exponentially

For most startups, growth is judged by the velocity at which the north star KPI is increasing (e.g. ARR for SaaS, GMV and take rate for marketplaces, DAUs & MAUs for social apps).

To raise, it’s more crucial to show that you’re able to grow consistently (over 3-6 months) at a 10-30% monthly growth rate than to hit an absolute number on your north start KPI (e.g. $1m ARR).

To be in the best conditions to raise a series A, you should show that you’re growing at more than 3x YoY. If your startup is not reaching that target, try to redefine your north star or a given perimeter of the north star metric such that it does. For example, focus on the part of your customer base growing at this rate.

In parallel, it’s important to demonstrate that your distribution engine is ready to scale and just need fuel to keep growing at an exponential rate. It means that you should be able to describe your go to market motion and explain where you will invest additional capital (sales & marketing people, paying acquisition channels) to sustain growth.

3/ Bonus

In its series A deck, Airbyte has an incredible slide where it demonstrates its execution speed.

E - Team

The objective of this section is to demonstrate that founders (i) are uniquely positioned to solve the problem they’re tackling and (ii) have a strong ability to hire top talents.

For (i), investors will look for previous relevant experiences in the industry or in the key success factors of the business:

Stanislas brought to Doctolib his field sales experience from The Fork

Jacques brought to Jow his content/media expertise from Canal+

Victor is building Sunday on the back of his experience of building BigMamma’s chain of restaurants

On your team slide, you should prioritize quantifiable achievements in your past achievements over logos and generic roles. You can also include in your appendixes a 12-18 month hiring plan with key profiles in your pipeline.

F - Vision

You should end your pitch by underlying the vision that you have for your company. You’ve spent the past minutes building credibility with your interlocutor to show that you’re tackling a real pain point, that you’re going after a large market, that your team is uniquely positioned to win the market and that you’re super strong in execution.

Now, it’s time to make your investor dream about what your company could become. The best founders are the ones who are able to both articulate (i) how straightforward the next 12-18 months will be articulated and (ii) how your company has a big vision for the mid to long term with unlimited upside.

Part II - Raise Capital

A - Active vs. Passive Fundraising Modes

We could distinguish two fundraising modes:

Active fundraising: you’re spending most of your time raising capital. You have meetings with investors, you spend time answering their due diligence requests and improving your deck/pitch based on the feedback you receive. Once you’re well prepared and you’ve a strong case to pitch, you could raise a round from first meetings to term sheets in 1-2 months.

Passive fundraising: you’re focused on building and growing your company. You decline most introduction requests from investors and you just cultivate a relationship with a reduced number of potential ideal investors.

After raising your seed round, you should spend some time shortlisting c.5 partners in funds who could be a perfect fit to lead your next round. You should find a way to meet them and start building a relationship by updating them on your progresses every 3-6 months. It will help you to remain top of mind for them and it will create momentum once you officially launch your funding process because these partners will tend to move faster than other investors.

B - When to Start Fundraising?

You shouldn’t start fundraising when you’re 6-month away from running out of cash but when you’ve the highest leverage to raise capital. Leverage can come from different mediums: a strong commercial traction, a key shift in your market, the achievement of the objectives that you’ve set during your seed round, etc.

C - Preparing Before Going into Active Fundraising Mode

You should run your fundraising process as a sales process. Investors are leads that should move into a sales funnel with key steps: contact to be established, contacting phase, 1st meeting planned, 1st meeting done, due diligence, partner meeting, waiting for term sheet, offer received, declined. You can create a master document (on Google Sheets, Airtable, Notion or your CRM) to track your process.

Make an exhaustive list of VCs that could invest in your series A. You have 3 criteria that you should check: (i) they invest in the domain in which you’re operating, (ii) their average ticket size matches the amount that you’re raising, and (iii) they did not invest in any competitor.

Rank your investors into tiers (tier 1 with your top 5 picks, tier 2 with your top 5-15 picks and tier 3 with other investors).

Identify the best person to reach out to in the fund. The more senior and knowledgeable about your space the interlocutor is, the better.

Before officially kickstarting your fundraising, you can do a rehearsal. You have two options. You can either practice (i) with your current investors, seed investors and entrepreneurs or (ii) with 2-3 investors in your tier-3 bucket. You should use these meetings to practice your pitch and gather initial feedbacks on your deck and on your pitch.

D - Fundraising

You should run your fundraising in waves. You should always have open conversations with 5-10 investors. It’s sufficient to have momentum in your round while having the time to run a smooth process with these funds.

To kickstart your fundraising, you can start by contacting the c.5 partners with whom you’ve built a relationship in the past few months. You can add another 5 investors high in your list. You should try to pack all first meetings in a 10-day timeline to be sure that everyone starts and move at the same pace. When investors drop, add new investors from your list.

To contact an investor, you should try to have an introduction and use cold emailing as last recourse. It’s a silly coutume in venture and I believe that a good cold email should be sufficient to get the attention of investors. But as the industry works like this, find an introduction.

Three types of individuals can make you an introduction: (i) a VC or business angel who invested in your previous round, (ii) an operator or an entrepreneur who knows the VC you’re trying to reach or (iii) an expert who is recognised in your space.

During the process, note (i) all the relevant questions asked by investors during your meetings as well as (ii) all the reasons why they’re passing on the opportunity. Work on answering them and don’t hesitate to make changes to your deck and pitch to better address them.

E - Closing Investors

You should also try to gather your partners meetings into a 1-2 weeks period. You want all your advanced leads to be in a position to send you a term-sheet more or less at the same time.

When you have a partner meeting planned, it means an investor is ready to push your company in front of his whole partnership. You should work hand in hand with him to prepare the partner meeting. Have a preparation call in which you discuss the key topics that you should focus on to convince the whole partnership.

Ask investors to give you a detailed term-sheet with economic terms (obviously) but also key legal terms to prepare the shareholder agreement.

Once you’ve received a term sheet from an investor that you like, ask him to send you contact details from founders they’ve worked with and that you can call to check their references.

Bibliography

How to raise a seed round? (Elizabeth Yin, Mar. 22)

Writing a Business Plan (Sequoia)

Series A Deck Template (Creandum, Mar. 21)

How to Raise your Next Funding Round (Creandum, Nov. 19)

How to Build a Great Series A Pitch Deck (YC)

A playbook for fundraising (Lenny Rachitsky, Sep. 20)

How to Raise Money (Paul Graham, Sep. 2013)

Front Series A Deck (M. Collin, Aug. 2016)

Airbyte Series A Deck (John Lafleur, Jun. 2021)

What you need to raise a Series A (Ophelia Brown, Aug. 2018)

Set Yourself Up for Series A Pitch Success (Emergence Capital, Jan. 2020)

Storytelling for your Series A Fundraise with Andrew Lee (Garry Tan)

The Founder’s Guide to Raising a Series A Venture Financing (Justin Kan)

Guide to Raise a Series A (Kindred)

Process and Leverage in Fundraising (Aaron Harris)

Why meeting Bob matters? (Hampus Jakobsson)

Thanks to Roméo, Clément, Paul and Julia (🦒) for the feedback! Thanks for reading! See you next week for another issue! 👋