🇫🇷 French Tech Ecosystem - H1-2022 Update

Overlooked #119

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing an update on what happened in H1-2022 in the French tech ecosystem.

I’m sure that you’ve heard in the past couple of months that the global tech sector is under pressure. In the United States, both public and private markets are impacted. I wanted to spend some time measuring what’s happening in the French tech ecosystem. On paper, the ecosystem seems to be on track for q record year in 2022. In reality, micro-signals are showing that the tide is turning and there is a high probability that we’ll experience a slowdown in H2-22. Valuation adjustments are being made and we’re entering a new paradigm (poor market behaviours to disappear, unconventional investors are out, refocus on capital efficiency). The French tech ecosystem has strong fundamentals and I’m confident that it’s still a golden era for entrepreneurs to build startups and for investors to fund them.

Part I - The Global Tech Sector is Under Pressure

The global tech sector is under pressure mainly driven by (i) increasing interest rates (higher cost of capital impacting discount rates with a stronger impact on tech companies which generate most of their cash flows in a long-term future) and (ii) expectations of an upcoming economic recession. As a result:

In the US, the stock market is falling, with tech being more impacted than the S&P and “Covid stocks” (Zoom, Shopify, Affirm, Robinhood, DoorDash) and “asset heavy stocks” (e.g. Carvana, Opendoor) are even more impacted.

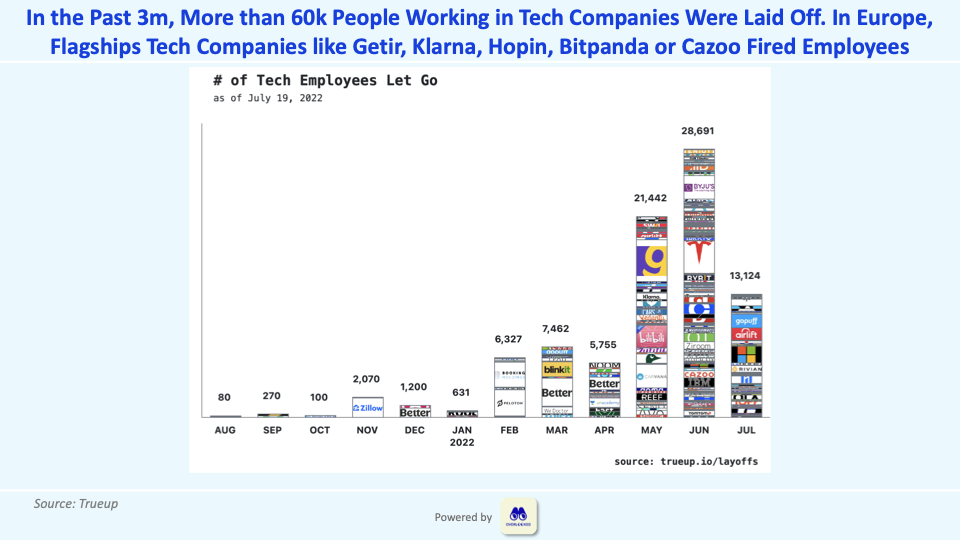

In the past 3 months, more than 60k people working in tech companies were laid off. It happened both in the US (Tesla, Better, GoPuff, Carvana, Peloton, Microsoft) and in Europe (Getir, Klarna, Hopin, Bitpanda, Cazoo).

Funding rounds in private markets are also impacted. We’re starting to see extreme cases like bankruptcies, self-repricing, downrounds and dirty term-sheets (using extreme financial protections to guarantee a minimum IRR).

Exits are massively slowing down. Most notably, the IPO window is now closed with 22 IPOs closed in H1-22 compared to 183 in 2021.

Part II - On Paper, 2022 is On Track to be a Record Year for the French Tech Ecosystem

On paper, the French ecosystem seems to continue its stellar growth trajectory.

The ecosystem had a record semester with €8.2bn raised in H1-22 across 441 transactions.

The French ecosystem has been more resilient than its European counterparts.

Foreign investors are still massively investing into French startups.

10 companies raised a round above $200m and 6 new unicorns were minted (Spendesk, Payfit, Front, Exotec, Ecovadis and Ankorstore).

Part III - In Reality, even in France, the Tide is Turning

In reality, we have early signals that the tide is turning. These signals have a high probability to be reflected in H2-22 funding data:

There is a double lagging effect. It takes 3-12 months for events to trickle down from the US to Europe and from the public market to the private market - starting with growth and ending with seed.

Recently listed French startups stock prices have plummeted (Believe, OVH, Made.com, Deezer).

Internal growth rounds (Doctolib, Electra, Akeneo, Pennylane) and top-up rounds are happening because new investors don’t want to fund companies at unadjusted valuations and internal investors want to make sure their best assets will survive a 24-36 months funding freeze.

Some French startups are starting to layoff employees (e.g. Sunday) and others are going bankrupt (e.g. Sigfox, Blade).

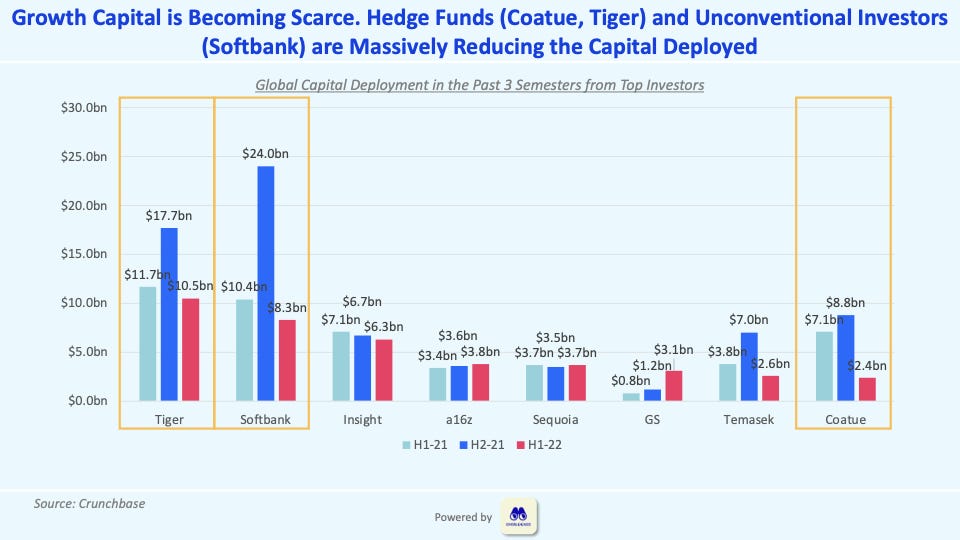

The annual capital influx for French startups is decreasing, driven by two factors: (i) unconventional investors (e.g. Softbank) or public/private investors (e.g. Tiger, Addition, Coatue) are allocating their capital elsewhere and (ii) VC will redeploy their funds in 3-4 years instead of 12-18 months like they used to do in the past 2-3 years.

Many rounds are not happening. Companies are failing to raise capital or are delaying their next fundraising to Q3-Q4 2022.

It will be extremely hard to raise capital in a Series B and onwards as long as valuations have not adjusted because nobody wants to catch a falling knife.

In Seed and Series A, variance is at all time high and should continue to increase as long as valuations have not adjusted.

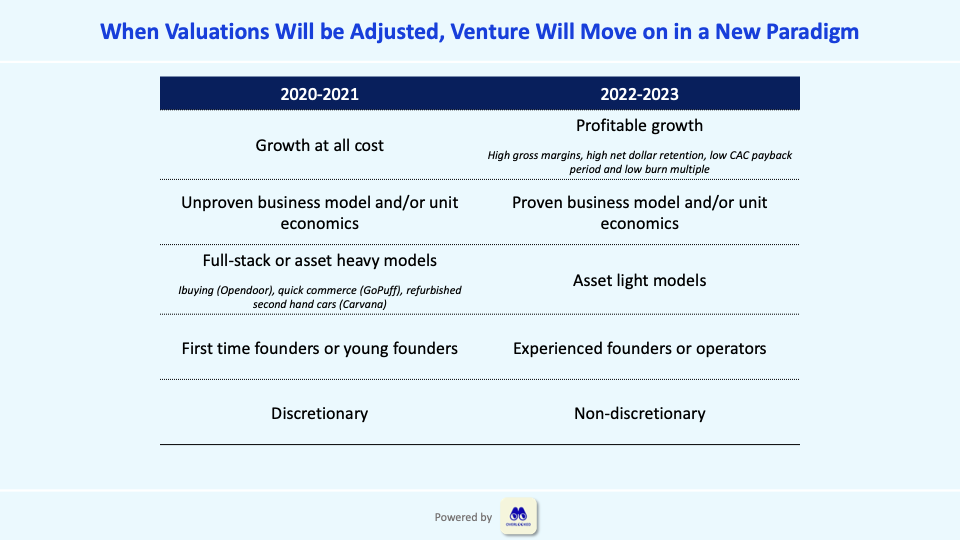

Part IV - We’re Entering a New Paradigm but I’m as Bullish as Ever on the French Tech Ecosystem

We’re entering a new paradigm but I’m bullish as ever on the French tech ecosystem. Valuations will adjust in the next 12-18 months (it will he harsh with bankruptcies, down-rounds, repricing, flat rounds or structured rounds with aggressive protections for new entrants) and the ecosystem will move on from there.

Poor market behaviours will disappear (short and shallow due diligences, back to back funding rounds, excessive founders cash out, no focus on unit economics).

The French tech flywheel is stronger than ever. Each new vintage of founders is more experienced and more ambitious with more and more serial entrepreneurs and experienced operators starting a new business. French startup mafias are growing. Experienced operators are starting to make a career in startups.

French funds have dry powder and there is a strong demand from foreign investors to invest in French startups.

Overall, investors are now looking for profitable growth, asset light models, experienced teams and downturn-resilient businesses.

Bonus - Noteworthy Trends for H1-2022

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Thanks for the update, it's great to see the European start-up scene starting to catch up to the US!